Annual Report 2008

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

External Borkers List

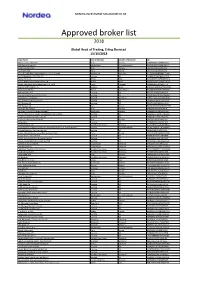

NORDEA INVESTMENT MANAGEMENT AB Approved broker list 2018 Global Head of Trading, Erling Skorstad 15/10/2018 Legal Name City of Domicile Country of Domicile LEI ABG Sundal Collier ASA Oslo Norway 2138005DRCU66B8BNY04 ABN Amro Group NV Amsterdam The Netherlands BFXS5XCH7N0Y05NIXW11 Arctic Securities AS Oslo Norway 5967007LIEEXZX4RVS72 Aurel BGC SAS Paris France 5RJTDGZG4559ESIYLD31 Australia and New Zealand Banking Group Limited Melbourne Australia JHE42UYNWWTJB8YTTU19 AUTONOMOUS RESEARCH LLP London UK 213800LBM6PT85IGM996 Banca IMI S.p.A Milan Italy QV4Q8OGJ7OA6PA8SCM14 Banco Bilbao Vizcaya Argentaria S.A Bilbao Spain K8MS7FD7N5Z2WQ51AZ71 Banco Português de Investimento, S.A. (BPI) Porto Portugal 213800NGLJLXOSRPK774 BANCO SANTANDER S.A Madrid Spain 5493006QMFDDMYWIAM13 Bank Vontobel AG Zurich Switzerland 549300L7V4MGECYRM576 Barclays Bank PLC London UK G5GSEF7VJP5I7OUK5573 Barclays Capital Securities Limited London UK K9WDOH4D2PYBSLSOB484 Bayerische Landesbank Munich Germany VDYMYTQGZZ6DU0912C88 BCS Prime Brokerage Limited London UK 213800UU8AHE2B6QUI26 BGC Brokers LP London UK ZWNFQ48RUL8VJZ2AIC12 BNP Paribas SA Paris France R0MUWSFPU8MPRO8K5P83 Carnegie AS Norway Oslo Norway 5967007LIEEXZX57BC18 Carnegie Investment Bank AB (publ) Stockholm Sweden 529900BR5NZNQZEVQ417 China International Capital Corporation (UK) Limited London UK 213800STG3UV87MDGA96 Citigroup Global Markets Limited London UK XKZZ2JZF41MRHTR1V493 Clarksons Platou Securities AS Oslo Norway 5967007LIEEXZXA40G44 CLSA (UK) London UK 213800VZMAGVIU2IJA72 Commerzbank AG Frankfurt -

Gasselskabernes Oversigtskort Transmissions- Og Distributionsnet (Stål) Pr

Gasselskabernes oversigtskort Transmissions- og distributionsnet (stål) pr. 11. maj 2020 Skagen Energinets transmissionsledninger med MR-stationer Distributionsselskabets Ålbæk Hirtshals Tversted fordelingsledninger Horne Bindslev Jerup Tornby Nybro gasbehandlingsanlæg Bjergby Strandby Astrup Sindal Elling Lønstrup Kvissel Hjørring Egtved Kompressorstation Ravnshøj Frederikshavn Lendum Gærum Tårs Gaslager Løkken Vrå Øster Vrå Hørby Sæby Nettilsluttede biogasanlæg Jerslev Vesterø Havn Dybvad Saltum Brønderslev Hune Øster Brønderslev Flauenskjold Klokkerholm Voerså Pandrup Kås Tylstrup Agersted Evida Moseby HjallerupDronninglund Vognmagervej 14 · 8800 Viborg Aabybro Nørre Halne Grindsted Biersted Birkelse Vestbjerg Vadum Tlf.: 6225 9000 Hanstholm Brovst Halvrimmen Vodskov Klim Fjerritslev Ulsted Ræhr Frøstrup Skovsgård www.evida.dk Vester Hassing Gjøl Hou Gandrup Klitmøller Aalborg E-mail: [email protected] Østerild Aalborg Nors Klarup Frejlev Sønderholm Gistrup Hals Nibe Sennels Svenstrup Gudumholm Løgstør Godthåb Energinet Nørre Vorupør Sjørring Thisted Ferslev Øster Hornum Tonne Kjærsvej 65 · 7000 Fredericia Hundborg EllidshøjEllidshøj Kongerslev Snedsted Ranum Tlf.: 7010 2244 Støvring Blenstrup Sundby Overlade www.energinet.dk Koldby Suldrup Bælum Øster Jølby Hornum Skørping Nederby Vester Hornum Rebild Terndrup E-mail: [email protected] Bedsted Aars Øster Hurup Nykøbing Mors HaverslevHaverslev Farsø Arden Astrup Skelund Als Vestervig Hurup Glyngøre Durup Hadsund Thyborøn Roslev Hvalpsund Nørager Aalestrup Jebjerg Breum Gedsted Valsgård -

