2011 Annual Report

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

TOKIO MARINE FINANCIAL SOLUTIONS LTD. (Incorporated with Limited Liability in the Cayman Islands) ¥400,000,000,000 Programme for the Issuance of Debt Instruments

Level: 6 – From: 6 – Tuesday, October 27, 2009 – 14:37 – eprint6 – 4145 Intro BASE PROSPECTUS TOKIO MARINE FINANCIAL SOLUTIONS LTD. (incorporated with limited liability in the Cayman Islands) ¥400,000,000,000 Programme for the Issuance of Debt Instruments This Base Prospectus has been approved by the United Kingdom Financial Services Authority (the “FSA”), which is the United Kingdom competent authority for the purposes of Directive 2003/71/EC (the “Prospectus Directive”) and relevant implementing measures in the United Kingdom, as a base prospectus issued in compliance with the Prospectus Directive and relevant implementing measures in the United Kingdom for the purpose of giving information with regard to the issue of debt instruments (“Instruments”) issued under the programme (the “Programme”) described in this Base Prospectus during the period of twelve months after the date hereof. An application has been made to admit such Instruments during the period of twelve months after the date hereof to listing on the Official List of the FSA and an application has been made to admit such Instruments to trading on the Regulated Market of the London Stock Exchange plc (the “London Stock Exchange”), which is an EEA Regulated Market (as defined below). The Programme also permits Instruments to be issued on the basis that they will not be admitted to listing, trading and/or quotation by any listing authority, stock exchange and/or quotation system or to be admitted to listing, trading and/or quotation by such other or further listing authorities, stock exchanges and/or quotation systems as may be agreed with Tokio Marine Financial Solutions Ltd (the “Issuer”). -

Integrated Annual Report CORPORATE PHILOSOPHY

2018 Integrated Annual Report CORPORATE PHILOSOPHY With customer trust as the foundation for all its activities, Tokio Marine Group continually strives to raise corporate value. Through the provision of the highest quality products and services, Tokio Marine Group aims to deliver safety and security to all our customers. By developing sound, profitable and growing businesses throughout the world, Tokio Marine Group will fulfill its mandate to shareholders. Tokio Marine Group will continue to build an open and dynamic corporate culture that enables each and every employee to demonstrate his or her creative potential. Acting as a good corporate citizen through fair and responsible management, Tokio Marine Group will broadly contribute to the development of society. We will be there for our customers, playing our part in society in times of need. We will balance our strength as an organization with compassion as individuals, looking beyond profit to deliver fully on our commitments. Through our collective efforts, we will strive to be a Good Company, living up to the trust placed in us. CONTENTS 2 What’s Tokio Marine Group 2 139-Year History 4 Current Strengths 5 Financial and Non-Financial Highlights Integrated Annual Report 2018 6 Tokio Marine Group’s Value Creation Model 8 Management Strategy Section 9 Message from the President and Group CEO 14 Explanation of Management Strategies by Group CFO 20 Aligned Group Management 22 Message from Group CRO 24 Message from Group CSSO and Group CDO 26 Message from Group CRSO and Group Co-CRSO 28 -

Tokio Marine Holdings, Inc

Tokio Tokio Marine Holdings, Inc. Annual Report 2008 Annual Report 2008 http://www.tokiomarinehd.com/ “Tokio Marine Holdings Annual Report 2008” Uses FSC Approved Paper The raw material of the Forest Stewardship Council (FSC) approved paper used in this annual report is lumber harvested from forests that have been properly managed and grown according to the afforestation-nurturing-deforestation cycle. The forest from which this paper comes was grown with its surrounding eco-system taken into full consideration. In this annual report we have used this eco-friendly FSC-approved paper as a result of our desire to support the preserva- tion of forests, which benefit the public in such numerous ways as by absorbing CO2. Printed in Japan Member of Financial Accounting Standards Foundation WorldReginfo - b2f92b7f-c93a-43ff-9e40-23504b4f6836 TokioMarineH_08AR表紙0920.indd 1 08.9.26 5:39:56 PM Kunio Ishihara Chairman Shuzo Sumi President With customer trust at the base of all of its activities, Tokio Marine Holdings seeks to ensure the appropriate disclosure of com- pany information by demonstrating business operations with high level of fairness and transparency while pursuing the drastic business renovation of the entire Tokio Marine Group. “Tokio Marine Holdings Annual Report 2008” describes the current management status of the Group including the busi- ness results for the year ended March 31, 2008. We hope this report will help you understand Tokio Marine Holdings and its group companies. Corporate Symbol The dynamic helicoid-shaped fi gure represents innovation and creativity to anticipate the future, while gently embracing and supporting our customers and the earth. -

