ZIMBABWE VULNERABILITY ASSESSMENT COMMITTEE (Zimvac)

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

(Ports of Entry and Routes) (Amendment) Order, 2020

Statutory Instrument 55 ofS.I. 2020. 55 of 2020 Customs and Excise (Ports of Entry and Routes) (Amendment) [CAP. 23:02 Order, 2020 (No. 20) Customs and Excise (Ports of Entry and Routes) (Amendment) “THIRTEENTH SCHEDULE Order, 2020 (No. 20) CUSTOMS DRY PORTS IT is hereby notifi ed that the Minister of Finance and Economic (a) Masvingo; Development has, in terms of sections 14 and 236 of the Customs (b) Bulawayo; and Excise Act [Chapter 23:02], made the following notice:— (c) Makuti; and 1. This notice may be cited as the Customs and Excise (Ports (d) Mutare. of Entry and Routes) (Amendment) Order, 2020 (No. 20). 2. Part I (Ports of Entry) of the Customs and Excise (Ports of Entry and Routes) Order, 2002, published in Statutory Instrument 14 of 2002, hereinafter called the Order, is amended as follows— (a) by the insertion of a new section 9A after section 9 to read as follows: “Customs dry ports 9A. (1) Customs dry ports are appointed at the places indicated in the Thirteenth Schedule for the collection of revenue, the report and clearance of goods imported or exported and matters incidental thereto and the general administration of the provisions of the Act. (2) The customs dry ports set up in terms of subsection (1) are also appointed as places where the Commissioner may establish bonded warehouses for the housing of uncleared goods. The bonded warehouses may be operated by persons authorised by the Commissioner in terms of the Act, and may store and also sell the bonded goods to the general public subject to the purchasers of the said goods paying the duty due and payable on the goods. -

Zimbabwe Rapid Response Drought 2015

Resident / Humanitarian Coordinator Report on the use of CERF funds RESIDENT / HUMANITARIAN COORDINATOR REPORT ON THE USE OF CERF FUNDS ZIMBABWE RAPID RESPONSE DROUGHT 2015 RESIDENT/HUMANITARIAN COORDINATOR Bishow Parajuli REPORTING PROCESS AND CONSULTATION SUMMARY a. Please indicate when the After Action Review (AAR) was conducted and who participated. The CERF After Action Review took place on 25 May 2016. The review brought together focal points from the following key sectors and agencies: Health and Nutrition: UNICEF and WHO, Agriculture: FAO, Food Security: WFP and WASH: UNICEF. Considering the importance of the lessons learnt element, some sectors which did not benefit from the funding did nevertheless participate in order to gain a better understanding of CERF priorities, requirements and implementation strategies. b. Please confirm that the Resident Coordinator and/or Humanitarian Coordinator (RC/HC) Report was discussed in the Humanitarian and/or UN Country Team and by cluster/sector coordinators as outlined in the guidelines. YES X NO Sector focal points were part of the CERF consultation from inception through to final reporting. In addition, a CERF update was a standing agenda item discussed during the monthly Humanitarian Country Team meetings. c. Was the final version of the RC/HC Report shared for review with in-country stakeholders as recommended in the guidelines (i.e. the CERF recipient agencies and their implementing partners, cluster/sector coordinators and members and relevant government counterparts)? YES X NO All -

Mopane Woodlands and the Mopane Worm: Enhancing Rural Livelihoods and Resource Sustainability

