Investor Guide Value Drivers 2017

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

1.1.3 Helicopters

Information on the Company’s Activities / 1.1 Presentation of the Company 1.1.3 Helicopters Airbus Helicopters is a global leader in the civil and military The HIL programme, for which the Airbus Helicopters’ H160 rotorcraft market, offering one of the most complete and modern was selected in 2017, was initially scheduled for launch range of helicopters and related services. This product range in 2022 by the current military budget law. Launching the currently includes light single-engine, light twin-engine, medium programme earlier will enable delivery of the fi rst H160Ms to and medium-heavy rotorcraft, which are adaptable to all kinds of the French Armed Forces to be advanced to 2026. The H160 mission types based on customer needs. See “— 1.1.1 Overview” was designed to be a modular helicopter, enabling its military for an introduction to Airbus Helicopters. version, with a single platform, to perform missions ranging from commando infi ltration to air intercept, fi re support, and anti-ship warfare in order to meet the needs of the army, the Strategy navy and the air force through the HIL programme. The new fi ve-bladed H145 is on track for EASA and FAA Business Ambition certifi cation in 2020. To ensure these certifi cations, two fi ve- bladed prototypes have clocked more than 400 fl ight hours Airbus Helicopters continues to execute its ambition to lead the in extensive fl ight test campaigns in Germany, France, Spain, helicopter market, build end-to-end solutions and grow new Finland, and in South America. First deliveries of the new H145 VTOL businesses, while being fi nancially sound. -

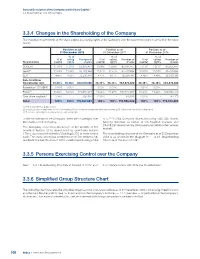

3.3.4 Changes in the Shareholding of the Company

General Description of the Company and its Share Capital / 3.3 Shareholdings and Voting Rights 3.3.4 Changes in the Shareholding of the Company The evolution in ownership of the share capital and voting rights of the Company over the past three years is set forth in the table below: Position as of Position as of Position as of 31 December 2018 31 December 2017 31 December 2016 % of % of % of % of voting Number of % of voting Number of % of voting Number of Shareholders capital rights shares capital rights shares capital rights shares SOGEPA 11.06% 11.06 % 85,835,477 11.08% 11.08% 85,835,477 11.11% 11.11% 85,835,477 GZBV(1) 11.04% 11.04 %85,709,82211.07% 11.07% 85,709,822 11.09% 11.09% 85,709,822 SEPI 4.16% 4.16 %32,330,381 4.17% 4.17% 32,330,381 4.18% 4.18% 32,330,381 Sub-total New Shareholder Agt. 26.26% 26.28% 203,875,680 26.32% 26.33% 203,875,680 26.38% 26.38% 203,875,680 Foundation “SOGEPA” 0.00% 0.00% 0 0.00% 0.00% - 0.00% 0.00% 0 Public(2) 73.66% 73.72% 571,855,277 73.66% 73.67% 570,550,857 73.60% 73.62% 568,853,019 Own share buyback(3) 0.08% - 636,924 0.02% - 129,525 0.02% - 184,170 Total 100% 100% 776,367,881 100% 100% 774,556,062 100% 100% 772,912,869 (1) KfW & other German public entities. -

