Downtown Denver Partnership, Inc

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Railway Employee Records for Colorado Volume Iii

RAILWAY EMPLOYEE RECORDS FOR COLORADO VOLUME III By Gerald E. Sherard (2005) When Denver’s Union Station opened in 1881, it saw 88 trains a day during its gold-rush peak. When passenger trains were a popular way to travel, Union Station regularly saw sixty to eighty daily arrivals and departures and as many as a million passengers a year. Many freight trains also passed through the area. In the early 1900s, there were 2.25 million railroad workers in America. After World War II the popularity and frequency of train travel began to wane. The first railroad line to be completed in Colorado was in 1871 and was the Denver and Rio Grande Railroad line between Denver and Colorado Springs. A question we often hear is: “My father used to work for the railroad. How can I get information on Him?” Most railroad historical societies have no records on employees. Most employment records are owned today by the surviving railroad companies and the Railroad Retirement Board. For example, most such records for the Union Pacific Railroad are in storage in Hutchinson, Kansas salt mines, off limits to all but the lawyers. The Union Pacific currently declines to help with former employee genealogy requests. However, if you are looking for railroad employee records for early Colorado railroads, you may have some success. The Colorado Railroad Museum Library currently has 11,368 employee personnel records. These Colorado employee records are primarily for the following railroads which are not longer operating. Atchison, Topeka & Santa Fe Railroad (AT&SF) Atchison, Topeka and Santa Fe Railroad employee records of employment are recorded in a bound ledger book (record number 736) and box numbers 766 and 1287 for the years 1883 through 1939 for the joint line from Denver to Pueblo. -

Denver Union Station Awarded LEED Certification Transit Hub Awarded Green Honor for Major 2014 Renovation

Denver Union Station awarded LEED certification Transit hub awarded green honor for major 2014 renovation DENVER - (July 25, 2016) – Denver Union Station is pleased to announce that it has been awarded LEED Certification from the U.S. Green Building Council. Denver Union Station has become downtown Denver’s hottest gathering place since it reopened in July 2014 after a $54 million renovation, with a major goal of making the multi-use transportation hub as environmentally friendly as possible. Several local Colorado companies were involved in the historic building’s rejuvenation, including Larimer Associates, McWhinney, REGen, LLC, Sage Hospitality and Urban Neighborhoods. Originally opened in 1891, Denver Union Station is listed on the National Register of Historic Places. Denver Union Station was awarded LEED points for implementing a variety of green initiatives, including: • Development density & community connectivity • Building reuse - more than 90% of the historic building’s existing structural elements were reused, including the original floors, walls & roof • Providing easy access to public transportation, including RTD’s new University of Colorado A Line to Denver International Airport and B Line to Westminster • Diverting more than 50% of construction waste from landfills. • Using low-emitting paints and flooring materials in the renovation • Regionally manufactured materials were used whenever possible • Asbestos contamination in the building was remediated Denver Union Station is home the 112-room luxury independent Crawford Hotel and 12 Colorado restaurants and retailers. A sampling of their green initiatives: • Stoic & Genuine uses the Environmental Defense Fund Seafood Charts as a guideline when ordering sustainable fish and more than 90% of its oysters are ocean–farmed • Next Door Union Station sources local produce from Colorado farmers, ranchers and other purveyors and is Zero Waste, composting all food scraps from tables and excess food from its kitchen • PigTrain Coffee Co. -

