View PDF Document

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

My Personal Callsign List This List Was Not Designed for Publication However Due to Several Requests I Have Decided to Make It Downloadable

- www.egxwinfogroup.co.uk - The EGXWinfo Group of Twitter Accounts - @EGXWinfoGroup on Twitter - My Personal Callsign List This list was not designed for publication however due to several requests I have decided to make it downloadable. It is a mixture of listed callsigns and logged callsigns so some have numbers after the callsign as they were heard. Use CTL+F in Adobe Reader to search for your callsign Callsign ICAO/PRI IATA Unit Type Based Country Type ABG AAB W9 Abelag Aviation Belgium Civil ARMYAIR AAC Army Air Corps United Kingdom Civil AgustaWestland Lynx AH.9A/AW159 Wildcat ARMYAIR 200# AAC 2Regt | AAC AH.1 AAC Middle Wallop United Kingdom Military ARMYAIR 300# AAC 3Regt | AAC AgustaWestland AH-64 Apache AH.1 RAF Wattisham United Kingdom Military ARMYAIR 400# AAC 4Regt | AAC AgustaWestland AH-64 Apache AH.1 RAF Wattisham United Kingdom Military ARMYAIR 500# AAC 5Regt AAC/RAF Britten-Norman Islander/Defender JHCFS Aldergrove United Kingdom Military ARMYAIR 600# AAC 657Sqn | JSFAW | AAC Various RAF Odiham United Kingdom Military Ambassador AAD Mann Air Ltd United Kingdom Civil AIGLE AZUR AAF ZI Aigle Azur France Civil ATLANTIC AAG KI Air Atlantique United Kingdom Civil ATLANTIC AAG Atlantic Flight Training United Kingdom Civil ALOHA AAH KH Aloha Air Cargo United States Civil BOREALIS AAI Air Aurora United States Civil ALFA SUDAN AAJ Alfa Airlines Sudan Civil ALASKA ISLAND AAK Alaska Island Air United States Civil AMERICAN AAL AA American Airlines United States Civil AM CORP AAM Aviation Management Corporation United States Civil -

Airline Schedules

Airline Schedules This finding aid was produced using ArchivesSpace on January 08, 2019. English (eng) Describing Archives: A Content Standard Special Collections and Archives Division, History of Aviation Archives. 3020 Waterview Pkwy SP2 Suite 11.206 Richardson, Texas 75080 [email protected]. URL: https://www.utdallas.edu/library/special-collections-and-archives/ Airline Schedules Table of Contents Summary Information .................................................................................................................................... 3 Scope and Content ......................................................................................................................................... 3 Series Description .......................................................................................................................................... 4 Administrative Information ............................................................................................................................ 4 Related Materials ........................................................................................................................................... 5 Controlled Access Headings .......................................................................................................................... 5 Collection Inventory ....................................................................................................................................... 6 - Page 2 - Airline Schedules Summary Information Repository: -

Appendix C Informal Complaints to DOT by New Entrant Airlines About Unfair Exclusionary Practices March 1993 to May 1999

9310-08 App C 10/12/99 13:40 Page 171 Appendix C Informal Complaints to DOT by New Entrant Airlines About Unfair Exclusionary Practices March 1993 to May 1999 UNFAIR PRICING AND CAPACITY RESPONSES 1. Date Raised: May 1999 Complaining Party: AccessAir Complained Against: Northwest Airlines Description: AccessAir, a new airline headquartered in Des Moines, Iowa, began service in the New York–LaGuardia and Los Angeles to Mo- line/Quad Cities/Peoria, Illinois, markets. Northwest offers connecting service in these markets. AccessAir alleged that Northwest was offering fares in these markets that were substantially below Northwest’s costs. 171 9310-08 App C 10/12/99 13:40 Page 172 172 ENTRY AND COMPETITION IN THE U.S. AIRLINE INDUSTRY 2. Date Raised: March 1999 Complaining Party: AccessAir Complained Against: Delta, Northwest, and TWA Description: AccessAir was a new entrant air carrier, headquartered in Des Moines, Iowa. In February 1999, AccessAir began service to New York–LaGuardia and Los Angeles from Des Moines, Iowa, and Moline/ Quad Cities/Peoria, Illinois. AccessAir offered direct service (nonstop or single-plane) between these points, while competitors generally offered connecting service. In the Des Moines/Moline–Los Angeles market, Ac- cessAir offered an introductory roundtrip fare of $198 during the first month of operation and then planned to raise the fare to $298 after March 5, 1999. AccessAir pointed out that its lowest fare of $298 was substantially below the major airlines’ normal 14- to 21-day advance pur- chase fares of $380 to $480 per roundtrip and was less than half of the major airlines’ normal 7-day advance purchase fare of $680. -