News Release: Announcement Of

May 24, 2007 Mitsubishi Heavy Industries, Ltd. Nippon Yusoki Co., LTD. Announcement of strengthening ownership relationship and promoting alliance Mitsubishi Heavy Industries, Ltd. (MHI) and Nippon Yusoki Co., Ltd. (Nichiyu) will strengthen the alliance in forklift business. Accordingly, Nichiyu will issue new shares via the Third Party Allocation, total amount of 4.2 billion yen, MHI will underwrite all of them and, consequently, MHI will become the largest shareholder of Nichiyu with 20% of the shares. MHI and Nichiyu currently have reciprocal sales agreement for Japanese market, by which MHI supplies Mitsubishi branded IC trucks to Nichiyu distribution network and Nichiyu supplies Nichiyu branded electric trucks to MHI distribution network. This time, by strengthening the alliance and cooperation each other, MHI and Nichiyu aim to be the industry leader. 1. Reason and details of the alliance Although there is significant growth in Asian countries, forklift industry is, in general, matured industry and there is trend of industry re-formation that some major players have sold their forklift business to either financial or strategic players. Under the circumstances, MHI and Nichiyu strengthen alliance relationship further in order to survive in forklift industry that is getting matured. As a part of the tighter relationship, MHI will increase its ownership of Nichiyu and strengthen ownership relation as well. (Current MHI’s ownership of Nichiyu is approx. 7.7%.) The alliance will be on the global basis. MHI, who has strong market position in IC truck segment, and Nichiyu, who is electric truck specialist and has strong distribution network in Japan, will complement each other and accelerate the collaboration activities in order to become leading company in forklift industry, who will be supported by stakeholders i.e. -

(Page 1 of 2) J.D. Power Asia Pacific Reports: Customer Retention

J.D. Power Asia Pacific Reports: Customer Retention Improves as Satisfaction with Claims Handling Increases Sony Life Insurance Ranks Highest in Customer Satisfaction With both Life Support Insurance and Medical Benefit Insurance TOKYO: 19 March 2014 — Customer satisfaction with insurance payment claims has increased for a second consecutive year, and continuous improvement in satisfaction with the claims process drives higher customer retention rates, according to the J.D. Power Asia Pacific 2014 Japan Life Insurance Claims Satisfaction StudySM released today. Now in its fourth year, the study measures overall satisfaction among customers who completed life insurance payment or benefits claim procedures during the past 12 months based on three factors (in order of importance): interaction channel; settlement; and claim filing process. Overall satisfaction scores are derived from customer evaluations of attributes in each factor. Customer satisfaction with medical benefit insurance improves to 668 (on a 1,000-point scale) in 2014 from 657 in 2013. Furthermore, 32 percent of customers indicate they intend to renew their policy, up from 30 percent in 2013. “In addition to the overall industry trend, policy renewal intention has increased by 4 percentage points among insurance companies with substantial increases in satisfaction scores—at least 30 points—during the past two years,” said Chie Numanami, senior manager of the Services Emerging Industries Division at J.D. Power Asia Pacific. “Improving satisfaction with claims handling helps foster customer loyalty.” Numanami noted that the key driver of higher customer satisfaction is not whether or not an explanation is provided, but whether or not the explanation promotes customer understanding. -