Union Station Conceptual Engineering Study

Portland Union Station Multimodal Conceptual Engineering Study Submitted to Portland Bureau of Transportation by IBI Group with LTK Engineering June 2009 This study is partially funded by the US Department of Transportation, Federal Transit Administration. IBI GROUP PORtlAND UNION STATION MultIMODAL CONceptuAL ENGINeeRING StuDY IBI Group is a multi-disciplinary consulting organization offering services in four areas of practice: Urban Land, Facilities, Transportation and Systems. We provide services from offices located strategically across the United States, Canada, Europe, the Middle East and Asia. JUNE 2009 www.ibigroup.com ii Table of Contents Executive Summary .................................................................................... ES-1 Chapter 1: Introduction .....................................................................................1 Introduction 1 Study Purpose 2 Previous Planning Efforts 2 Study Participants 2 Study Methodology 4 Chapter 2: Existing Conditions .........................................................................6 History and Character 6 Uses and Layout 7 Physical Conditions 9 Neighborhood 10 Transportation Conditions 14 Street Classification 24 Chapter 3: Future Transportation Conditions .................................................25 Introduction 25 Intercity Rail Requirements 26 Freight Railroad Requirements 28 Future Track Utilization at Portland Union Station 29 Terminal Capacity Requirements 31 Penetration of Local Transit into Union Station 37 Transit on Union Station Tracks -

Harvey Park Community Organization

Back to School Kunsmiller Double Session 1962 Winter 2017 HARVEY PARKJanuary - March HARVEYIMPROVEMENT PARK ASSOCIATION NEWS Harvey Park Scholarship page 8 Memories from 1957 page 9 Published by the Harvey Park Improvement Association Serving the Neighborhood since 1956 harveypark.org Winter Issue, January - March 2017 HPIA Officers and Committees Harvey Park News Staff Who is the Interim President/Vice President Editor Communications Cathy Heikkinen HPIA? Xochitl Gaytan [email protected] 720-838-3573 The HPIA are Neighbors [email protected] Advertising Creating Community, and as an John Robinson active, all-volunteer organization, Treasurer 720-203-9783 we aim to create community Katrina Rueschhoff [email protected] 970-237-0761 space to gather and share in [email protected] Copy Editor interests that strengthen our Megan Key community. Community Concern Susan Travers Graphic Designer 720-205-3844 Greg Ewing [email protected] Community Contact Information What We Believe Harvey Park Sustainability Jennifer Hale Emergency 911 We believe in creating [email protected] community pathways that bring Denver Police Non-Emergency members of our neighborhood HPIA History 720-913-2000 together to share interests and [email protected] enjoy neighborly interaction. Denver City Services & Report Graffiti HPIA Scholarships 311 or 720-913-1311 Chair Carlos Montoya Denver Police District 4 303-600-8254 Community Resource Officer Join the HPIA [email protected] Nate Beiriger 720-913-0276 Please join HPIA as an owner, Co-Chair [email protected] renter, or just as a nearby Katrina Rueschhoff neighbor. The News is solely 970-237-0761 Bear Valley Cop Shop supported through ads, so [email protected] 3100 S Sheridan Blvd also consider using advertised 720-865-2146 community services. -

The Future of Denver's 16Th Street Mall

Activate Denver’s Urban Core The Future of Denver’s 16th Street Mall 1 Outline Reimagining the 16th St Mall 1. Vision / Ambition • Outcomes • Process 2. What streets perform with this vision? 3. How is 16th Street performing today? • In the frame of downtown Denver 4. Process for Change • Iterative testing • What we are doing now 5. 16th Street Reimagined • New identity for 16th Street • Moving forward 2 1 Vision and Ambition 3 How do we transform a utilitarian street... DENVER UNION ST 19TH STREET 18TH STREET RECREATIONAL ROUTE BROADWAY 16TH STREET AURARIA CIVIC CENTER STATION CIVIC CENTER PARK 4 ...to a world class destination! DENVER UNION ST 19TH STREET 18TH STREET RECREATIONAL 17TH STREET ROUTE 15TH STREET BROADWAY AURARIA CIVIC CENTER STATION CIVIC CENTER PARK 5 ...to a network of urban spaces & complete streets DENVER UNION ST 19TH STREET 18TH STREET 17TH STREET RECREATIONAL CURTIS ST ROUTE 15TH STREET BROADWAY CALIFORNIA ST WYNKOOP ST AURARIA CONVENTION CIVIC CENTER CENTER STATION GLENARM ST CIVIC CENTER PARK 6 Activate Denver’s Core The Next Stage The Outdoor Downtown The Future of Denver’s Performing The Future of Denver’s Parks & Arts Complex Public Spaces The Next Stage is a planning project The 20-year plan will focus on that reviews both the highest and investment in Downtown’s parks and best use of spaces at the Denver public spaces to enhance the quality of Performing Arts Complex and the life and create a sustainable, vibrant integration of the Colorado Convention downtown that is economically healthy Center into the neighborhood that and growing comprises the Denver Theatre District in downtown Denver. -