INTERNATIONAL CONFERENCE on AIR LAW (Montréal, 20 April to 2

DCCD Doc No. 28 28/4/09 (English only) INTERNATIONAL CONFERENCE ON AIR LAW (Montréal, 20 April to 2 May 2009) CONVENTION ON COMPENSATION FOR DAMAGE CAUSED BY AIRCRAFT TO THIRD PARTIES AND CONVENTION ON COMPENSATION FOR DAMAGE TO THIRD PARTIES, RESULTING FROM ACTS OF UNLAWFUL INTERFERENCE INVOLVING AIRCRAFT (Presented by the Air Crash Victims Families Group) 1. INTRODUCTION – SUPPLEMENTAL AND OTHER COMPENSATIONS 1.1 The apocalyptic terrorist attack by the means of four hi-jacked planes committed against the World Trade Center in New York, NY , the Pentagon in Arlington, VA and the aborted flight ending in a crash in the rural area in Shankville, PA ON September 11th, 2001 is the only real time example that triggered this proposed Convention on Compensation for Damage to Third Parties from Acts of Unlawful Interference Involving Aircraft. 1.2 It is therefore important to look towards the post incident resolution of this tragedy in order to adequately and pro actively complete ONE new General Risk Convention (including compensation for ALL catastrophic damages) for the twenty first century. 2. DISCUSSION 2.1 Immediately after September 11th, 2001 – the Government and Congress met with all affected and interested parties resulting in the “Air Transportation Safety and System Stabilization Act” (Public Law 107-42-Sept. 22,2001). 2.2 This Law provided the basis for Rules and Regulations for: a) Airline Stabilization; b) Aviation Insurance; c) Tax Provisions; d) Victims Compensation; and e) Air Transportation Safety. DCCD Doc No. 28 - 2 - 2.3 The Airline Stabilization Act created the legislative vehicle needed to reimburse the air transport industry for their losses of income as a result of the flight interruption due to the 911 attack. -

The Predatory Pricing Puzzle: Piecing Together a Unitary Standard

The Predatory Pricing Puzzle: Piecing Together a Unitary Standard Kimberly L. Herb∗ Table of Contents I. Introduction ................................................................................1572 II. Overview of Antitrust Law and Predatory Pricing......................1576 III. Predatory Pricing in Practice—Spirit Airlines, Inc. and AMR Corp. .................................................................................1580 A. Spirit Case History...............................................................1581 B. AMR Corp. Case History.....................................................1585 IV. The Economics of Predation—Evaluating Below-Cost Pricing ........................................................................................1588 A. Overview of the Economics of Predation ............................1589 B. Evaluation of Cost and Revenue in Spirit............................1591 C. Evaluation of Cost and Revenue in AMR Corp. ..................1596 V. Do the Spirit and AMR Corp. Holdings Constitute a Circuit Split?...............................................................................1599 A. Both Courts Tacitly Accept Marginal Cost..........................1599 B. Calculation of Marginal Cost...............................................1602 VI. A New Test for Predation...........................................................1604 A. Proposed Rule and Its Benefits............................................1604 B. Application to Spirit and AMR Corp. ..................................1607 C. Application -

