ITS Interconnection 22Oct12 Endnoted

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Vodacom Annual Results Presentation

Vodacom Group Annual Results For the year ended 31 March 2020 The future is exciting. Ready? Disclaimer The following presentation is being made only to, and is only directed at, persons to whom such presentations may lawfully be communicated (‘relevant persons’). Any person who is not a relevant person should not act or rely on this presentation or any of its contents. Information in the following presentation relating to the price at which relevant investments have been bought or sold in the past or the yield on such investments cannot be relied upon as a guide to the future performance of such investments. This presentation does not constitute an offering of securities or otherwise constitute an invitation or inducement to any person to underwrite, subscribe for or otherwise acquire securities in any company within the Group. Promotional material used in this presentation that is based on pricing or service offering may no longer be applicable. This presentation contains certain non-GAAP financial information which has not been reviewed or reported on by the Group’s auditors. The Group’s management believes these measures provide valuable additional information in understanding the performance of the Group or the Group’s businesses because they provide measures used by the Group to assess performance. However, this additional information presented is not uniformly defined by all companies, including those in the Group’s industry. Accordingly, it may not be comparable with similarly titled measures and disclosures by other companies. Additionally, although these measures are important in the management of the business, they should not be viewed in isolation or as replacements for or alternatives to, but rather as complementary to, the comparable GAAP measures. -

From Telkom to Hellkom1: a Critical Reflection on the Current Telecommunication Policy in South Africa from a Social Justice Perspective

ARTICLE IN PRESS + MODEL The International Information & Library Review (2008) xx,1e7 available at www.sciencedirect.com journal homepage: www.elsevier.com/locate/iilr To talk or not to talk? From Telkom to Hellkom1: A critical reflection on the current telecommunication policy in South Africa from a social justice perspective S.R. Ponelis a, J.J. Britz a,b,* a Department of Information Science, School of Information Technology, University of Pretoria, 0002 Pretoria, South Africa b School of Information Studies, University of Wisconsin-Milwaukee, 3210 N, Maryland Avenue, Milwaukee WI 53211, United States KEYWORDS Abstract With the development of new information and communication technologies, the Telecommunications; right to communicate assumes new dimensions, since it is almost impossible to fully participate Right to communicate; in the globalized world without access to modern information and communication technolo- South Africa; gies. South Africa held its first democratic elections in 1994 and has subsequently returned Telkom; to the international arena. Its citizens should rightly expect to be able to participate in all that Social justice this return offers, not only politically, but also economically and socially. Telecommunications are vital to making such participation possible. In recognition of this fact, the newly elected government developed policies and enacted legislation to ensure that the telecommunications sector, and specifically the sole fixed line service provider Telkom, provides South African citi- zens affordable access to the telecommunications infrastructure whilst providing acceptable levels of service. However, rather than meeting its obligation to the government and the people of South Africa, Telkom has misused its monopoly. The social injustice that this situa- tion creates is critically examined against the background of the right to communicate based on Rawls’ principles of social justice and Sen’s capability approach. -

An Overview of Today's and Tomorrow's M- Commerce In

AN OVERVIEW OF TODAY’S AND TOMORROW’S M- COMMERCE IN THE NETHERLANDS AND EUROPE Hong-Vu Dang BMI Paper AN OVERVIEW OF TODAY’S AND TOMORROW’S M- COMMERCE IN THE NETHERLANDS AND EUROPE Hong-Vu Dang BMI Paper Vrije Universiteit Amsterdam Faculty of Sciences Business Mathematics and Informatics De Boelelaan 1081a 1081 HV Amsterdam www.few.vu.nl August 2006 PREFACE A part of the masters programme of the study that I am following, Business Mathematics & Informatics (BMI) at the Vrije Universiteit Amsterdam, is writing a BMI paper. In this paper a problem in the field of BMI is assessed using existing literature. The subjects addressed in this paper are the past, present and future developments of the relatively new phenomenon called m-commerce. Developments discussed will be from a technological perspective as well as a business perspective. I would like to express my gratitude to Dr. S. Bhulai of the Vrije Universiteit Amsterdam for his guidance while I was writing this paper. Hong-Vu Dang BMI paper: An Overview Of Today’s And Tomorrow’s M-Commerce In The Netherlands And Europe ABSTRACT This paper explains: • What m-commerce is: in a nutshell, it is commerce using a mobile device such as a hand-held device or a smart phone; • What it is used for: currently, m-commerce in Europe mainly consists of messaging, such as SMS, and mobile entertainment (think of ringtones, wallpapers, and mobile games); • What technology is involved with m-commerce: this paper describes the history and future of mobile networks from 1G to 3G, and how other technologies can be used for m-commerce such as GPS, and Wi-Fi; • The business aspects of m-commerce: how much does it cost to enable m- commerce (for instance the costs of the European UMTS network) and how much turnover is made. -

