Rostov-On-Don

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

High Commissioner on National Minorities

Organization for Security and Co-operation in Europe High Commissioner on National Minorities The Hague, 12 January 2001 Dear Mr. Minister, In the beginning of last year the government of Ukraine requested me to investigate the situation of Ukrainian language education in your country. When I discussed this with your government, it offered to facilitate such an investigation. Earlier, your government had requested me to investigate the situation of Russian language education in Ukraine. The government of Ukraine also declared itself willing to facilitate such an investigation. In the summer of last year I have studied the situation of Ukrainian language education in your country, assisted by two experts, Prof. Bowring from the United Kingdom and Mr. Zhekov from Bulgaria. My conclusions are based on visits to Moscow, St. Petersburg and Tyumen, where conversations took place with local and regional authorities and with representatives of Ukrainian organisations. In Moscow extensive consultations took place with governmental authorities. While in Moscow, I also received representatives of Ukrainian organisations in Krasnodar, Ekatarinburg and Moscow Oblast. I want to thank your government for its co-operation. H.E. Mr. Igor Ivanov Minister of Foreign Affairs Moscow P.O. Box 20062 Telephone Telefax [email protected] 2500 EB, The Hague (+31-70) 312 55 00 (+31-70)363 59 10 http://www.osce.org Prinsessegracht 22 2514 AP, The Hague The Netherlands Earlier in the summer, I have conducted similar studies in Ukraine, again assisted by Prof. Bowring and Mr. Zhekov. I visited, Kharkiv, Lviv, Odessa and Simferopol, and met there with the local and regional authorities and with representatives of the Russian community. -

Survey of Land and Real Estate Transactions in the Russian Federation

36117 V. 1 Public Disclosure Authorized Foreign Investment Advisory Service, Project is co-financed by the a joint service of the European Union International Finance Corporation in the framework of the and the World Bank Policy Advice Programme Public Disclosure Authorized SURVEY OF LAND AND REAL ESTATE TRANSACTIONS IN THE RUSSIAN FEDERATION CROSS-REGIONAL REPORT Public Disclosure Authorized March 2006 Public Disclosure Authorized Survey of Land and Real Estate Transactions in the Russian Federation. Cross-Regional Report The project has also received financial support from the Government of Switzerland, the State Secretariat for Economic Affairs (seco). Report is prepared by the Media Navigator marketing agency, www.navigator,nnov.ru Disclaimer (EU) This publication has been produced with the financial assistance of the European Union. The contents of this publication are the sole responsibility of its authors and can in no way be taken to reflect the views of the European Union. Disclaimer (FIAS) The Organizations (i.e. IBRD and IFC), through FIAS, have used their best efforts in the time available to provide high quality services hereunder and have relied on information provided to them by a wide range of other sources. However they do not make any representations or warranties regarding the completeness or accuracy of the information included this report, or the results which would be achieved by following its recommendations. 2 Survey of Land and Real Estate Transactions in the Russian Federation. Cross-Regional Report TABLE OF -

FULL LIST of WINNERS the 8Th International Children's Art Contest

FULL LIST of WINNERS The 8th International Children's Art Contest "Anton Chekhov and Heroes of his Works" GRAND PRIZE Margarita Vitinchuk, aged 15 Novocherkassk, Rostov Oblast, Russia for “The Lucky One” Age Group: 14-17 years olds 1st place awards: Anna Lavrinenko, aged 14 Novocherkassk, Rostov Oblast, Russia for “Ward No. 6” Xenia Grishina, aged 16 Gatchina, Leningrad Oblast, Russia for “Chameleon” Hei Yiu Lo, aged 17 Hongkong for “The Wedding” Anastasia Valchuk, aged 14 Prokhladniy, Kabardino-Balkar Republic, Russia for “Ward Number 6” Yekaterina Kharagezova, aged 15 Novocherkassk, Rostov Oblast, Russia for “Portrait of Anton Chekhov” Yulia Kovalevskaya, aged 14 Prokhladniy, Kabardino-Balkar Republic, Russia for “Oversalted” Valeria Medvedeva, aged 15 Serov, Sverdlovsk Oblast, Russia for “Melancholy” Maria Pelikhova, aged 15 Penza, Russia for “Ward Number 6” 1 2nd place awards: Anna Pratsyuk, aged 15 Omsk, Russia for “Fat and Thin” Maria Markevich, aged 14 Gomel, Byelorussia for “An Important Conversation” Yekaterina Kovaleva, aged 15 Omsk, Russia for “The Man in the Case” Anastasia Dolgova, aged 15 Prokhladniy, Kabardino-Balkar Republic, Russia for “Happiness” Tatiana Stepanova, aged 16 Novocherkassk, Rostov Oblast, Russia for “Kids” Katya Goncharova, aged 14 Gatchina, Leningrad Oblast, Russia for “Chekhov Reading Out His Stories” Yiu Yan Poon, aged 16 Hongkong for “Woman’s World” 3rd place awards: Alexander Ovsienko, aged 14 Taganrog, Russia for “A Hunting Accident” Yelena Kapina, aged 14 Penza, Russia for “About Love” Yelizaveta Serbina, aged 14 Prokhladniy, Kabardino-Balkar Republic, Russia for “Chameleon” Yekaterina Dolgopolova, aged 16 Sovetsk, Kaliningrad Oblast, Russia for “The Black Monk” Yelena Tyutneva, aged 15 Sayansk, Irkutsk Oblast, Russia for “Fedyushka and Kashtanka” Daria Novikova, aged 14 Smolensk, Russia for “The Man in a Case” 2 Masha Chizhova, aged 15 Gatchina, Russia for “Ward No. -

