University of Cincinnati

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Artemis Karamolegos Wines Descriptions for Wine Experts

ARTEMIS KARAMOLEGOS WINES DESCRIPTIONS FOR WINE EXPERTS Having its roots in the volcanic soil of Santorini and tradition that goes back to 1952, the winery of Artemis Karamolegos is one of the most dynamic and rapidly evolving wineries of Santorini. All its wines have been distinguished in several important International Wine Competitions. The winery has the most modern facilities for wine production, spaces for wine testing and a shop for wines and selected local products. Artemis Karamolegos had the innovative idea to combine the experience of a tour at the winery with lunch at the restaurant Aroma Avlis, the menu of which has the signature of the talented chef Christos Coskinas. In its spacious new yard offering view to the vineyard and the beaches of Monolithos and Avis, as well as in the dinning halls, you can taste the delicious Mediterranean and local dishes made with fresh, carefully selected local products, accompanied with wines from the winery. The history of the winery goes back to the 1952, where the grandfather, Artemis, was cultivating the vineyards in order to produce wine for his own family and later on, in order to sell it in the island and in the rest of Greece. Artemis Karamolegos, the grandson who succeeded his grandfather and his father at the winery of Exo Gonia, is an energetic young man full of passion for his Job. Since 2004 and until today, he managed to lead, miraculously, the family business many steps ahead very fast. In 2004, a turn to a modern and of a high quality production winery took place, with the production of a bottled, labeled and of a good quality wine named “SANTORINI”. -

Wine Map of the Peleponnese 2014

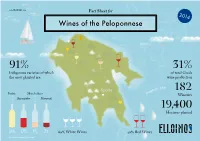

www.ELLOINOS.com Fact Sheet for 2014 Wines of the Peloponnese Patras Athens 91% 31% Indigenous varieties of which of total Greek the most planted are: wine production n Sea Sparta gea 182 Ae Roditis Moschofilero Wineries Agiorgitiko Mavroudi 19,400 Hectares planted 34% 17% 9% 7% 60% White Wines 40% Red Wines Information design by ideologio Protected Designation of Origin Wine Colors Muscat of Rio Patras Grape: Muscat Blanc Mavrodaphne of Patras Grapes: Mavrodaphne, Korinthiaki Athens Nemea Grape Agiorgitiko Muscat of Patras Mantinia Grape: Muscat Blanc Grape Moschofilero Patras Epidaurus Grape: Roditis Sea ean eg Kalamata A In the EU, schemes of geographical indications known as Protected Designation of Origin (PDO) and Protected Monemvassia Geographical Indication (PGI), promote and protect names of —Malvasia quality agricultural and food products. Amongst many other products, the names of wines are also protected by these Grapes: Monemvassia (min 51%), laws. Assyrtiko, Asproudes, Kydonitsa PDO products are prepared, processed, and produced in a given geographical area, using recognized know-how and therefore acquire unique properties. White Wine Sweet White Wine Red Wine Sweet Red Wine Indigenous grapes International grapes Region Note There are additional grape varieties allowed, but PGI products are closely linked to the geographical current plantings are small. area in which they are traditionally and at least White indigenous: Asproudes Patras, Aidani, partially manufactured (prepared, processed OR Assyrtiko, Athiri, Glikerithra, Goustolidi, Laghorthi, produced), and have specific qualities attributable to Migdali, Petroulianos, Potamissi, Robola, Rokaniaris, Skiadopoulo, Sklava, Volitsa Aspro. that geographical area, therefore acquiring unique properties. Depending on their geographical breadth, Red indigenous: Limniona, Skylopnichtis, Thrapsa, Voidomatis, Volitsa. -

Table of Contents

TABLE OF CONTENTS Sparkling & Champagne ............................. 3 White Wine .................................................. 4 Greece ........................................................................................4 Mediterranean ......................................................................5 Germany ...................................................................................5 Italy ................................................................................................5 Spain ........................................................................................... 6 France ........................................................................................ 6 From the New World .......................................................7 Rosé Wine ................................................ 8 Skin-Contact Wine ................................... 9 Red Wine .................................................10 Greece .............................................................................10 Mediterranean ...........................................................12 Italy ..................................................................................... 12 Spain .................................................................................. 13 France............................................................................... 13 From the New World ............................................ 14 Thrace Macedonia Epirius Thessaly Ionian Islands Aegean Peloponnese Islands Crete 2 SPARKLING -