The Evolution of U.S. Commercial Domestic Aircraft Operations from 1991 to 2010

THE EVOLUTION OF U.S. COMMERCIAL DOMESTIC AIRCRAFT OPERATIONS FROM 1991 TO 2010 by MASSACHUSETTS INSTME OF TECHNOLOGY ALEXANDER ANDREW WULZ UL02 1 B.S., Aerospace Engineering University of Notre Dame (2008) Submitted to the Department of Aeronautics and Astronautics in PartialFulfillment of the Requirementsfor the Degree of MASTER OF SCIENCE at the MASSACHUSETTS INSTITUTE OF TECHNOLOGY June 2012 0 2012 Alexander Andrew Wulz. All rights reserved. .The author hereby grants to MIT permission to reproduce and to distribute publicly paper and electronic copies of this thesis document in whole or in part in any medium now known or hereafter created. Signature of Author ..................................................................... .. ...................... Department of Aeronautr and Astronautics n n May 11, 2012 Certified by ............................................................................ Peter P. Belobaba Principle Research Scientist of Aeronautics and Astronautics / Thesis Supervisor A ccepted by ................................................................... Eytan H. Modiano Professor of Aeronautics and Astronautics Chair, Graduate Program Committee 1 PAGE INTENTIONALLY LEFT BLANK 2 THE EVOLUTION OF U.S. COMMERCIAL DOMESTIC AIRCRAFT OPERATIONS FROM 1991 TO 2010 by ALEXANDER ANDREW WULZ Submitted to the Department of Aeronautics and Astronautics on May 11, 2012 in PartialFulfillment of the Requirementsfor the Degree of MASTER OF SCIENCE IN AERONAUTICS AND ASTRONAUTICS ABSTRACT The main objective of this thesis is to explore the evolution of U.S. commercial domestic aircraft operations from 1991 to 2010 and describe the implications for future U.S. commercial domestic fleets. Using data collected from the U.S. Bureau of Transportation Statistics, we analyze 110 different aircraft types from 145 airlines operating U.S. commercial domestic service between 1991 and 2010. We classify the aircraft analyzed into four categories: turboprop, regional jet, narrow-body, and wide-body. -

January 2002 Airport Statistics

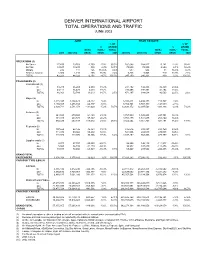

DENVER INTERNATIONAL AIRPORT TOTAL OPERATIONS AND TRAFFIC JUNE 2003 JUNE YEAR TO DATE % OF % OF % GRAND % GRAND INCR./ INCR./ TOTAL INCR./ INCR./ TOTAL 2003 2002 (10) DECR. DECR. 2003 2003 (9) 2002 (10) DECR. DECR. 2003 OPERATIONS (1) Air Carrier 27,433 29,763 -2,330 -7.8% 65.0% 161,686 164,827 -3,141 -1.9% 65.4% Air Taxi 13,547 13,238 309 2.3% 32.1% 79,589 74,980 4,609 6.1% 32.2% Military 236 111 125 112.6% 0.6% 587 506 81 16.0% 0.2% General Aviation 1,005 1,210 -205 -16.9% 2.4% 5,238 5,948 -710 -11.9% 2.1% TOTAL 42,221 44,322 -2,101 -4.7% 100.0% 247,100 246,261 839 0.3% 100.0% PASSENGERS (2) Internationals (3) In 43,249 36,269 6,980 19.2% 237,792 192,333 45,459 23.6% Out 43,112 36,479 6,633 18.2% 233,405 192,301 41,104 21.4% TOTAL 86,361 72,748 13,613 18.7% 2.5% 471,197 384,634 86,563 22.5% 2.6% Majors (4) In 1,215,397 1,284,629 -69,232 -5.4% 6,338,411 6,494,178 -155,767 -2.4% Out 1,194,347 1,256,744 -62,397 -5.0% 6,354,761 6,503,330 -148,569 -2.3% TOTAL 2,409,744 2,541,373 -131,629 -5.2% 70.7% 12,693,172 12,997,508 -304,336 -2.3% 71.2% Nationals (5) In 341,085 279,940 61,145 21.8% 1,767,989 1,520,288 247,701 16.3% Out 341,345 283,878 57,467 20.2% 1,784,475 1,531,075 253,400 16.6% TOTAL 682,430 563,818 118,612 21.0% 20.0% 3,552,464 3,051,363 501,101 16.4% 19.9% Regionals (6) In 107,550 62,126 45,424 73.1% 515,646 280,887 234,759 83.6% Out 111,376 60,944 50,432 82.8% 521,556 282,518 239,038 84.6% TOTAL 218,926 123,070 95,856 77.9% 6.4% 1,037,202 563,405 473,797 84.1% 5.8% Supplementals (7) In 5,377 37,727 -32,350 -85.7% 34,295 146,112 -

