Analysis of the Effect of Health Insurance on Health Care Utilization in Rwanda

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Nowhere to Go : Informal Settlement Eradication in Kigali, Rwanda

University of Louisville ThinkIR: The University of Louisville's Institutional Repository College of Arts & Sciences Senior Honors Theses College of Arts & Sciences 5-2017 Nowhere to go : informal settlement eradication in Kigali, Rwanda. Emily E Benken University of Louisville Follow this and additional works at: https://ir.library.louisville.edu/honors Part of the Social and Cultural Anthropology Commons Recommended Citation Benken, Emily E, "Nowhere to go : informal settlement eradication in Kigali, Rwanda." (2017). College of Arts & Sciences Senior Honors Theses. Paper 127. http://doi.org/10.18297/honors/127 This Senior Honors Thesis is brought to you for free and open access by the College of Arts & Sciences at ThinkIR: The University of Louisville's Institutional Repository. It has been accepted for inclusion in College of Arts & Sciences Senior Honors Theses by an authorized administrator of ThinkIR: The University of Louisville's Institutional Repository. This title appears here courtesy of the author, who has retained all other copyrights. For more information, please contact [email protected]. NOWHERE TO GO: INFORMAL SETTLEMENT ERADICATION IN KIGALI, RWANDA By Emily Elizabeth Benken Submitted in partial fulfillment of the requirements for Graduation summa cum laude and for Graduation with Honors from the Department of Anthropology University of Louisville May 2017 i ii NOWHERE TO GO: INFORMAL SETTLEMENT ERADICATION IN KIGALI, RWANDA By Emily Elizabeth Benken A Thesis Approved on March 27th, 2017 by the following Thesis Committee: Thesis Advisor Thesis Committee Member Thesis Committee Member iii DEDICATION This thesis is dedicated to my grandmother Mrs. Joyce Graeter Whose unending support made this thesis possible. -

TWUBAKANE Decentralization and Health Program Rwanda

TWUBAKANE Decentralization and Health Program Rwanda QUARTERLY PERFORMANCE MONITORING REPORT #18 APRIL— JUNE 2009 USAID/Rwanda Cooperative Agreement # 623-A-00-05-00020-00 Distribution: USAID/Rwanda Twubakane Team Partners Government of Rwanda Ministry of Local Administration Ministry of Health National AIDS Control Commission Twubakane Steering Committee Members Twubakane Partner Districts NGOs, Bilateral and Multi-lateral Partner Agencies Twubakane Quarterly Report #18, April-June, 2009 TABLE OF CONTENTS ACRONYMS ..................................................................................................................................... 1 TWUBAKANE PROGRAM HIGHLIGHTS APRIL-JUNE, 2009 ............................................................ 2 1. INTRODUCTION .................................................................................................................... 3 2. KEY ACCOMPLISHMENTS AND PROGRESS .......................................................................... 3 2.1 TWUBAKANE PROGRAM FIELD OFFICES ............................................................................ 4 3. PERFORMANCE REVIEW BY PROGRAM COMPONENT ........................................................ 4 3.1 FAMILY PLANNING/REPRODUCTIVE HEALTH ACCESS AND QUALITY .............................. 4 3.2 CHILD SURVIVAL, MALARIA AND NUTRITION ACCESS AND QUALITY .............................. 7 3.3 DECENTRALIZATION PLANNING, POLICY AND MANAGEMENT ....................................... 10 3.4 DISTRICT-LEVEL CAPACITY BUILDING .......................................................................... -

Exploring Rwanda's Continuing Education Capacity for Information Communications Technology (ICT) Skills Li Keen Lim SIT Study Abroad

SIT Graduate Institute/SIT Study Abroad SIT Digital Collections Independent Study Project (ISP) Collection SIT Study Abroad Fall 2017 Exploring Rwanda's Continuing Education Capacity for Information Communications Technology (ICT) Skills Li Keen Lim SIT Study Abroad Follow this and additional works at: https://digitalcollections.sit.edu/isp_collection Part of the Adult and Continuing Education Commons, African Languages and Societies Commons, African Studies Commons, Community-Based Learning Commons, Computer Sciences Commons, Technology and Innovation Commons, and the Vocational Education Commons Recommended Citation Lim, Li Keen, "Exploring Rwanda's Continuing Education Capacity for Information Communications Technology (ICT) Skills" (2017). Independent Study Project (ISP) Collection. 2690. https://digitalcollections.sit.edu/isp_collection/2690 This Unpublished Paper is brought to you for free and open access by the SIT Study Abroad at SIT Digital Collections. It has been accepted for inclusion in Independent Study Project (ISP) Collection by an authorized administrator of SIT Digital Collections. For more information, please contact [email protected]. Exploring Rwanda’s Continuing Education Capacity for Information Communications Technology (ICT) Skills SIT Study Abroad Rwanda: Post-Genocide Restoration and Peace Building Fall 2017 Independent Study Project Report Li Keen ‘Leeks’ Lim Academic Director: Celine Mukamurenzi Rwanda’s Continuing Education Capacity in ICT Skills Lim 1 List of Abbreviations AUCA Adventist University -

