Investor Guide FY 2019

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

1.1.3 Helicopters

Information on the Company’s Activities / 1.1 Presentation of the Company 1.1.3 Helicopters Airbus Helicopters is a global leader in the civil and military The HIL programme, for which the Airbus Helicopters’ H160 rotorcraft market, offering one of the most complete and modern was selected in 2017, was initially scheduled for launch range of helicopters and related services. This product range in 2022 by the current military budget law. Launching the currently includes light single-engine, light twin-engine, medium programme earlier will enable delivery of the fi rst H160Ms to and medium-heavy rotorcraft, which are adaptable to all kinds of the French Armed Forces to be advanced to 2026. The H160 mission types based on customer needs. See “— 1.1.1 Overview” was designed to be a modular helicopter, enabling its military for an introduction to Airbus Helicopters. version, with a single platform, to perform missions ranging from commando infi ltration to air intercept, fi re support, and anti-ship warfare in order to meet the needs of the army, the Strategy navy and the air force through the HIL programme. The new fi ve-bladed H145 is on track for EASA and FAA Business Ambition certifi cation in 2020. To ensure these certifi cations, two fi ve- bladed prototypes have clocked more than 400 fl ight hours Airbus Helicopters continues to execute its ambition to lead the in extensive fl ight test campaigns in Germany, France, Spain, helicopter market, build end-to-end solutions and grow new Finland, and in South America. First deliveries of the new H145 VTOL businesses, while being fi nancially sound. -

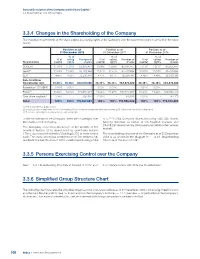

3.3.4 Changes in the Shareholding of the Company

General Description of the Company and its Share Capital / 3.3 Shareholdings and Voting Rights 3.3.4 Changes in the Shareholding of the Company The evolution in ownership of the share capital and voting rights of the Company over the past three years is set forth in the table below: Position as of Position as of Position as of 31 December 2018 31 December 2017 31 December 2016 % of % of % of % of voting Number of % of voting Number of % of voting Number of Shareholders capital rights shares capital rights shares capital rights shares SOGEPA 11.06% 11.06 % 85,835,477 11.08% 11.08% 85,835,477 11.11% 11.11% 85,835,477 GZBV(1) 11.04% 11.04 %85,709,82211.07% 11.07% 85,709,822 11.09% 11.09% 85,709,822 SEPI 4.16% 4.16 %32,330,381 4.17% 4.17% 32,330,381 4.18% 4.18% 32,330,381 Sub-total New Shareholder Agt. 26.26% 26.28% 203,875,680 26.32% 26.33% 203,875,680 26.38% 26.38% 203,875,680 Foundation “SOGEPA” 0.00% 0.00% 0 0.00% 0.00% - 0.00% 0.00% 0 Public(2) 73.66% 73.72% 571,855,277 73.66% 73.67% 570,550,857 73.60% 73.62% 568,853,019 Own share buyback(3) 0.08% - 636,924 0.02% - 129,525 0.02% - 184,170 Total 100% 100% 776,367,881 100% 100% 774,556,062 100% 100% 772,912,869 (1) KfW & other German public entities. -

Weapon System of Choice 38 New Eurofighter Typhoon Aircraft for the Luftwaffe 2021 · EUROFIGHTER WORLD 2021 · EUROFIGHTER WORLD 3

