Hawai'i Community Foundation

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Honolulu County Community Health Needs Assessment and Implementation Plan Report

Honolulu County Community Health Needs Assessment and Implementation Plan Report February 28, 2013 Updated March 2017 Table of Contents Executive Summary .............................................................................................................................. 5 Introduction .................................................................................................................................................. 5 Approach ....................................................................................................................................................... 5 Data Sources and Methods ........................................................................................................................... 5 Areas of Need ................................................................................................................................................ 6 Selected Priority Areas .................................................................................................................................. 7 Note to the Reader ....................................................................................................................................... 9 1 Introduction .................................................................................................................................. 10 1.1 Summary of CHNA Report Objectives and context ........................................................................ 10 1.1.1 Healthcare Association of Hawaii .......................................................................................... -

ANNUAL REPORT 2010—2011 Health Programs Financial Information Leader in Disease Independent Auditors’ Report

Celebrating 30 years of waging peace, fighting disease, and building hope 30 ANNUAL REPORT 2010—2011 HEALTH PROGRAMS FINANCIAL INFORMATION Leader in Disease Independent Auditors’ Report . 64 Eradication and Elimination . 20 Financial Statements . 65 Partner for Village-Based Notes to Statements . 70 Health Care Delivery . 22 OUR COMMUNITY The Carter Center at a Glance . 2. Voice for Mental Health Care . 24 The Carter Center Around Aontents Message from President Health Year in Review . 26 the World . 84 CJimmy Carter . 3 PHILANTHROPY Senior Staff . 86 Interns . 86 Our Mission . 4 A Message About Our Donors . 32 A Letter from the Officers . 5 International Task Force for Donors with Cumulative Lifetime Disease Eradication . 87 Giving of $1 Million or More . 33 PEACE PROGRAMS Friends of the Inter-American Pioneer of Election Observation . 8 Donors During 2010–2011 . 34 Democratic Charter . 87 Trusted Broker for Peace . 10 Ambassadors Circle . 48 Mental Health Boards . 88 Champion for Human Rights . 12 Legacy Circle . 58 Board of Councilors . 89 Peace Year in Review . 14 Founders . 61 Board of Trustees . 92 A woman works at a small-scale subsistence mine in the province of Katanga, southeastern Democratic Republic of the Congo . The Carter Center’s work in the country is raising awareness about the nation’s lucrative mining industry, which generates huge profits while impoverished local communities receive few of the benefits . 1 The Carter Center at a Glance Overview • Strengthening international standards for human rights The Carter Center was founded in 1982 by former U.S. and the voices of individuals defending those rights in President Jimmy Carter and his wife, Rosalynn, in their communities worldwide partnership with Emory University, to advance peace and • Pioneering new public health approaches to preventing health worldwide. -

State of Hawaii Community Health Needs Assessment

State of Hawaii Community Health Needs Assessment February 28, 2013 Table of Contents Executive Summary .............................................................................................................................. 4 Introduction .................................................................................................................................................. 4 Approach ....................................................................................................................................................... 4 Data Sources and Methods ........................................................................................................................... 4 Areas of Need ................................................................................................................................................ 5 Selected Priority Areas ................................................................................................................................. 6 Note to the Reader ....................................................................................................................................... 6 1 Introduction ..................................................................................................................................... 1 1.1 Summary of CHNA Report Objectives and context ............................................................................. 1 1.1.1 Healthcare Association of Hawaii ................................................................................................ -