Investor Guide FY 2019

Airbus - Investor Guide FY 2019 A Global Leader Key Financials Contact . A global leader in aeronautics, space and related services 2018 2019 Head of Investor Relations and Financial Communication: . 86% civil revenues, 14% defence . Three reportable segments: Airbus, Helicopters, Defence and Space Revenues (€ bn) 63.7 70.5 Thorsten Fischer [email protected] +33 5 67 19 02 64 . Robust and diverse backlog EBIT adjusted (€ bn) 5.8 6.9 Institutionals and Analysts: . Global footprint with European industrial roots RoSbased on EBIT adjusted 9.2% 9.9% 2019 Consolidated Airbus 2019 Consolidated Airbus EBIT reported (€ bn) 5.0 1.3 Mohamed Denden [email protected] +33 5 82 05 30 53 External Revenue by Division Order Book in value by Region Net Income/ loss (€ bn) 3.1 -1.4 Philippe Gossard [email protected] +33 5 31 08 59 43 EPS reported (€) 3.94 -1.75 Pierre Lu [email protected] +65 82 92 08 00 Dividend (€) 1.65 1.80* Net Cash Position (€bn) 13.3 12.5 Individual Investors : [email protected] +33 800 01 2001 FCF before M&A and Customer Financing (€bn) 2.9 3.5 € 70.5 bn € 471 bn t/o defence € 38 bn Further information on https://www.airbus.com/investors.html t/o defence € 10.1 bn Click here for guidance . * Board proposal to be submitted to the AGM 2020, subject to AGM approval. Airbus 2019 External Revenue Split 2019 Deliveries by Programme (units) 2019 Orders & Deliveries Airbus 77% Asia Pacific 31% Middle East 9% Key Financials Helicopters 8% Europe 28% Latin America 6% 2018 2019 Defence and Space 15% North America 18% Other 8% . -

AED Fleet Contact List

AED Fleet Contact List September 2021 Make Model Primary Office Operations - Primary Operations - Secondary Avionics - Primary Avionics - Secondary Maintenance - Primary Maintenance - Secondary Air Tractor All Models MKC Persky, David (FAA) Hawkins, Kenneth (FAA) Marsh, Kenneth (FAA) Rockhill, Thane D (FAA) BadHorse, Jim (FAA) Airbus A300/310 SEA Hutton, Rick (FAA) Dunn, Stephen H (FAA) Gandy, Scott A (FAA) Watkins, Dale M (FAA) Patzke, Roy (FAA) Taylor, Joe (FAA) Airbus A318-321 CEO/NEO SEA Culet, James (FAA) Elovich, John D (FAA) Watkins, Dale M (FAA) Gandy, Scott A (FAA) Hunter, Milton C (FAA) Dodd, Mike B (FAA) Airbus A330/340 SEA Culet, James (FAA) Robinson, David L (FAA) Flores, John A (FAA) Watkins, Dale M (FAA) DiMarco, Joe (FAA) Johnson, Rocky (FAA) Airbus A350 All Series SEA Robinson, David L (FAA) Culet, James (FAA) Watkins, Dale M (FAA) Flores, John A (FAA) Dodd, Mike B (FAA) Johnson, Rocky (FAA) Airbus A380 All Series SEA Robinson, David L (FAA) Culet, James (FAA) Flores, John A (FAA) Watkins, Dale M (FAA) Patzke, Roy (FAA) DiMarco, Joe (FAA) Aircraft Industries All Models, L-410 etc. MKC Persky, David (FAA) McKee, Andrew S (FAA) Marsh, Kenneth (FAA) Pruneda, Jesse (FAA) Airships All Models MKC Thorstensen, Donald (FAA) Hawkins, Kenneth (FAA) Marsh, Kenneth (FAA) McVay, Chris (FAA) Alenia C-27J LGB Nash, Michael A (FAA) Lee, Derald R (FAA) Siegman, James E (FAA) Hayes, Lyle (FAA) McManaman, James M (FAA) Alexandria Aircraft/Eagle Aircraft All Models MKC Lott, Andrew D (FAA) Hawkins, Kenneth (FAA) Marsh, Kenneth (FAA) Pruneda, -

2021 AHNA Options Catalogue

OPTIONS CATALOGUE 2021 Return to the Table of Contents Contact and Order Information U.S.A: +1 800-COPTER-1 [email protected] Canada: +1 800-267-4999 [email protected] © July 2021 Airbus Helicopters, all rights reserved. 002 | Options Catalogue 2021 Options Catalogue INTRODUCTION At Airbus Helicopters in North America, our engineering excellence and completions capability is an integral part of meeting your operating requirements. We are committed to providing OEM approved equipment modifications that further enhance your experience with our product line. This catalogue illustrates a grouping of our most important and interesting options available for the H125, H130, H135, and H145 aircraft families. Airbus Helicopters, Inc. is a certified “Design Approval Organization” by the Federal Aviation Administration. Airbus Helicopters Canada is a certified “Design Approval Organization” by Transport Canada. As customer centers, we have also been recognized as an Authorized Design Organization by the Airbus Helicopters Group (AH Group). For more information, please visit Airbus World or see contact information on the next page. Airbus Helicopters' Airbus World customer portal simplifies customers’ daily operations and allows them to focus on what really matters: their business. Air- bus World is an innovative online platform for accessing technical publications, placing orders and quotations, managing fleet data as well as warranty claims, and receiving quick responses to support and services questions. Airbus Helicopters reserves the right to make configuration and data changes at any time without notice. Information contained in this document is expressed in good faith and does not constitute any offer or contract with Airbus Helicopters. -