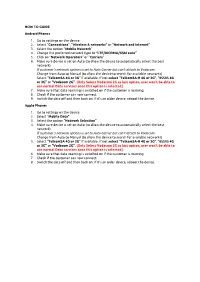

HOW to GUIDE Android Phones 1. Go to Settings on the Device. 2. Select “ Connections”, “Wireless & Networks” Or “N

HOW TO GUIDE Android Phones 1. Go to settings on the device. 2. Select “Connections”, “Wireless & networks” or “Network and Internet” 3. Select the option “Mobile Network” 4. Change the preferred network type to “LTE/WCDMA/GSM auto” 5. Click on “Network Operators” or “Carriers” 6. Make sure device is set on Auto (to allow the device to automatically select the best network) If customer’s network options is set to Auto Carrier but can’t attach to Vodacom: Change from Auto to Manual (to allow the device to search for available networks) Select “TelkomSA 4G or 3G” if available. If not select “TelkomSA-R 4G or 3G”, “65505 4G or 3G” or “Vodacom 2G”. (Only Select Vodacom 2G as last option, user won’t be able to use normal Data services once this option is selected.) 7. Make sure that data roaming is switched on if the customer is roaming. 8. Check if the customer can now connect. 9. Switch the data off and then back on. If it’s an older device, reboot the device. Apple Phones 1. Go to settings on the device. 2. Select “Mobile Data” 3. Select the option “Network Selection” 4. Make sure device is set on Auto (to allow the device to automatically select the best network) If customer’s network options is set to Auto Carrier but can’t attach to Vodacom: Change from Auto to Manual (to allow the device to search for available networks) 5. Select “TelkomSA 4G or 3G” if available. If not select “TelkomSA-R 4G or 3G”, “65505 4G or 3G” or “Vodacom 2G”. -

An Assessment of Claims Regarding Health Effects of 5G Mobile Telephony Networks

An Assessment of Claims regarding Health Effects of 5G Mobile Telephony Networks C R Burger, Z du Toit, A A Lysko, M T Masonta, F Mekuria, L Mfupe, N Ntlatlapa and E Suleman Contact: Dr Moshe Masonta [email protected] 2020-05-11 Contents Preamble .............................................................................................................................. 2 1. Overview of 5G Networks .............................................................................................. 3 1.1 What are 5G networks? ............................................................................................... 3 1.2 What are the health effects of mobile networks? .......................................................... 6 1.3 What can we expect from 5G networks?...................................................................... 7 2. Summary Technical Data on 5G .................................................................................... 9 2.1 Which frequencies will be used for 5G in South Africa? .......................................... 9 2.2 A Brief Comparison of 4G and 5G ......................................................................... 11 3. Summary notes ............................................................................................................ 12 Preamble This document was produced by a team of researchers from the Next Generation Enterprises and Institutions, and Next Generation Health clusters of the CSIR. It is a response to media claims of links between 5G mobile telephone networks -

6. Market Distortions and Infrastructure Sharing

102959 world development report Public Disclosure Authorized BACKGROUND PAPER Digital Dividends The Economics and Policy Public Disclosure Authorized Implications of Infrastructure Sharing and Mutualisation in Africa Jose Marino Garcia Public Disclosure Authorized World Bank Group Tim Kelly World Bank Group Public Disclosure Authorized The economics and policy implications of infrastructure sharing and mutualisation in Africa Jose Marino Garcia [email protected] and Tim Kelly [email protected] November 2015 Table of contents Executive summary ......................................................................................................................................... 1 1. Introduction ............................................................................................................................................... 2 2. Demand trends, new technologies and the impact on infrastructure sharing ........................ 4 3. Internet supply markets and the Internet Ecosystem .................................................................... 8 4. Analysis of infrastructure sharing models ..................................................................................... 11 5. The role of infrastructure sharing to reduce market and regulatory failures in the provision of broadband internet ........................................................................................................ 30 6. Market distortions and infrastructure sharing .............................................................................. -