Health and Housing Portfolio PDF of Selected

MASS Design Group Select Projects Health and Housing March 2020 Architecture can heal. Butaro Oncology Support Centre Butaro, Burera District, Rwanda Infectious Disease Mitigation Over the past ten years, our team has developed an expertise in the planning, design, construction and evaluation of transformative healthcare environments. Our history has been defined by partnering with leading organizations at the front lines Select Project Chronology of the world’s major health challenges - from responding to acute epidemics of Ebola and cholera, to addressing the chronic injustices of structural health inequities. 2008 Butaro Medical Campus 2013 Rwinkwavu Hospital Masterplan Always prioritizing local capacity building and sustainable development practices, Butaro, Rwanda Rwinkwavu, Kayonza District, Rwanda we are uniquely positioned to shape innovative, elegant, and cost-effective health care infrastructure globally. 2011 GHESKIO Tuberculosis Hospital 2014 Albert Schweitzer Hospital Port-au-Prince, Haiti Lambarene, Gabon From our beginning, MASS, or a Model of Architecture Serving Society, has been committed to dignifying design that creates transformative impact. Our work in Butaro directly 2011 Rwinkwavu Neonatal Intensive Care Unit 2015 Buhanga Specialty Hospital responded to the needs of the community, and through continued proximate engagement, Rwinkwavu, Kayonza District, Rwanda Kigali, Rwanda we worked with Partners In Health and the Government of Rwanda to transform Butaro into 2011 Maternity Hospital of Rwanda 2015 Butaro Sharehousing a hub for global health excellence. Nyanza, Rwanda Butaro, Burera District, Rwanda Our work in Rwanda, Haiti, and Liberia taught us that true impact extended 2011 Mamohau Hospital 2015 University of Global Health Equity (UGHE) beyond the singular healthcare facility. We have worked directly with the communities Mamohau, Lesotho Butaro, Rwanda and governments of these nations to create new standards of healthcare infrastructure. -

Downloadable (540) BYAGUFASHA ______

Official Gazette nº 22 of 14/06/2021 Umwaka wa 60 Year 60 60ème Année Igazeti ya Leta n° 22 yo ku Official Gazette n° 22 of Journal Officiel n° 22 du wa 14/06/2021 14/06/2021 14/06/2021 Ibirimo/Summary/Sommaire page/urup. A. Iteka rya Ministiri w’Intebe/Prime Minister’s Order/Arrêté du Premier Ministre No 011/03 ryo ku wa 07/06/2021 Iteka rya Minisitiri w’Intebe ryirukana ku kazi Abashinjacyaha …………………………………..3 No 011/03 of 07/06/2021 Prime Minister’s Order dismissing from office Prosecutors……………………………………....3 No 011/03 du 07/06/2021 Arrêté du Premier Ministre portant révocation des Officiers de Poursuite Judiciaire ……………...3 B. Guhindura amazina/Change of names/Changement de noms Icyemezo gitanga uburenganzira bwo guhindura izina/Change of name certificate : MUTAMURIZA Grace ……………………………………………………………………..……8 NSHIMIYIMANA Patrick ………………………………………………………………………..9 NIYOMUGABO Albert ………………………………………………………………………....10 INGABIRE Delphine ……………………………………………………………………..……..11 NYIRANZABAMWITA Jeannette …………………………………..…………………………12 NGAMIJE Ali ………………………………………………………………………..………….13 SADIKI Jean …………………………………………………………………..………………...14 NSABIMBONA Serge ……………………………………………………………………..……15 GAKUBA Shikina ……………………………………………………………………..………..16 DUSENGIMANA Samuel ………………………………………………………………………17 1 Official Gazette nº 22 of 14/06/2021 AHORUKAMEYE Jean Pierre ………………………………………………………………….18 BAVARA John Bosco ……………………………………………………………………..……19 NKUNDABAREZI Benjamin …………………………………………………………………..20 RUGAMBWA Cherie …………………………………………………………………………...21 NGABONZIZA Ntwali …………………………………………………………………………22 -