WINES SELECTION Italian Law Quality Guarantee Marks

DRINK LIST OUR BEST WINES SELECTION Italian Law Quality Guarantee Marks D.O.C. Controlled Origin D.O.C.G. Controlled and Guaranteed Origin GREEK WINES WHITE WINES ESTATE P.D.O. OAK BARELS MORAITIS Winery: Moraitis Features: Dry white wine, 80% of the wine is fermented in a stainless steel vat with 6 months maturation on its lees. The rest Area of Origin: Paros , Greece 20% is fermented and matured for 6 months in new French oak barrels. Bright yellow gold color. Intense aromas of exotic fruits Grape Variety: 100% Monemvassia/ and citrus. The oak is well integrated and the crispness and elegan Vineyard Kamares ce of the wine easily dominates. Alcohol: 13 %vol. Price per Bottle 38 T S E KTIMA ALFA B E C C H OI Winery: Alpha Estate Area of Origin: Amyntaion, Greece Features: Bright white wine with intense flavor and rich aroma of citrus. Grape Variety: Sauvignon Blanc 100% Price per Bottle 29,5 Alcohol: 13,5 %vol. ESTATE MALAGOUSIA BIO MORAITIS Winery: Moraitis Features: Dry white wine, pale white yellow colour with green Area of Origin: Paros , Greece reflections. Rich in citrus and exotic fruit aromas. On the palate it is balanced, fruity, with notes of lemon peel and grapefruit. Grape Variety: Malagousia Price per Bottle 28,5 Alcohol: 12,5 %vol. CHARDONNAY GEROVASSILIU Winery: Gerovassiliu Area of Origin: Epanomi-Salonicco, Features: White wine aged in oak barrels, with a strong flavor and Greece characteristic with notes of citrus, dried fruit and vanilla. Grape Variety: Chardonnay Price per Bottle 33,5 Alcohol: 12,5 %vol. -

Phenolic Compounds As Markers of Wine Quality and Authenticity

foods Review Phenolic Compounds as Markers of Wine Quality and Authenticity Vakare˙ Merkyte˙ 1,2 , Edoardo Longo 1,2,* , Giulia Windisch 1,2 and Emanuele Boselli 1,2 1 Faculty of Science and Technology, Free University of Bozen-Bolzano, Piazza Università 5, 39100 Bozen-Bolzano, Italy; [email protected] (V.M.); [email protected] (G.W.); [email protected] (E.B.) 2 Oenolab, NOI Techpark South Tyrol, Via A. Volta 13B, 39100 Bozen-Bolzano, Italy * Correspondence: [email protected]; Tel.: +39-0471-017691 Received: 29 October 2020; Accepted: 28 November 2020; Published: 1 December 2020 Abstract: Targeted and untargeted determinations are being currently applied to different classes of natural phenolics to develop an integrated approach aimed at ensuring compliance to regulatory prescriptions related to specific quality parameters of wine production. The regulations are particularly severe for wine and include various aspects of the viticulture practices and winemaking techniques. Nevertheless, the use of phenolic profiles for quality control is still fragmented and incomplete, even if they are a promising tool for quality evaluation. Only a few methods have been already validated and widely applied, and an integrated approach is in fact still missing because of the complex dependence of the chemical profile of wine on many viticultural and enological factors, which have not been clarified yet. For example, there is a lack of studies about the phenolic composition in relation to the wine authenticity of white and especially rosé wines. This review is a bibliographic account on the approaches based on phenolic species that have been developed for the evaluation of wine quality and frauds, from the grape varieties (of V. -