PROGRAMME NEWS & FEATURES JANUARY 2021 Chain Reaction Pilot Brief: Interoperability Eurofighter and FCAS Weapon System of Choice 38 new Eurofighter Typhoon aircraft for the Luftwaffe 2021 · EUROFIGHTER WORLD 2021 · EUROFIGHTER WORLD 3 Contents Programme News & Features January 2021 Welcome 4 Weapon System of Choice Airbus’ Head of Combat Aircraft Systems Kurt Rossner discusses the full implications of Germany’s decision to replace its existing Tranche 1 aircraft under the Quadriga programme. Cover: © Picture: images.art.design. GmbH, 12 Chain Reaction Lucas Westphal We speak to four businesses across Europe about the importance of the Eurofighter Typhoon programme for the Looking back, 2020 was a year few of us will ever The Eurofighter programme supports over 400 business- defence industry and the enriched technology capabilities forget. Because of the impact of the Covid-19 es across Europe, sustaining more than 100,000 jobs. it has helped bring about. pandemic we all faced huge professional and personal That’s why in this edition we shine the spotlight on some Eurofighter World is published by challenges. What stood out for me was the way every- of those supply chain businesses. Eurofighter Jagdflugzeug GmbH 18 Mission Future: Eurofighter and FCAS one involved in the Eurofighter project worked closer PR & Communications In the first of series of exclusive articles our experts exam- together than ever before to deliver. Elsewhere in the magazine we examine Eurofighter’s Am Söldnermoos 17, 85399 Hallbergmoos [email protected] ine Eurofighter’s place alongside a next generation fighter place alongside a next gen- in the future operating environment. Germany’s decision to replace eration fighter in the future Editorial Team Tony Garner its existing Tranche 1 aircraft battlespace. -

Investor Guide Value Drivers 2017

Airbus SE - Investor Guide Value Drivers 2017 Market Outlook Portfolio Highlights Investment Case . The world’s passenger air traffic is set to grow at 4.4% per year between A world leading manufacturer of aircraft in the category of 100 seats and more . products through continuous innovation (A320neo, A330neo, Market leading 2017 and 2036 supporting strong aircraft demand. Best-selling single-aisle – A320 Family with New Engine Option (neo) entry A350 XWB) . 34,899 new deliveries between 2017-2036 into service 2016. Backlog of 6,141 aircraft (December 2017) . Record backlog supporting ramp-up plans . Single-aisle: 71% of units, Wide-bodies: 54% of value . Versatile and complementary wide-body A330 Family with neo version to Revenue visibility: backlog represents ~9 years of production at current production rates be delivered in summer 2018. Backlog of 317 aircraft (December 2017) . on family aircraft to 60 per month by mid-2019, 20 Years New Deliveries of Passenger and Freighter Aircraft (units) . New generation A350 XWB: designed to reduce operating costs, fuel burn Production rate increase A320 and CO2 emissions. Backlog of 712 aircraft (December 2017) on A350 XWB to 10 per month by end of 2018 . The world´s largest commercial aircraft – A380: in service with 13 . Partnership with Bombardier on C Series bringing together two complementary operators. Backlog of 95 aircraft (December 2017) product lines to rapidly extend our product offering into a fast growing market sector (subject to regulatory approvals) Commercial Aircraft Source: Airbus Global Market Forecast Passenger aircraft (≥ 100 seats) | Jet freight aircraft (>10 tonnes), Rounded figures to the nearest 10 A380 A330neo A350 XWB A321neo A global leader in the civil and military helicopter market . -