Mopane Woodlands and the Mopane Worm: Enhancing rural livelihoods and resource sustainability Final Technical Report Edited by Jaboury Ghazoul1, Division of Biology, Imperial College London Authors and contributors Mopane Tree Management: Dirk Wessels2, Member Mushongohande3, Martin Potgeiter7 Domestication Strategies: Alan Gardiner4, Jaboury Ghazoul Kgetsie ya Tsie Case Study: John Pearce5 Livelihoods and Marketing: Jayne Stack6, Peter Frost7, Witness Kozanayi3, Tendai Gondo3, Nyarai Kurebgaseka8, Andrew Dorward9, Nigel Poole5 New Technologies: Frank Taylor10, Alan Gardiner Choice experiments: Robert Hope11, Witness Kozanayi, Tendai Gondo Mopane worm diseases: Robert Knell12 Start and End Date 1 May 2001 – 31 January 2006 DFID Project Reference Number R 7822 Research Programme Forestry Research Programme (FRP) Research Production System Forest Agriculture Interface 1 Also ETH Zürich, Department of Environmental Sciences, ETH Zentrum CHN, Universitätstrasse 16, Zürich 8092, Switzerland 2 Department of Botany, university fo the North, South Africa 3 Forest Commission, Harare, Zimbabwe 4 Veld Products Research and Development, Gabarone, and Division of Biology, Imperial College London 5 Kgetsie ya Tsie, Tswapong Hills, Botswana 6 Imperial College London and University of Zimbabwe, Project Co-ordinator 7 Institute of Environmental Studies 8 Southern Alliance for Indigenous Resources 9 Imperial College London, Centre for Environmental Policy. 10 Veld Products Research and Development 11 University of Newcastle 12 Queen Mary College, University of London 1 Contents Executive Summary 3 Background 3 Project Purpose 6 Research Activities Section 1. Mopane tree ecology and management 7 Section 2.1 Mopane worm productivity and domestication 18 Section 2.2 Mini-livestock: Rural Mopane Worm Farming at the Household Level 34 Section 3. A case study of the Kgetsie ya Tsie community enterprise model for managing and trading mopane worms 59 Section 4. -

Bulawayo City Mpilo Central Hospital

Province District Name of Site Bulawayo Bulawayo City E. F. Watson Clinic Bulawayo Bulawayo City Mpilo Central Hospital Bulawayo Bulawayo City Nkulumane Clinic Bulawayo Bulawayo City United Bulawayo Hospital Manicaland Buhera Birchenough Bridge Hospital Manicaland Buhera Murambinda Mission Hospital Manicaland Chipinge Chipinge District Hospital Manicaland Makoni Rusape District Hospital Manicaland Mutare Mutare Provincial Hospital Manicaland Mutasa Bonda Mission Hospital Manicaland Mutasa Hauna District Hospital Harare Chitungwiza Chitungwiza Central Hospital Harare Chitungwiza CITIMED Clinic Masvingo Chiredzi Chikombedzi Mission Hospital Masvingo Chiredzi Chiredzi District Hospital Masvingo Chivi Chivi District Hospital Masvingo Gutu Chimombe Rural Hospital Masvingo Gutu Chinyika Rural Hospital Masvingo Gutu Chitando Rural Health Centre Masvingo Gutu Gutu Mission Hospital Masvingo Gutu Gutu Rural Hospital Masvingo Gutu Mukaro Mission Hospital Masvingo Masvingo Masvingo Provincial Hospital Masvingo Masvingo Morgenster Mission Hospital Masvingo Mwenezi Matibi Mission Hospital Masvingo Mwenezi Neshuro District Hospital Masvingo Zaka Musiso Mission Hospital Masvingo Zaka Ndanga District Hospital Matabeleland South Beitbridge Beitbridge District Hospital Matabeleland South Gwanda Gwanda Provincial Hospital Matabeleland South Insiza Filabusi District Hospital Matabeleland South Mangwe Plumtree District Hospital Matabeleland South Mangwe St Annes Mission Hospital (Brunapeg) Matabeleland South Matobo Maphisa District Hospital Matabeleland South Umzingwane Esigodini District Hospital Midlands Gokwe South Gokwe South District Hospital Midlands Gweru Gweru Provincial Hospital Midlands Kwekwe Kwekwe General Hospital Midlands Kwekwe Silobela District Hospital Midlands Mberengwa Mberengwa District Hospital . -

PLAAS RR46 Smeadzim 1.Pdf

Chrispen Sukume, Blasio Mavedzenge, Felix Murimbarima and Ian Scoones Faculty of Economic and Management Sciences Research Report 46 Space, Markets and Employment in Agricultural Development: Zimbabwe Country Report Chrispen Sukume, Blasio Mavedzenge, Felix Murimbarima and Ian Scoones Published by the Institute for Poverty, Land and Agrarian Studies, Faculty of Economic and Management Sciences, University of the Western Cape, Private Bag X17, Bellville 7535, Cape Town, South Africa Tel: +27 21 959 3733 Fax: +27 21 959 3732 Email: [email protected] Institute for Poverty, Land and Agrarian Studies Research Report no. 46 June 2015 All rights reserved. No part of this publication may be reproduced or transmitted in any form or by any means without prior permission from the publisher or the authors. Copy Editor: Vaun Cornell Series Editor: Rebecca Pointer Photographs: Pamela Ngwenya Typeset in Frutiger Thanks to the UK’s Department for International Development (DfID) and the Economic and Social Research Council’s (ESRC) Growth Research Programme Contents List of tables ................................................................................................................ ii List of figures .............................................................................................................. iii Acronyms and abbreviations ...................................................................................... v 1 Introduction ........................................................................................................ -