Vestbjerg Bakker 02854.00

02854.00 Afgørelser - Reg. nr.: 02854.00 Fredningen vedrører: Vestbjerg Bakker Domme Taksationskommissionen 08-09-1986 Naturklagenævnet Overfredningsnævnet 20-01-1965 Fredningsnævnet 10-09-1962 Kendelser Deklarafioner TAKSATIONSKOMMISSIONEN> TAKSATIONSKOMM ISSIONEN VEDRØRENDE NATURFREDNING ADRESSE: REG. NR. ~ SLf AMALIEGADE t3, t256 KØBENHAVN K e--LF. 01- tt 9565 • • Sag nr. 226. Fredning af arealer i Hammer-Vestbjerg Bakker. Genoptagelse af erstatningsspørgsmålet vedr. matr.nr. 3 b, 16 c Østbjerg, Hammer. Kendelse: (Meddelt den B. september 1986) e Ved kendelse afsagt den lo. september 1962 af fredningsnævnet e for Alborg amtsrådskreds frededes den bebyggede landbrugs- e ejendom matr.nr. 3 ~, 16 ~ Østbjerg, Hammer, tilhørende fabri- kant Poul E. Poulsen, København, samt en ubebygget landbrugs- lod matr.nr. 17 ibd. Fredningsbestemmelserne gik alene ud på, at der pålagdes ejen- dommene forbud mod terrænændringer i væsentlig grad og mod op- førelse af nogen art af bygninger; dog var det tilladt på matr. nr. 3 ~, 16 ~ under de påtaleberettigedes censur at opføre de for landbrugsdriften fornødne bygninger (lader, stalde m.v.). 2·35 2. Landbrugsejendommens bygninger var, bortset fra en forfalden ladebygning, beliggende på matr.nr. 3 c. Poul E. Poulsen havde under sagen oplyst, at han havde planer om at opføre en beboelsesbygning til udleje på matr.nr. 16 c for derved at styrke sin økonomi. Ejeren af matr.nr. 17 havde oplyst, at han agtede at sælge ejendommen til sommerhusbebyggelse eller helårsbeboelse. Det anføres i fredningskendelsen, at de fredede arealer i deres helhed er omfattet af bestemmelserne om skovbyggelin- jen i naturfredningslovens (lovbekendtgørelse nr. 194 af • 16. juni 1961) § 25, stk. 2, og at nævnet "ville ikke, så- fremt begæring om dispensation var blevet fremsat, have meddelt en sådan." Fredningsnævnet lod ejendommene vurdere af særligt udpegede vurderingsmænd, der anslog værdien af landbrugsejendommen til 40.000 kr., heraf 20.000 kr. -

Nye Byroller I Kommuneplanen - Kort Fortalt

NYE BYROLLER I KOMMUNEPLANEN - kort fortalt godt i gang med Kommuneplan 2009 Nye byrollerMiljøministeriet i kommuneplanen | Realdania Forord Aalborg Kommune byder på et bredt udvalg af spændende og attraktive oplandsbyer og enestående naturkva- liteter. Udviklingsmulighederne i den enkelte oplandsby bestemmes ikke mindst af evnen til at udnytte egne styrker og muligheder i det regionale bynetværk. Bystrukturen består udover Aalborg, af en række mellemstore byer som Nibe, Svenstrup, Storvorde, Hals og Vodskov samt mange mindre byer og landsbyer. Kommunalreformen har skabt anledning til at se nærmere på de mange oplandsbyer for at kunne udvikle byer, der tager udgangspunkt i dets befolkning, relationer, styrker og forskelligheder. Til det arbejde har Aalborg Kommune har modtaget støtte af Realdania til at udvikle et nyt bykoncept, der erstatter det tidligere bymønster i amtets og de 4 sammenlægningskommuners planlægning. Resultatet vil i Kommuneplan 2009 for Aalborg Kommune, der snart offentliggøres. Dette hæfte samler ”kort fortalt” op på nogle af de spændende resultater projektet ’Nye byroller i kommu- neplanlægningen’ har resulteret i. Projektet er udarbejdet i perioden 2007-09 og for mere information kan henvises til: Plan09’s hjemmeside www.plan09.dk/Aalborg Aalborg kommunes hjemmeside www.aalborgkommune.dk Ny byroller i kommuneplanen - kort fortalt Udgivet af | Aalborg Kommune med støtte fra Plan09 Styregruppe | Peter Mikkelsen, Jens-Erik Qourtrup, Jørn Hviid Carlsen og Mette Kristoffersen, Aalborg Kommune Arbejdegruppe | Jesper Schultz, -

