Annual Report and Accounts 2019 Connecting Customers to Opportunities

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

18 February 2019 Solvency and Diversification in Insurance Remain Key Strengths Despite Change in Structure

FINANCIAL INSTITUTIONS ISSUER IN-DEPTH Lloyds Banking Group plc 18 February 2019 Solvency and diversification in insurance remain key strengths despite change in structure Summary RATINGS In 2018, Lloyds Banking Group plc (LBG) altered its structure to comply with the UK's ring- Lloyds Banking Group plc Baseline Credit a3 fencing legislation, which requires large banks to separate their retail and SME operations, Assessment (BCA) and deposit taking in the European Economic Area (EEA) from their other activities, including Senior unsecured A3 Stable the riskier capital markets and trading business. As part of the change, LBG designated Lloyds Bank plc as the“ring-fenced” entity housing its retail, SME and corporate banking operations. Lloyds Bank plc It also assumed direct ownership of insurer Scottish Widows Limited, previously a subsidiary Baseline Credit A3 Assessment (BCA) of Lloyds Bank. The changes had little impact on the creditworthiness of LBG and Lloyds Adjusted BCA A3 Bank, leading us to affirm the deposit and senior unsecured ratings of both entities. Scottish Deposits Aa3 Stable/Prime-1 Widows' ratings were unaffected. Senior unsecured Aa3 Stable » LBG's reorganisation was less complex than that of most UK peers. The Lloyds Lloyds Bank Corporate Markets plc Banking Group is predominantly focused on retail and corporate banking, and the Baseline Credit baa3 required structural changes were therefore relatively minor. The group created a small Assessment (BCA) separate legal entity, Lloyds Bank Corporate Markets plc (LBCM), to manage its limited Adjusted BCA baa1 Deposits A1 Stable/Prime-1 capital markets and trading operations, and it transferred its offshore subsidiary, Lloyds Issuer rating A1 Stable Bank International Limited (LBIL), to LBCM from Lloyds Bank. -

Using Replicated Ledger to Reduce Swift Costs

WHITE PAPER USING REPLICATED LEDGER TO REDUCE SWIFT COSTS Abstract Nientibus et harum la aliquos que dunt harunte nat qui assimin ctincti nimoloratur? Quis sin enim expello rescitis aliberiosam, sumendu cienimil es ab in pelibus antiunt, eatur sit volorec tetur, occus asi suntiss imporer eperis dolupta que quid quatis mo volorit quas maio. Im acest, eos si beat. Ur? Nonseque reribus. Itatium re, nissi nullupietur audis sit adis con non corrum fugias eosae nones nonsenimus Itate esto moluptatur autatis sinctota dolent labo. Sum autem reriossum eos acerestectur rem que et haribus vel etur Introduction This paper proposes an approach to build a payment product that could be deployed across units of same bank or banks which have correspondent relationships, to reduce SWIFT message costs and to conserve liquidity by reducing need for Settlement and Nostro accounts. The paper proposes an outline of a product that implements a replicated, single wrapper around existing ledgers of such bank units to enable quick, irrevocable, tamper-proof approach to managing electronic payments between correspondent bank units. Existing ledgers of the bank would not be replaced or disturbed. Instead a wrapper application would be deployed that tracks specific entries in the ledger and replicates the changes to all members. This enables each member bank to see the same ledger at the same time and also be guaranteed of its accuracy. For this purpose, it is recommended the product be built using Blockchain for established and proven security. Such a replicated ledger would reduce active, recurring costs of using SWIFT network to pass payment messages. This will also reduce the much larger passive cost of holding funds in a non- remunerative settlement a/c with the correspondent bank. -