香港知識產權公報hong Kong Intellectual Property

香港知識產權公報 Hong Kong Intellectual Property Journal 2013年11月22日 22 November 2013 公報編號 Journal No.: 555 公布日期 Publication Date: 22-11-2013 分項名稱 Section Name: 目錄 Contents 目錄 Contents 根據專利條例第 20 條發表的指定專利申請記錄請求 Requests to Record Designated Patent Applications published under section 20 of the Patents Ordinance 1. 按國際專利分類排列 Arranged by International Patent Classification 2. 按發表編號排列 Arranged by Publication Number 3. 按申請編號排列 Arranged by Application Number 4. 按申請人姓名/名稱排列 Arranged by Name of Applicant 根據專利條例第 27 條發表批予標準專利 Granted Standard Patents published under section 27 of the Patents Ordinance 1. 按國際專利分類排列 Arranged by International Patent Classification 2. 按發表編號排列 Arranged by Publication Number 3. 按申請編號排列 Arranged by Application Number 4. 按專利所有人姓名/名稱排列 Arranged by Name of Proprietor 1/398 公報編號 Journal No.: 555 公布日期 Publication Date: 22-11-2013 分項名稱 Section Name: 目錄 Contents 根據專利條例第 118 條發表批予短期專利 Granted Short-term Patents published under section 118 of the Patents Ordinance 1. 按國際專利分類排列 Arranged by International Patent Classification 2. 按發表編號排列 Arranged by Publication Number 3. 按申請編號排列 Arranged by Application Number 4. 按專利所有人姓名/名稱排列 Arranged by Name of Proprietor 根據專利條例(第 514 章)公布的其他公告 Other Notices Published under the Patents Ordinance (Cap. 514) 根據專利條例第 20 條發表後撤回,當作已予撤回或被拒的申請 Applications withdrawn, deemed to have been withdrawn, or refused, after publication under section 20 of the Patents Ordinance 根據專利條例第 39 條,標準專利因未繳續期費而停止有效 Standard Patents Ceased through Non-payment of Renewal Fees under section 39 of the Patents Ordinance 根據專利條例第 39(1)(b)條,標準專利 -

' Good Company '

T o b e a ‘ Good Company ’ To be a ‘Good Company’ Published In: September 2013 Published By: Global Human Resources Group, International Business Development Dept. Tokio Marine Holdings, Inc. Contact Person: Kaz Okamoto ([email protected]) Naho Imai ([email protected]) It has been over 130 years since the foundation of the Tokio Marine Group in 1879 as the first insurance Table of Contents company in Japan. From the time we started, global business has been integral to our operations and we currently have a presence in 37 countries and regions with operations in 456 cities. Through this network we provide safety and security to our customers throughout the world. 3 Currently there are approximately 40,000 employees Message from the President & CEO around the world, working to shape and grow the group. They represent a rich and diverse range of cultures, countries and backgrounds. To be able to leverage fully 5 the strengths of such diversity it is essential that we are all The History of the Tokio Marine Group working towards a single and shared vision. As the Tokio Marine Group we are committed always to 7 operating "for the benefit of customers, business partners and society". It is this very dedication that will ensure that Global Expansion in Recent Years customers will continue to choose our services and allow us to continue to grow in the next 50 or 100 years. This is only possible through the efforts of all employees to build 9 a Good Company. Worldwide Network This publication was prepared to be a guide that will help to lead the way as a Good Company. -

Tokio Marine Group Will Continue Taking on Challenges

2017 INTEGRATED ANNUAL REPORT WorldReginfo - e8a53897-488b-41a1-8dff-01214076d916 We will be there for our customers, playing our part in society in times of need. We will balance our strength as an organization with compassion as individuals, looking beyond profit to deliver fully on our commitments. Through our collective efforts, we will strive to be a Good Company, living up to the trust placed in us. In Times of Need When Venturing into a New Area We Want to Be a Strong and Reassuring Presence Integrated Annual Report 2017 WorldReginfo - e8a53897-488b-41a1-8dff-01214076d916 Always Mindful of This Spirit... Tokio Marine Group Will Continue Taking on Challenges Tokio Marine Holdings 1 WorldReginfo - e8a53897-488b-41a1-8dff-01214076d916 Tokio Marine Group Corporate Philosophy With customer trust as the foundation for all its activities, Tokio Marine Group continually strives to raise corporate value. Through the provision of the highest quality products and services, Tokio Marine Group aims to deliver safety and security to all our customers. By developing sound, profi table and growing businesses throughout the world, Tokio Marine Group will fulfi ll its mandate to shareholders. Tokio Marine Group will continue to build an open and dynamic corporate culture that enables each and every employee to demonstrate his or her creative potential. Acting as a good corporate citizen through fair and responsible management, Tokio Marine Group will broadly contribute to the development of society. 2 Integrated Annual Report 2017 WorldReginfo - e8a53897-488b-41a1-8dff-01214076d916 -