Årsprogra M 2020

HALS ÅRSPROGRAM 2020 ÅRSPROGRAM 1 Generalforsamling og hasselnødder Onsdag d. 12. februar kl.19 Fjordparken 2, 9370 Hals Pris : 0 kr. medlem/ 50 kr ikke medlem Inkl. kaffe og brød Ingen tilmelding Kl.19 til ca. 19.30: Generalforsamling ifølge vedtægterne. Se næste side Kl. ca. 19.30: Inspirationsaften om hasselnødder ved Mabel Nielsen fra Loddebakken i Ulsted. I nøddeplantagen på Loddebakken i Ulsted dyrkes der 10 forskellige slags hasselnødder. De første nøddebuske blev plantet ud i 2003. Mabel vil for- tælle om tilblivelsen af hasselnøddeplantagen, om hasselnødders livscyklus og vækstbetingelser, og også lidt om hvad de kan bruges til. Se mere på www.loddebakken.dk 2 HAVESELSKABET HALS Generalforsamling 2020 onsdag d.12. februar Dagsorden 1. Valg af dirigent, stemmetællere og referent. 2. Bestyrelsens beretning om kredsens virksomhed i det forløbne år. 3. Aflæggelse af revideret regnskab til godkendelse. 4. Forelæggelse af kredsens budget og aktivitetsplan til orientering. 5. Indkomne forslag fra bestyrelse eller medlemmer. 6. Valg a. Medlemmer til bestyrelsen (Vælges for 2 år) På valg er Mona Pedersen og Kirsten Bengtson b. Bestyrelsessuppleant (vælges for 2 år) På valg er Karin Høj c. Revisor (vælges for 2 år) På valg er Dorthe Poulstrup d. Revisorsuppleant (vælges for 1 år ) På valg er Erik Winther e. Valg af delegerede til afdelingens delegeretmøder. ( vælges for 1 år) 7. Eventuelt. Med de nye vedtægter for Haveselskabet, kan man supplere bestyrel- sen helt op til 12 personer. Forslag der ønskes behandlet, skal meddeles skriftligt (pr. email) til formanden senest 8 dage før generalforsamlingens afholdelse. 3 David Austin og hans roser Onsdag d. -

4432341-6945660-1.Pdf

* Transporttid til GF1: Omsorg, sundhed og pædagogik Skagen# Kortet viser den korteste transporttid til en erhvervsskole, der tilbyder GF1: Omsorg, sundhed og pædagogik, for alle byer i Nordjylland med over 500 indbyggere. Den samlede transporttid beregnes fra afgangs- tidspunkt i by til ringetid på uddannelsesinstitutionen på en hverdag i * # * september 2019. # * # Ålbæk Tversted * Hirtshals# * k < 30 min # * # * Åbyen # * k # Horne 30 - 45 min Bindslev Jerup * Tornby # * Bjergby # * k 45 - 60 min # Strandby * # * # * # Astrup (Hjørring) * # 60 - 75 min # Sindal Elling # * * k # Lønstrup Hjørring Ravnshøj * SOSU Hjørring # 75 - 90 min Frederikshavn * # * k # Kilden Lendum * k 90 - 120 # Gærum Tårs # * * # * > 120 Løkken # k Vrå Østervrå * # !(Sæby D Ikke muligt Serritslev * # * # Jerslev ! SOSU Aalborg Dybvad * !(Saltum Brønderslev# (! Flauenskjold " SOSU Aars Hune Øster Brønderslev (! # !( SOSU Hjørring !(Pandrup !( Klokkerholm (! Voerså !(Kås !(Tylstrup (! Agersted # SOSU Hobro Dronninglund AabybroNørhalne !(Sulsted !(Hjallerup !( !( Asaa SOSU Thisted Birkelse !( !((!Grindsted !( " !( !(Biersted (! !( Vestbjerg (!Vadum Vodskov ! Techcollege, Rørdalsvej Hanstholm Halvrimmen (! ") (!!( !(Langholt Brovst !( Ræhr Fjerritslev !( ") Frøstrup ") Skovsgård Vester Hassing ") ! !(Ulsted (! Gjøl (Nørresundby !( (!(! ! !( Gandrup !(Hou Klitmøller ! Techcollege, Rørdalsvej ") Østerild SOSU Aalborg (!Aalborg Nors ") ") (!Klarup !Frejlev !( ( (!Storvorde Hals Sønderholm (!Gistrup !( !( (! Gudumholm Nibe Dall Villaby SOSU Thisted ") (!(!Svenstrup -