EN All Nippon Helicopter's H160 Completes First

All Nippon Helicopter’s H160 completes first flight #WeMakeItFly #H160ReasonsWhy Marignane, 14 January 2021 – All Nippon Helicopter’s (ANH) H160 has performed its first flight test, a 95-minute flight at the Marseille Provence Airport. This successful maiden flight paves the way for the aircraft’s entry into service in Japan. ANH deploys a helicopter fleet comprising six AS365s and five H135s for electronic news gathering for the TV stations across Japan. This H160 will replace one of its AS365s. “We are delighted to see the successful inaugural flight of Japan’s very first H160, and we are looking forward to this next-generation helicopter playing an important role in our nationwide missions,” said Jun Yanagawa, President of ANH. “Since the introduction of the AS365 helicopter three decades ago, the requirements of the electronic news gathering market is constantly evolving and has significantly improved. This state-of-the-art helicopter H160 is a timely welcome for our operations.” The H160 was granted its type certificate by the European Union Aviation Safety Agency (EASA) in July 2020, with the certification from the Japan Civil Aviation Bureau (JCAB) expected in early 2021. Upon delivery of the helicopter, specialised equipment installation and customisation will be performed at Airbus Helicopters’ Kobe facility, before its entry into service. “We are honoured to have ANH as our H160 launch customer in Japan, as they renew their fleet. This successful first flight is particularly meaningful during this unprecedented time for the industry. We thank our customer and the teams involved for devoting maximum efforts into this achievement. -

TMB-2019-H160M.Pdf

Introduction to H160M HELICOPTERS 1 Donauworth, November 4th 2019 Introduction to H160M Introduction to H160M Military version of the H160, 6-tonne class Benefitting from all innovations developed by Airbus Helicopters for the H160: A brand new platform with 68 new patents Developed with innovative tools and methods accelerating aircraft maturity at entry-into-service in 2020 Designed with accessibility in mind to ease maintenance: aircraft and engine maintenance plans fully aligned, aiming at high availability rates for reduced maintenance costs 2 Donauworth, November 4th 2019 Introduction to H160M One single platform = a true multi-role aircraft One single versatile platform for a wide range of missions Modular architecture for quick mission reconfiguration Fleet rationalization: one type of helicopter instead of several specialized types, aiming at reducing maintenance and training costs, and improving operational flexibility Typical missions: commando infiltration, national airspace protection, air intercept, search and rescue, anti-surface warfare, naval force protection, maritime security, maritime environment monitoring and intelligence, reconnaissance, special forces, C4I. e Designed with the French armed forces: configuration is the result of 10 years of joint e collaboration between Airbus Helicopters and the 3 different French Armed Forces 3 Donauworth, November 4th 2019 Introduction to H160M Key platform characteristics Platform key characteristics : Latest generation avionics from Thales (FlytX) Powered by latest-generation -

1.1 Presentation of the Company

Information on the Company’s Activities / 1.1 Presentation of the Company 1.1 Presentation of the Company 1.1.1 Overview Due to the nature of the markets in which the Company operates and the confi dential nature of its businesses, any statements with respect to the Company’s competitive position set out in paragraphs 1.1.1 through 1.1.5 below have been based on the Company’s internal information sources, unless another source has been specifi ed below. With consolidated revenues of € 63.7 billion in 2018, the Company expand the Airbus single-aisle family to cover the 100-150 seat is a global leader in aeronautics, space and related services. segment – and respond to a worldwide market demand for Airbus offers the most comprehensive range of passenger single-aisle jetliners in that segment. airliners. The Company is also a European leader providing tanker, combat, transport and mission aircraft, as well as one of the Despite challenges in the traditional helicopter market, Airbus world’s leading space companies. In helicopters, the Company Helicopters has shown resilient performance, keeping its market provides the most effi cient civil and military rotorcraft solutions leadership in the civil & parapublic segments. worldwide. In 2018, it generated 84.5% of its total revenues in the civil sector (compared to 85% in 2017) and 15.5% in the defence 2. Preserve our leading position in European Defence, Space sector (compared to 15% in 2017). As of 31 December 2018, the and Government markets by focusing on providing military Company’s active headcount was 133,671 employees. -