Economic and Social Council

UNITED NATIONS E Economic and Social Distr. GENERAL Council ECE/MP.WAT/2006/16/Add.6 18 October 2006 Original: ENGLISH ECONOMIC COMMISSION FOR EUROPE MEETING OF THE PARTIES TO THE CONVENTION ON THE PROTECTION AND USE OF TRANSBOUNDARY WATERCOURSES AND INTERNATIONAL LAKES Fourth meeting Bonn (Germany), 20–22 November 2006 Item 7 (e) of the provisional agenda PRELIMINARY ASSESSMENT OF TRANSBOUNDARY RIVERS IN EASTERN EUROPE AND THE CAUCASUS DISCHARGING INTO THE BLACK SEA AND THEIR MAJOR TRANSBOUNDARY TRIBUTARIES Submitted by the Chairperson of the Working Group on Monitoring and Assessment Addendum 1. This preliminary assessment is an intermediate product that deals with major transboundary rivers discharging from Eastern Europe and the Caucasus into the Black Sea and some of their transboundary tributaries. 2. Based on the countries’ responses to the datasheets 1 and data available from other sources, only a very limited number of watercourses have been dealt with so far as shown in the table below. The other watercourses will be included in the updated version to be submitted to the sixth Ministerial Conference “Environment for Europe” (Belgrade, October 2007). This update will also cover other transboundary rivers discharging into the Black Sea (e.g. Rezvaya, Velaka, Danube, Siret and Delta-Liman) and their major transboundary tributaries. 1 The cut-off date was 1 September 2006. GE.06-25894 ECE/MP.WAT/2006/16/Add.6 Page 2 Transboundary rivers discharging into the Black Sea and their major transboundary tributaries (Eastern Europe and -

Argus Russian Coal

Argus Russian Coal Issue 17-36 | Monday 9 October 2017 MARKET COmmENTARY PRICES Turkey lifts coal imports from Russia Russian coal prices $/t Turkey increased receipts of Russian thermal coal by 9pc on Delivery basis NAR kcal/kg Delivery period 6 Oct ± 29 Sep the year in January-August, to 7.79mn t, according to data fob Baltic ports 6,000 Nov-Dec 17 86.97 -0.20 from statistics agency Tuik, amid higher demand from utili- fob Black Sea ports 6,000 Nov-Dec 17 90.63 -0.25 ties and households. Russian material replaced supplies from cif Marmara* 6,000 Nov 17 100.33 0.33 South Africa, which redirected part of shipments to more fob Vostochny 6,000 Nov-Dec 17 100.00 1.00 profitable markets in Asia-Pacific this year. fob Vostochny 5,500 Nov-Dec 17 87.0 0 1.75 *assessment of Russian and non-Russian coal In August Russian coal receipts rose to over 1.26mn t, up by 15pc on the year and by around 19pc on the month. Russian coal prices $/t This year demand for sized Russian coal is higher com- Delivery basis NAR kcal/kg Delivery period Low High pared with last year because of colder winter weather in 2016-2017, a Russian supplier says. Demand for coal fines fob Baltic ports 6,000 Nov-Dec 17 85.25 88.00 fob Black Sea ports 6,000 Nov-Dec 17 89.50 91.00 from utilities has also risen amid the launch of new coal- fob Vostochny 6,000 Nov-Dec 17 100.00 100.00 fired capacity, the source adds. -

