FINAL DSST Financials FY2020

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Frequently Asked Questions

DSST FAQ’s for Incoming High School Students 2015-2016 1. What is the High School Dress Code? a. Shirts (tops) with a collar, this includes dresses. The sleeves must be short or long as long as it covers the student’s full shoulders. Turtlenecks, mock turtlenecks and polo shirt with a collar are also permitted. b. Pants – No jeans, capri’s mid-calf or lower, no leggings or tights c. Shoes – Must have hard bottom and be closed-toe, , no athletic shoes d. Skirts/Dresses – Must be 1 inch above the knee or lower 2. What classes do students take each year in High School? 9th Grade: 11th Grade: Physics Biology (option for Biology X) Humanities Earth Science Math (Integrated Algebra/Geometry 1 American Literature or 2 or Honors Algebra 2) Math (Algebra 2 or Pre-Calc or AP Spanish Calculus) *Student have the opportunity to choose Spanish between these two courses: U.S. History (option for U.S. History X) Internship Creative Engineering This course aims to bring technology such as 12th Grade: laser printing, computer coding, electronics, and 3D printing into projects. English Math (Pre-Calc or AP Calculus) Drama Civics This course is designed for students to learn Science (Choose Physics/AP Physics or and appreciate all aspects of Bio-Chem) theatre. Students will develop their creativity and imaginations with workshops in Lab (Choose Engineering or Bio-Tech) playwriting, set construction, costume and Senior Elective (Currently Spanish/AP makeup design, and performance Spanish, Psychology, AP Chemistry) Senior Project th 10 Grade: Chemistry World Literature Math (Integrated Algebra/Geometry 2, Algebra 2 or Honors Pre-Calc) Spanish World History 3. -

Breakthrough Kent Denver Inspiring Today’S Students and Tomorrow’S Teachers

Learn. Teach. Achieve. Breakthrough Kent Denver Inspiring Today’s Students and Tomorrow’s Teachers ANNUAL REPORT 2018-2019 1 OUR MISSION Breakthrough Kent Denver is a six-year after school and summer program To increase the that supports middle and high school students educational and through challenges and transitions while social opportunities simultaneously training aspiring educators. of motivated, financially under-resourced, middle and high school students through a All programs and services are provided at quality year-round no cost to all of our students. program. To motivate and train college students for Breakthrough’s Impact in 2018-2019: careers in education. 100% of Breakthrough high school seniors graduated in 2019 179 middle school students served from over 190 high school students served from over 60 Denver Public Schools (DPS) and Englewood Public Schools (EPS) 89% of Breakthrough graduates matriculated into an institution of higher education For eight consecutive years 100% of Breakthrough seniors have graduated high school! 35 days of additional academic instruction 25th year of closing the achievement gap in Denver Public Schools and Englewood Public Schools “Breakthrough is different because it’s not like typical school, classes are fun and it pushes us outside of our comfort zone by introducing us to things we’re not used to. For example, this summer every student was expected to get up in front of the community at some point either to present or perform something. Even though it can be scary, getting out of your comfort zone is something you have to do in order to grow. If I were to say one thing to anyone who hasn’t been to Breakthrough it would be, ‘you have to come.’” ” - Nashi Mason, 8th grade, GALS Middle School 2 DENVER & ENGLEWOOD Public School Partnerships Breakthrough Successfully Served 34 Denver and Englewood Middle Schools in 2018-2019 I-70 I-25 Bear Valley Federal Blvd. -

Raptor Rundown

Volume V Issue 3 DSST: Green Valley Ranch High School Raptor Rundown Director’s Note Core Values Hello Raptor Nation, *Respect * Responsibility * Courage * It was wonderful to see so many students and families at Back to * Curiosity * School Night – thank you for coming! We sincerely enjoyed the opportunity to meet our families, deepen relationships, and share *Integrity * Doing Your Best* our priorities for the school year. For families unable to attend, I want to take this opportunity to introduce our first GVR Campus Plus 1 Campaign. We know you work hard each and every day to support your students on their journey to college. Together, we know that we can strengthen our entire community by working together to support the greater communi- ty. From volunteering your time, sharing expertise, or making community connections, your help truly makes a differ- ence. All parents are asked to give ONE thing to our community this year; hence the theme, “+1”. Please find details about the +1 campaign attached to this Raptor Rundown, and please return the form with your student if you have not already. I’m looking forward to the second half of September – there are lots of exciting things happening in the DSST: GVR communi- ty. I am especially looking forward to our first college visits, homecoming week, and seniors submitting their first college ap- plications! As always, please do not hesitate to reach out to our team with any questions, feedback, or concerns. Best, Jenna Saludos Nacion de Raptores, Fue maravilloso ver a tantos estudiantes y familias en Noche de Regreso a la Escuela - gracias por venir! Disfrutamos sincera- mente la oportunidad de conocer a nuestras familias, profundizar las relaciones, y compartir nuestras prioridades para el año escolar. -