AED Fleet Contact List

AED Fleet Contact List September 2021 Make Model Primary Office Operations - Primary Operations - Secondary Avionics - Primary Avionics - Secondary Maintenance - Primary Maintenance - Secondary Air Tractor All Models MKC Persky, David (FAA) Hawkins, Kenneth (FAA) Marsh, Kenneth (FAA) Rockhill, Thane D (FAA) BadHorse, Jim (FAA) Airbus A300/310 SEA Hutton, Rick (FAA) Dunn, Stephen H (FAA) Gandy, Scott A (FAA) Watkins, Dale M (FAA) Patzke, Roy (FAA) Taylor, Joe (FAA) Airbus A318-321 CEO/NEO SEA Culet, James (FAA) Elovich, John D (FAA) Watkins, Dale M (FAA) Gandy, Scott A (FAA) Hunter, Milton C (FAA) Dodd, Mike B (FAA) Airbus A330/340 SEA Culet, James (FAA) Robinson, David L (FAA) Flores, John A (FAA) Watkins, Dale M (FAA) DiMarco, Joe (FAA) Johnson, Rocky (FAA) Airbus A350 All Series SEA Robinson, David L (FAA) Culet, James (FAA) Watkins, Dale M (FAA) Flores, John A (FAA) Dodd, Mike B (FAA) Johnson, Rocky (FAA) Airbus A380 All Series SEA Robinson, David L (FAA) Culet, James (FAA) Flores, John A (FAA) Watkins, Dale M (FAA) Patzke, Roy (FAA) DiMarco, Joe (FAA) Aircraft Industries All Models, L-410 etc. MKC Persky, David (FAA) McKee, Andrew S (FAA) Marsh, Kenneth (FAA) Pruneda, Jesse (FAA) Airships All Models MKC Thorstensen, Donald (FAA) Hawkins, Kenneth (FAA) Marsh, Kenneth (FAA) McVay, Chris (FAA) Alenia C-27J LGB Nash, Michael A (FAA) Lee, Derald R (FAA) Siegman, James E (FAA) Hayes, Lyle (FAA) McManaman, James M (FAA) Alexandria Aircraft/Eagle Aircraft All Models MKC Lott, Andrew D (FAA) Hawkins, Kenneth (FAA) Marsh, Kenneth (FAA) Pruneda, -

Joint Press Release

Joint Press Release Demonstrator phase launched: Future Combat Air System takes major step forward @AirbusDefence @dassault_onair @MTUaeroeng @Safran @ThalesGroup Paris/ Munich, 12 February 2020 – The governments of France and Germany have awarded Dassault Aviation, Airbus, together with their partners MTU Aero Engines, Safran, MBDA and Thales, the initial framework contract (Phase 1A), which launches the demonstrator phase for the Future Combat Air System (FCAS). This framework contract covers a first period of 18 months and initiates work on developing the demonstrators and maturing cutting-edge technologies, with the ambition to begin flight tests as soon as 2026. Since early 2019, the industrial partners have been working on the future architecture as part of the programme’s so called Joint Concept Study. Now, the FCAS programme enters into another decisive phase with the launch of the demonstrator phase. This phase will, in a first step, focus on the main technological challenges per domains: Next Generation Fighter (NGF), with Dassault Aviation as prime contractor and Airbus as main partner, to be the core element of Future Combat Air System, Unmanned systems Remote Carrier (RC) with Airbus as prime contractor and MBDA as main partner, Combat Cloud (CC) with Airbus as prime contractor and Thales as main partner, Engine with Safran and MTU as main partner. A Simulation Environment will be jointly developed between the involved companies to ensure the consistency between demonstrators. The launch of the Demonstrator Phase underlines the political confidence and determination of the FCAS partner nations and the associated industry to move forward and cooperate in a fair and balanced manner. -

Lifetime Excellence Lifetime Excellence | 3 Power for the World

MTU Aero Engines AG The full range of engine expertise Firmly established worldwide balanced portfolio, the company is represented in all thrust and power categories for commercial engines. Highpres MTU Aero Engines is Germany’s leading engine manufacturer sure compressors, lowpressure turbines and turbine center and a firmly established player in the international aviation frames “made by MTU” rank among the best in their class. industry. The company designs, develops, manufactures, markets and supports commercial and military propulsion In commercial engine maintenance, MTU Maintenance systems for aircraft and helicopters, and stationary gas tur sets global standards with its comprehensive services and bines, and offers full system capability in engine construction. innovative repair techniques. MTU Power offers compelling intelligent maintenance solutions for industrial gas turbines. MTU is the industrial lead company for almost all engines operated by the German Armed Forces and plays a key role High power density in major European military engine programs. MTU offers solutions for the entire engine lifecycle—from development to production to maintenance. With its well 2 | Lifetime Excellence Lifetime Excellence | 3 Power for the world MTU Maintenance Lease Services SMBC Aero Engine Lease MTU Maintenance Hannover MTU Maintenance Berlin-Brandenburg MTU Maintenance Canada Pratt & Whitney Canada Customer Service Centre Europe MTU Aero Engines North America EME Aero MTU Aero Engines Polska MTU Aero Engines, Headquarters MTU Maintenance Dallas For MTU Aero Engines, Aerospace Embedded Solutions customer proximity is key. Ceramic Coating Center This is delivered by around MTU Maintenance Zhuhai 10,000 employees from over 60 nations at 15 locations worldwide. Through its sub- sidiaries and joint ventures, Major locations and participations MTU is present in all key IGT Service Centers regions and markets. -