Industrial Property Journal

REGISTRATION AND PROTECTION OF INTELLECTUAL PROPERTY RIGHTS INDUSTRIAL PROPERTY JOURNAL (Journal of Trademarks) No 29/2014 The 5th December, 2014 Published Monthly Application accepted for registration NOTICE is given that any person who has grounds of opposition to the Registration of any of the trade marks advertised herein according to these classes may within 60 days from the date of this Journal, Lodge a notice of opposition Letter from 05th December to 05th February 2015. The period of lodging the notice of opposition may be extended by Registrar as he deems fit and upon such terms as he may direct. Any request for such extension should be made to the Registrar to reach him before the expiry of the period allowed. 2 (310) RW/T/2014/428 (320) 17/09/2014 (330) (750) SHANTHA BIOTECHNICS LIMITED (731) 3rd & 4th Floor, Vasantha Chambers Fateh Maidan Road Basheerbagh Hyderabad, 500 004 ANDHRA PRADESH, India (740) TRUST LAW CHAMBERS Plot 1680 Umuganda Boulevard,Kimihurura,P.O.Box:6679 , kigali (510) (5) Vaccines for human use (540) ShanIPV ___________ (310) RW/T/2014/434 (320) 23/09/2014 (330) (750) Chemi & Cotex Industries Limited (731) P.O.Box: 347, Dar es Salaam, United Republic Of Tanzania (740) Cedar Ark Law 14th Floor, Kigali City Tower, Avenue du commerce, P.O.Box: 6428, Kigali (510) (3) Soaps; Perfumery; Essential Oils; Hair Products and Cosmetics (540) TRESSA PROFESSIONAL ___________ (310) RW/T/2014/514 (320) 05/11/2014 (330) (750) TRUSTCO RWANDA LTD (731) Kimihurura, P.O.Box: 3562, Kigali, Rwanda (740) SAM IBINGIRA Gasharu, Kicukiro, P.O.Box:3562, Kigali (510) (3) Cleaning and gardening (540) TRUSTCO (and logo) ___________ 3 (310) RW/T/2014/515 (320) 06/11/2014 (330) (750) BRALIRWA LTD (731) KN 500, Ngoma, Gasharu-Kicukiro, P.O.Box: 131 , Kigali, Rwanda (740) KAMUKUNDE Godfrey , Kigali (510) (32) Beers (540) LEGEND (and logo) ___________ 4 (310) RW/T/2014/516 (320) 06/11/2014 (330) (750) CATERPILLAR (QUINGZHOU) LTD (731) No. -

Exploring the Urban Digital Divide in Kigali: Spatial Analysis And

Exploring the Urban Digital Divide in Kigali: Spatial Analysis and Institutional Adaptation OTIOMA CHUKS February, 2017 SUPERVISORS: Dr. M. Madureira Dr. J.A. Martinez Exploring the Urban Digital Divide in Kigali: Spatial Analysis and Institutional Adaptation OTIOMA CHUKS Enschede, The Netherlands, February, 2017 Thesis submitted to the Faculty of Geo-Information Science and Earth Observation of the University of Twente in partial fulfilment of the requirements for the degree of Master of Science in Geo-Information Science and Earth Observation. Specialisation: Urban Planning and Management SUPERVISORS: Dr. M. Madureira Dr. J.A. Martinez THESIS ASSESSMENT BOARD: Dr. R.V. Sliuzas (Chair) Prof. Dr.-Ing. P. Gotsch (External Examiner) DISCLAIMER This document describes work undertaken as part of a programme of study at the Faculty of Geo-Information Science and Earth Observation of the University of Twente. All views and opinions expressed therein remain the sole responsibility of the author, and do not necessarily represent those of the Faculty. ABSTRACT The availability and use of the ICTs, which hold potentials for cities, are often uneven across geographies and demographics; a condition which has been referred to as the digital divide. Given the invisibility of digital access, certain geo-demographic groups could face the risk of digital exclusion. Bridging the digital divide entails understanding at least the baseline ICT asset ownership and use in the focus cases, to ensure that interventions are relevant to problem context and geography. However, most studies explore the digital divide at macro-spatial levels (frequently, national and regional levels), which makes them less relevant for knowledge generation and policies at intra-urban scales, the actual hubs of innovations. -