Zimbabwean Government Gazette, 8Th February, 1985 103

GOVERNMENT?‘GAZETTE Published by Autry £ x | Vol. LX, No, 8 f 8th FEBRUARY,1985 Price 30c 3 General Notice 92 of 1985, The service to operate as follows— Route 1: , 262] > * ROAD MOTOR TRANSPORTATION ACT [CHAPTER (a) depart Bulawayo Monday 9 am., arrive Beitbridge 3.15 p.m.; Applications in Connexion with Road Service Permits (b) depart Bulawayo. Friday 5 pm., arrive Beitbridge as 11.15 p.m. _ IN terms of subsection(4) of section 7 of the- Road Moter ‘(c) depart BulawayoB Saturday 10 am., arrive Beitbridge Transportation Act [Chapter 262], notice is hereby given that 13 ‘p. the applications detailed in the Schedule, for the issue or | (d) depart eitbridge Tuesday 8.40 a.m., astive Bulawayo amendment of road service its, have been received for the 3.30 p. consideration of the Control}ér of Road Motor Transportation. (e) depart Beitbridge Saturday 3.40 am., arrive Bulawayo Any personwishing to Object to any such application must - a.m} ‘lodge with the Controlle? of Road Motor Transportation, (f) depart’ Beitbridge Sunday 9.40 am., arrive Bulawayo P.O. Box 8332, Causeway— 4.30 p.m, ~ . : eg. (a) a notice; in writing, of his intention fo object, so as to - Route 2: No change. _* teach the Controller'ss office not later than the Ist March, Cc. R. BHana. ’ 1985; 0/284/84. Permit: 23891."Motor-omnibus. Passenger-capacity: (b) his objection and the groiinds therefor, on form R.M.T, 24, tozether with two copies thereof, so as to reach the Route: Bulawayo - Zyishavane - _Mashava - Masvingo - Controller’s office not later than the 22nd March, 1985. -

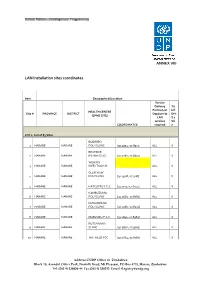

LAN Installation Sites Coordinates

ANNEX VIII LAN Installation sites coordinates Item Geographical/Location Service Delivery Tic Points (List k if HEALTH CENTRE Site # PROVINCE DISTRICT Dept/umits DHI (EPMS SITE) LAN S 2 services Sit COORDINATES required e LOT 1: List of 83 Sites BUDIRIRO 1 HARARE HARARE POLYCLINIC [30.9354,-17.8912] ALL X BEATRICE 2 HARARE HARARE RD.INFECTIO [31.0282,-17.8601] ALL X WILKINS 3 HARARE HARARE INFECTIOUS H ALL X GLEN VIEW 4 HARARE HARARE POLYCLINIC [30.9508,-17.908] ALL X 5 HARARE HARARE HATCLIFFE P.C.C. [31.1075,-17.6974] ALL X KAMBUZUMA 6 HARARE HARARE POLYCLINIC [30.9683,-17.8581] ALL X KUWADZANA 7 HARARE HARARE POLYCLINIC [30.9285,-17.8323] ALL X 8 HARARE HARARE MABVUKU P.C.C. [31.1841,-17.8389] ALL X RUTSANANA 9 HARARE HARARE CLINIC [30.9861,-17.9065] ALL X 10 HARARE HARARE HATFIELD PCC [31.0864,-17.8787] ALL X Address UNDP Office in Zimbabwe Block 10, Arundel Office Park, Norfolk Road, Mt Pleasant, PO Box 4775, Harare, Zimbabwe Tel: (263 4) 338836-44 Fax:(263 4) 338292 Email: [email protected] NEWLANDS 11 HARARE HARARE CLINIC ALL X SEKE SOUTH 12 HARARE CHITUNGWIZA CLINIC [31.0763,-18.0314] ALL X SEKE NORTH 13 HARARE CHITUNGWIZA CLINIC [31.0943,-18.0152] ALL X 14 HARARE CHITUNGWIZA ST.MARYS CLINIC [31.0427,-17.9947] ALL X 15 HARARE CHITUNGWIZA ZENGEZA CLINIC [31.0582,-18.0066] ALL X CHITUNGWIZA CENTRAL 16 HARARE CHITUNGWIZA HOSPITAL [31.0628,-18.0176] ALL X HARARE CENTRAL 17 HARARE HARARE HOSPITAL [31.0128,-17.8609] ALL X PARIRENYATWA CENTRAL 18 HARARE HARARE HOSPITAL [30.0433,-17.8122] ALL X MURAMBINDA [31.65555953980,- 19 MANICALAND -