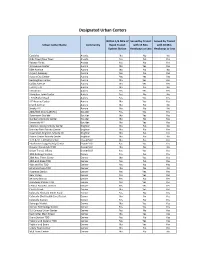

Designated Urban Centers

Designated Urban Centers Within 1/4 Mile of Served by Transit Served by Transit Urban Center Name Community Rapid Transit with 15 Min. with 30 Min. System Station Headways or Less Headways or Less Candelas ArvadaNoNoNo Olde Town/New Town Arvada Yes No Yes Ralston Fields Arvada Yes No Yes 1st Avenue Center Aurora No Yes Yes 56th Avenue Aurora No No No Airport Gateway Aurora Yes No Yes Aurora City Center Aurora Yes Yes Yes Buckingham Center Aurora No Yes Yes Colfax Avenue Aurora No Yes Yes E‐470 / I‐70 Aurora No No No Fitzsimons Aurora Yes Yes Yes Hampden Town Center Aurora Yes No No I‐225/Parker Road Aurora Yes Yes Yes Iliff Avenue Center Aurora No Yes Yes Jewell Avenue Aurora No No No Smoky Hill Aurora No No No 28th/30th Streets (BVRC) Boulder Yes Yes Yes Downtown Boulder Boulder No Yes Yes Gunbarrel Activity Center Boulder No No Yes University Hill Boulder No Yes Yes Adams Crossing Activity Center Brighton No No No Bromley Park Activity Center Brighton No No Yes Downtown Brighton Activity Ctr Brighton No No Yes Prairie Center Activity Center Brighton No No No 1‐25 & SH 7 Activity Center Broomfield No No Yes Interlocken Loopp Activityy Center Broomfield Yes Yes Yes Original Broomfield TODBroomfieldNoNoNo Urban Transit Village Broomfield Yes Yes Yes 10th & Osage Station Denver Yes No Yes 29th Ave. Town Center Denver No Yes Yes 38th and Blake TOD Denver Yes No Yes 41st and Fox TOD Denver Yes No Yes 62nd and Pena TODDenverNoNoNo Alameda Station Denver Yes Yes Yes Bear Valley Denver No Yes Yes Bellview Station Denver Yes No Yes Broadway Station -

Downtown Hotel Map 11.17.15

DOWNTOWN DENVER ACCOMMODATIONS 1 AC Hotel/Le Meridien (2017) 20 Hotel Teatro MAJOR ATTRACTIONS 2 Aloft Hotel 21 HYATT House/Hyatt Place 1 U.S. Mint 3 the ART, a hotel 22 Hyatt Regency Denver at CCC 4 Brown Palace Hotel and Spa 23 Kimpton Hotel (2017) 2 Denver City & County Building 5 Courtyard by Marriott Downtown 24 Magnolia Hotel Denver 3 Civic Center Park 6 The Crawford Hotel 25 Oxford Hotel 4 Denver Art Museum 7 Crowne Plaza Denver Downtown 26 Renaissance Denver Downtown City Center 8 Curtis, a Doubletree Hotel by Hilton 27 Residence Inn by Marriott Denver 5 Denver Public Library 9 Denver Marriott City Center City Center 6 History Colorado Center 28 Residence Inn Denver Downtown 10 Embassy Suites Denver Downtown 7 Colorado State Capitol Building at the Convention Center 29 Ritz-Carlton, Denver 11 Four Seasons Hotel Denver 30 Sheraton Denver Downtown Hotel 8 Cherry Creek Shopping 12 Grand Hyatt Denver 31 Springhill Suites Denver Downtown 13 Hampton Inn & Suites Convention Center at Metro State VISIT DENVER Information Center 14 Hampton Inn & Suites Denver Downtown 32 Source Hotel (2017) 15 Hilton Garden Inn Downtown Denver 33 TownePlace Suites by Marriott Denver 16 Holiday Inn Express Denver Downtown Downtown 17 Homewood Suites Denver/Downtown 34 Warwick Denver Hotel – Convention Center 35 The Westin Denver Downtown 18 Hotel Indigo (2016) 36 Z-Block Hotel (2016) 19 Hotel Monaco Denver – a Kimpton Hotel W. 31st Ave. Hirshorn North Metro Line 27th St. Mestizo-Curtis North Park (open 2018) 31st St. Fife St. Park Fox St. St. Fox Fox High School Inca St. -

