Energy Spectrum

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Annual Report and Accounts 2006 Annual Report and Accounts 2006

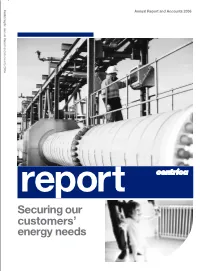

Centrica plc Annual Report and Accounts 2006 Annual Report and Accounts 2006 report Securing our customers’ energy needs Our vision is to become a leading integrated energy company in selected markets in order to maximise value to shareholders. In 2006 we focused on securing energy to meet our customers’ future needs. Our strategy Our strategy is to create a distinctive business model that delivers sustained profitability through the commodity cycle. We will achieve this by focusing on the following clear priorities: Transform British Gas Sharpen up the organisation and reduce costs Reduce risk by adding new sources of gas and power Build on our multiple growth platforms Our main activities Our upstream business Our downstream business We source energy internationally We supply energy to homes We find and produce gas predominantly in the UK We are Britain’s largest gas and electricity retailer, and have acquired licence blocks in Norway and supplying 49% of the residential gas market and 22% north and west Africa. We trade energy in the UK, of residential electricity. We are a growing North America and Europe and secure contracts force in North America, serving customers in five to bring gas to the UK. Canadian provinces and 15 US states. We generate energy We supply energy to businesses We generate electricity through our gas-fired power In Britain, we are a major supplier of gas and stations in the UK and US and through a growing electricity to the commercial sector. We also have portfolio of wind assets and purchasing agreements. customers in Belgium, the Netherlands and Spain. -

LDA Report Template

The Planning Act 2008 The Infrastructure Planning (Applications: Prescribed Forms and Procedure) Regulations 2009 Section 37(3)(c) Planning Act 2008 The Proposed Rookery South (Resource Recovery Facility) Order Consultation Report 4 August 2010 Document Reference: 7.1 Covanta Rookery South Limited LDA Design 7.1: Consultation Report 2 Covanta Rookery South Limited LDA Design Contents 0.0 Foreword ....................................................................................................... 11 1.0 Summary ....................................................................................................... 15 1.1. Introduction ............................................................................................. 15 1.2. Consultation Outcomes .......................................................................... 16 1.3. Conclusion .............................................................................................. 22 2.0 Introduction ................................................................................................... 25 2.1. Background ............................................................................................ 25 2.2. The Applicant: Covanta .......................................................................... 25 2.3. The Purpose of this Report ..................................................................... 26 2.4. The Proposed Project ............................................................................. 26 2.5. Covanta‟s Application Strategy .............................................................. -

SPALDING ENERGY EXPANSION CARBON CAPTURE READINESS FEASIBILITY STUDY March 2009

SPALDING ENERGY EXPANSION LTD SPALDING ENERGY EXPANSION CARBON CAPTURE READINESS FEASIBILITY STUDY March 2009 Prepared by Prepared for Parsons Brinckerhoff Ltd Spalding Energy Expansion Limited Amber Court 81 George Street William Armstrong Drive 3rd Floor Newcastle upon Tyne Edinburgh NE4 7YQ EH2 3ES UK Parsons Brinckerhoff Contents Page i of ii CONTENTS Page LIST OF ABBREVIATIONS 1 1. INTRODUCTION 1 2. APPROACH 2 3. LEGAL STATUS 3 3.1 Current arrangement 3 4. POWER PLANT 5 4.1 Sizing of CCS chain 5 5. CAPTURE PLANT TECHNOLOGY 7 6. STORAGE 10 6.1 Potential storage sites 10 6.2 Competing industrial factors 11 6.3 SEE project specific storage solutions 12 6.4 Potential future schemes 12 7. TRANSPORT 13 7.1 Additional CO2 sources 13 7.2 CO2 transportation by pipeline 14 7.2.1 Established technology 15 7.2.2 Risks 15 7.2.3 Legal and regulatory framework 15 7.2.4 Pipeline transport of CO2 from the SEE project 15 7.3 CO2 transportation by road 16 7.4 CO2 transportation by rail 17 7.5 Shipping 18 7.6 Compression 19 7.7 Liquefaction 19 8. INTEGRATION 20 8.1 Steam 20 8.2 Electricity 21 8.3 Space 22 8.4 Cooling 22 8.5 Summary 24 Document No. PBP/INT/SH/000003 SEE CCR FEASIBILITY REPORT.DOC/S3/2/K Parsons Brinckerhoff Contents Page ii Page 9. RETROFITTING CCS 25 9.1 Options for producing steam 25 9.1.1 Option 1 – LP steam turbine extraction 25 9.1.2 Option 2 – HP and/or IP steam turbine exhaust extraction 25 9.1.3 Option 3 – HRSG extraction 26 9.1.4 Option 4 – External steam supply 26 9.2 EA checklist for coal plant 26 9.2.1 Main requirements for CCGT plant 26 10. -