Safety of Technogenic and Natural Systems 2020

№3 Safety of Technogenic and Natural Systems 2020 UDC 614.849 https://doi.org/10.23947/2541-9129-2020-3-21-32 Territorial fire statistics and assessment of their causes and consequences on the example of the Rostov region V. G. Ustin1, Yu. I. Bulygin2, P. P. Tretyakov3, V. V. Maslenskiy4 1 MD of the MES of Russia for the Rostov region (Rostov-on-Don, Russian Federation) 2,3,4 Don State Technical University (Rostov-on-Don, Russian Federation) Introduction. A deep and comprehensive analysis of the parameters of the situation with fires in the territories of the Russian Federation and its relationship with socio-economic processes is more relevant than ever for Russia. The article presents, summarizes and analyzes statistical data on the situation with fires and their consequences on the territory of the Rostov region for 2018-2019. Problem Statement. The paper considers the problem of official statistical accounting of fires, the procedure for accounting for people killed and injured in a fire in the context of a changing regulatory framework in this area. The analysis of the situation, official and verified information on fires and their consequences will create a reliable socio- economic characteristic of the Rostov region. Theoretical Part. The paper deals with the peculiarities of accounting of fires and their consequences in Russia. The source materials are the official statistics of the MD of the MES of Russia for the Rostov region on the number of fires on the territory, months, the number of people injured and killed in fires and their distribution by gender, age and time of death, objects and causes of fires. -

Argus Nefte Transport

Argus Nefte Transport Oil transportation logistics in the former Soviet Union Volume XVI, 5, May 2017 Primorsk loads first 100,000t diesel cargo Russia’s main outlet for 10ppm diesel exports, the Baltic port of Primorsk, shipped a 100,000t cargo for the first time this month. The diesel was loaded on 4 May on the 113,300t Dong-A Thetis, owned by the South Korean shipping company Dong-A Tanker. The 100,000t cargo of Rosneft product was sold to trading company Vitol for delivery to the Amsterdam-Rotter- dam-Antwerp region, a market participant says. The Dong-A Thetis was loaded at Russian pipeline crude exports berth 3 or 4 — which can handle crude and diesel following a recent upgrade, and mn b/d can accommodate 90,000-150,000t vessels with 15.5m draught. 6.0 Transit crude Russian crude It remains unclear whether larger loadings at Primorsk will become a regular 5.0 occurrence. “Smaller 50,000-60,000t cargoes are more popular and the terminal 4.0 does not always have the opportunity to stockpile larger quantities of diesel for 3.0 export,” a source familiar with operations at the outlet says. But the loading is significant considering the planned 10mn t/yr capacity 2.0 addition to the 15mn t/yr Sever diesel pipeline by 2018. Expansion to 25mn t/yr 1.0 will enable Transneft to divert more diesel to its pipeline system from ports in 0.0 Apr Jul Oct Jan Apr the Baltic states, in particular from the pipeline to the Latvian port of Ventspils. -

MEGA Rostov-On-Don Rostov-On-Don, Russia a Way of 15 MLN Life for All VISITORS ANNUALLY

MEGA Rostov-on-Don Rostov-on-Don, Russia A way of 15 MLN life for all VISITORS ANNUALLY Conveniently located near the M4 federal highway, with Enjoying over 15 million visitors a year, MEGA Rostov-on-Don a competitive mix of anchor tenants, affordable family has the highest footfall in the region. Our concept allows every value, and an exceptional food and beverage offer, guest to find something which appeals to the whole family, be MEGA Rostov-on-Don has the highest brand awareness that leisure or shopping. Our wide range of stores, services and among our competitors. leisure opportunities significantly increases dwell time, providing Luhansk high sales and a fun day out for our guests. Kamensk-Shakhtinskiy Gukovo Donetsk Novoshakhtinsk ShakhtyShakaty Novocherkassk Volgodonsk ROSTOV-ON-DON City Centre Taganrog Bataysk Azov Catchment Areas People Distance ● Primary 40,720 11 km ● Secondary 1,450,920 11–18 km ● Tertiary 2,831,070 > 18–211 km 59% EyskTotal area: 4,322,710 9 33% CUSTOMERS COME BUS ROUTES LIFESTYLE BY CAR GUESTS Sal’sk Tikhoretsk A region with Loyal customers MEGA Rostov is located in the city of Rostov–on-Don and attracts shoppers from all over the strong potential city and surrounding area. MEGA is loved by families, lifestyle and experienced guests alike. Rostov region The city of Rostov-on-Don Rostov region is a part of the Southern Federal District. Considered as a southern capital of Russia, Rostov- GUESTS VISIT MEGA 125 MINS 756km away from Moscow it has major railway routes on-Don has a diverse economical profile, with major AVERAGE 34% 62% 2.7 TIMES PER MONTH DWELL TIME passing in many directions across Russia and abroad. -