Hsbc to Acquire Lloyds Banking Group Onshore Assets in the Uae

Ab c 29 March 2012 HSBC TO ACQUIRE LLOYDS BANKING GROUP ONSHORE ASSETS IN THE UAE HSBC Bank Middle East Ltd (‘HSBC’), an indirect wholly-owned subsidiary of HSBC Holdings plc, has entered into an agreement to acquire the onshore retail and commercial banking business of Lloyds Banking Group (‘Lloyds’) in the United Arab Emirates (‘UAE’). The value of the gross assets being acquired is US$769m as at 31 December 2011. The transaction, which is subject to regulatory approvals, is expected to complete in 2012. HSBC’s largest operations in the MENA region are based in the UAE where HSBC enjoys a market-leading trade and commercial banking presence, in addition to the largest international retail banking and wealth management business. The business being acquired from Lloyds has approximately 8,800 personal and commercial customers and a loan book of approximately US$573m as at 31 December 2011. Commenting on the acquisition, Simon Cooper, Deputy Chairman and Chief Executive Officer of HSBC in MENA, said: “HSBC is the leading international bank in the UAE and the addition of Lloyds’ strong presence in retail and commercial banking is highly complementary to our business. The acquisition underscores the strategic importance of the UAE, and of the MENA region as a whole, to HSBC.” Media enquiries to: Tim Harrison + 971 4 4235632 [email protected] Brendan McNamara +44 (0) 20 7991 0655 [email protected] ends/more Registered Office and Group Head Office: This news release is issued by 8 Canada Square, London E14 5HQ, United Kingdom Web: www.hsbc.com HSBC Holdings plc Incorporated in England with limited liability. -

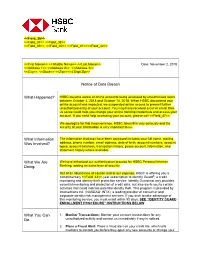

HSBC Became Aware of Online Accounts Being Accessed by Unauthorized Users Between October 4, 2018 and October 14, 2018

<<Field_36>> <<Field_37>> <<Field_38>> <<Field_39>>, <<Field_40>> <<Field_41>><<Field_42>> <<First Name>> << Middle Name>> <<Last Name>> Date: November 2, 2018 <<Address 1>> <<Address 2>> <<Address 3>> <<City>>, <<State>> <<Zip>><<4 Digit Zip>> Notice of Data Breach What Happened? HSBC became aware of online accounts being accessed by unauthorized users between October 4, 2018 and October 14, 2018. When HSBC discovered your online account was impacted, we suspended online access to prevent further unauthorized entry of your account. You may have received a call or email from us so we could help you change your online banking credentials and access your account. If you need help accessing your account, please call <<Field_47>>. We apologize for this inconvenience. HSBC takes this very seriously and the security of your information is very important to us. What Information The information that may have been accessed includes your full name, mailing Was Involved? address, phone number, email address, date of birth, account numbers, account types, account balances, transaction history, payee account information, and statement history where available. What We Are We have enhanced our authentication process for HSBC Personal Internet Doing. Banking, adding an extra layer of security. Out of an abundance of caution and at our expense, HSBC is offering you a complimentary <<Field_43>>-year subscription to Identity Guard®, a credit monitoring and identity theft protection service. Identity Guard not only provides essential monitoring and protection of credit data, but also alerts you to certain activities that could indicate potential identity theft. This program is provided by Intersections Inc. (NASDAQ: INTX), a leading provider of consumer and corporate identity risk management services. -

Svenska Handelsbanken AB

OFFERING CIRCULAR Svenska Handelsbanken AB (publ) (Incorporated as a public limited liability banking company in The Kingdom of Sweden) U.S.$50,000,000,000 Euro Medium Term Note Programme for the issue of Notes with a minimum maturity of one month On 26th June, 1992 Svenska Handelsbanken AB (publ) (the “Issuer” or the “Bank”) entered into a U.S.$1,500,000,000 Euro Medium Term Note Programme (the “Programme”) and issued an offering circular on that date describing the Programme. This Offering Circular supersedes any previous offering circular and supplements therein prepared in connection with the Programme. Any Notes (as defined below) issued under the Programme on or after the date of this Offering Circular are issued subject to the provisions described herein. This does not affect any Notes already in issue. Under the Programme, the Bank may from time to time issue Notes (the “Notes”), which expression shall include Notes (i) issued on a senior preferred basis as described in Condition 3 (“Senior Preferred Notes”), (ii) issued on a senior non-preferred basis as described in Condition 4 (“Senior Non-Preferred Notes”), (iii) issued on a subordinated basis and which rank on any voluntary or involuntary liquidation (Sw. likvidation) or bankruptcy (Sw. konkurs) of the Bank as described in Condition 5 (“Subordinated Notes”) and (iv) issued on a subordinated basis with no fixed maturity and which rank on any voluntary or involuntary liquidation (Sw. likvidation) or bankruptcy (Sw. konkurs) of the Bank as described in Condition 6 (“Additional Tier 1 Notes”). The Outstanding Principal Amount (as defined in Condition 2) of each Series (as defined below) of Additional Tier 1 Notes will be subject to Write Down (as defined in Condition 2) if the Common Equity Tier 1 Capital Ratio (as defined in Condition 2) of the Bank and/or the Handelsbanken Group (as defined Condition 2) is less than the relevant Trigger Level (as defined in Condition 2). -