233 08 SD50 Environment Permitting Decision Document

Environment Agency Review of an Environmental Permit for an Installation subject to Chapter II of the Industrial Emissions Directive under the Environmental Permitting (England & Wales) Regulations 2016 Decision document recording our decision-making process following review of a permit The Permit number is: EPR/BK0701IW The Operator is: Spalding Energy Company Limited The Installation is: Spalding Power Station This Variation Notice number is: EPR/BK0701IW/V005 What this document is about Article 21(3) of the Industrial Emissions Directive (IED) requires the Environment Agency to review conditions in permits that it has issued and to ensure that the permit delivers compliance with relevant standards, within four years of the publication of updated decisions on best available techniques (BAT) conclusions. We have reviewed the permit for this installation against the revised BAT Conclusions for large combustion plant published on 17th August 2017. This is our decision document, which explains the reasoning for the consolidated variation notice that we are issuing. It explains how we have reviewed and considered the techniques used by the Operator in the operation and control of the plant and activities of the installation. This review has been undertaken with reference to the decision made by the European Commission establishing best available techniques (BAT) conclusions (‘BAT Conclusions’) for large combustion plant as detailed in document reference IEDC-7-1. It is our record of our decision-making process and shows how we have taken into account all relevant factors in reaching our position. It also provides a justification for the inclusion of any specific conditions in the permit that are in addition to those included in our generic permit template. -

Annual-Report-And-Accounts-2019.Pdf

Satisfying the changing needs of our customers Enabling the transition to a lower carbon future Annual Report and Accounts 2019 Group Snapshot Centrica plc is a leading international energy services and solutions provider focused on satisfying the changing needs of our customers and enabling the transition to a lower carbon future. The world of energy is changing rapidly and Centrica is now equipped to help customers transition to a lower carbon future, with capabilities and technologies to allow them to reduce their emissions. Therefore, we announced in July 2019 our intention to complete the shift towards the customer, by exiting oil and gas production. The Company’s two customer-facing divisions, Centrica Consumer and Centrica Business, are focused on their strengths of energy supply and its optimisation, and on services and solutions, with a continued strong focus on delivering high levels of customer service. Centrica is well placed to deliver for our customers, our shareholders and for society. We aim to be a good corporate citizen and an employer of choice. Technology is increasingly important in the delivery of energy and services to our customers. We are developing innovative products, offers and solutions, underpinned by investment in technology. We are targeting significant cost efficiency savings by 2022 to position Centrica as the lowest cost provider in its markets, consistent with our chosen brand positioning and propositions. Alongside our distinctive positions and capabilities, this will be a key enabler as we target -

Modified UK National Implementation Measures for Phase III of the EU Emissions Trading System