Mediaplay Fibre Frequently Asked Questions

MEDIAPLAY FIBRE FREQUENTLY ASKED QUESTIONS 1. What is MediaPlay Fibre? MediaPlay Fibre is a converged tariff plan offering uncapped Fibre, C-Fibre Connector mobile that’s inclusive of mobile voice, mobile data, mobile Wi-Fi calling benefits and BINGE Premium entertainment package on black with access to local and international movies, series, music videos, Kid's shows, documentaries and much more. 2. Where can I sign up for MediaPlay Fibre? MediaPlay Fibre is available through the following channels: Cell C Fibre Field sales team which you can email at [email protected]; Cell C Fibre Telesales team which you can contact on 084 135 or email at [email protected]; Through our online channel, namely online sales channel, which can be accessed at https://www.cellc.co.za/cellc/c-fibre; Cell C Business Sales Channel which you can contact on 084 194 4000 or email [email protected]; Through select Cell C owned and franchise stores, which can be viewed at https://www.cellc.co.za/cellc/c-fibre. 3. What are the benefits of the new MediaPlay Fibre plans? MediaPlay Fibre tariff plans provide subscribers with the following inclusive benefits; Unlimited, unrestricted and unshaped Fibre; C-Fibre Connector mobile offering; o 1000 Any-net voice minutes per SIM per month o 2GB of mobile data per SIM per month o Unlimited free black streaming data included on C-Fibre Connector Mobile until 10 November 2018 o 500 Any-net Wi-Fi calling minutes per SIM per month BINGE Premium entertainment package on black: with access to over 60 TV channels, local and international movies, series, music videos, kid’s shows, documentaries and much more. -

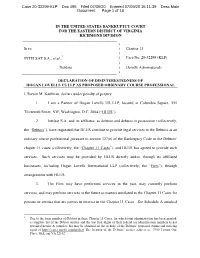

Chapter 11 ) INTELSAT

Case 20-32299-KLP Doc 495 Filed 07/09/20 Entered 07/09/20 15:11:39 Desc Main Document Page 1 of 16 IN THE UNITED STATES BANKRUPTCY COURT FOR THE EASTERN DISTRICT OF VIRGINIA RICHMOND DIVISION ) In re: ) Chapter 11 ) 1 INTELSAT S.A., et al., ) Case No. 20-32299 (KLP) ) Debtors. ) (Jointly Administered) ) DECLARATION OF DISINTERESTEDNESS OF HOGAN LOVELLS US LLP AS PROPOSED ORDINARY COURSE PROFESSIONAL I, Steven M. Kaufman, declare under penalty of perjury: 1. I am a Partner of Hogan Lovells US LLP, located at Columbia Square, 555 Thirteenth Street, NW, Washington, D.C. 2004 (“HLUS”). 2. Intelsat S.A. and its affiliates, as debtors and debtors in possession (collectively, the “Debtors”), have requested that HLUS continue to provide legal services to the Debtors as an ordinary course professional pursuant to section 327(e) of the Bankruptcy Code in the Debtors’ chapter 11 cases (collectively, the “Chapter 11 Cases”), and HLUS has agreed to provide such services. Such services may be provided by HLUS directly and/or through its affiliated businesses, including Hogan Lovells International LLP (collectively, the “Firm”), through arrangements with HLUS. 3. The Firm may have performed services in the past, may currently perform services, and may perform services in the future in matters unrelated to the Chapter 11 Cases for persons or entities that are parties in interest in the Chapter 11 Cases. See Schedule A attached 1 Due to the large number of Debtors in these Chapter 11 Cases, for which joint administration has been granted, a complete list of the Debtor entities and the last four digits of their federal tax identification numbers is not provided herein. -

17594 Vc Ir2021

Notice of annual general meeting Monday 19 July 2021 at 10:00 am Dear shareholder The following documents are enclosed: z Notice of AGM setting out the resolutions to be proposed at the meeting; and z A form of proxy. As a consequence of the ongoing impact of Covid-19 and with the health of our shareholders in mind, the board has determined that the AGM will be held I have the pleasure of by way of an electronic platform. This electronic platform will enable inviting you to attend shareholders to attend, speak and vote at the AGM. Details for accessing the the twenty-sixth annual electronic platform and the appropriate registration process will be published general meeting (AGM) on SENS prior to the AGM. of the company, which In continuing our commitment to minimising our environmental footprint, will be held virtually Vodacom supports the use of electronic communications which will deliver on Monday 19 July 2021 savings to the company in terms of administration, printing and postage costs, at 10:00. The AGM is a as well as speeding up the provision of information. We believe that our continued focus on strategic sustainable development will benefit all of our valuable opportunity stakeholders. for shareholders to communicate with With this in mind, and in an effort to lower our paper consumption while at the same time reducing solid waste and our carbon footprint, we will be printing a the Board to review limited number of the 2021 integrated report. Should you wish to receive a the performance of printed copy of the 2021 integrated report , kindly email your request to the company. -