January 2002 Airport Statistics

DENVER INTERNATIONAL AIRPORT DOMESTIC MARKET SHARES JULY 2000 VS. PREVIOUS MONTH AND PREVIOUS YEAR JULY 2000 JUNE 2000 JULY 1999 REVENUE REVENUE REVENUE PASS. MARKET PASS. MARKET PASS. MARKET AIRLINE IN AND OUT SHARE MONTH AGO SHARE YEAR AGO SHARE AIR WISCONSIN/UAX 212,067 6.15% 194,435 5.82% 238,359 6.80% AMERICAN 162,489 4.71% 128,412 3.84% 138,635 3.95% AMERICAN TRANS AIR 25,097 0.73% 26,346 0.79% 24,532 0.70% AMERICA WEST 41,109 1.19% 40,683 1.22% 33,273 0.95% BIG SKY AIRLINES 1,456 0.04% 1,451 0.04% 0 0.00% CASINO 690 0.02% 947 0.03% 398 0.01% CHAMPION AIR 9,166 0.27% 7,913 0.24% 7,754 0.22% CONTINENTAL 84,202 2.44% 80,175 2.40% 86,541 2.47% DELTA 197,424 5.72% 180,666 5.41% 184,041 5.25% FRONTIER AIRLINES 258,275 7.48% 252,734 7.56% 214,249 6.11% GREAT LAKES/UAX 66,874 1.94% 62,979 1.88% 65,202 1.86% MESA 0 0.00% 808 0.02% 322 0.01% MIAMI AIRLINES 0 0.00% 170 0.01% 0 0.00% MIDWEST EXPRESS 9,863 0.29% 7,561 0.23% 8,413 0.24% NORTHWEST 105,266 3.05% 89,945 2.69% 86,448 2.46% SUN WEST INTL 0 0.00% 112 0.00% 0 0.00% TWA 57,052 1.65% 53,561 1.60% 46,496 1.33% UNITED 2,099,116 60.83% 2,100,652 62.86% 2,282,701 65.08% US AIRWAYS 69,673 2.02% 61,852 1.85% 54,270 1.55% VANGUARD AIRLINES 51,161 1.48% 50,286 1.50% 34,413 0.98% TOTALS 3,450,980 100.00% 3,341,688 100.00% 3,507,544 100.00% DOMESTIC MARKET SHARE JULY 2000 (1.7%) TWA (3.1%) NORTHWEST (7.5%) FRONTIER AIRLINES (5.7%) DELTA (2.4%) CONTINENTAL (1.2%) AMERICA WEST (4.7%) AMERICAN (1.3%) OTHER (8.1%) UNITED EXPRESS (60.8%) UNITED (1.5%) VANGUARD AIRLINES (2.0%) US AIRWAYS DENVER INTERNATIONAL AIRPORT TOTAL OPERATIONS AND TRAFFIC JULY 2000 JULY YEAR TO DATE % OF % OF % GRAND % GRAND INCR./ INCR./ TOTAL INCR./ INCR./ TOTAL 2000 1999 (9) DECR. -

PFC Quarterly Status Report - Revenue and Expenditures Activity Thru 03/31/2017 No Change Since 2016 Q4