Annual Report 1998 Unidanmark Unibank Contents

Annual Report 1998 Unidanmark Unibank Contents Summary . 6 Financial review . 8 The Danish economy . 14 Business description . 15 Retail Banking . 15 Corporate Banking . 21 Markets . 23 Investment Banking . 25 Risk management . 26 Capital resources . 33 Employees . 35 Management and organisation . 37 Accounts Accounting policies . 42 The Unidanmark Group . 44 Unidanmark A/S . 50 Unibank A/S . 55 Notes . 59 Unidanmark’s Local Boards of Shareholders . 84 Unibank’s Business Forum . 85 Branches in Denmark . 86 International directory . 88 Notice of meeting . 90 Management Supervisory Board of Unidanmark Jørgen Høeg Pedersen (Chairman) Holger Klindt Andersen Laurids Caspersen Boisen Lene Haulrik* Steffen Hvidt* Povl Høier Mogens Hugo Jørgensen Brita Kierrumgaard* Kent Petersen* Mogens Petersen Keld Sengeløv * Appointed by employees Executive Board of Unidanmark Thorleif Krarup Supervisory Board of Unibank Unibank’s Supervisory Board has the same members as the Supervisory Board of Unidanmark. In addition, as required by Danish banking legisla- tion, the Danish Minister of Business and Industry has appointed one mem- ber of the Supervisory Board of Unibank, Mr Kai Kristensen. Executive Board of Unibank Thorleif Krarup (Chairman) Peter Schütze (Deputy Chairman) Christian Clausen Jørn Kristian Jensen Peter Lybecker Henrik Mogensen Vision We are a leading financial services company in Denmark with a prominent position in the Nordic market. We ensure our shareholders a return in line with the return of the best among comparable Nordic financial services companies. Through our customer focus, efficient business processes and technology we create customer satisfaction and attract new customers. This confirms the customers in their choice of bank. Unibank is an attractive workplace where team spirit and customer focus are important criteria for individual success. -

K O M M U N E P L a N Tillæg 8.009 Byudviklingsplan for Storvorde/Sejlflod

K O M M U N E P L A N Hovedstruktur Retningslinier Kommuneplanrammer Bilag Planredegørelse Lokalplaner Andre planer Tillæg 8.009 Byudviklingsplan for Storvorde/Sejlflod Aalborg Byråd godkendte den 12. september 2016 kommuneplantillæg 8.009 Byudviklingsplan for Storvorde/Sejlflod. Planen består af: Byudviklingsplan for Storvorde/Sejlflod Retningslinje 2.1.1 Egentlig byudvikling og byformål Retningslinje 7.1.3 Øvrige bymidter samt bydels- og lokalcentre Retningslinje 11.1.2 Grøn-blå Struktur Retningslinje 11.2.3 Øvrige landområder Retningslinie 11.2.4 Skovrejsningsområder Retningslinje 11.3.8 Økologiske forbindelser Retningslinje 11.4.1 Område A, Det nære kystlandskab Retningslinje 11.4.2 Område B, Planlagt kystlandskab Kommuneplanramme 8.1.B1 Storvorde By Kommuneplanramme 8.1.B2 Tofthøjbakken Kommuneplanramme 8.1.B3 Rødageren Kommuneplanramme 8.1.C1 Tofthøjvej Kommuneplanramme 8.1.H1 Industrivej Kommuneplanramme 8.1I1 Storvorde Øst Kommuneplanramme 8.1.O1 Kirken Kommuneplanramme 8.1.O2 Stationsvej Kommuneplanramme 8.1.O3 Skole Kommuneplanramme 8.1.O4 Specialarbejderskole Kommuneplanramme 8.1.O5 Børnehaven Troldvej Kommuneplanramme 8.1.O6 Ny institution Kommuneplanramme 8.1.R1 Vandværksvej Kommuneplanramme 8.1.R2 Storvorde Vest Kommuneplanramme 8.1.R3 Sejlflod Banesti Kommuneplanramme 8.2.L1 Sejlflod Kommuneplanramme 8.2.O1 Spejderhus m.m. Kommuneplanramme 8.2.O2 Kirke Kommuneplanramme 8.2.D1 Kirkebakken Redegørelse til byudviklingsplan for Storvorde/Sejlflod Miljørapport til byudviklingsplan for Storvorde/Sejlflod Planen er først og fremmest tænkt som en digital plan. Det er dog op til dig selv, hvorvidt du ønsker at læse planen på skærmen, eller du vil udskrive den. Ønsker du en pdf-fil af det samlede tillæg, så tryk her. -