2021 AHNA Options Catalogue

OPTIONS CATALOGUE 2021 Return to the Table of Contents Contact and Order Information U.S.A: +1 800-COPTER-1 [email protected] Canada: +1 800-267-4999 [email protected] © July 2021 Airbus Helicopters, all rights reserved. 002 | Options Catalogue 2021 Options Catalogue INTRODUCTION At Airbus Helicopters in North America, our engineering excellence and completions capability is an integral part of meeting your operating requirements. We are committed to providing OEM approved equipment modifications that further enhance your experience with our product line. This catalogue illustrates a grouping of our most important and interesting options available for the H125, H130, H135, and H145 aircraft families. Airbus Helicopters, Inc. is a certified “Design Approval Organization” by the Federal Aviation Administration. Airbus Helicopters Canada is a certified “Design Approval Organization” by Transport Canada. As customer centers, we have also been recognized as an Authorized Design Organization by the Airbus Helicopters Group (AH Group). For more information, please visit Airbus World or see contact information on the next page. Airbus Helicopters' Airbus World customer portal simplifies customers’ daily operations and allows them to focus on what really matters: their business. Air- bus World is an innovative online platform for accessing technical publications, placing orders and quotations, managing fleet data as well as warranty claims, and receiving quick responses to support and services questions. Airbus Helicopters reserves the right to make configuration and data changes at any time without notice. Information contained in this document is expressed in good faith and does not constitute any offer or contract with Airbus Helicopters. -

Issue 4 – 2014

The Quarterly Bulletin of the COUNCIL OF EUROPEAN AEROSPACE SOCIETIES 3AF–AIAE–AIDAA–CzAeS –DGLR–FTF–HAES–NVvL–PSAA–RAAA–RAeS–SVFW–TsAGI–VKI Issue 4 - 2014 December 1 2 3 TOUCH DOWN! 1122 NOVEMBER 2014 AATT 15:34 UTC, ‘PHILAE’, THE ROSETTROSETTAA MISSION’S LANDER TOUCHESTOUCHES DOWN ON THE NUCLEUS OF COMET 67P/CHUR67P/CHURYMOV-GERASIMENKO:YMOVYMOV-GERASIMENKO: SPSPACEACE EUROPE MARKS QUITE AN IMPORTIMPORTANTTANTANTANT DATTEE IN THE HISTORHISTORYY OF SPSPACEACE EXPLORAEXPLORATIONTION . 1 THIS IMAGE CONFIRMSIRMS THATTHAATT ‘PHILAE’ IS ONO THE SURFACESURFACE OF THE COMET 2 THETHE ROSETTAROSETTA MISSION CREW MEMBERS ATAT THE EUROPEAN OPERATIONSOPERAAATIONSTIONS SPACESPAACECE CENTRE IN DARMSTADT,DARMSTADT, GERMANY,GERMANY, CELEBRATECELEBRATE ‘PHILAE’ SUCCESSFUL LANDING 3 ININ THE PREMISES OF THE ‘PHILAE’ SCIENCE OPERATIONSOPERATIONS AND NAVIGATIONNAVIGAVIGATION CENTRE IN CNES, TOULOUSE, FRANCE, THIS IS THE RELIEF AND THE EXPLOSION OF JOY WHAT IS THE CEAS ? THE CEAS MANAGEMENT the council of european aerospace societies (ceas) is an International non-Profit asso ciation, with the aim to develop a framework within which BOARD the major aerospace societies in europe can work together. It presently comprises 15 Member socie ties: 3af (france), aIae (spain), It Is structured as follows : aIdaa (Italy), czaes (czech republic), dGlr (Germany), ftf (sweden), haes (Greece), nVvl (netherlands), Psaa (Poland), aaar (romania), • General functions: President, director raes (united Kingdom), sVfw (switzerland), tsaGI (russia), VKI ((Von General, finance, -