Tokio Marine Holdings, Inc

Tokio Marine Holdings, Inc. Tokio Tokio Marine Holdings 2009 Annual Report Annual Report 2009 http://www.tokiomarinehd.com/ Tokio Marine Nichido Building Shinkan, 2-1, Marunouchi 1-chome, Chiyoda-ku, Tokyo 100-0005, Japan phone: +81-3-6212-3333 Member of Financial Accounting Standards Foundation Printed in Japan WorldReginfo - f3e90a66-22df-4cf8-91ff-c484d804e87e Overseas offi ces: Located in 399 cities in 36 countries and regions Branches of Tokio Marine & Nichido • Expatriate staff: 173 • Local staff: Approx. 14,600 Representative and Liaison Offi ces of Tokio Marine & Nichido Underwriting Agents of Tokio Marine & Nichido • Claims agents: Located in 250 countries and regions Subsidiaries and Affi liates Middle & Near East U.A.E. k Dubai ȣ Tokio Marine Middle East Limited (Dubai) v Al-Futtaim Development Services Co. (Dubai) Saudi Arabia k Jeddah, Riyadh and Al Khobar v Hussein Aoueini & Co., Ltd. (Jeddah, Riyadh and Al Khobar) ȣ Tokio Marine Saudi Arabia Limited (to be established) Tokio Marine Group Corporate Philosophy Bahrain ȣ The Arab-Eastern Insurance Co. Ltd E.C. (Manama) Turkey ȣ Allianz Sigorta A.S. (Istanbul) With customer trust as the foundation for all its activities, Tokio Marine Group continually strives ȣ Allianz Hayat ve Emeklilik A.S. (Istanbul) to raise corporate value. Oceania & Micronesia Australia k Sydney and Melbourne • Through the provision of the highest quality products and services, Tokio Marine Group aims to ȣ Tokio Marine Management (Australasia) Pty. Ltd. (Sydney, Melbourne and Adelaide) deliver safety and security to all our customers. New Zealand v IAG New Zealand Insurance Limited (Auckland) Guam k Guam • By developing sound, profi table and growing businesses throughout the world, Tokio Marine ȣ Tokio Marine Pacifi c Insurance Limited (Guam) Group will fulfi ll its mandate to shareholders. -

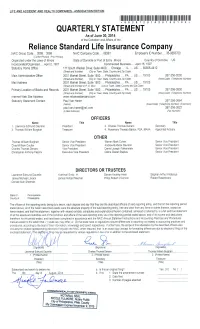

Premiums and Annuity Considerations for Life and Accident and Health Contracts Received in Advance Less $

Statement as of June 30, 2014 of the Reliance Standard Life Insurance Company ASSETS Current Statement Date 4 1 2 3 Net Admitted December 31 Nonadmitted Assets Prior Year Net Assets Assets (Cols. 1 - 2) Admitted Assets 1. Bonds........................................................................................................................................... ..........6,013,542,404 ................................... ..........6,013,542,404 ..........5,035,014,958 2. Stocks: 2.1 Preferred stocks................................................................................................................. ...............54,845,761 ................................... ...............54,845,761 ...............21,858,975 2.2 Common stocks................................................................................................................. .............237,534,652 ................................... .............237,534,652 .............165,920,124 3. Mortgage loans on real estate: 3.1 First liens............................................................................................................................ ...............33,654,687 ................................... ...............33,654,687 ...............31,586,285 3.2 Other than first liens........................................................................................................... ...............70,776,049 ................................... ...............70,776,049 ...............41,022,014 4. Real estate: 4.1 Properties occupied by the company -