Announcements Families Will Now Receive Emergency Texts from the District

DSST: Green Valley Ranch High School Memo 10/01/2018 Announcements Update about drills at the Evie Dennis Campus: Families will now receive emergency texts from the district. The communications team will also send emergency robo-calls. Messages will be sent during crises such as lockdowns, evacuations and weather delays/closures. We are excited about this change because sending text messages will inform families of crises in a much shorter time frame than what it takes for a robo-call or robo- email to be delivered. Parents and guardians, you have been automatically opted-in to receive emergency texts based on cell phone numbers provided during registration. Please check to make sure your information is up-to-date in Parent Portal. Messages will be sent in English and Spanish. Learn more about lockdowns and lockouts here. Upcoming Dates: FAFSA Night – Tuesday, October 2nd, 4-7pm in Building 2 College Fair – Thursday, October 4th during the school day Hispanic Cultural Celebration – Thursday, October 11th, 5pm (in Cafeteria) Picture Day Retakes – Tuesday, October 16th. Chipotle Fundraiser - Tuesday, October 16th from 4:00pm-8:00pm. Student Opportunities www.InvolveBoard.com Looking for more ways to explore your passions and get involved in the community?!? Check out Involve Board! Make an account and browse the opportunities. There are new programs being added all the time, so check back often! CU Pre-Health Scholars Program: The Anschutz Medical campus is recruiting freshmen, sophomores and juniors to join the CU Pre-Health Scholars Program (CUPS). The CUPS Program includes monthly Saturday session focused on career exploration and development, as well as hands-on summer academies throughout your high school years. -

2019-2020 Leverage Leadership Institute Fellow Profiles

2019-2020 LEVERAGE LEADERSHIP INSTITUTE FELLOW PROFILES Riley Bauling Regional Superintendent, Achievement First Brooklyn, NY Riley Bauling is a regional superintendent for Achievement First, working with New York-based middle schools and principals. Prior to his current role, he was the principal of Achievement First Bushwick Middle School. Before becoming principal, he taught math after being placed there by Teach For America and worked as the STEM dean at the school. In a previous life, he was a policy analyst for the Albuquerque City Council, ran literacy tutoring programs in Bremerton, Wash., and was a journalist in Albuquerque, N.M. He has his bachelor’s degree from the University of New Mexico in political science, and a master’s of public administration from New York University, along with a master’s of education from Hunter College. In his free time, he loves spending time with his wife, Leah, and their dog, Oso. Alex Bronson Principal, Williamsburg Collegiate, Uncommon Schools Brooklyn, NY Alex Bronson became the Principal at Williamsburg Collegiate Charter School after working as a 5th grade science teacher and Dean of Curriculum and Instruction at WCCS. Alex was a 2007 Teach for America Corps Member in Brooklyn, NY where she first fell in love with teaching. After her first two years of teaching Alex sought a community of people working together to end educational inequity, which is when she found Uncommon Schools. Under her leadership WCCS has grown both academically and culturally, seeing double digit gains in math and ELA on the State Exam. Alex is deeply invested in the mission at Uncommon Schools and is grateful for the opportunity to track student progress not only in middle school but in high school and college as well. -

A 21St Century School System in the Mile-High City

A 21ST CENTURY SCHOOL SYSTEM IN THE MILE-HIGH CITY BY DAVID OSBORNE A 21ST CENTURY SCHOOL SYSTEM IN THE MILE-HIGH CITY 2 PROGRESSIVE POLICY INSTITUTE A 21ST CENTURY SCHOOL SYSTEM IN THE MILE-HIGH CITY A 21ST CENTURY SCHOOL SYSTEM IN THE MILE-HIGH CITY BY DAVID OSBORNE MAY 2016 PROGRESSIVE POLICY INSTITUTE 3 A 21ST CENTURY SCHOOL SYSTEM IN THE MILE-HIGH CITY ACKNOWLEDGMENTS David Osborne would like to thank the Walton Family Foundation, The Eli and Edythe Broad Foundation, and the Laura and John Arnold Foundation for their support of this work. He would also like to thank the dozens of people within Denver Public Schools, Denver’s charter schools, and the broader education reform community who shared their experience and wisdom with him. Thanks go also to those who generously took the time to read drafts and provide feedback. Finally, David is grateful to those at the Progressive Policy Institute who contributed to this report, including President Will Marshall, who provided editorial guidance, intern Cullen Wells, who assisted with graphs, and Steven K. Chlapecka, who shepherded the manuscript through to publication. 4 PROGRESSIVE POLICY INSTITUTE A 21ST CENTURY SCHOOL SYSTEM IN THE MILE-HIGH CITY TABLE OF CONTENTS A 21ST CENTURY SCHOOL SYSTEM IN THE MILE-HIGH CITY THE DENVER STORY . 2 MEASURING PERFORMANCE: DENVER’S SCHOOL PERFORMANCE FRAMEWORK . 6 WINNING THE POLITICIAL BATTLE . 10 DELIVERING RESULTS . 11 DENVER’S SCHOOL CHOICE ENVIRONMENT . 12 CHARTER SCHOOLS LEAD THE WAY . 16 INNOVATION SCHOOLS STRUGGLE FOR AUTONOMY . 18 DENVER’S REMAINING CHALLENGES . 22 DENVER OFFERS A LESSON ON PERFORMANCE PAY . -