HSBC Holdings Plc Senior Management Appointments

3 December 2012 SENIOR MANAGEMENT APPOINTMENTS HSBC Holdings plc announces that Paul Thurston will retire as a Group Managing Director and Chief Executive of Retail Banking and Wealth Management (RBWM), after a distinguished 37-year career with the HSBC Group, on 31 December 2012. John Flint is appointed a Group Managing Director and will succeed Thurston as Chief Executive of RBWM, one of HSBC's four global businesses, with effect from 1 January 2013. Guilherme Lima will succeed Flint as Group Head of Strategy and Planning and Chief of Staff to the Group Chief Executive. Separately, Antonio Losada (57), Chief Executive of Latin America and the Caribbean since 1 February 2012, has been appointed a Group Managing Director with effect from 1 December 2012. Losada has been with the HSBC Group since 1973 and has served in Brazil and as CEO of Argentina. "I would like to thank Paul for his 37 years of dedicated service to HSBC. Paul had planned to retire two years ago but stayed on at my request to help establish RBWM as a globally managed business. Under Paul's leadership RBWM has developed and rolled out consistent business models across multiple markets as part of a new, highly targeted strategy to build a global business," said Stuart Gulliver, Group Chief Executive. Thurston, 59, started his career at HSBC in 1975 in the United Kingdom, where he worked in a range of roles. Thurston moved to Hong Kong in 2000 to lead retail banking in the territory and was appointed a Group General Manager in 2003 when he took up responsibility for retail banking across the Asia-Pacific region. -

Giving Private Banking a Stroke of Elegance

PRIVATE BANKER May 2015 Issue 320 www.privatebankerinternational.com On track for digital wellness • Interview: Arbuthnot Latham's James Fleming • PBI London Awards: Preview • Interview: Lombard Odier's Dominic Tremlett • Country survey: France PBI 320.indd 1 22/05/2015 20:11:30 Join thousands of financial services Intelligent Environments, the international professionals who have joined The provider of digital solutions in association with Retail Banker International, Digital Banking Club to understand Cards International, Electronic and discuss the future of mobile and Payments International, Private Banker online financial services International and Motor Finance Membership benefits 10% discount on Delegate passes for Motor Finance and Private Banking UK conferences Annual Subscription to Retail Banker International, Cards International, Electronic Payments International, Motor Finance and Private Banker International publications (new subscribers only) World Market Intelligence Ltd’s archive of over 250 Retail Banking, Private Banking and Cards and Payments research reports (for new report purchasers only) Annual subscription to Retail Banking Intelligence Centre and Wealth Insight Intelligence database (new subscribers only) World Market Intelligence Ltd’s bespoke research and consultancy services For further information please email: [email protected] Join The Club! www.thedigitalbankingclub.com Or For further information please email: [email protected] PBI 320.indd 2 22/05/2015 20:11:30 TDBC-Advert-Dec-2014.indd 1 19/01/2015 09:03:48 Private Banker International EDITOR’S LETTER ANALYSIS CONTENTS London state of mind NEWS Join thousands of financial services Intelligent Environments, the international 2: NEWS BRIEFS hese are exciting times for wealth exposure. provider of digital solutions in association management in the UK. -