Tokio Marine Holdings, Inc

Tokio Marine Holdings, Inc. Tokio Tokio Marine Holdings 2009 Annual Report Annual Report 2009 http://www.tokiomarinehd.com/ Tokio Marine Nichido Building Shinkan, 2-1, Marunouchi 1-chome, Chiyoda-ku, Tokyo 100-0005, Japan phone: +81-3-6212-3333 Member of Financial Accounting Standards Foundation Printed in Japan WorldReginfo - f3e90a66-22df-4cf8-91ff-c484d804e87e Overseas offi ces: Located in 399 cities in 36 countries and regions Branches of Tokio Marine & Nichido • Expatriate staff: 173 • Local staff: Approx. 14,600 Representative and Liaison Offi ces of Tokio Marine & Nichido Underwriting Agents of Tokio Marine & Nichido • Claims agents: Located in 250 countries and regions Subsidiaries and Affi liates Middle & Near East U.A.E. k Dubai ȣ Tokio Marine Middle East Limited (Dubai) v Al-Futtaim Development Services Co. (Dubai) Saudi Arabia k Jeddah, Riyadh and Al Khobar v Hussein Aoueini & Co., Ltd. (Jeddah, Riyadh and Al Khobar) ȣ Tokio Marine Saudi Arabia Limited (to be established) Tokio Marine Group Corporate Philosophy Bahrain ȣ The Arab-Eastern Insurance Co. Ltd E.C. (Manama) Turkey ȣ Allianz Sigorta A.S. (Istanbul) With customer trust as the foundation for all its activities, Tokio Marine Group continually strives ȣ Allianz Hayat ve Emeklilik A.S. (Istanbul) to raise corporate value. Oceania & Micronesia Australia k Sydney and Melbourne • Through the provision of the highest quality products and services, Tokio Marine Group aims to ȣ Tokio Marine Management (Australasia) Pty. Ltd. (Sydney, Melbourne and Adelaide) deliver safety and security to all our customers. New Zealand v IAG New Zealand Insurance Limited (Auckland) Guam k Guam • By developing sound, profi table and growing businesses throughout the world, Tokio Marine ȣ Tokio Marine Pacifi c Insurance Limited (Guam) Group will fulfi ll its mandate to shareholders. -

China's Insurance Companies' Efficiency: an Empirical Study Jiayan

China’s Insurance Companies’ Efficiency: An Empirical Study Jiayan ZHU Thesis submitted as partial requirement for the conferral of the degree of Doctor of Management Supervisor: Prof. Álvaro Rosa, Associate Professor, ISCTE University Institute of Lisbon Co-supervisor: Prof. Liping, Full Professor, University of Electronic Science and Technology of China, School of Management and Economics Sep. 2019 China’s Insurance Companies’ Efficiency:An Empirical Study Jiayan ZHU - Spine Spine – China’s Insurance Companies’ Efficiency: An Empirical Study Jiayan ZHU Thesis submitted as partial requirement for the conferral of the degree of Doctor of Management Supervisor: Prof. Álvaro Rosa, Associate Professor, ISCTE University Institute of Lisbon Co-supervisor: Prof. Liping, Full Professor, University of Electronic Science and Technology of China, School of Management and Economics Sep. 2019 Statement of honor Submission of master's dissertation or project work or doctoral thesis I the undersigned state on my honor that: - The work submitted herewith is original and of my exclusive authorship and that I have indicated all the sources used. - I give my permission for my work to be put through Safe Assign plagiarism detection tool. - I am familiar with the ISCTE-IUL Student Disciplinary Regulations and the ISCTE-IUL Code of Academic Conduct. - I am aware that plagiarism, self-plagiarism or copying constitutes an academic violation. Full name: Jiayan ZHU Course:Doctor of management Student number: Email address: [email protected] Telephone number:+86-18611661950 ISCTE-IUL, 15/5/2019 Signed Abstract Great achievements have been seen in China’s insurance industry in the past 20 years, however, inefficiency problems were prevailing as many insurance company only pursuing the expansion of the quantity, but not the increase of their key competitiveness.