Modified UK National Implementation Measures for Phase III of the EU Emissions Trading System As submitted to the European Commission in April 2012 following the first stage of their scrutiny process This document has been issued by the Department of Energy and Climate Change, together with the Devolved Administrations for Northern Ireland, Scotland and Wales. April 2012 UK’s National Implementation Measures submission – April 2012 Modified UK National Implementation Measures for Phase III of the EU Emissions Trading System As submitted to the European Commission in April 2012 following the first stage of their scrutiny process On 12 December 2011, the UK submitted to the European Commission the UK’s National Implementation Measures (NIMs), containing the preliminary levels of free allocation of allowances to installations under Phase III of the EU Emissions Trading System (2013-2020), in accordance with Article 11 of the revised ETS Directive (2009/29/EC). In response to queries raised by the European Commission during the first stage of their assessment of the UK’s NIMs, the UK has made a small number of modifications to its NIMs. This includes the introduction of preliminary levels of free allocation for four additional installations and amendments to the preliminary free allocation levels of seven installations that were included in the original NIMs submission. The operators of the installations affected have been informed directly of these changes. The allocations are not final at this stage as the Commission’s NIMs scrutiny process is ongoing. Only when all installation-level allocations for an EU Member State have been approved will that Member State’s NIMs and the preliminary levels of allocation be accepted. -

Centrica Plc's Proposed Acquisition of TXU Europe's King's Lynn

September 2001 Centrica plc’s proposed acquisition of TXU Europe’s King’s Lynn and Peterborough power stations A consultation paper 1. Introduction Purpose of this document 1.1 This document: ♦ gives details of the proposed acquisition of King’s Lynn and Peterborough power stations by Centrica plc; ♦ explains the merger control process for this transaction; and ♦ requests comments on the regulatory issues arising from the proposed transaction. 1.2 Ofgem will make recommendations to the Director General of Fair Trading in relation to this acquisition. In order to allow comments to be considered, Ofgem needs to receive these not later than 5pm on Wednesday 19 September 2001. 2. Details of the proposed acquisition 2.1 TXU Europe Group plc (TXU) owns both the gas fired power station businesses at King’s Lynn and Peterborough. TXU is proposing to sell these businesses to Centrica plc (Centrica). 2.2 Both King’s Lynn and Peterborough are wholly owned subsidiaries of TXU - namely Anglian Power Generators Limited (APGL) and Peterborough Power Limited (PPL), respectively. Centrica has entered into a binding contract with TXU, PPL and APGL to acquire the leaseholds and other interests in the power station businesses of PPL and APGL. 2.3 Centrica announced the proposed acquisition on 24 August 2001. The parties have notified the completed transaction to the Office of Fair Trading (OFT) for a decision by the Secretary of State to clear the transaction or to refer it to the Competition Commission for further investigation. 3. Merger Control Process 3.1 This transaction falls within the scope of UK merger control law since the value of Centrica’s assets exceeds the £70 million threshold under the Fair Trading Act 1973 (FTA). -

Kier Group Plc Infrastructure Services Seminar 6 July 2016

Kier Group plc Infrastructure Services Seminar 6 July 2016 1 Haydn Mursell Chief Executive Kier Group plc 2 Disclaimer No representation or warranty, expressed or implied, is made or given by or on behalf of Kier Group plc (the “Company” and, together with its subsidiaries and subsidiary undertakings, the "Group" or any of its directors or any other person as to the accuracy, completeness or fairness of the information contained in this presentation and no responsibility or liability is accepted for any such information. This presentation does not constitute an offer of securities by the Company and no investment decision or transaction in the securities of the Company should be made on the basis of the information contained in this presentation. Not all of the information in this presentation has been audited. Further, this presentation includes or implies statements or information that are, or may deemed to be, "forward-looking statements". These forward-looking statements may use forward- looking terminology, including the terms "believes", "estimates", "anticipates", "expects", "intends", "may", "will" or "should". By their nature, forward-looking statements involve risks and uncertainties and recipients are cautioned that any such forward- looking statements are not guarantees of future performance. The Company's or the Group’s actual results and performance may differ materially from the impression created by the forward-looking statements or any other information in this presentation. The Company undertakes no obligation to update or revise any information contained in this presentation, except as may be required by applicable law or regulation. Nothing in this presentation is intended to be, or intended to be construed as, a profit forecast or a guide as to the performance, financial or otherwise, of the Company or the Group whether in the current or any future financial year. -