Airbus in Germany 02 Airbus in Germany Airbus – a Success Story

Airbus in Germany 02 Airbus in Germany Airbus – a success story The Airbus Group – formerly EADS – was formed in 2000 from the merger of German DaimlerChrysler Aerospace, French Aérospatiale Matra and Spanish CASA. Today, the group is the best example of European integration in the field of high technology. Shareholder structure 11% Germany 11% France 26% 4% Spain 74 % State participation Free float shares Airbus in Germany 03 Airbus is a global leader in aeronautics, space and related services. The Group employs a workforce of around 130,000 people in nearly 180 locations around the world. Airbus offers the most comprehensive range of airliners from 100 to more than 600 seats. Airbus is also a European leader providing tanker, combat, transportation and mission aircraft, as well as Europe‘s number one space enterprise and the world‘s second largest space business. In helicopters, Airbus provides the most efficient civil and military rotorcraft solutions worldwide. Increase in revenue in billions of euros +145+176% % 24.2 67.0 2000 2017 In 2017, Airbus generated revenues of € 66.8 billion. Thus, the group has more than doubled its business volume since its formation in 2000. Orders totalling over € 1,800 billion since 2000 saw the Group’s backlog of orders increase by more than fivefold to € 997 billion by the end of 2017. 04 Airbus in Germany Worldwide growth thanks to European best performance Since the group’s formation, the number of employees has increased by 52%. In the home countries of Germany, France, Great Britain and Spain alone, the number of employees has increased by 30,000 since the formation of Airbus (EADS) in 2000. -

Liste Des Candidats Cftc

LISTE DES CANDIDATS CFTC Nom Prénom Entreprise ROMAIN Frédéric ATR GAU Isabelle AIRBUS SAS LOZIER Jean-François ONERA GARRIGUES Jacques AIRBUS OPERATIONS SAS OLLIVIER Thierry STELIA AEROSPACE LYON Christophe AIRBUS HELICOPTERS CROSNIER Emmanuel AIRBUS DEFENCE AND SPACE VIGNERON Sylvie DAHER BONGRAND Denis AIRBUS OPERATIONS SAS ALLER Eric MBDA FRANCE ZUCCHI Béatrice AIRBUS HELICOPTERS DEGRANGE Eric APSYS FRANCE SUAZE Corinne AIRBUS DEFENCE AND SPACE VELETCHY Florent AIRBUS OPERATIONS SAS SALIBA Dominique DASSAULT AVIATION BASSET Philippe AIRBUS BUSINESS ACADEMY ARTHUR Marie-Pierre AIRBUS SAS COLLINS Jérôme NAVBLUE AUFFRAY Maryline ATR OUDOT Bernadette AIRBUS DS SLC SAS DEVOS Aurélie AIRBUS OPERATIONS SAS FERAUD Guy AIRBUS HELICOPTERS ABADIE Jean-Christophe AIRBUS OPERATIONS SAS DMYTRUK Martine ATR DE PAYSAC Damien AIRBUS DEFENCE AND SPACE BACABARA Corinne AIRBUS OPERATIONS SAS LECONTE Philippe ATR PINTO Laetitia ASB STAWICKI Renaud ARIANEGROUP SAS BARBEROUSSE François AIRBUS SAS SAINT-ANTONIN Laurent AIRBUS ONEWEB SATELLITES SAS AUVINET Marc AIRBUS OPERATIONS SAS BELLORGE Marina AIRBUS OPERATIONS SAS NEFF David AIRBUS OPERATIONS SAS BRY Hervé AIRBUS DEFENCE AND SPACE DEHAN Marc AIRBUS HELICOPTERS DELNEVO Alexia AIRBUS DEFENCE AND SPACE ELUARD Estelle AIRBUS OPERATIONS SAS PERRIN Olivier AIRBUS DS SLC SAS FRANCOIS Vincent AIRBUS OPERATIONS SAS ERMINE Marie AIRBUS OPERATIONS SAS BARUSSAUD Alain ARIANEGROUP SAS GURRET Joël STELIA AEROSPACE HEULIN Charlotte AIRBUS OPERATIONS SAS IBANEZ Jean-François AIRBUS OPERATIONS SAS CHARPIN Philippe AIRBUS -