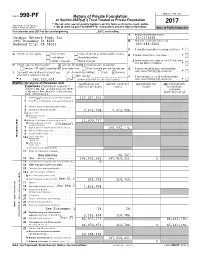

ONFI-2017-990-PF.Pdf

OMB No. 1545-0052 Form 990-PF Return of Private Foundation or Section 4947(a)(1) Trust Treated as Private Foundation 2017 G Do not enter social security numbers on this form as it may be made public. Department of the Treasury Internal Revenue Service G Go to www.irs.gov/Form990PF for instructions and the latest information Open to Public Inspection For calendar year 2017 or tax year beginning , 2017, and ending , A Employer identification number Omidyar Network Fund, Inc 20-1173866 1991 Broadway St #200 B Telephone number (see instructions) Redwood City, CA 94063 650-482-2500 C If exemption application is pending, check here. G G Check all that apply: Initial return Initial return of a former public charity D1Foreign organizations, check here. G Final return Amended return Address change Name change 2 Foreign organizations meeting the 85% test, check here and attach computation . G H Check type of organization:X Section 501(c)(3) exempt private foundation Section 4947(a)(1) nonexempt charitable trust Other taxable private foundation E If private foundation status was terminated under section 507(b)(1)(A), check here. G IJFair market value of all assets at end of year Accounting method: CashX Accrual (from Part II, column (c), line 16) Other (specify) F If the foundation is in a 60-month termination G $ 545,202,008. (Part I, column (d) must be on cash basis.) under section 507(b)(1)(B), check here. G Part I Analysis of Revenue and (a) Revenue and (b) Net investment (c) Adjusted net (d) Disbursements Expenses (The total of amounts in expenses per books income income for charitable columns (b), (c), and (d) may not neces- purposes sarily equal the amounts in column (a) (cash basis only) (see instructions).) 1 Contributions, gifts, grants, etc., received (attach schedule). -

Are the Auction Houses Doing All They Should Or Could to Stop Online Fraud?

Federal Communications Law Journal Volume 52 Issue 2 Article 8 3-2000 Online Auction Fraud: Are the Auction Houses Doing All They Should or Could to Stop Online Fraud? James M. Snyder Indiana University School of Law Follow this and additional works at: https://www.repository.law.indiana.edu/fclj Part of the Antitrust and Trade Regulation Commons, Communications Law Commons, Consumer Protection Law Commons, Internet Law Commons, and the Legislation Commons Recommended Citation Snyder, James M. (2000) "Online Auction Fraud: Are the Auction Houses Doing All They Should or Could to Stop Online Fraud?," Federal Communications Law Journal: Vol. 52 : Iss. 2 , Article 8. Available at: https://www.repository.law.indiana.edu/fclj/vol52/iss2/8 This Note is brought to you for free and open access by the Law School Journals at Digital Repository @ Maurer Law. It has been accepted for inclusion in Federal Communications Law Journal by an authorized editor of Digital Repository @ Maurer Law. For more information, please contact [email protected]. NOTE Online Auction Fraud: Are the Auction Houses Doing All They Should or Could to Stop Online Fraud? James M. Snyder* I. INTRODUCTION ............................................................................. 454 II. COMPLAINTS OF ONLINE AUCTION FRAUD INCREASE AS THE PERPETRATORS BECOME MORE CREATV ................................. 455 A. Statistical Evidence of the Increase in Online Auction Fraud.................................................................................... 455 B. Online Auction Fraud:How Does It Happen? ..................... 457 1. Fraud During the Bidding Process .................................. 457 2. Fraud After the Close of the Auction .............................. 458 IlL VARIOUS PARTES ARE ATrEMPTNG TO STOP ONLINE AUCTION FRAUD .......................................................................... 459 A. The Online Auction Houses' Efforts to Self-regulate........... -

Threat from the Right Intensifies

THREAT FROM THE RIGHT INTENSIFIES May 2018 Contents Introduction ..................................................................................................................1 Meeting the Privatization Players ..............................................................................3 Education Privatization Players .....................................................................................................7 Massachusetts Parents United ...................................................................................................11 Creeping Privatization through Takeover Zone Models .............................................................14 Funding the Privatization Movement ..........................................................................................17 Charter Backers Broaden Support to Embrace Personalized Learning ....................................21 National Donors as Longtime Players in Massachusetts ...........................................................25 The Pioneer Institute ....................................................................................................................29 Profits or Professionals? Tech Products Threaten the Future of Teaching ....... 35 Personalized Profits: The Market Potential of Educational Technology Tools ..........................39 State-Funded Personalized Push in Massachusetts: MAPLE and LearnLaunch ....................40 Who’s Behind the MAPLE/LearnLaunch Collaboration? ...........................................................42 Gates -