FCAS Overview

The Future Combat System: An Overview A Second Line of Defense Overview on the Standup and Evolution 8/1/21 of the FCAS In this report, we have brought together our FCAS articles from both Second Line of Defense and Defense.info published since its standup in 2018 and covered through the Bundestag Budget Committee’s Green Light on funding for the program in June 2021. Report Authors: Robbin Laird, Murielle Delaporte and Pierre Tran The Future Combat System: An Overview The Future Combat System: An Overview A SECOND LINE OF DEFENSE OVERVIEW ON THE STANDUP AND EVOLUTION OF THE FCAS Preface ................................................................................................................................................... 3 The Future Combat Air System: The View from Paris ........................................................................... 4 France Leads FCAS Effort ................................................................................................................................. 4 The F-4 Upgrade .............................................................................................................................................. 4 A Team Approach to Air Combat Superiority .................................................................................................. 6 Companies and FCAS ...................................................................................................................................... 6 F-4 Technology as a FCAS Building Block ...................................................................................................... -

EN All Nippon Helicopter's H160 Completes First

All Nippon Helicopter’s H160 completes first flight #WeMakeItFly #H160ReasonsWhy Marignane, 14 January 2021 – All Nippon Helicopter’s (ANH) H160 has performed its first flight test, a 95-minute flight at the Marseille Provence Airport. This successful maiden flight paves the way for the aircraft’s entry into service in Japan. ANH deploys a helicopter fleet comprising six AS365s and five H135s for electronic news gathering for the TV stations across Japan. This H160 will replace one of its AS365s. “We are delighted to see the successful inaugural flight of Japan’s very first H160, and we are looking forward to this next-generation helicopter playing an important role in our nationwide missions,” said Jun Yanagawa, President of ANH. “Since the introduction of the AS365 helicopter three decades ago, the requirements of the electronic news gathering market is constantly evolving and has significantly improved. This state-of-the-art helicopter H160 is a timely welcome for our operations.” The H160 was granted its type certificate by the European Union Aviation Safety Agency (EASA) in July 2020, with the certification from the Japan Civil Aviation Bureau (JCAB) expected in early 2021. Upon delivery of the helicopter, specialised equipment installation and customisation will be performed at Airbus Helicopters’ Kobe facility, before its entry into service. “We are honoured to have ANH as our H160 launch customer in Japan, as they renew their fleet. This successful first flight is particularly meaningful during this unprecedented time for the industry. We thank our customer and the teams involved for devoting maximum efforts into this achievement. -

TMB-2019-H160M.Pdf

Introduction to H160M HELICOPTERS 1 Donauworth, November 4th 2019 Introduction to H160M Introduction to H160M Military version of the H160, 6-tonne class Benefitting from all innovations developed by Airbus Helicopters for the H160: A brand new platform with 68 new patents Developed with innovative tools and methods accelerating aircraft maturity at entry-into-service in 2020 Designed with accessibility in mind to ease maintenance: aircraft and engine maintenance plans fully aligned, aiming at high availability rates for reduced maintenance costs 2 Donauworth, November 4th 2019 Introduction to H160M One single platform = a true multi-role aircraft One single versatile platform for a wide range of missions Modular architecture for quick mission reconfiguration Fleet rationalization: one type of helicopter instead of several specialized types, aiming at reducing maintenance and training costs, and improving operational flexibility Typical missions: commando infiltration, national airspace protection, air intercept, search and rescue, anti-surface warfare, naval force protection, maritime security, maritime environment monitoring and intelligence, reconnaissance, special forces, C4I. e Designed with the French armed forces: configuration is the result of 10 years of joint e collaboration between Airbus Helicopters and the 3 different French Armed Forces 3 Donauworth, November 4th 2019 Introduction to H160M Key platform characteristics Platform key characteristics : Latest generation avionics from Thales (FlytX) Powered by latest-generation