Travel Itinerary for Your Trip to Greece Created by Mina Agnos

Travel Itinerary for your trip to Greece Created by Mina Agnos You have a wonderful trip to look forward to! Please note: Entry into the European countries in the Schengen area requires that your passport be valid for at least six months beyond your intended date of departure. Your Booking Reference is: ITI/12782/A47834 Summary Accommodation 4 nights Naxian Collection Luxury Villas & Suites 1 Luxury 2-Bedroom Villa with Private Pool with Breakfast Daily 4 nights Eden Villas Santorini 1 Executive 3-BR Villa with Outdoor Pool & Caldera View for Four with Breakfast Daily 4 nights Blue Palace Resort & Spa 1 2 Bedroom Suite with Sea View and Private Heated Pool for Four with Breakfast Daily Activity Naxos Yesterday & Today Private Transportation Local Guide Discover Santorini Archaeology & Culture Private Transportation Entrance Fees Local Guide Akrotiri Licensed Guide Knossos & Heraklion Discovery Entrance Fees Private Transportation Local Guide Spinalonga, Agios Nikolaos & Kritsa Discovery Entrance Fees Private Transportation Local Guide Island Escape and Picnic Transportation Private Helicopter from Mykonos to Naxos Transfer Between Naxos Airport & Stelida (Minicoach) Targa 37 at Disposal for 8 Days Transfer Between Naxos Port & Stelida (Minicoach) Santorini Port Transfer (Mini Coach) Santorini Port Transfer (Mini Coach) Transfer Between Plaka and Heraklion (Minivan) Transfer Between Plaka and Heraklion (Minivan) Day 1 Transportation Services Arrive in Mykonos. Private Transfer: Transfer Between Airport and Port (Minivan) VIP Assistance: VIP Port Assistance Your VIP Assistant will meet and greet you at the port, in which he will assist you with your luggage during ferry embarkation and disembarkation. Ferry: 4 passengers departing from Mykonos Port at 04:30 pm in Business Class with Sea Jets, arriving in Naxos Port at 05:10 pm. -

Santorini Is a Place of Tranquility and One of the Most Sought-Out Greek Isles Known for Its Beauty and Gracious Mediterranean Culture

Overview: Santorini is a place of tranquility and one of the most sought-out Greek isles known for its beauty and gracious Mediterranean culture. Perched along the cliffs of Imerovigli along a scenic hiking road that connects Oia to Fira, Andronis Concept welcomes guests to immerse in the island's serene surroundings, calming breeze, and breathtaking views overlooking the volcano framed by the protruding dramatic cliffs of the caldera. The views are alluring where the sky blends in with the deep blue waters of the Aegean Sea. In the evening, the views overlooking the sunset are mesmerizing. Its seclusion and intimate setting allow guests to engage in the moment. Each of the suites and villas boast private balconies and infinity pools where its subdued interiors infuse a traditional Santorini-style with bright contemporary touches. Here at Andronis Concept, the only limit is your imagination. Location: Set on the on the fringe of Imerovigli along a provincial road that connects Oia to Fira. The Santorini Airport (JTR) is a 12-minute drive away while the port is a 20-minute drive. Page 1 Accommodations: Designed to offer incredible sunset views, each 28-suites and villas across four categories is well- appointed and intimate boasting private balconies and infinity pools. Its subdued interiors infuse a traditional Santorini-style with bright contemporary touches. Cozy Suites (8) (377 sq. foot) Wake to spectacular views across Santorini’s volcanic caldera in this open-plan Cycladic-style suite, which boasts a private terrace and infinity pool. It can accommodate up to two people. Wet Allure Suites (8) (592 sq. -

Athens to Venice, Venice to Athens

STAR CLIPPERS SHORE EXCURSIONS Athens to Venice : Athens - Mykonos – Santorin – Katakolon - Corfu – Kotor – Dubrovnik – Korcula - Hvar - Cres - Venice Venice to Athens : Venice - Cres - Hvar - Dubrovnik – Kotor – Corfu – Katakolon - Santorin – Mykonos – Athens All tours are offered with English speaking guides. The length of the tours and time spent on the sites is given as an indication as it may vary depending on the road, weather, sea and traffic conditions and on the group’s pace. Minimum number of participants indicated per coach or group. Walking tours in Croatia can only be guided in one language. The level of physical fitness required for our activities is given as a very general indication without any knowledge of our passenger’s individual abilities. Broadly speaking to enjoy activities such as hiking, biking, snorkelling, boating or other activities involving physical exertion, passengers should be fit and active. Passengers must judge for themselves whether they will be capable of participating in and above all enjoying such activities. STAR CLIPPERS SHORE EXCURSIONS All information concerning excursions is correct at the time of printing. However Star Clippers reserves the right to make changes, which will be relayed to passengers during the Cruise Director’s onboard information sessions Excursion prices quoted may vary if entrance fees to sites and VAT increase in 2021. STAR CLIPPERS SHORE EXCURSIONS CROATIA CRES The best way to experience the city is to stroll through the Old Town. Here you will find a typically Medieval atmosphere with tall narrow buildings huddling together and a maze of winding streets. Emblems on the house fronts and doors indicate the trades of their former inhabitants – farm labourer, blacksmith, fisherman etc. -