Maintenance Training Courses 002 Maintenance Training

HELICOPTERS Training Services ® Maintenance Training Courses 002 Maintenance Training Maintenance Courses ADVANCED COURSES 1 week–6 months TYPE RATING 1–6 weeks PRE-ENTRY LEVEL COURSES 1–4 weeks PRE-ENTRY LEVEL SELF-ASSESSMENT 1–5 h AB INITIO 2400 h Maintenance Training 003 Annual Key Figures 121 COURSES ON +2,500 TRAINEES CUSTOMER’S SITE in Marignane around the world 13,000 HRS COURSE 19 TRAINING CENTRES DEVELOPMENT around the world for tailored courses 2,800 HOURS 98% OF OUR TRAINEES SIMULATION & FLIGHT SATISFIED in Marignane with the skills they have learnt during maintenance courses Training 04 > Learner Portal 05 > Pre-entry Level Self-Assessment Contents 06 > HCare Training 08 > Pre-entry Level Training 12 > Type Qualifications 16 > Training Network 20 > Favourites 22 > Advanced Training 28 > Customised Solutions 004 Maintenance Training Learner Portal FREE Training is just one click away with the Airbus Helicopters Learning Management System (LMS) Available on the Learner Portal: > Worldwide training offer > Course schedule & request Free-of-charge > Self-assessment Available worldwide > Course information & material > Register at www.airbushelicopterstrainingservices.com Maintenance Training 005 Pre-Entry Level Self-Assessment FREE Free online self-assessment for a successful training experience • Evaluate prerequisites > Adapt training to specific needs • Familiarise with the course level > Get immediate results • Access worldwide > 1 hour/modules > 4 modules available Standard Practices Fundamentals of Mechanics Pre-Entry Level Fundamentals of Avionics Training English language Register 1 on AHTS website Test 2 prerequisites Adapt 3 training course 006 Maintenance Training Training & Flight Ops HCare Services Offer An optimal training offer whatever your requirements in one of our 19 training centres or on the customer’s premises around the world. -

Airbus Presents Latest Innovations at the 2018 ILA Berlin Air Show

Airbus presents latest innovations at the 2018 ILA Berlin Air Show Toulouse, 20 April 2018 – Airbus will present its extensive product portfolio and a number of innovations at the 2018 ILA Berlin Air Show from 25 to 29 April, and will once again be the largest single exhibitor. This year’s ILA partner country is France. In the commercial aircraft segment, Airbus aircraft on display will be an Emirates Airline A380 and the A350-900 MSN 2. This A350 played a major role in the flight testing of the world’s most modern long-haul aircraft. More than 150 A350 XWBs are already in service around the world, including at Lufthansa, which has its home base for this aircraft type in Munich. Both the A380 and A350 XWB show the close cooperation between Germany and France within Airbus. The development, large-scale component manufacturing such as the fuselage, cockpit or vertical stabiliser, as well as final assembly and delivery activities for these aircraft are carried out at sites including Hamburg, Toulouse, Stade, Bremen, St. Nazaire and Nantes. A special attraction at Airbus this year will be the A340 BLADE (Breakthrough Laminar Aircraft Demonstrator in Europe). The wings of this test aircraft were modified to analyse new aerodynamic concepts for laminar flow as part of the European research project Clean Sky. In addition to the Eurofighter, Airbus Defence and Space will exhibit the C295 military transport aircraft and several Unmanned Aerial Vehicle (UAV) systems. For the first time ever, visitors to ILA will have the opportunity to view a 1:1 model of the future European UAV system MALE RPAS (Medium Altitude, Long Endurance; Remotely Piloted Aircraft System).