Quarterly Report for Q1 2008 for Spar Nord Bank DKK 183 Million in Pre-Tax Profits - Forecast for Core Earnings for the Year Repeated

To Stock Exchange Announcement OMX The Nordic Exchange Copenhagen No. 5, 2008 and the press For further information, contact: Lasse Nyby Chief Executive Officer Tel. +45 9634 4011 30 April 2008 Ole Madsen, Communications Manager Tel. +45 9634 4010 Quarterly report for Q1 2008 for Spar Nord Bank DKK 183 million in pre-tax profits - forecast for core earnings for the year repeated • Annualized 18% return on equity before tax • Net interest income up 15% to DKK 313 million • Net income from fees, charges and commissions down 20% to DKK 104 million • Market-value adjustments reduced to DKK 8 million • Costs grew 11% • DKK 8 million recognized as net income due to reversed impairment of loans and advances and related items • Earnings from the trading portfolio and an extra payment regarding Totalkredit amount to DKK 37 million in total • Lending up 15%, and a 26% hike in deposits • Forecast for core earnings for the year repeated Spar Nord Bank A/S • Moody’s rating: C, A1, P-1 (unchanged, outlook stable) Skelagervej 15 Developments in Q1 2008 P. O. Box 162 • 13 consecutive quarterly periods with net growth in customers DK-9100 Aalborg • Net interest income DKK 13 million up on Q4 2007 • Net income from fees, charges and commissions in line with Q3 and Q4 2007 results Reg. No. 9380 • Sustained strong credit quality level – reporting recognition of net income from Telephone +45 96 34 40 00 impairment of loans, advances, etc. for the 10th consecutive quarterly period Telefax + 45 96 34 45 60 • Business volume at same level as at end-2007 Swift spno dk 22 • Leasing activities continue to develop on a very satisfactory note • Interest margin widening at a moderate pace www.sparnord.dk • Wider yield spread between Danish mortgage-credit bonds and government bonds means distinctively lower market-value adjustments and loss on earnings from invest- [email protected] ment portfolios • Improved excess coverage relative to strategic liquidity target CVR-nr. -

Waste to Energy in Aalborg a Historical Perspective of Global Warming Impact Based on Life Cycle Assessment

Waste to Energy in Aalborg A Historical Perspective of Global Warming Impact based on Life Cycle Assessment Komal Habib Master Thesis Department of Development and Planning Aalborg University, Denmark. June 2011 Waste to Energy in Aalborg A Historical Perspective of Global Warming Impact based on Life Cycle Assessment Master Thesis Komal Habib MSc in Environmental Management Department of Development and Planning Aalborg University, Denmark Supervisor Prof. Per Christensen External Examiner Hanne Johnsen June 2011 No. of Copies: 3 No. of Pages: 99 Title Picture Source: http://www.microphilox.com/reference_01.htm Table of Contents Acknowledgements .................................................................................................................................. i List of Abbreviations .............................................................................................................................. ii Abstract .................................................................................................................................................. iii 1. Introduction ......................................................................................................................................... 1 1.1. Waste Management ...................................................................................................................... 1 1.2. History of Waste management Policy in EU ............................................................................... 2 1.3. Country Situation – Denmark -

