(2017) Currency Innovation for Sustainable Financing of Smes: Context, Case Study and Scalability

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

LOW-CARBON CURRENCIES: the POTENTIAL of TIME BANKING and LOCAL MONEY SYSTEMS for COMMUNITY CARBON-REDUCTION by Gill Seyfang C

LOW-CARBON CURRENCIES: THE POTENTIAL OF TIME BANKING AND LOCAL MONEY SYSTEMS FOR COMMUNITY CARBON-REDUCTION by Gill Seyfang CSERGE Working Paper EDM 09-04 1 LOW-CARBON CURRENCIES: THE POTENTIAL OF TIME BANKING AND LOCAL MONEY SYSTEMS FOR COMMUNITY CARBON-REDUCTION Gill Seyfang CSERGE, School of Environmental Sciences, University of East Anglia [email protected] ISSN 0967-8875 2 ABSTRACT The challenge of achieving low-carbon communities cannot be underestimated. While government policies set ambitious targets for carbon-reduction over the next 40 years, there remains an urgent need for tools and initiatives to deliver these reductions through behaviour-change among individuals, households and communities. This chapter sets out a ‘New Economics’ agenda for sustainable consumption which addresses the need for low- carbon communities. It then applies these criteria in a critical examination of complementary currencies in the UK (time banking and local money). These are alternative mechanisms for exchanging goods and services within a community, which do not use money, and which aim instead to build local economic resilience and social capital. The potential of these initiatives as carbon-reduction tools has not previously been considered. Time banking appears to offer the greatest potential for carbon-reduction through offering a supportive social network which meets some of the participants’ social and psychological needs for recognition, esteem and belongingness – needs which might otherwise be met through material consumption. In contrast, local money systems aim to strengthen and build resilience in local economies, and their principal impact on consumption is through localisation and import-substitution – which brings carbon-reductions from avoiding transport costs. -

A Tool for Building Community Resilience?

This article was downloaded by: [University of East Anglia Library] On: 15 February 2012, At: 09:32 Publisher: Routledge Informa Ltd Registered in England and Wales Registered Number: 1072954 Registered office: Mortimer House, 37-41 Mortimer Street, London W1T 3JH, UK Local Environment: The International Journal of Justice and Sustainability Publication details, including instructions for authors and subscription information: http://www.tandfonline.com/loi/cloe20 A tool for building community resilience? A case study of the Lewes Pound Jeppe Dyrendom Graugaard a a University of East Anglia, Norwich, UK Available online: 15 Feb 2012 To cite this article: Jeppe Dyrendom Graugaard (2012): A tool for building community resilience? A case study of the Lewes Pound, Local Environment: The International Journal of Justice and Sustainability, DOI:10.1080/13549839.2012.660908 To link to this article: http://dx.doi.org/10.1080/13549839.2012.660908 PLEASE SCROLL DOWN FOR ARTICLE Full terms and conditions of use: http://www.tandfonline.com/page/terms-and- conditions This article may be used for research, teaching, and private study purposes. Any substantial or systematic reproduction, redistribution, reselling, loan, sub-licensing, systematic supply, or distribution in any form to anyone is expressly forbidden. The publisher does not give any warranty express or implied or make any representation that the contents will be complete or accurate or up to date. The accuracy of any instructions, formulae, and drug doses should be independently verified with primary sources. The publisher shall not be liable for any loss, actions, claims, proceedings, demand, or costs or damages whatsoever or howsoever caused arising directly or indirectly in connection with or arising out of the use of this material. -

Money That Matters

Qoin – money that matters Money makes our world go around. Money is not given, but man-made. We can re-invent and re-design it to fit our purpose. Qoin introduces, implements, and manages professional Community Currencies throughout Europe. We assist authorities, SMEs and citizens to use Community Currencies to reach sustainable economic growth, ecological balance, and social progress. We do our work with a passionate team. Money = man-made Current legal tender currency systems are very strong in developing high profits and building a globalised society. However, they have proved less effective in supporting regional economic development, stimulating ecological policy goals and behaviours, and encouraging an active civil society. The current economic and financial crisis faced by many regions in Europe calls for new arrangements for communities to remain or become resilient. Community Currencies are social instruments Community Currencies (‘complementary currencies’, ‘alternative currencies’ or ‘social currencies’), are monetary instruments that develop and implement specific social, environmental and commercial objectives. Throughout history, both in concept and in practise, a large variety of Community Currencies can be found. It is difficult to distinguish the many programs from one another, making it hard to understand the best use, setup and impact. Many currencies are used properly, but quit often this is not the case. In our ‘Body of Knowledge on Complementary Currencies’, we describe the set of most frequently used currencies and their impact. A key characteristic is that they all understand money as a socially and politically construction. Community Currencies offer a proven ‘toolbox’ for stimulating the creation of jobs at local level, re-localising production and consumption, supporting a vibrant SME (small and medium sized enterprise sector), building a strong and active civil society, stimulating innovation and the development of local solutions to global problems, e.g. -