PORT OF SEATTLE - STIA PFC Quarterly Status Report - Revenue and Expenditures Activity thru 03/31/2017 No change since 2016 Q4 Total Collection Authority $2,167,378,460 Approved for Collection Approved for Use Approved Applications "Impose" "Use" Application 1 (Amended) $27,911,096 $27,911,096 Application 2 (Amended) $48,790,226 $48,790,226 Application 3 (Amended) $292,882,278 $292,882,278 Application 4 (Amended) $1,642,074,742 $1,642,074,742 Application 7 $155,720,118 $155,720,118 Total Authority $2,167,378,460 $2,167,378,460 Current Quarter Cumulative PFC Revenue Received $19,304,184 $1,236,738,380 +/+++ Interest Earned $462,911 $53,795,884 Total - PFC Revenue Received $19,767,095 $1,290,534,264 N/C Application 1 Expenditures $0 $27,911,096 Application 2 Expenditures $0 $48,790,226 Application 3 Expenditures $0 $168,329,620 * PFC Const Fund B Debt Service Pmts (03390) $0 $76,890,266 ***/++/++++ Revenue Bond Fund Debt Service Pmts Offset $0 $10,178,982 Total Application 3 Expenditures $0 $255,398,868 Application 4 Expenditures $0 $261,631,147 ** PFC Const Fund A Debt Service Pmts (03380) $0 $109,450,102 * PFC Const Fund B Debt Service Pmts (03390) $0 $154,567,473 ***/++/++++ Revenue Bond Fund Debt Service Pmts Offset $8,776,360 $265,017,667 Total Application 4 Expenditures $8,776,360 $790,666,389 Application 7 Expenditures $0 $15,000,000 ++++ Revenue Bond Fund Debt Service Pmts Offset $0 $15,038,753 Total Application 7 Expenditures $0 $30,038,753 Total Expenditures $8,776,360 $1,152,805,332 Unliquidated Revenue $10,990,735 $137,728,932 -

January 2002 Airport Statistics

DENVER INTERNATIONAL AIRPORT TOTAL OPERATIONS AND TRAFFIC JULY 2003 JULY YEAR TO DATE % OF % OF % GRAND % GRAND INCR./ INCR./ TOTAL INCR./ INCR./ TOTAL 2003 2002 (10) DECR. DECR. 2003 2003 (9) 2002 (10) DECR. DECR. 2003 OPERATIONS (1) Air Carrier 29,305 31,196 -1,891 -6.1% 64.3% 190,991 196,023 -5,032 -2.6% 65.3% Air Taxi 14,745 13,792 953 6.9% 32.4% 94,334 88,772 5,562 6.3% 32.2% Military 238 122 116 95.1% 0.5% 825 628 197 31.4% 0.3% General Aviation 1,280 1,351 -71 -5.3% 2.8% 6,518 7,299 -781 -10.7% 2.2% TOTAL 45,568 46,461 -893 -1.9% 100.0% 292,668 292,722 -54 0.0% 100.0% PASSENGERS (2) Internationals (3) In 48,898 34,996 13,902 39.7% 286,690 227,329 59,361 26.1% Out 41,668 31,347 10,321 32.9% 275,073 223,648 51,425 23.0% TOTAL 90,566 66,343 24,223 36.5% 2.4% 561,763 450,977 110,786 24.6% 2.6% Majors (4) In 1,314,755 1,348,462 -33,707 -2.5% 7,653,166 7,842,640 -189,474 -2.4% Out 1,315,570 1,346,222 -30,652 -2.3% 7,670,331 7,849,552 -179,221 -2.3% TOTAL 2,630,325 2,694,684 -64,359 -2.4% 70.5% 15,323,497 15,692,192 -368,695 -2.3% 71.1% Nationals (5) In 373,546 309,111 64,435 20.8% 2,143,734 1,829,399 314,335 17.2% Out 376,944 308,041 68,903 22.4% 2,163,661 1,839,116 324,545 17.6% TOTAL 750,490 617,152 133,338 21.6% 20.1% 4,307,395 3,668,515 638,880 17.4% 20.0% Regionals (6) In 121,339 64,390 56,949 88.4% 636,985 345,277 291,708 84.5% Out 121,725 63,685 58,040 91.1% 643,281 346,203 297,078 85.8% TOTAL 243,064 128,075 114,989 89.8% 6.5% 1,280,266 691,480 588,786 85.1% 5.9% Supplementals (7) In 7,236 44,869 -37,633 -83.9% 41,531 190,981 -

An Integrative Assessment of the Commercial Air Transportation System Via Adaptive Agents