The Anschutz Foundation

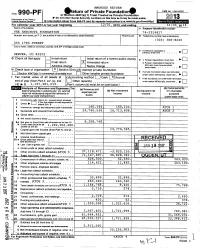

AMENDED RETURN OMB No 1545-0052 *eturn of Private Foundatio n Form 990 -PF or'^3ection 4947(a)(1) Trust Treated as Private Foundation 10, Do not enter Social Security numbers on this form as it may be made public. 2013 Department of the Treasury Internal Revenue Service ► Information about Form 990-PF and its separate Instructions is at v ww.its.gov/form990pf. • • • • For calendar y ear 2013 or tax y ear beg inning 12/01 , 2013, and endin g 11/30, 2014 Name of foundation A Employer Identification number THE ANSCHUTZ FOUNDATION 74-2316617 Number and street (or P 0 box number if mail is not delivered to street address ) Room/suite B Telephone number (see instructions) (303) 308-8220 555 17TH STREET City or town, state or province , country, and ZIP or foreign postal code q C If exemption application is ► pend ing, ch eck here • • • • • • DENVER, CO 80202 G Check all that apply Initial return Initial return of a former public charity D 1 . oreign F organizations , check here . ► Ti Final return X Amended return 2. Foreign organizations meeting the q Address chan 85% test, check here and attach ► ge Name change com p utation • • • • . • H Check type of organization X Section 501(c 3 exempt private foundation E If private foundation status was terminated Section 4947 ( a)( 1 ) nonexem pt charitable trust Other taxable p rivate foundation under q section 507(b)(1)(A) , check here . ► I Fair market value of all assets at J Accounting method Cash X Accrual F If t h e foundation is in a 60-month termination end of year (from Part Il, col (c), line Other (specify) E] _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ __ under section 507(b)(1)(B). -

CVHS 21-22 DSST Student Family

Student and Family Handbook 2021-2022 DSST: DSST College View High School Page | 1 Table of Contents Letter from the School Director • Page1 DSST Public Schools’ Mission • Page2 DSST Public Schools’ Vision • Page3 DSST Public Schools’ Core Values • Page4 DSST Public Schools’ Guiding Principles • Page5 I. Campus Policies • Page6 Closed Campus Attendance Arrival and Dismissal Dress Code Parents/Guardians and Visitors Student Phone Usage Deliveries to Students II. Academic Policies • Page10 Academic Honor Code Academic Effort Advisory Program Grades Report Cards and Progress Reports Honors and Awards Middle School Promotion Requirements High School Promotion Requirements Graduation Requirements III. Discipline • Page19 Student Behavioral Expectations Policies Habitually Disruptive Student Actions that May Warrant Interventions or Suspensions Actions that will Lead to an Expulsion Hearing The Discipline Process Consequences Expulsion Page | 2 IV. Facilities and Resources Policies • Page24 School Property Textbooks Laptop Computers Responsibility for Personal Property Lost and Found School Supplies Student Resource Fees V. General School Policies • Page26 Non-Discrimination Statement Student Records and FERPA Mandated Reporting of Suspected Abuse and Neglect Media Release Distribution of Published Materials or Documents Commerce Enrollment Transportation Informal Parent/Guardian Grievance Policy Formal Parent/Guardian Grievance Policy VI. Athletics and Extracurricular Activities • Page28 Participation Science and Tech Parent Group (STP) VII. Weather and Emergency Procedures • Page29 Accident or Medical Emergency School Closings Fire Alarms and Building Emergencies Appendices for Current Academic School Year • Page30 A. School Hours B. Student Dress Code for the 2020-2021 School Year C. Make-up Work Policy D. Student Technology Use Summary E. Family and Student Core Value Pledge F. -