Bank of England, Local Currency Scheme Websites, ONS and Bank Calculations

Topical articles Banknotes, local currencies and central bank objectives 317 Banknotes, local currencies and central bank objectives By Mona Naqvi and James Southgate of the Bank’s Notes Division.(1) • A few towns and cities in the United Kingdom have set up local currency schemes to promote local sustainability. The schemes issue paper instruments with some similar design features to banknotes. This article explains how these instruments differ from banknotes. • The size, structure and backing arrangements of existing schemes mean that local currencies are unlikely to pose a risk to the Bank’s monetary and financial stability objectives. Nonetheless, consumers should be aware that local currency instruments do not benefit from the same level of consumer protection as banknotes. Overview The Bank of England’s issuance of banknotes feeds into its Summary table Features of local currency schemes that monetary stability objective, which includes maintaining mitigate potential risks to the Bank’s objectives confidence in the physical currency. This requires people to Objective of the Bank Potential risk to that Feature(s) of local currencies that be confident that the banknotes they hold will continue to objective can reduce that risk be widely accepted at face value. The promise by the Bank of Price stability Local currency schemes The schemes are small relative to lead to significant and aggregate spending in the England to make good the value of its banknotes for all time, unanticipated impacts on economy. aggregate economic as well as its use of robust security features and a activity. wide-ranging programme of education on how to identify Confidence in the Fears surrounding the Design features and marketing genuine banknotes, helps to ensure that this objective is met. -

Black Currency of Middle Ages and Case for Complementary Currency

Journal of Risk and Financial Management Article Black Currency of Middle Ages and Case for Complementary Currency Pezhwak Kokabian Department of Economics, Claremont Graduate University, Claremont, CA 91711, USA; [email protected] Received: 16 March 2020; Accepted: 2 June 2020; Published: 3 June 2020 Abstract: Monetary historians argue that two types of currencies were circulating in the middle ages of Europe. The first was the standard historical form of money made up of gold and silver coins, and the second was a set of small pieces of copper and other metallic substances used mainly in towns and townships for local trade as currency. Jetton and tokens are monetized objects that are not official currencies; they were of lower quality of the inferior metallic object, which were used for day-to-day transaction needs. The drive for local monetary decentralization is pointed to build up fiscal autonomy and responsible local monetary institutions. This paper reasons that the monetary regime of the Renaissance was a real and genuine trimetallic currency regime. Keywords: the second currency; complementary currency; middle ages currency; counter-cyclicality; barter 1. Introduction There are several narratives of the historical origins of currency. The majority of economists make a factual error when they equate the origin of money with the history and origins of coinage (Innes 1913), whether we acknowledge that economic history has been eliminated from the curriculums of the majority of western economic departments programs. While the history of currency and coinage may overlap in some periods in the history of humankind, even then, it is a historical fact that money predates coin minting by more than 3000 years. -

IJCCR 2011 Special Issue 12 Ryan Collins

Building Local Resilience: The Emergence of the UK Transition Currencies Josh Ryan-Collins new economics foundation IJCCR [email protected] Abstract This paper examines the emergence of a new type of local currency – ‘Transition Currencies’ - in the United Kingdom over the past 4 years. The Transition Currency ‘model’, shared by the initial four schemes, is explained and the theoretical roots of the schemes reviewed. The paper goes on to examine the success and limitations of the currencies and reMlects on potential future developments and how the Transition currencies might upscale and deliver additional social, economic and environmental objectives. Introduction reimagining how settlements and local economies might be able to adapt the shocks One of the most interesting developments in these two phenomenon will inevitably create the UK complementary currency movement without creating major social and economic over the past 4 years has been the emergence dislocation. The notion of resilience is key to of local paper currency schemes in ‘Transition Transition thinking, deMined as: towns’. Following Totnes in 2007, the towns of Lewes, Stroud and Brixton in South London ...the capacity of a system to absorb disturbance have all successfully launched local ‘pounds’, and reorganise while undergoing change, so as the usage of which is restricted to independent to still retain essentially the same function, businesses in their respective areas. Broadly structure, identity and feedbacks (Walker et al, speaking, the goal of the currencies is to help 2004) re-localise production and consumption and To create greater resilience, Transition argues build economic ‘resilience’, a key tenet of the for the re-localisation of many aspects of Transition movement. -