VOL.14 Issue 1 January 15, 2014

VOL.14 ISSUE 1 January 15, 2014 IN THIS ISSUE ANNUAL LEGISLAtiVE BUDGET INFORMAtiONAL BRIEFINGS ► Message From Kalani pg 1 Each year, the Senate Committee on Ways and Means and the House Finance Com- ► WAM Info Briefing pg 1 mittee conduct a series of joint informational briefings over a couple of weeks, on the State’s fiscal projections and the budget requests for the various State departments. ► 2013 CIP Update pg 2 This session, the committees held the revenue forecast briefing with the Council of ► Food Summit & Caucus pg 3 Revenues earlier than usual, December instead of January, to expedite the compilation ► Realtors Capitol Visit pg 3 the Hawai‘i State budget. ► Plane Crash Investigation pg 4 On December 18, 2013, committee members were briefed on the administration’s fiscal year (FY) 2015 Executive Supplemental Budget and Multi-Year General Fund Financial Plan by Kalbert Young, Director of the Budget and Finance Department. His testimony MESSAGE FROM KALANI stated that the State’s financial footing has substantially improved during the last three fiscal years and generated a healthy and unprecedented preliminary general fund end- ing balance of $844 million for FY 2013. There were five strategic financial plan goals The start of the 27th Legislative Session when shaping their budget decisions: build the State’s financial structure and fiscal brings great expectations for the people health; rebuild reserves; build and manage positive ending balances; fund programs for of Hawai’i. An ever higher standard of sustainability; and address long term liabilities. co-operation and unity is unique to the Aloha State. -

E Traordinary Together

ER T A O R D INA R Y T O G E THER 2013 REPOrt TO THE COMMUNITY Philanthropyx Every day, we work with people who want to make a difference 2 0 E(x)ponential Results: Beyond Simple Math in the community. Some seek to help individuals; some aspire to achieve community-wide goals; still others want to affect global 03 Leading and Following by E(x)ample change. Our job is to multiply the effect of their good intentions. 05 E(x)periencing the Gift that Comes from Giving In math, an exponential equation graph looks like a hockey stick. 07 E x panding Ownership ( ) In philanthropy, it means that the results can extend far beyond the 09 Leadership E(x)emplified gift itself. Think of starting with the formula 1 + 1 = 2, and watching 11 E(x)ceptional Youth two become four, and four become eight; that’s what happens when philanthropy works best. When those who give can see the difference their giving is making in someone else’s life, they can feel the change in their own. Hawai‘i Community Foundationx 13 Vision & Mission Statements In this year’s report, we are pleased to share with you some recent stories about the magnifying power of philanthropy that can happen in real life. When a gift supports a scholarship student who is first in his family to go to college, 14 Belief Statement it moves beyond that person to change the trajectory for his younger siblings. When a family involves the youngest 15 Your Personal Resource for Giving of its members in choosing where donations will go, a future generation learns the value of philanthropy. -

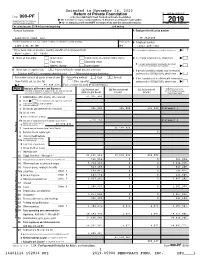

2019 Form 990-PF

Extended to November 16, 2020 Return of Private Foundation OMB No. 1545-0047 Form 990-PF or Section 4947(a)(1) Trust Treated as Private Foundation | Do not enter social security numbers on this form as it may be made public. Department of the Treasury 2019 Internal Revenue Service | Go to www.irs.gov/Form990PF for instructions and the latest information. Open to Public Inspection For calendar year 2019 or tax year beginning , and ending Name of foundation A Employer identification number Democracy Fund, Inc. 38-3926408 Number and street (or P.O. box number if mail is not delivered to street address) Room/suite B Telephone number 1200 17th St NW 300 (202) 420-7943 City or town, state or province, country, and ZIP or foreign postal code C If exemption application is pending, check here ~ | Washington, DC 20036 G Check all that apply: Initial return Initial return of a former public charity D 1. Foreign organizations, check here ~~ | Final return Amended return 2. Foreign organizations meeting the 85% test, Address change Name change check here and attach computation ~~~~ | X H Check type of organization: Section 501(c)(3) exempt private foundation E If private foundation status was terminated Section 4947(a)(1) nonexempt charitable trust Other taxable private foundation under section 507(b)(1)(A), check here ~ | X I Fair market value of all assets at end of year J Accounting method: Cash Accrual F If the foundation is in a 60-month termination (from Part II, col. (c), line 16) Other (specify) under section 507(b)(1)(B), check here ~ | | $ 87,348,415. -

A Conversation with Hawai'i's Own Pierre Omidyar Taking the Hawai'i International Confere