From AT&T/Lucent 3G Third Generation (Mobile Network) 3GPP

1-ESS x-ESS series of "Electronic Switching Systems" from AT&T/Lucent 3G Third Generation (Mobile Network) 3GPP Third-Generation Partnership Project 3WC Three Way calling 4GL Fourth-Generation Language 800 or 888 Freephone 802.x Series of LAN standards developed by IEEE 911 Emergency telephone number in North America AAV Alternative Access Vendor ABR Available Bit Rate Access Control, or Alternating Current, or Authentication Center (also AC AUC) ACD Automatic Call Distributor ACE Authentication Encryption ACEK Authentication Encryption Key ACK Acknowledgement ACP Access Control Point ACRE Authorization and Call Routing Equipment ADM Add-Drop Multiplexer (SDH Element) ADPCM Adaptive Differential Pulse Code Modulation ADSL Asymmetric Digital Subscriber Line AGRAS Air-Ground Radiotelephone Automated Service AIOD Automatic Identification of Outward Dialed calls AIN Advanced Intelligent Network (ANSI IN Standard) A-key Authentication key ALI Automatic Location Information AM Amplitude Modulation AMPS Advanced Mobile Phone System ANI Automatic Number Identification ANS Advanced Network Services ANSI American National Standards Institute ANSI-41 ANSI standard for mobile management (ANSI/TIA/EIA-41) ANT ADSL Network Terminator AOA Angle of Arrival AOL America On Line (ISP) API Application Programming Interface APPC Advanced Program-to Program Communications (IBM SNA) APPN Advanced Peer-to-Peer Network (IBM SNA) ARCnet Attached Resource Computer Network (Datapoint) ARDIS Advanced Radio Data Information Service ARP Address Resolution Protocol ARPA -

2020 Annual Report Dear Stockholders

2020 ANNUAL REPORT DEAR STOCKHOLDERS, 2020 was a year like no other for Consolidated Communications. Searchlight’s investment enabled us to completely refinance our debt and We entered the year with strong momentum and a clear set of strategic extend our maturity profile by seven years. Importantly, this investment goals to guide our path and focus for the year: and partnership with an experienced strategic investor in our sector is • stabilize revenue and EBITDA while growing free cash flow enabling us to accelerate our fiber expansion plans immediately. • leverage our network across the regional territories we serve while • We are in a strong position to accelerate our fiber investments with continuing to invest in the expansion of our fiber network; and a fully funded build, supporting our growth initiatives across three customer groups; carrier, commercial and consumer. We have • continue to execute on our disciplined capital allocation plan, including a embarked on a five-year investment initiative to upgrade 1.6 million strategic refinancing, to position the Company for investment in the future. passings and enable multi-gigabit, symmetrical speeds over fiber services. And then the COVID-19 pandemic arrived, testing us in previously We have a proven track record of growing broadband, and we are now unimaginable ways. But your Company and its employees responded positioned to expedite our fiber expansion plans, boost customer speeds with incredible energy, engagement and support for one another. We and expand gigabit fiber services to 70 percent of our addressable market. focused immediately and intensely to ensure the safety of our employees As part of our fiber expansion plans, we intend to transform the customer and customers while at the same time ensuring business continuity and experience by making it easy for customers to do business with us. -

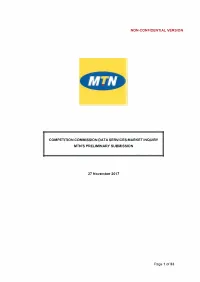

Mtn's Preliminary Submission

NON-CONFIDENTIAL VERSION COMPETITION COMMISSION DATA SERVICES MARKET INQUIRY MTN'S PRELIMINARY SUBMISSION 27 November 2017 Page 1 of 53 2 Table of Contents Page No 1. Introduction and executive summary.......... .......... ..................................................... 3 2. Data services value chain .. .......... ............................................................................. 6 3. Competition in mobile data services.......... ........ ......... ................. .......................... 21 4. MTN's new strategic initiative .................................................................................. 39 5. Regulatory context .................................................................................................. 42 6. Constraints on the further development of data services.................... .................... 46 7. Next steps............ ............................................................................ ............. .......... 53 Page 2 of 53 3 1. Introduction and executive summary Introduction 1.1 On 18 August 2017, the Competition Commission (the "Commission") initiated a market inquiry into Data Services in South Africa in terms of Chapter 4A of the Competition Act No. 89 of 1998 (as amended) (the "Competition Act"). On 20 September 2017, the Commission invited stakeholders to make formal submissions. Mobile Telephone Networks Proprietary Limited ("MTN") would like to thank the Commission for the opportunity to make this submission. 1.2 MTN is mindful of the context within which the