Career Break Or a New Career? Extremist Foreign Fighters in Ukraine

Career Break or a New Career? Extremist Foreign Fighters in Ukraine By Kacper Rekawek (@KacperRekawek) April 2020 Counter Extremism Project (CEP) Germany www.counterextremism.com I @FightExtremism CONTENTS: ABOUT CEP/ABOUT THE AUTHOR 2 EXECUTIVE SUMMARY 3 INTRODUCTION 5 SECTION I INTRODUCING FOREIGN FIGHTERS IN THE WAR IN UKRAINE 7 THE XRW FOREIGN FIGHTER: A WORLDVIEW 9 TALKING TO FOREIGN FIGHTERS: THEIR WORDS AND SYMBOLS 11 THE “UNHAPPY” FOREING FIGHTERS 13 CIVIL WAR? 15 SECTION II WHY THEY FIGHT 17 A CAREER BREAK OR NEW CAREER? 18 FOREIGN FIGHTERS WAR LOGISTICS 22 SECTION III FOREIGN FIGHTERS AS A THREAT? 25 TENTATIVE CONCLUSION: NEITHER A UKRAINIAN 29 NOR A WESTERN PROBLEM? ENDNOTES 31 Counter Extremism Project (CEP) 1 counterextremism.com About CEP The Counter Extremism Project (CEP) is a not-for-profit, non-partisan, international policy organization formed to combat the growing threat from extremist ideologies. Led by a renowned group of former world leaders and diplomats it combats extremism by pressuring financial and material support networks; countering the narrative of extremists and their online recruitment; and advocating for smart laws, policies, and regulations. About the author Kacper Rekawek, PhD is an affiliated researcher at CEP and a GLOBSEC associate fellow. Between 2016 and 2019 he led the latter’s national security program. Previously, he worked at the Polish Institute of International Affairs (PISM) and University of Social Sciences in Warsaw, Poland. He held Paul Wilkinson Memorial Fellowship at the Handa Centre -

The Donbas As an Intentional Community

THIS IS A DRAFT PAPER From Exit to Take-Over: The Evolution of the Donbas as an Intentional Community VLAD MYKHNENKO* International Policy Fellow The Central European University & Open Society Institute E-mail: [email protected] Paper for Workshop No 20. The Politics of Utopia: Intentional Communities as Social Science Microcosms The European Consortium for Political Research Joint Sessions of Workshops 13-18 April 2004 Uppsala, Sweden ABSTRACT: The Donbas – a large old industrial region in the Ukrainian-Russian Cossack borderland – constitutes a particular intentional community. According to earlier positive accounts, it was a space, the open steppe, a frontier land, a fugitive’s paradise, where the notions of and desires for freedom and dignifying labour had been realised. According to its current negative associations, the Donbas is an allegedly realised utopia of an ‘anti-modern’ community, dominated by a ‘criminal-political nexus’ of terrorising mafia gangs and political clans. The purpose of this paper is to compare the Donbas community, the evolution of intentions of its founders and of the images produced in the process of its construction, in three very different points in time – under the Russian Empire, under the Bolshevik Rule and Stalin’s Great Terror, and during the post-communist transformation. * I would like to express my gratitude here to the International Policy Fellowships, affiliated with the Central European University and Open Society Institute – Budapest, for their generous help, which has allowed me, among many other things, to work on this paper. 2 In both a geographical and symbolic sense, the Donbas constitutes a particular community, just as a nation, city, or village does. -