Volume 33, Number 1 Spring 2010 INSIDE: Be True to Your School | A Conversation with Hawai‘i’s Own Pierre Omidyar Taking the Hawai‘i International Conference on System Sciences to New Heights DEAn’s MessAGE “We are proud to announce that our undergraduate program has, for the first time, been named as one of the nation’s top business programs by Bloomberg BusinessWeek.” Aloha, Conference on System Sciences into nation’s best by Bloomberg BusinessWeek. The Shidler College of Business one of the world’s leading gatherings on This is truly a credit to our entire faculty is a special place where people of all information systems applications. and staff who have worked tirelessly to cultures and backgrounds come together For those of you who are aspiring strengthen our programs, student services, to share ideas, dreams and business entrepreneurs, be sure to check out the internships and career placement. aspirations. Our global community of excerpts from our exclusive interview It has been a remarkable six months alumni, students, faculty and business with eBay founder Pierre Omidyar. As the and we thank you for sharing an interest professionals lies at the heart of our featured speaker for the Kı¯papa i ke Ala in all that we have accomplished. As success and is what makes this such a Lecture, he inspired us all to dream big. always, we hope that you enjoy this issue unique place to learn, grow and develop. Shidler pride continues to reign of Shidler Business. We welcome your The stories and articles in this issue of strong among our alumni. -

Canopy, Spring 2019 (PDF)

SPRING 2019 ALUMS MAKING A STRONGER, MORE SUSTAINABLE NEW HAVEN Page 16 A Growing Nation A group of F&ES students travels to Rwanda each year with faculty members Bill Weber and Amy Vedder to learn about wildlife conservation, ecotourism, and local culture. Students visit several national parks, including Nyungwe National Park in Rwanda, where sustainable land management practices like terrace farming (seen here) have become more commonplace. andy lee andy IN THIS ISSUE CANOPY Toolkit for an 'Apocalypse' 4 executive editor Keeping It in the Family 6 Matthew Garrett Director of Communications and Web Operations News & Notes 8 editors Kevin Dennehy Research Updates 13 Associate Director of Communications Josh Anusewicz Keeping It Local 16 Assistant Editor art director Out & About 24 Angela Chen-Wolf Design Manager A Post-Coal Future for Appalachia 26 designer Jamie Ficker Making the Invisible Visible 28 editorial advisory board Danielle Dailey, Kristin Floyd, Brad Gentry, Hannah Peragine It Takes a Network 30 Melanie Quigley, Os Schmitz, Karen Seto, and Julie Zimmerman dean In Defense of the Predator 32 Indy Burke Carl W. Knobloch, Jr. Dean Commencement 2019 37 contributors Katie Bleau Parting Thoughts From an F&ES Favorite 42 cover photo Matthew Garrett Class Notes 44 Canopy is published twice a year (spring and fall) by the In Memoriam 59 Yale School of Forestry & Environmental Studies (F&ES). Editorial offices are located at Bookshelf 60 Sage Hall 205 Prospect Street New Haven, CT 06511 Endnote 61 [email protected] 203-436-4805 Every time you get a new email address, relocate, or change positions, please send us an update at [email protected]. -

SHOULD YOU GIVE THROUGH an LLC? JOHN: Good Morning Everyone

Friday, October 25, 2019, Aviara (T21_1) SHOULD YOU GIVE THROUGH AN LLC? JOHN: Good morning everyone. My name is John Tyler. I’m the general counsel secretary, chief ethics officer for the Ewing Kauffman Foundation and it’s my privilege to be able to moderate and facilitate this session on really philanthropy and use of the LLC model. The Jan Zuckerberg initiative made a big splash a couple of years ago when Mark and Priscilla announced that they were going to set up their philanthropy through an LLC. And there was all sorts of, mostly uproar and a little bit of excitement and quite a bit of misunderstanding in the uproar. But Jan Zuckerberg was not by any means, the first philanthropy to be approached with this structure. But it did ignite interest in the structure and that has continued to this day. And I think that there is some good strong curiosity among high net worth individuals about, is this a good structure for me to operate my philanthropy through. And it’s more of an enterprise structure rather than a foundation single structure. It’s looking more the LLC structure through philanthropy is usually encompasses a variety of things. And so we’ve got high net worth individuals wondering is it a good structure for them. We’ve got foundations and community foundations and DAFs and other funders curious about, well wait a second, can we collaborate, can we do work with these for profit philanthropies and so there are questions about that. And there are just questions then that the sector has more broadly: Is the LLC structure going to hurt the credibility, if you will, of the philanthropic sector because it can get away with all of these things? And we’re going to solve all of those questions here this morning.