Notice of Variation and Consolidation with Introductory Note the Environmental Permitting (England & Wales) Regulations 2010

Notice of variation and consolidation with introductory note The Environmental Permitting (England & Wales) Regulations 2010 Spalding Energy Company Limited Spalding Power Station West Marsh Road Spalding Lincolnshire PE11 2BB Variation application number EPR/BK0701IW/V004 Permit number EPR/BK0701IW Spalding Power Station Spalding Power Station Permit number EPR/BK0701IW Introductory note This introductory note does not form a part of the notice. Under the Environmental Permitting (England & Wales) Regulations 2010 (schedule 5, part 1, paragraph 19) a variation may comprise a consolidated permit reflecting the variations and a notice specifying the variations included in that consolidated permit. Schedule 1 of the notice specifies that all the conditions of the permit have been varied and schedule 2 comprises a consolidated permit which reflects the variations being made and contains all conditions relevant to this permit. The requirements of the Industrial Emissions Directive (IED) 2010/75/EU are given force in England through the Environmental Permitting (England and Wales) Regulations 2010 (the EPR) (as amended). This Permit, for the operation of large combustion plant (LCP), as defined by articles 28 and 29 of the Industrial Emissions Directive (IED), is varied by the Environment Agency to implement the special provisions for LCP given in the IED, by the 1 January 2016 (Article 82(3)). The IED makes special provisions for LCP under Chapter III, introducing new Emission Limit Values (ELVs) applicable to LCP, referred to in Article 30(2) and set out in Annex V. As well as implementing Chapter III of IED, the consolidated variation notice takes into account and brings together in a single document all previous variations that relate to the original permit issued. -

Centrica Plc Annual Report and Accounts 2010

Centrica plc Registered office: Millstream, Maidenhead Road, Windsor, Berkshire SL4 5GD Company registered in England Report Annual and Wales No. 3033654 www.centrica.com and Accounts and 2010 Annual Report and Accounts 2010 Transporting personnel to the North Sea platforms UK: British Gas, Centrica Energy and Centrica Storage North America: Direct Energy PERFORMANCE ‡ ‡ ‡ Revenue Operating Profit* Employees 10% 16% 26% 7% 1% HIGHLIGHTS 4% 57% 51% 79% 1% Centrica’s main operations are in the UK and North America. 32% We have two types of business – downstream and upstream. 16% Downstream UK Upstream UK Storage UK North America Operating ◊ ‡ Adjusted earnings Group revenue Dividend per share Revenue‡ profit*‡ £m £m pence £m £m Downstream UK 1,297 14.30 22,423 21,963 1,111 12.80 1,122 20,872 12.20 Residential energy supply We are the biggest energy supplier in Britain’s domestic market. 8,355 742 11.57 911 9.92 Residential services We are Britain’s largest operator in the installation and maintenance of 16,065 15,893 707 domestic central heating and gas appliances. 1,464 241 Business energy supply We are Britain’s leading supplier of energy and related services and services to businesses. 2,906 233 06 07 08 09 10 06 07 08 09 10 06 07 08 09 10 Upstream UK With assets primarily in the UK and Norwegian continental shelf, our Financial highlights 2010 2009 Upstream gas and oil activities include gas and oil production, development and exploration. 864 581 ‡ Revenue £22.42bn £21.96bn We own and operate eight gas fired power stations, have a leading position Adjusted operating profit*‡ £2,390m £1,857m Power generation in offshore wind and a 20% stake in British Energy’s nuclear fleet. -