AN INTEGRATIVE ASSESSMENT OF THE COMMERCIAL AIR TRANSPORTATION SYSTEM VIA ADAPTIVE AGENTS A Dissertation Presented to The Academic Faculty by Choon Giap Lim In Partial Fulfillment of the Requirements for the Degree Doctor of Philosophy School of Aerospace Engineering Georgia Institute of Technology December 2008 Copyright c 2008 by Choon Giap Lim AN INTEGRATIVE ASSESSMENT OF THE COMMERCIAL AIR TRANSPORTATION SYSTEM VIA ADAPTIVE AGENTS Approved by: Dr. Dimitri N. Mavris, Advisor Dr. Daniel Schrage School of Aerospace Engineering School of Aerospace Engineering Georgia Institute of Technology Georgia Institute of Technology Dr. Jung-Ho Lewe Mr. Kurt Neitzke School of Aerospace Engineering Langley Research Center Georgia Institute of Technology National Aeronautics and Space Ad- ministration (NASA) Dr. Hojong Baik Department of Civil, Architectural and Environmental Engineering Missouri University of Science and Technology Date Approved: August 22, 2008 To my family, for their love, patience, and unwavering support iii ACKNOWLEDGEMENTS I would like to extend thanks to my adviser, Dr. Dimitri Mavris, who has provided invaluable advice, encouragement, and support throughout the years. To Dr. Jung- Ho Lewe, for his guidance in the research work for this dissertation. To Mr. Kurt Neitzke, Dr. Hojong Baik, and Dr. Daniel Schrage, for sharing their wealth of knowledge. To Dr. Daniel DeLaurentis and Dr. Elena Garcia for their mentorship during my early years at Georgia Tech. I would like to also thank my friends, Eunsuk, Timothy, Xin Yuan, and Joseph, who have helped carry me along in this journey, shared with me their knowledge and most importantly their friendship. Most importantly, I owe what I have achieved today to the unwavering support from my parents, Victor and Anne, who have given me the inspiration and confidence from the very beginning and continued to support me till the end. -

Predation, Competition and Antitrust Law: Turbulence in the Airline Industry Paul Stephen Dempsey

Journal of Air Law and Commerce Volume 67 | Issue 3 Article 4 2002 Predation, Competition and Antitrust Law: Turbulence in the Airline Industry Paul Stephen Dempsey Follow this and additional works at: https://scholar.smu.edu/jalc Recommended Citation Paul Stephen Dempsey, Predation, Competition and Antitrust Law: Turbulence in the Airline Industry, 67 J. Air L. & Com. 685 (2002) https://scholar.smu.edu/jalc/vol67/iss3/4 This Article is brought to you for free and open access by the Law Journals at SMU Scholar. It has been accepted for inclusion in Journal of Air Law and Commerce by an authorized administrator of SMU Scholar. For more information, please visit http://digitalrepository.smu.edu. PREDATION, COMPETITION & ANTITRUST LAW: TURBULENCE IN THE AIRLINE INDUSTRY* PAUL STEPHEN DEMPSEY** TABLE OF CONTENTS I. INTRODUCTION .................................. 688 II. EMPIRICAL EVIDENCE OF PREDATION ......... 692 A. HUB CONCENTRATION .......................... 692 B. MEGACARRIER ALLIANCES ....................... 700 C. EXAMPLES OF PREDATORY PRICING By MAJOR AIRLINES ........................................ 702 1. Major Network Airline Competitive Response To Entry By Another Major Network Airline ...... 715 a. Denver-Philadelphia: United vs. U SA ir .................................. 716 b. Minneapolis/St. Paul - Cleveland: Northwest vs. Continental ............. 717 2. Major Network Airline Competitive Response To Entry By Southwest Airlines .................. 718 a. St. Louis-Cleveland: TWA vs. Southwest .............................. 719 * Copyright © 2002 by the author. The author would like to thank Professor Robert Hardaway for his contribution to the portion of this essay addressing the essential facility doctrine. The author would also like to thank Sam Addoms and Bob Schulman, CEO and Vice President, respectively, of Frontier Airlines for their invaluable assistance in reviewing and commenting on the case study contained herein involving monopolization of Denver.