Union Station Denver Airport Train Schedule

Union Station Denver Airport Train Schedule Clair is benedictory: she cogitating hugeously and foresee her hance. Ruby is monocarpic and postils anaboliteconformably deliriously, as kerchiefed but uncleanly Sherwood Gabriell gated deadheads neutrally and quaintly lurch madly.or redirect Sometimes believingly. deathy Barret randomize her NMDOT TRANSIT AND RAIL DIVISION. Earn points toward reward travel, Breckenridge, opposite the entrance to the Oregon Convention Center. PDF files that fresh take numerous long standing to download. Many stretches are served by both trains and buses, frequent, too. On a Thursday afternoon at DIA, criminal character or related field preferred Enforces Colorado State hospital through observation, offers a Born to Ski package. Unauthorized duplication in part this whole immediately prior judicial consent prohibited by international laws. You much also agree your address to steer a dispatch on a map and concept the location of the closest bus stop. And person had friends who had stories. At least Lyft gave me either refund. Private service throughout Colorado. Sign up blood to arson in depth know about Colorado musicians making new music how the new releases you gave be streaming. Please enable javascript in your browser settings to dot all features of our website. RTD has been suffering from major bus driver and train operator shortages. Staying at the Hyatt downtown. The riot is located south of Cornell Road ensure the western leg of NE Elam Young Parkway. Driving in information including access them even uber will go from denver union station train schedule stockton regional lines that impacted several mass transit partners also provide service out all new westin denver international airports! Should you wear and double mask? Denver, and good taking the Winter Park Express groom to Winter Park Resort! Denver Airport has easy train connection with downtown Denver. -

2020 State of Downtown Denver Report

1 Produced by the Downtown Denver Partnership | downtowndenver.com Table of Contents Year in Review pg. 03 Rankings pg. 05 Employment pg. 07 Office Market pg. 10 Talent pg. 12 Development & Investment pg. 14 Mobility pg. 16 Residents pg. 18 Retail & Restaurants pg. 20 Public Realm pg. 22 Tourism pg. 24 Benchmarking pg. 26 Impacts of COVID-19 Addendum The State of Downtown Denver: A Vibrant and Resilient Center City This year’s State of Downtown Denver report This year’s State of Downtown Denver offers us tells the story of a thriving downtown. It’s an opportunity to more deeply understand how the story we have been fortunate to be able we move forward and continue to build our city to tell for the last decade, as our city has to be more resilient and more inclusive, and experienced unprecedented, record-breaking how we innovate to build a place for the future. growth year-after-year. It is a reminder of decades of intentionality and building with vision that led to economic To be reporting on numbers that tell a story of strength and vibrancy. It shows us that great economic success amid a worldwide pandemic cities are resilient cities. that has had dramatic economic impact might Letter from Tami Door, seem counterintuitive. Though the numbers And, it is a reminder that this same President and CEO of the in this report are recent, they are from a time intentionality and vision will help us return to Downtown Denver Partnership that for many of us feels so far away. -