Naxos and Santorini Walking in the Cyclades

SLOWAYS SRL - EMAIL: [email protected] - TELEPHONE +39 055 2340736 - WWW.SLOWAYS.EU WALKING type : Self-Guided level : duration : 8 days period: Apr May Jun Jul Aug Sep Oct code: GRSW016 Walking in the Cyclades: Naxos and Santorini - Greece 8 days, price from € 524 This journey includes two among the most beautiful islands of the Cyclades: Naxos, the island of contrasts, and Santorini, which do not need presentation. One week though green olive- orchards and the sharp contrast of deep blue Aegean Sea, which you will be able to enjoy from the summit of Mount Zas. You will discover the beauties of Naxos,the place where as the Greek mith tells Theseus abandoned Arianna: in this island, the biggest of the Cyclades, a lively night life coexists with heartfelt traditions. Santorini feels like no other place on heart: the whitewashed cube-shaped houses and bright blue doors and windos is famous worldwide. You will discover its secrets walking slowly through the narrow paved streets and steep cliffs, result of an explosion of the Thira Volcano thousands of years ago. To crown it all, you will enjoy the signature flavours of Greek kitchen: dishes based on fresh fish, seasoned with olive oil, a real local specialty. The tips of Valentina: Lose yourself among the narrow paved streets of Greek villages; Enjoy a spectacular sunset on the sea; Discover Akrotiri, the Greek Pompei; Immerse yourself in the fascination of Greek myths, from Zeus to the ancient city of Atlantis. Route Day 1 Arrival in Santorini; boat to Naxos Your trip starts at Santorini airport where you will be met by a taxi which will take you to the port for your ferry to Naxos. -

Vaso Wine List Final 2016-01-17

WINE LIST RED WINE Glass Bottle Greek Red Wines Limnio 2012 – Limnio "Organic" (Ktima Vourvoukeli Winery, Avdira, Greece) 12 36 Paros Moraitis Reserve 2009 – Mandilaria & Monemvassia (Paros, Greece) 13 39 Alexandra's Nostos 2012 – Syrah, Grenache, Mourvedre (Vatolakkos, Crete) 14 42 Red by JK 2011 – Cabernet , Merlot, Xynomavro (Mount Velventos, Greece) 12 38 Naoussea 2008 – Xynomavro (Naoussa, Greece) 12 36 Nemea 2010 – Agiorgitiko (Nemea, Greece) 12 36 King Of Hearts 2013 – Cabernet, Merlot (Nico Lazaridis Chateau, Drama, Greece) 11 36 The Black SheeP 2013 – Syrah, Merlot (Nico Lazaridis Chateau, Mount Pangeon, Greece) 11 36 Award Winning Greek Red Wines Amethystos 2011 – Cabernet , Merlot, Agiorgitiko (Lazardis Vineyards, Drama, Greece) - 49 Areti 2008 – Agiorgitko (Biblia Chora, Kokkinochori, Kavala, Greece) - 71 Magic Mountain (Μαγικό Βουνό) 2009 – Cabernet Sauv, Cabernet Franc (Drama, Greece) - 79 Avantis Estate 2011 – Mandilaria (Evia Island, Greece) - 51 Perpetuus 2007 – Sangiovese, Cabernet Sauv (Drama, Greece) - 81 Heritage 2012 – Maratheftiko (Keo Winery, Pitsillia, Cyprus) - 51 Italian Red Wines Rocche Costamagna Barbera D'Alba 2013 – Nebbiolo, Barbera (Piedmont, Italy) 13 39 San Vito Chianti 2013 – Sangiovese (Florence, Tuscany, Italy) 10 31 ValPolicella Classico SuPeriore 2012 – RiPasso (Verona, Italy) 12 36 Brancaia Chianti Classico Riserva 2011 – Sangiovese (DOCG, Tuscany, Italy) - 78 Ca’Bea del Maniero 2012 – Pinot Noir (Pavia, Italy) 11 33 Poggio al Tesoro Sondraia 2011 – Cabernet Sauv, Merlot, Cabernet Franc (Tuscany, -