Local Community Currency Obtains Its Value Entirely From

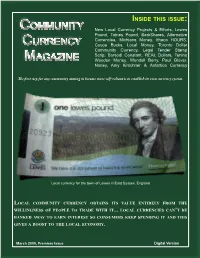

INS I DE TH I S I SSUE : COMMUNITY New Local Currency Projects & Efforts, Lewes Pound, Totnes Pound, BerkShares, Alternative Currencies, Michiana Money, Ithaca HOURS, CURREN C Y Cocoa Bucks, Local Money, Toronto Dollar Community Currency, Legal Tender Stamp Scrip, Borsodi Constant, REAL Dollars, Tenino MAGAZINE Wooden Money, Wendell Berry, Paul Glover, Noney, Amy Kirschner & Antartica Currency The first step for any community aiming to become more self-reliant is to establish its own currency system. Local currency for the town of Lewes in East Sussex, England LOCA L COMMUNITY CURRENCY OBTAINS ITS VA L UE ENTIRE L Y FROM THE WI ll INGNESS OF PEOP L E TO TRADE WITH IT ... L OCA L CURRENCIES CAN ’T BE BANKED AWAY TO EARN INTEREST SO CONSUMERS KEEP SPENDING IT AND THIS GIVES A BOOST TO THE L OCA L ECONOMY . March 2009, Premiere Issue Digital Version http://www.flickr.com/photos/writemboyo/2960993841/ New Local Currency Projects & Efforts REAL Dollars - Local Currency for Page 4 Lawrence, Kansas (2000-2003) Lewes Pound Page 26 Page 6 The Complete Story of Tenino Wooden Totnes Pound Project Money Page 8 By Don Major Thurston County Independent, 2/19/65 BerkShares Success Enables Page 27 Exchange Rate Change Announcement from Berkshares The Idea of a Local Economy Page 9 by Wendell Berry Page 28 Fundamentals of Alternative Currencies and Value Measurement Noney by Thomas Greco Rhymes with money Page 10 Page 30 Michiana Money Is The New Sense Beyond The Dollar - A Primer Community Currency On Local Currencies Page 12 by Amy Kirschner Page 31 Ithaca HOURS use steady By David Durrett The Coldest Currency on The Planet? Page 13 BankOfAntartica.com Page 34 The Destiny of Dollars Cover by Paul Glover The Lewes one pound note features Page 14 Thomas Paine who lived in Lewes from 1768 - 1774. -

Synthese Faire Mouvement Lyon 2011

Faire mouvement Rencontre internationale des Acteurs des Monnaies Sociales et Complémentaires 18 février 2011 - Lyon – France Synthèse des débats Février 2012 monnaiesendebat.org Présentation La journée « Faire mouvement » - Rencontre internationale des Acteurs des Monnaies Sociales et Complémentaires était partie intégrante de la Semaine des Monnaies Sociales et Complémentaires (MSC) organisée à Lyon – France, du 15 au 18 février 2011. Elle s'est inscrite dans la continuité du colloque académique international « Trente années de monnaies sociales et complémentaires – et après ? » des 16 et 17 février organisé par le Laboratoire Triangle (Université Lyon 2) et dont vous retrouvez, en fin d’annexes, un compte-rendu bref mais particulièrement éclairant sur les dynamiques à l’œuvre dans le champ universitaire international et propres aux MSC. Plus de 250 personnes en provenance des 5 continents ont participé à ces temps d'échange, de débats, de présentations de dispositifs de MSC de par le monde, faisant de ces journées la première rencontre internationale d’importance sur ce thème, à un moment-clef de l’écho médiatique et citoyen sans précédent rencontré, à l’échelle internationale, par la mise à nu précise, documentée et largement commentée des réalités recouvrant les mécanismes économiques et financiers présidant à la marche du monde tel que nous le connaissons aujourd’hui. Rassembler les acteurs des MSC pour dialoguer, affirmer, peser, construire et inspirer, constituait le pari que les organisateurs avaient souhaité relever : pari tenu au vu de la mobilisation des participants ayant rejoint l’aventure et des vœux unanimes de continuité formulés à l’issue de la rencontre. Vous retrouverez ici une synthèse des présentations et débats riches de la journée du 18 février 2011 qui a donné la parole à une diversité inédite de systèmes en place et d’expérimentations en cours de MSC. -

Developing a Value Proposition: The

INCLUSIVE ECONOMY INSTITUTE DEVELOPING A VALUE PROPOSITION: THE BRISTOL POUND INCLUSIVE ECONOMY INSTITUTE Table of Contents EXECUTIVE SUMMARY ............................................................................................................................... 3 INTRODUCTION ......................................................................................................................................... 4 MOST IMPORTANT CHARACTERISTICS OF B2B PARTNERS ............................................................................ 8 SAMPLE ..................................................................................................................................................... 9 CURRENT £B MEMBERS ............................................................................................................................ 10 £B MEMBERSHIP: INTERPRETING THE DATA .............................................................................................. 11 MEMBERSHIP OF OTHER NETWORKS ........................................................................................................ 15 VALUING SERVICES AND FEATURES OF NETWORKS ................................................................................... 18 INTERPRETING THE DATA ......................................................................................................................... 18 PAYING FOR SERVICES .............................................................................................................................. 26 SUMMARY -