Tendayi Mutimukuru-Maravanyika Phd Thesis

Can We Learn Our Way to Sustainable Management? Adaptive Collaborative Management in Mafungautsi State Forest, Zimbabwe. Tendayi Mutimukuru-Maravanyika Thesis committee Thesis supervisors Prof. dr. P. Richards Professor of Technology and Agrarian Development Wageningen University Prof. dr. K.E. Giller Professor of Plant Production Systems Wageningen University Thesis co-supervisor Dr. ir. C. J. M. Almekinders Assistant Professor, Technology and Agrarian Development Group Wageningen University Other members Prof. dr. ir. C. Leeuwis, Wageningen University Prof. dr. L.E. Visser, Wageningen University Dr. ir. K. F. Wiersum, Wageningen University Dr. B.B. Mukamuri, University of Zimbabwe This research was conducted under the auspices of the CERES Research School for Resource Studies for Development. Can We Learn Our Way to Sustainable Management? Adaptive Collaborative Management in Mafungautsi State Forest, Zimbabwe. Tendayi Mutimukuru-Maravanyika Thesis submitted in fulfilment of the requirements for the degree of doctor at Wageningen University by the authority of the Rector Magnificus Prof. dr. M. J. Kropff in the presence of the Thesis Committee appointed by the Academic Board to be defended in public on Friday 23 April 2010 at 11 a.m. in the Aula. Tendayi Mutimukuru-Maravanyika Can We Learn Our Way to Sustainable Management? Adaptive Collaborative Management in Mafungautsi State Forest, Zimbabwe. 231 pages Thesis Wageningen University, Wageningen, NL (2010) ISBN 978-90-8585-651-1 Dedication To my parents, my husband Simeon , my son Tafadzwa -

Process Monitoring and Evaluation II of Zimbabwe's Results

LEARNING FROM IMPLEMENTATION Process Monitoring and Evaluation II of Zimbabwe’s Results-Based Financing Project : The Case of M u t o k o , C h i r e d z i , N k a y i a n d Kariba Districts Research Team Irene Moyo (Qualitative Research Consultant) and Crecentia Gandidzanwa (Qualitative Research Consultant) World Bank Harare – Zimbabwe; Tafadzwa Tsikira (MPH Graduate Intern) and Thubelihle Mabhena (MPH Graduate Intern) College of Health Sciences – University of Zimbabwe Dr. Marjolein Dieleman (Mixed Methods Research Senior Technical Advisor) and Dr. Sumit Kane (Health Systems Research Technical Advisor) KIT – The Netherlands; Technical Guidance Dr. Patron Mafaune (Provincial Medical Director and MOHCC Designated Technical Advisor to PME II) World Bank Task Team Ronald Mutasa (Senior Health Specialist/Task Team Leader) Chenjerai Sisimayi (Health Specialist/Field Study Coordinator) Jed Friedman (Senior Economist) Ashis Das (Health Specialist) Leah Jones (Knowledge Management Specialist/Consultant) Ha Thi Nguyen (Senior Health Economist) CONTENTS 1. Introduction and Background .............................................................................. 1 1.1 Introduction .............................................................................................................. 1 1.2 Background to Process Evaluation in RBF .............................................................. 1 1.2.1 PME Objectives ................................................................................................ 2 2. Methodology/Technical Approaches -

Mashonaland Central Province : 2013 Harmonised Elections:Presidential Election Results