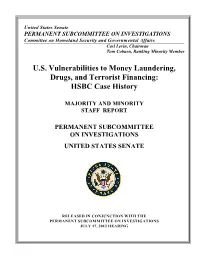

HSBC Case History

United States Senate PERMANENT SUBCOMMITTEE ON INVESTIGATIONS Committee on Homeland Security and Governmental Affairs Carl Levin, Chairman Tom Coburn, Ranking Minority Member U.S. Vulnerabilities to Money Laundering, Drugs, and Terrorist Financing: HSBC Case History MAJORITY AND MINORITY STAFF REPORT PERMANENT SUBCOMMITTEE ON INVESTIGATIONS UNITED STATES SENATE RELEASED IN CONJUNCTION WITH THE PERMANENT SUBCOMMITTEE ON INVESTIGATIONS JULY 17, 2012 HEARING SENATOR CARL LEVIN Chairman SENATOR TOM COBURN, M.D. Ranking Minority Member PERMANENT SUBCOMMITTEE ON INVESTIGATIONS ELISE J. BEAN Staff Director and Chief Counsel ROBERT L. ROACH Counsel and Chief Investigator LAURA E. STUBER Senior Counsel ALLISON ABRAMS Detailee ERIC WALKER Detailee KRISTIN GWIN Congressional Fellow BRIAN EGGER Detailee CHRISTOPHER J. BARKLEY Staff Director to the Minority KEITH B. ASHDOWN Chief Investigator to the Minority JUSTIN J. ROOD Senior Investigator to the Minority JAMIE BENCE MICHAEL WOLF Law Clerk Law Clerk BILL GAERTNER ARIELLE WORONOFF Law Clerk Law Clerk CURTIS KOWALK TAMIR HADDAD Law Clerk Intern KATIE MARTIN-BROWNE SOFIA KNUTSSON Law Clerk Intern WELLESLEY BAUN NOELIA ORTIZ Law Clerk Intern LAUREN ROBERTS JASWANT SINGH Law Clerk Intern MARY D. ROBERTSON Chief Clerk 7/16/12 Permanent Subcommittee on Investigations 199 Russell Senate Office Building – Washington, D.C. 20510 Majority: 202/224-9505 – Minority: 202/224-3721 Web Address: http://www.hsgac.senate.gov/subcommittees/investigations U.S. Vulnerabilities to Money Laundering, Drugs, and Terrorist Financing: HSBC Case History TABLE OF CONTENTS I. EXECUTIVE SUMMARY ................................................ 1 A. Findings. ......................................................... 10 (1) Longstanding Severe AML Deficiencies. 10 (2) Taking on High Risk Affiliates. ................................... 10 (3) Circumventing OFAC Prohibitions. 10 (4) Disregarding Terrorist Links. -

3Q20 Earnings Release

Hong Kong Exchanges and Clearing Limited and The Stock Exchange of Hong Kong Limited take no responsibility for the contents of this document, make no representation as to its accuracy or completeness and expressly disclaim any liability whatsoever for any loss howsoever arising from or in reliance upon the whole or any part of the contents of this document. 27 October 2020 (Hong Kong Stock Code: 5) HSBC Holdings plc 3Q20 EARNINGS RELEASE The attached announcement is being released to all the stock exchanges on which HSBC Holdings plc is listed. For and on behalf of HSBC Holdings plc Aileen Taylor Group Company Secretary and Chief Governance Officer The Board of Directors of HSBC Holdings plc as at the date of this announcement comprises: Mark Tucker*, Noel Quinn, Laura Cha†, Henri de Castries†, James Anthony Forese†, Steven Guggenheimer†, Irene Lee†, José Antonio Meade Kuribreña†, Heidi Miller†, Eileen K Murray†, David Nish†, Ewen Stevenson, Jackson Tai† and Pauline van der Meer Mohr†. * Non-executive Group Chairman † Independent non-executive Director HSBC Holdings plc Registered Office and Group Head Office: 8 Canada Square, London E14 5HQ, United Kingdom Web: www.hsbc.com Incorporated in England with limited liability. Registered in England: number 617987 27 OCTOBER 2020 HSBC HOLDINGS PLC 3Q20 EARNINGS RELEASE Noel Quinn, Group Chief Executive, said: “These were promising results against a backdrop of the continuing impacts of Covid-19 on the global economy. I'm pleased with the significantly lower credit losses in the quarter, and we are moving at pace to adapt our business model to a protracted low interest rate environment. -