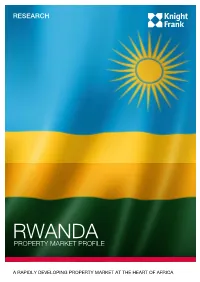

Rwanda Property Market Profile

RESEARCH RWANDA PROPERTY MARKET PROFILE A RAPIDLY DEVELOPING PROPERTY MARKET AT THE HEART OF AFRICA RWANDA: AFRICA’S UGANDA RISING STAR DEMOCRATIC The small landlocked country of Rwanda has emerged as Nyagatare REPUBLIC TANZANIA an unlikely star among Africa’s economies in recent years. OF THE Lake Burera Ruhengeri It has averaged GDP growth of more The capital Kigali is generally recognised CONGO than 7% per annum over the last as one of the cleanest, greenest and safest Byumba decade, outperforming the wider cities in Africa. Its streets are remarkably Sub-Saharan region. This has been litter-free; Rwanda was one of the first achieved despite Rwanda having fewer countries in the world to ban plastic bags Gisenyi natural resources than many of Africa’s and all adults participate in Umuganda, a other fast-growing economies. mandatory monthly clean-up day. Lake Ihema The country’s economic growth has The Rwandan government has placed RWANDA FIGURE 1 been fostered by the Rwandan information technology at the heart of the Kayonza GDP growth rates government’s investment in infrastructure country’s development. Its Vision 2020 KIGALI and by its concerted efforts to encourage Lake Kivu plan envisages a shift from an agricultural Kibuye Rwamagana business activity and entrepreneurship. 12% to a knowledge-based economy, and FORECAST It has introduced a series of reforms over 5,000 km of fibre optic cable has Gitarama Lake Mugesera with the specific aim of meeting the criteria been laid across the country. Kigali’s 10% of the World Bank’s Doing Business technology sector is currently centred Kibungo survey, which ranks countries’ commercial on Telecom House in Kacyiru; this is the environments. -

Mapping of Public Spaces in Kigali: Towards City-Wide Public Space Strategy

Mapping of Public Spaces in Kigali: Towards City-Wide Public Space Strategy June 2020 Copyright © June 2020 The Global Green Growth Institute Jeongdong Building 19F 21-15, Jeongdong-gil Jung-gu, Seoul, 100-784 Republic of Korea The Global Green Growth Institute does not make any warranty, either express or implied, or assumes any legal liability or responsibility for the accuracy, completeness, or any third party’s use or the results of such use of any information, apparatus, product, or process disclosed of the information contained herein or represents that its use would not infringe privately owned rights. The views and opinions of the authors expressed herein do not necessarily state or reflect those of the Global Green Growth Institute. Cover Image © Ilija Gubic Acknowledgements This report is drafted by Ilija Gubic of the Global Green Growth Institute and Solange Muhirwa of the City of Kigali with technical inputs by Inyumba Architectural Design LTD. Review of this report was done by Eric Hakizimana of the Ministry of Infrastructure and Dr. Ernest Nsabimana of the City of Kigali as well as Lilian Uwanziga Mupende of Global Green Growth Institute. Report is edited by Pamela Birungi of Global Green Growth Institute and designed by Inyumba Architectural Design LTD. This rapid assessment report is prepared to inform the much broader strategy of city’s public spaces, to support work of the Ministry of Infrastructure on reporting on average share of built up area of cities that is open and green for public use and above all will be a baseline for “Kigali Yacu: Activating Public Outdoor Space One Bench at a Time” initiative led by the City of Kigali. -