Satisfying the Changing Needs of Our Customers

Satisfying the changing needs of our customers Annual Report and Accounts 2018 Group Highlights Group Operational Group Financial Summary Performance (Year ended 31 December 2018) Total customer account holdings Group Revenue Return on average capital employed – Consumer (‘000) (ROACE) 2018 25,067 £29.7bn 13% 2017 25,316 2017: £28.0bn 2017: 14% 6% 1ppt Total customer account holdings Adjusted operating profit Statutory operating profit – Business (‘000) 2018 1,209 £1,392m £987m 2017 1,273 2017: £1,247m(1) 2017: £481m(1) 12% 105% Total customer gas consumption Adjusted earnings Statutory profit for the year (mmth) attributable to shareholders Total customer gas consumption 2018 12,465 £631m £183m 2017 11,630 2017: £693m(1) 2017: £328m(1) 9% 44% Total customer electricity Adjusted basic earning per share Statutory basic earning per share consumption (GWh) (EPS) Total customer electricity 2018 130,350 11.2p 3.3p 2017 133,869 2017: 12.5p(1) 2017: 5.9p(1) 10% 44% Direct Group headcount(2) Adjusted operating cash flow Statutory net cash flow Direct Group headcount from operating activities 2018 30,520 2017 33,138 £2,245m £1,934m 2017: £2,069m 2017: £1,840m 9% 5% Total recordable injury frequency Group net debt Net exceptional charge after taxation rate per 200,000 hours worked included in statutory profit Lost time injury frequency rate 2018 1.02† £2,656m £235m 2017 0.98 2017: £2,596m 2017: £476m 2% 51% (1) Restated for adoption of IFRS 15: revenue from contracts with customers. (2) Direct Group headcount excludes contractors, Read more about our Key Performance Indicators agency and outsourced staff. -

Satisfying the Changing Needs of Our Customers

Satisfying the changing needs of our customers Annual Report and Accounts 2016 We are an energy and services company. Everything we do is focused on satisfying the changing needs of our customers. Group Highlights GROUP FINANCIAL SUMMARY (Year ended 31 December) Group revenue Adjusted operating profit Adjusted earnings Adjusted basic earnings per share (EPS) £27.1bn £1,515m £895m 16.8p 2015: £28.0bn 2015: £1,459m 2015: £863m 2015: 17.2p ▼ 3% ▲ 4% ▲ 4% ▼ 2% Adjusted operating Group net debt Return on average capital Growth revenue cash flow employed (ROACE) £2,686m £3,473m 16% £194m 2015: £2,253m 2015: £4,747m 2015: 12% 2015: £114m ▲ 19% ▼ 27% ▲ 4ppt ▲ 70% Statutory operating Statutory profit/(loss) Net exceptional items Basic earnings per share profit/(loss) for the year attributable after taxation included to shareholders in statutory profit/(loss) £2,486m £1,672m £27m 31.4p 2015: £(857)m 2015: £(747)m 2015: £(1,846)m 2015: (14.9)p ● nm ● nm ● nm ● nm GROUP KEY OPERATIONAL PERFORMANCE INDICATORS Total customer Total customer Total customer Total customer account holdings – account holdings – gas consumption electricity consumption Home Business (mmth) (GWh) 26,196 1, 3 4 8 12,022 144,810 2015: 27,069 2015: 1,396 2015: 12,177 2015: 151,595 ▼ 3% ▼ 3% ▼ 1% ▼ 4% *year end, ‘000s *year end, ‘000s Direct Group headcount1 Total recordable 1 Direct Group headcount excludes contractors, agency injury frequency rate and outsourced staff. 2015 has been restated to include North America DE&P. 36,494 0.98 2015: 39,389 2015: 1.10 ▼ 7% ▼ 11% *year end *per 200,000 hours worked At a Glance Iain Conn Group Chief Executive GOOD FINANCIAL INVESTING IN NEW “We delivered our key objectives PERFORMANCE TECHNOLOGIES AND including improved safety CAPABILITIES performance, better customer service, and more innovative Adjusted operating Enhanced ‘Internet of offerings and solutions, while profit and adjusted Things’ platform, data repositioning the portfolio, earnings both up 4%.