Alternative Currencies

POSTNOTE Number 475 August 2014 Alternative Currencies Overview Alternative currencies include global currencies like Bitcoin and local community currencies such as the Bristol Pound. They are meant to complement, not replace, national currency. Local community alternative currencies are designed to regenerate local areas, address social exclusion and value unpaid work and Alternative currencies are types of money or activities. exchange that can be used instead of and Global alternative currencies are designed to alongside national currency. A number of bypass intermediaries like banks. alternative currencies are used in the UK Alternative currencies are largely today. This POSTnote outlines the different unregulated in the UK. types and aims of these currencies. It also Consumers may not be protected against sets out how alternative currencies are being loss of global alternative currency. used and highlights regulatory and policy The use of some local community currencies challenges regarding consumer protection, may affect eligibility for benefits. financial crime and taxation and benefits. Background Local community currencies There is no commonly accepted view on what counts as There are three main types of local community currency in money or currency,1 but currencies typically fulfil three use in the UK, each with distinct aims. These are Transition functions: providing a unit for measuring the value of an Town Pounds, Time Banks and Local Exchange Trading item; acting as a store of value for future use; and being Systems (LETS). used as a ‘medium of exchange,’ which allows goods and services to be purchased using commonly accepted units Transition Town Pounds and tokens (e.g. a five pound note). -

The Future of Community Currencies: Physical Cash Or Solely Electronic?

Pre-Conference DRAFT 2014-08-06 The future of Community Currencies: physical cash or solely electronic? Jonathan Warner Professor of Economics, Quest University Canada 3200 University Boulevard, Squamish, BC V8B 0N8 Canada [email protected] Keywords: Cash; Community currencies; payment mechanisms Abstract Accompanying the decline in the use of cash over the past 20 years has been a revival of interest in, and development of, near-moneys - alternative, complementary and community currencies. Much of the growth has been in non-physical (i.e. non-cash or –voucher based) forms, but there are market segments where physicality is essential, making them resilient to any trend away from cash. Alternative currencies, that seek to compete with (and perhaps ultimately even replace) national currencies, are likely to become digitized. Bitcoin, despite its shaky start, seems to be gaining traction; and there is no suggestion that it needs to be anything other than digital. Complementary currencies, that seek to fill gaps that are badly served by conventional currencies, such as Business to Business currencies, and business currencies such as Air miles, are only rarely physical, and, where they are, are more likely to be business-specific gift certificates, rather than a circulating medium of exchange. On the other hand, certain forms of community currencies – local currencies designed to promote transactions within a particular area are more likely to be physical, in other words, cash. Although time-based systems, such as Community Exchange Systems, have adopted a completely non-tangible approach, currency-based community currencies (where the unit of account is set equal to the national currency) have almost invariably adopted a physical medium. -

Project Information Pack

Innovating Complementary Currencies UEA London, Monday 20th September 2010 Project Information Pack Reference Project Delegate Project type Location A Bristol Pound Mark Burton In development UK B CC Lite Hugh Barnard LETS software UK C Community Forge Matthew Slater LETS software Geneva / Europe D Complementary Currencies backed by knowledge Pep de la Rosa Project concept ? E Complementary Currencies in German speaking countries (Regiogeld) Ludwig Schuster Active projects / in development / German speaking concepts countries F Hanbat LETS Miguel Yasuyuki Hirota Active project South Korea G INESPO Hélène Joachain Research project Belgium / EU H Kékfrank Zsuszanna Szalay Active project Hungary I Linking a complementary currency to Eco-system services / Lewes Pound Colin Tingle Project concept / active project UK J Liquidity Network Graham Barnes In development Republic of Ireland K Palmas Bank Carlos de Freitas Active project Brazil / Ecuador / France L Peer-to-Peer Finance Chris Cook In development ? M Spice Becky Booth Active project UK N Talente-Tauschkreis Vorarlberg Rolf Schilling Active project Austria O Transition currencies 2.0 Josh Ryan Collins Active project UK P Value for People John Rogers Currency support and Europe development The Bristol and Bath Local Currency Scheme This new currency initiative is being developed following the launch of Transition currencies in Totnes, Brixton, Lewes and Stroud and it has emerged as a project out of Transition Bristol. It therefore shares the same aims and objectives as the existing Transition