MAPPING of URBAN REFUGEES' Cover Photo of Downtown Kigali. Credit

MAPPING OF URBAN REFUGEES’ ACCESS TO ESSENTIAL SERVICES IN RWANDA Cover Photo of Downtown Kigali. Credit: Bigstock Images / Black Sheep Media January 2016 ACKNOWLEDGEMENTS This report is a result of team work and collaboration with different actors. It is written based on data collected by qualified and trained enumerators. Guided by MIDIMAR and UNHCR Rwanda office, CWS and YWCA Rwanda worked closely to design the survey tools, implement activities and analyze data. Without good collaboration and support from the Ministry of Disaster Management and Refugee Affairs (MIDIMAR), Government Local Leaders in both Kigali and Huye; and colleagues from UNHCR Kigali and Huye offices, this work would not have been realized. The project and report-writing team included: Mr. Innocent Hitayezu, independent consultant who who served as Mapping Coordinator; Bertrand Maniraguha, Data Entry Specialist with YWCA Rwanda; Erick Rutaihwa, Urban Refugees Self-Reliance Program Coordinator with CWS; and Andrew Fuys, Director for Program Innovation and Evaluation with CWS; with support from Pudentienne Uzamukunda, YWCA Rwanda’s Executive Director. We are extremely grateful to all respondents who accepted to dedicate their time and willingness to share some of their private information. Their inputs are highly valued. Finally, we thank all enumerators whose commitment and hard work enabled to reach out to as many respondents as possible. 2 of 55 DISCLAIMER This evaluation was commissioned jointly by Church World Service (CWS) and Young Women Christian Association (YWCA) Rwanda, in the framework of “Strengthening Urban Refugee Self Reliance” as funded by Church World Service (CWS) and UNHCR. This report offers independent analysis of CWS and YWCA Rwanda with technical support of the independent consultant; Mr. -

The Economic Geography of Rwanda

Final report The economic geography of Rwanda Anirudh Rajashekar Marion Richard Dimitri Stoelinga March 2019 When citing this paper, please use the title and the following reference number: C-38415-RWA-1 THE ECONOMIC GEOGRAPHY OF RWANDAN CITIES | MARCH 2019 This report was prepared by Laterite (www.laterite.com) and funded by the International Growth Centre (IGC) Support from the Ministry of Infrastructure (MININFRA) and the Rwanda Revenue Authority (RRA) were instrumental in the design and implementation of this study. Laterite would like to thank Mr. Edward Kyazze at MININFRA, and Ms. Agnes Kanyangeyo and Ms. Gaudence Uwimana at the RRA for their support. Laterite would also like to thank James Byiringiro and Venant Habarugira the National Institute of Statistics (NISR) for providing us with latest verisons of datasets we requested. Laterite is also extremely grateful for the helpful input, feedback and assistance of Sally Murray, Jonathan Bower, Victor Steenbergen and Ewoud Nijhof at the International Growth Centre over the course of the project. Dimitri Stoelinga, Anirudh Rajashekar and Marion Richard led the research team responsible for this report, with support from Mike O’Doherty, Carlo Menon and David Wickland. Laterite is a data, research and advisory firm based in Rwanda, Ethiopia, India, Uganda, Kenya and the Netherlands (www.laterite.com). Laterite specializes in innovative data collection and analysis techniques that help answer critical development questions. 2 THE ECONOMIC GEOGRAPHY OF RWANDAN CITIES | MARCH 2019 Contents -

Ibirimo/Summary/Sommaire Page/Urup

Official Gazette no.46 of 12/11/2018 Ibirimo/Summary/Sommaire page/urup. A. Guhindura amazina / Change of names / Changement de noms Icyemezo gitanga uburenganzira bwo guhindura izina: - NDAYISENGA Dan …………………………………………………..............................3 - NYAMUCENCERA Alexandra …………………………………....................................4 - BAKUNDUKIZE Cleophace …………………………………………………………....5 - MBARIMOMBAZI………………………………………………………………............6 - MIRUHO Ramadhan ……………………………………………………………….........7 - IZERE Guy…………………………………………………………………………….....8 - NIYOGAKIZA Hodal …………………………………………………………………... 9 - BIRIHANZE…………………………………………………………………………….10 - NDORIHIRWE………………………………………………………………………….11 - UMUNYANA Belyse …………………………………………………………………..12 - Anny KAKUZE…………………………………………………………………………13 Ingingo z’ingenzi z’urwandiko rusaba guhindura amazina: - NYIRANZAYINO Marie Diane………………………………………………………..14 - NYIRANDIMUBANZI Violette.....................................................................................14………………………………………………………. - BUNANI ………………………………………………………………………………. 15 - NTAKIYIMANA ……………………………………………………………………… 15 - DUNIYA Herve ……………………………………………………………………….. 16 - BAGUMA NDAYAMBAJE Frank …………………………………………………… 17 - UMUTONI Artine ……………………………………………………………………... 17 - AGASARO Johanna …………………………………………………………………… 18 - UWANYIRIGIRA Jacqueline …………………………………………………………18. - GIRAMATA Marguerite Marie Alacoque……………………………………………..18 - NYIRAMUBI Clementine ……………………………………………………………..19 - ZIBIKA LISA Fadhila …………………………………………………………………19 - KANDORO BUKASA ………………………………………………………………… 20 - UWIMANA Floride