As of June 30, 2018

LIST OF AFFILIATES Sberbank of Russia (full corporate name of the joint-stock company) Issuer code: 0 1 4 8 1 – В as 3 0 0 6 2 0 1 8 of (indicate the date on which the list of affiliates of the joint-stock company was compiled) Address of the issuer: 19, Vavilova St., Moscow 117997 (address of the issuer – the joint-stock company – indicated in the Unified State Register of Legal Entities where a body or a representative of the joint-stock company is located) Information contained in this list of affiliates is subject to disclosure pursuant to the laws of the Russian Federation on securities. Website: http://www.sberbank.com; http://www.e-disclosure.ru/portal/company.aspx?id=3043 (the website used by the issuer to disclose information) Deputy Chairperson of the Executive Board of Sberbank B. Zlatkis (position of the authorized individual of the joint-stock company) (signature) (initials, surname) L.S. “ 03 ” July 20 18 . Issuer codes INN (Taxpayer Identificat ion Number) 7707083893 OGRN (Primary State Registrati on Number) 1027700132195 I. Affiliates as of 3 0 0 6 2 0 1 8 Item Full company name (or name for a Address of a legal entity or place of Grounds for recognizing the entity Date on which Interest of the affiliate Percentage of ordinary No. nonprofit entity) or full name (if any) of residence of an individual (to be as an affiliate the grounds in the charter capital of shares of the joint- the affiliate indicated only with the consent of became valid the joint-stock stock company owned the individual) company, % by the affiliate, % 1 2 3 4 5 6 7 Entity may manage more than The Central Bank of the Russian 12, Neglinnaya St., Moscow 20% of the total number of votes 1 21.03.1991 50.000000004 52.316214 Federation 107016 attached to voting shares of the Bank 1. -

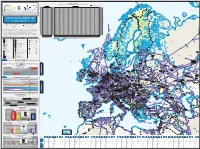

System Development Map 2019 / 2020 Presents Existing Infrastructure & Capacity from the Perspective of the Year 2020

7125/1-1 7124/3-1 SNØHVIT ASKELADD ALBATROSS 7122/6-1 7125/4-1 ALBATROSS S ASKELADD W GOLIAT 7128/4-1 Novaya Import & Transmission Capacity Zemlya 17 December 2020 (GWh/d) ALKE JAN MAYEN (Values submitted by TSO from Transparency Platform-the lowest value between the values submitted by cross border TSOs) Key DEg market area GASPOOL Den market area Net Connect Germany Barents Sea Import Capacities Cross-Border Capacities Hammerfest AZ DZ LNG LY NO RU TR AT BE BG CH CZ DEg DEn DK EE ES FI FR GR HR HU IE IT LT LU LV MD MK NL PL PT RO RS RU SE SI SK SM TR UA UK AT 0 AT 350 194 1.570 2.114 AT KILDIN N BE 477 488 965 BE 131 189 270 1.437 652 2.679 BE BG 577 577 BG 65 806 21 892 BG CH 0 CH 349 258 444 1.051 CH Pechora Sea CZ 0 CZ 2.306 400 2.706 CZ MURMAN DEg 511 2.973 3.484 DEg 129 335 34 330 932 1.760 DEg DEn 729 729 DEn 390 268 164 896 593 4 1.116 3.431 DEn MURMANSK DK 0 DK 101 23 124 DK GULYAYEV N PESCHANO-OZER EE 27 27 EE 10 168 10 EE PIRAZLOM Kolguyev POMOR ES 732 1.911 2.642 ES 165 80 245 ES Island Murmansk FI 220 220 FI 40 - FI FR 809 590 1.399 FR 850 100 609 224 1.783 FR GR 350 205 49 604 GR 118 118 GR BELUZEY HR 77 77 HR 77 54 131 HR Pomoriy SYSTEM DEVELOPMENT MAP HU 517 517 HU 153 49 50 129 517 381 HU Strait IE 0 IE 385 385 IE Kanin Peninsula IT 1.138 601 420 2.159 IT 1.150 640 291 22 2.103 IT TO TO LT 122 325 447 LT 65 65 LT 2019 / 2020 LU 0 LU 49 24 73 LU Kola Peninsula LV 63 63 LV 68 68 LV MD 0 MD 16 16 MD AASTA HANSTEEN Kandalaksha Avenue de Cortenbergh 100 Avenue de Cortenbergh 100 MK 0 MK 20 20 MK 1000 Brussels - BELGIUM 1000 Brussels - BELGIUM NL 418 963 1.381 NL 393 348 245 168 1.154 NL T +32 2 894 51 00 T +32 2 209 05 00 PL 158 1.336 1.494 PL 28 234 262 PL Twitter @ENTSOG Twitter @GIEBrussels PT 200 200 PT 144 144 PT [email protected] [email protected] RO 1.114 RO 148 77 RO www.entsog.eu www.gie.eu 1.114 225 RS 0 RS 174 142 316 RS The System Development Map 2019 / 2020 presents existing infrastructure & capacity from the perspective of the year 2020.