Strategic Report 2019 Connecting Customers to Opportunities

HSBC Holdings plc Strategic Report 2019 Connecting customers to opportunities HSBC aims to be where the growth is, enabling businesses to thrive and economies to prosper, and ultimately helping people to fulfil their hopes and realise their ambitions. We aim to deliver long-term value for our shareholders through... ...our extensive ...our access to ...and our balance sheet international network... high-growth markets... strength. We are a leading international Our global footprint and market- We continue to maintain a bank, serving more than leading transaction banking strong capital, funding and 40 million personal, wealth franchise provide extensive liquidity position with a and corporate customers. access to faster-growing diversified business model. markets, particularly in Asia and the Middle East. Reported revenue by global business RBWM 41% CMB 27% GB&M 27% GPB 3% Corporate Centre 2% Total assets Common equity tier 1 ratio Reported revenue by region $2.7tn 14.7% (2018: $2.6tn) (2018: 14.0%) Asia 49% Europe 29% North America 11% Latin America 5% Middle East and North Africa 6% HSBC Holdings plc Strategic Report 2019 Contents Overview 2 Highlights 4 HSBC at a glance 6 Group Chairman’s statement 8 Group Chief Executive’s review Strategy 10 Global trends and strategic advantages 12 Delivering our strategy How we do business 14 Our approach 15 Our ESG metrics and targets 16 Customers This Strategic Report was approved by the Board 18 Employees on 18 February 2020. 20 Supporting sustainable growth 22 Task Force on Climate-related Financial Disclosures (‘TCFD’) 24 Responsible business culture Mark E Tucker Group Chairman Financial overview 26 Delivery against our June 2018 financial targets/2020 business update A reminder and new Group financial targets The currency we report in is US dollars. -

We Understand the Value of Global Connections. Do You?

We understand the value of global connections. Do you? China Student and graduate careers 2014-2015 We’re inspired by the way the world is changing Across the world, economic growth is bringing new prosperity. Businesses are pioneering new trade routes and new centres of wealth and influence are emerging. We’re inspired by these changes and the opportunities they bring for our business, our employees and our customers. The best and brightest people are also excited by this progress. These are the people we are looking to connect with, because these people will help shape the future of HSBC. We have a proud history built on our values, which are reflected in everything we do. Our values are: to be open to different ideas and cultures, dependable in having the courage to make decisions based on doing the right thing without compromising our global standards and the integrity on which HSBC is built, and to be connected to our customers, communities, regulators and each other. It’s these values that define who we are. Achieve your potential at HSBC. www.hsbc.com/careers A world of knowledge and experience As one of the largest banking and financial services This ensures we are well positioned for long-term organisations in the world, with offices across more than sustainable growth and to make a positive contribution to 75 countries and territories, our long-term success has the environment and communities in which we operate. been built on the value of local knowledge and being where the growth is. See where your future could take you at HSBC. -

List of PRA-Regulated Banks

LIST OF BANKS AS COMPILED BY THE BANK OF ENGLAND AS AT 2nd December 2019 (Amendments to the List of Banks since 31st October 2019 can be found below) Banks incorporated in the United Kingdom ABC International Bank Plc DB UK Bank Limited Access Bank UK Limited, The ADIB (UK) Ltd EFG Private Bank Limited Ahli United Bank (UK) PLC Europe Arab Bank plc AIB Group (UK) Plc Al Rayan Bank PLC FBN Bank (UK) Ltd Aldermore Bank Plc FCE Bank Plc Alliance Trust Savings Limited FCMB Bank (UK) Limited Allica Bank Ltd Alpha Bank London Limited Gatehouse Bank Plc Arbuthnot Latham & Co Limited Ghana International Bank Plc Atom Bank PLC Goldman Sachs International Bank Axis Bank UK Limited Guaranty Trust Bank (UK) Limited Gulf International Bank (UK) Limited Bank and Clients PLC Bank Leumi (UK) plc Habib Bank Zurich Plc Bank Mandiri (Europe) Limited Hampden & Co Plc Bank Of Baroda (UK) Limited Hampshire Trust Bank Plc Bank of Beirut (UK) Ltd Handelsbanken PLC Bank of Ceylon (UK) Ltd Havin Bank Ltd Bank of China (UK) Ltd HBL Bank UK Limited Bank of Ireland (UK) Plc HSBC Bank Plc Bank of London and The Middle East plc HSBC Private Bank (UK) Limited Bank of New York Mellon (International) Limited, The HSBC Trust Company (UK) Ltd Bank of Scotland plc HSBC UK Bank Plc Bank of the Philippine Islands (Europe) PLC Bank Saderat Plc ICBC (London) plc Bank Sepah International Plc ICBC Standard Bank Plc Barclays Bank Plc ICICI Bank UK Plc Barclays Bank UK PLC Investec Bank PLC BFC Bank Limited Itau BBA International PLC Bira Bank Limited BMCE Bank International plc J.P.