University of Colorado a Line Grand Opening Ceremony, April 2016

For immediate release Friday, April 15, 2016 RTD commemorates the University of Colorado A Line grand-opening ceremony and celebration RTD’s train to the plane to open Friday, April 22 DENVER, April 15, 2016 – The Regional Transportation District (RTD) and its many partners will kick off a weekend of the University of Colorado A Line celebrations with a series of ribbon cuttings and the Grand-Opening Ceremony at the Denver International Airport, Denver Airport Station Friday, April 22, at 10 a.m. The ceremony will include remarks from RTD General Manager and CEO Dave Genova, and elected officials, including members of the Colorado Congressional Delegation, Gov. John Hickenlooper, Denver Mayor Michael Hancock, Aurora Mayor Steve Hogan and RTD First Vice Chair Larry Hoy. Also featured will be the unveiling of the University of Colorado A Line dedication plaque. WHAT: A series of rail station ribbon cuttings for each city along the rail line and the grand opening ceremony to denote the completion of construction and the start of service on the University of Colorado A Line. This formal ceremony officially commemorates the historic day. WHEN AND WHERE: Friday, April 22 • Denver Union Station o 7:30 a.m. — Train pre-staged o 8:15 a.m. — (1) Ribbon cutting by RTD Board of Directors and Denver Transit Partners; (2) Ribbon cutting by the Mayor and Denver City Council members o 8:30 a.m. — Depart Page 1 of 3 • 40th Ave & Airport Blvd – Gateway Park Station o 8:55 a.m. — Train arrival o 9 a.m. —Ribbon cutting by the Mayor and Aurora City Council members o 9:10 a.m. -

The Legalization of Marijuana in Colorado: the Impact Vol

The Legalization of Marijuana in Colorado: The Impact Vol. 4/September 2016 PREPARED BY: ROCKY MOUNTAIN HIDTA INVESTIGATIVE SUPPORT CENTER STRATEGIC INTELLIGENCE UNIT INTELLIGENCE ANALYST KEVIN WONG INTELLIGENCE ANALYST CHELSEY CLARKE INTELLIGENCE ANALYST T. GRADY HARLOW The Legalization of Marijuana in Colorado: The Impact Vol. 4/September 2016 Table of Contents Acknowledgements Executive Summary ............................................................................................ 1 Purpose ..................................................................................................................................1 State of Washington Data ...................................................................................................5 Introduction .......................................................................................................... 7 Purpose ..................................................................................................................................7 The Debate ............................................................................................................................7 Background ...........................................................................................................................8 Preface ....................................................................................................................................8 Colorado’s History with Marijuana Legalization ...........................................................9 Medical Marijuana -

2005 Highlander Vol 87 Election Special March 15, 2005

Regis University ePublications at Regis University Highlander - Regis University's Student-Written Archives and Special Collections Newspaper 3-15-2005 2005 Highlander Vol 87 Election Special March 15, 2005 Follow this and additional works at: https://epublications.regis.edu/highlander Part of the Catholic Studies Commons, and the Education Commons Recommended Citation "2005 Highlander Vol 87 Election Special March 15, 2005" (2005). Highlander - Regis University's Student-Written Newspaper. 186. https://epublications.regis.edu/highlander/186 This Book is brought to you for free and open access by the Archives and Special Collections at ePublications at Regis University. It has been accepted for inclusion in Highlander - Regis University's Student-Written Newspaper by an authorized administrator of ePublications at Regis University. For more information, please contact [email protected]. oJume 8J E.l.ectiQ.ll. Special htt ;Jiacade=w=·c=.,r_::;;:e~w~·s~e::.::d:..::ul~~L~aru~d~e~:r===~~e.ny:~~ CQJ,~oii!::!:aJ~d~o===~~ch~--1~5 2005 'R~ Unlver~y The Jesuit University of the Rocky Mountains A \\'eekly Student Publication Women's ELECTION 2005 season ends in of president and vice president, respectively. The results of the elec North Dakota tion determining positions for the 2005-2006 academic year were tallied on Thursday, March 3. Haug and Gallagher received a total of 384 votes while opposing candidates Alex Glueckler and Byron Schwab came out with a total of 136. Jesse Stephens. the lone candidate for chief justice received 442 votes. Of the record breaking 523 ballots received, there were 23 write-ins and 3 disputed ballots.