MASHONALAND CENTRAL PROVINCE : 2013 HARMONISED ELECTIONS:PRESIDENTIAL ELECTION RESULTS Mugabe Robert Mukwazhe Ncube Dabengwa Gabriel (ZANU Munodei Kisinoti Welshman Tsvangirayi Total Votes Ballot Papers Total Valid Votes District Local Authority Constituency Ward No. Polling Station Facility Dumiso (ZAPU) PF) (ZDP) (MDC) Morgan (MDC-T) Rejected Unaccounted for Total Votes Cast Cast Bindura Bindura Municipality Bindura North 1 Bindura Primary Primary School 2 519 0 1 385 6 0 913 907 Bindura Bindura Municipality Bindura North 1 Bindura Hospital Tent 0 525 0 8 521 11 0 1065 1054 2 POLLING STATIONS WARD TOTAL 2 1,044 0 9 906 17 0 1,978 1,961 Bindura Bindura Municipality Bindura North 2 Bindura University New Site 0 183 2 1 86 2 0 274 272 Bindura Bindura Municipality Bindura North 2 Shashi Primary Primary School 0 84 0 2 60 2 0 148 146 Bindura Bindura Municipality Bindura North 2 Zimbabwe Open UniversityTent 2 286 1 4 166 5 0 464 459 3 POLLING STATIONS WARD TOTAL 2 553 3 7 312 9 0 886 877 Bindura Bindura Municipality Bindura North 3 Chipindura High Secondary School 2 80 0 0 81 1 2 164 163 Bindura Bindura Municipality Bindura North 3 DA’s Campus Tent 1 192 0 7 242 2 0 444 442 2 POLLING STATIONS WARD TOTAL 3 272 0 7 323 3 2 608 605 Bindura Bindura Municipality Bindura North 4 Salvation Army Primary School 1 447 0 7 387 12 0 854 842 1 POLLING STATIONS WARD TOTAL 1 447 0 7 387 12 0 854 842 Bindura Bindura Municipality Bindura North 5 Chipadze A Primary School ‘A’ 0 186 2 0 160 4 0 352 348 Bindura Bindura Municipality Bindura North 5 Chipadze B -

38678 10-4 Roadcarrierp Layout 1

Government Gazette Staatskoerant REPUBLIC OF SOUTH AFRICA REPUBLIEK VAN SUID-AFRIKA Vol. 598 Pretoria, 10 April 2015 No. 38678 N.B. The Government Printing Works will not be held responsible for the quality of “Hard Copies” or “Electronic Files” submitted for publication purposes AIDS HELPLINE: 0800-0123-22 Prevention is the cure 501272—A 38678—1 2 No. 38678 GOVERNMENT GAZETTE, 10 APRIL 2015 IMPORTANT NOTICE The Government Printing Works will not be held responsible for faxed documents not received due to errors on the fax machine or faxes received which are unclear or incomplete. Please be advised that an “OK” slip, received from a fax machine, will not be accepted as proof that documents were received by the GPW for printing. If documents are faxed to the GPW it will be the sender’s respon- sibility to phone and confirm that the documents were received in good order. Furthermore the Government Printing Works will also not be held responsible for cancellations and amendments which have not been done on original documents received from clients. CONTENTS INHOUD Page Gazette Bladsy Koerant No. No. No. No. No. No. Transport, Department of Vervoer, Departement van Cross Border Road Transport Agency: Oorgrenspadvervoeragentskap aansoek- Applications for permits:.......................... permitte: .................................................. Menlyn..................................................... 3 38678 Menlyn..................................................... 3 38678 Applications concerning Operating Aansoeke aangaande Bedryfslisensies:. -

For Human Dignity

ZIMBABWE HUMAN RIGHTS COMMISSION For Human Dignity REPORT ON: APRIL 2020 i DISTRIBUTED BY VERITAS e-mail: [email protected]; website: www.veritaszim.net Veritas makes every effort to ensure the provision of reliable information, but cannot take legal responsibility for information supplied. NATIONAL INQUIRY REPORT NATIONAL INQUIRY REPORT ZIMBABWE HUMAN RIGHTS COMMISSION ZIMBABWE HUMAN RIGHTS COMMISSION For Human Dignity For Human Dignity TABLE OF CONTENTS FOREWORD .................................................................................................................................................. vii ACRONYMS.................................................................................................................................................... ix GLOSSARY OF TERMS .................................................................................................................................. xi PART A: INTRODUCTION TO THE NATIONAL INQUIRY PROCESS ................................................................ 1 CHAPTER 1: INTRODUCTION ........................................................................................................................ 1 1.1 Establishment of the National Inquiry and its Terms of Reference ....................................................... 2 1.2 Methodology ..................................................................................................................................... 3 CHAPTER 2: THE NATIONAL INQUIRY PROCESS .........................................................................................