12Thjune 2014 Helsinki Eba Clearing Shareholders

REPORT OF THE BOARD EBA CLEARING SHAREHOLDERS MEETING 12TH JUNE 2014 HELSINKI Contents 1. Introduction 3 2. The Company’s activities in 2013 5 2.1 EURO1/STEP1 Services 5 2.2 STEP2 Services 8 2.3 Operations 15 2.4 Legal, Regulatory & Compliance 18 2.5 Risk Management 20 2.6 Other corporate developments 21 2.7 The MyBank initiative 23 2.8 Activities of Board Committees 23 2.9 Corporate matters 26 2.10. Financial situation 29 3. The Company’s activities in 2014 32 3.1 EURO1/STEP1 Services 32 3.2 STEP2 Services 33 3.3 PRETA S.A.S. 35 3.4 Other relevant matters of interest 36 Appendix 1: Changes in EURO1/STEP1 participation 37 Appendix 2: List of participants in EURO1/STEP1 40 Appendix 3: List of direct participants in STEP2 45 Appendix 4: Annual accounts for 2013 53 2 EBA CLEARING SHAREHOLDERS MEETING // 12th June 2014 // Report of the Board 1. Introduction 2013 was marked by the major changeover that the SEPA migration end-date for euro retail payments of 1st February 2014 represented for payment service providers in the Eurozone and their customers. SEPA migration-related activities were also the top priority for EBA CLEARING throughout 2013. The Company continued to strengthen and enhance the STEP2 platform and intensified its customer support activities to assist its users across Europe in ensuring a disruption-free changeover to the SEPA instruments for their customers. SEPA migration affirmed the position of the STEP2 platform among the leading retail payment systems in Europe. The timely delivery of its SEPA Services as well as the processing capacity, operational robustness and rich functionality of the system made STEP2 the platform of first choice of many European communities in preparation of and during this migration. -

Fra Ry Af Ghetto Til Attraktivt Kvarter (Entré 30 Kr.)

2 Aalborg NORDJYSKE Stiftstidende Mandag 12. august 2013 Mandag 12. august 2013 NORDJYSKE Stiftstidende Aalborg 3 . Med nybyggeri, herunder også »»Vi kan ikke være bekendt, hvis vi fast- dagligvarebutikker,»» vil vi få et holder en mental og fysisk barriere ved Aalborg egentligt bymiljø, som samler folk. Universitetsboulevarden. Telefon 99353535 Fax 99353375 E-mail [email protected] Peder BALtzer NieLSeN, stadsarkitekt Peder BAltzer NielseN, stadsarkitekt Adresse Langager vej 1, 9220 Aal borg Ø { AALBORG: I forbindelse med afviklingen af Den Blå Fe- stival og Meutiviti Festival inviterer Artbreak Hotel til tre dage med jazz. Torsdag15. august kl. 20 går FLUX på sce- nen i gallerilokalerne i Danmarksgade, inden turen kom- mer til Kenneth Knudsen Trio lørdag 17. august kl. 14 Fra ry af ghetto til attraktivt kvarter (entré 30 kr.). Til slut spiller Westerhof/Poulsen søndag. STADSARKITEKT: Renovering, nybyggeri og nye adgangs- Forstadskonkurrencen ”City in between”, der i november sidste år LoKALdeBAt blev vundet af Team Vandkunsten, organiserer bydelen omkring veje vil gøre Aalborg Øst til bydel med tiltrækningskraft Astrupstien, som i forslaget er ført under Humlebakken og over Universitetsboulevarden. Arkivfoto: Torben Hansen Af Niels Brauer det samme. området, siger Peder Baltzer [email protected] - Vi vil også komme til at se Nielsen. Solstrålehistorie omend ikke højhuse, så byg- Ifølge vinderforslaget kan get opmærksomme på og vil bro over Universitetsboule- Af Kirsten Algren borger i skånejob, som gi- AALBORG: En del af det østlige gerier, der skyder lidt i vej- Aalborg Øst, der er på stør- det her, men uden en over- varden. Byrådsmedlem (DF), Halsvej 139A, ver en god livskvalitet for Aalborg er i dag på regerin- ret, så man får udnyttet de relse med Hobro, rumme ordnet plan er det nemt for- Odda var spået guld, men dagsformen rakte dog kun til bronze.