Greece - Cyclades - Santorini - Imerovigli

Pantheon Apartments Greece - Cyclades - Santorini - Imerovigli location: 2 to 4 persons - shared pool – air condition Imerovigli 1 km black sandy beaches 2 persons: 1 living room 10 km 4 persons: 1 double bedroom – 1 bathroom with tub/ WC – 1 at a glance: living-/bedroom with kitchenette – 1 single bedroom – 1 shower/ baby bed/cot WC - safe – telephone/fax – Sat-TV – HIFI with CD player CD-Player DVD-Player all apartments: hair dryer breackfast – service – sauna – restaurant pets: NICHT erlaubt heating This well-maintained, luxurious villa estate is situated on top of the highchair spectacular Caldera between Imerovigli and the artist’s village of Oia. air condition The estate’s unique and peaceful location offers expansive, breathtaking sea view views of the island of Thirassia, the volcano Nea Kameni and out over mosquito nets the Aegean Sea. Here, the soft evening light turns the sunsets into an shared pool unforgettable experience. Pantheon offers three different types of safe box holiday apartments. Near the common area pool are the two-storey SAT/cable-TV apartments for four guests and the studio apartments for two. telephone The many small terraces of the buildings offer a variety of shady spots service included: right through the day. All accommodations have a direct view of the sea. daily breakfast and A generous breakfast of your choice is included in the price. If you cleaning service, airport require, the chef of the small restaurant will gladly prepare meals for transfers the guests, which can be served either by the pool or in the apartment. Of course, there is daily room service. -

Curriculum Studies Guide

TECHNOLOGICAL EDUCATIONAL INSTITUTE OF ATHENS FACULTY OF FOOD TECHNOLOGY & NUTRITION DEPARTMENT OF OENOLOGY & BEVERAGE TECHNOLOGY CURRICULUM STUDIES GUIDE ACADEMIC YEAR 2010-2011 CURRICULUM FOR THE ACADEMIC YEAR 2010-2011 Contact Details: Address St. Spyridonos, 12210, Aigaleo Head of the Department Panagiotis Kaldis, Professor 210-5385503 Department Secretariat Eleni Zoulinou, Chief Secretary: Chrysso Bogiatzi 210-5385538 210-5385504 Fax 210-5385504 Department Secretariat Email [email protected] Department Email [email protected] Department Website www.teiath.gr/stetrod/oenology T.E.I. of Athens Website www.teiath.gr Curriculum Studies Guide Text: Elias Korkas, Assistant Professor Curriculum Studies Guide Editing: Chrysso Bogiatzi, Department Secretariat CURRICULUM FOR THE ACADEMIC YEAR 2010-2011 CONTENTS 1 HISTORY OF THE DEPARTMENT 1 2 CONTENT OF THE DEPARTMENT’S STUDIES 5 3 ORGANIZATION – ADMINISTRATION OF THE DEPARTMENT 12 4 DEPARTMENT STAFF 14 5 DEPARTMENT FACILITIES 16 6 RESEARCH ACTIVITIES – SEMINARS - WORKSHOPS 17 7 CURRICULUM 18 8 PRACTICAL TRAINING GUIDE 137 9 DISSERTATION GUIDE 139 CURRICULUM FOR THE ACADEMIC YEAR 2010-2011 TECHNOLOGICAL FACULTY OF FOOD TECHNOLOGY & NUTRITION EDUCATIONAL DEPARTMENT OF OENOLOGY & BEVERAGE TECHNOLOGY INSTITUTE OF ATHENS 1 HISTORY OF THE DEPARTMENT In Greece the provision of a comprehensive higher education course exclusively devoted to oenology has been a standing request of the wine industry since 1983, when the Technological Educational Institutes were first established. At that time a few courses in oenology or viticulture were taught at University Agricultural Faculties, in the Faculties of Food Technology of the TEI Institutes in Athens and Thessaloniki (oenology courses only) and at the Agricultural Technology Faculties of the TEI Institutes (viticulture courses only).