To Download the 2019-2020 BKD

Learn. Teach. Achieve. at KENT DENVER ANNUAL REPORT 2019-2020 WHO ARE WE? WHAT’S OUR IMPACT? at KENT DENVER OUR MISSION To increase the is a six-year after school and summer program that educational and supports middle and high school students through social opportunities challenges and transitions while simultaneously of motivated, financially training aspiring educators. under-resourced middle and high school All programs and services are provided students through a at no cost to all of our students quality year-round and Teaching Fellows. program. To motivate and train BREAKTHROUGH’S IMPACT IN 2019-2020: college students for careers in education. 100% of Breakthrough high school seniors graduated in 2020 100% of Breakthrough 2020 graduates are pursuing a college degree 12% of students deferred enrollment, due to COVID-19, to Spring or Fall 2021 184 middle school students 200 high school students 60 Denver Public Schools (DPS) and Englewood Public Schools (EPS) For nine consecutive years 100% of Breakthrough seniors have graduated high school! 35 days of additional in person and virtual academic instruction 26th year of closing the opportunity gap in Denver Public Schools and Englewood Public Schools “What made me apply for Breakthrough was the ability to get ahead and be more prepared for the following year. One thing I really love now about being a part of Breakthrough is the teachers and full community. All of the teachers are very loving and caring and as a student they make me feel valued and supported ” - Anthony Martinez-Baros, 8th grade, Strive Prep Westwood 2 DENVER & ENGLEWOOD PUBLIC SCHOOL PARTNERSHIPS Breakthrough successfully served middle and high school students from over 60 Denver and Englewood Public Schools in 2019-2020 MIDDLE SCHOOLS SERVED: I-70 I-25 Federal Blvd. -

DECEMBER 2013 Winter Welcome Kicks Off the Holiday Season

Distributed to the Stapleton, Park Hill, Lowry, Montclair, Mayfair, Hale and East Colfax neighborhoods DENVER, COLORADO DECEMBER 2013 Winter Welcome Kicks Off the Holiday Season Nearly 3,000 people gathered in the 29th Ave. Town Center for the 2013 Winter Welcome, a Staple- Greenway. New to Winter Welcome this year: the MCA closed 29th Avenue from Quebec to Roslyn ton holiday tradition. This year the Girl Scouts made 1,000 s’mores and all but 30 were eaten. Pro- to have more room for the festivities, and a reindeer and a snowboard simulator were added. ceeds from the event will go to The Urban Farm, Bluff Lake Nature Center and Sand Creek Regional Look on page 35 for another perspective on the holidays—the carbon footprint. Check out our new interactive Stapleton Reacts to Elementary Boundary Changes website and comment on articles. www.FrontPorchStapleton.com By Carol Roberts n the rest of DPS, and in most public school districts across the country, school Guide to Kids’ Sports I In January the Front Porch will print a attendance is established by directory of NE Denver sports teams boundaries. The location of a for kids. Parents and coaches please person’s home determines their send name of sport, name of assigned neighborhood school. league and contact information to However, from the time [email protected]. Stapleton opened its second If known, please also elementary school, a different include ages, whether kind of system was established— boys, girls or both, one that allows everyone in the seasons, and a contact community to select from all the person who could pro- schools. -

FY15 Q4 CC Transactions

Posting Date Merchant Name Merchant City, State/Province Amount 4/1/2015 Einstein Bros Bagels3350 Aurora, CO $33.61 4/10/2015 Brunswick Zone Green M Lakewood, CO $1,018.98 4/10/2015 Carmines On Penn Italian Denver, CO $6.43 4/10/2015 Dollartree.Com 877-530-8733, VA $88.08 4/10/2015 Papa John'S 04224 303-371-7272, CO $28.65 4/10/2015 Chipotle 0871 Aurora, CO $48.45 4/10/2015 King Soopers #0019 Denver, CO $43.52 4/10/2015 Paypal Sosoutreach 402-935-7733, CA $387.50 4/13/2015 King Soopers #0083 Denver, CO $45.08 4/13/2015 Hobby-Lobby #0017 Aurora, CO $21.55 4/13/2015 Papa John'S 04224 303-371-7272, CO $33.27 4/13/2015 Wal-Mart #5334 Aurora, CO $82.37 4/13/2015 Norcostco Denver 303-6209734, CO $1,246.16 4/13/2015 Sq Restrant Moe'S Broadw Denver, CO $42.40 4/13/2015 Target 00028209 Denver, CO $12.04 4/13/2015 Wm Supercenter #3566 Denver, CO $20.11 4/13/2015 York Street Crossfit L Denver, CO $720.00 4/13/2015 York Street Crossfit L Denver, CO $720.00 4/13/2015 Dolrtree 4834 00048348 Denver, CO $79.93 4/13/2015 Wal-Mart #5334 Aurora, CO $21.56 4/13/2015 Travel Insurance Policy 800-729-6021, VA $8.50 4/13/2015 Southwes 5262499234015 800-435-9792, TX $408.00 4/13/2015 Southwes 5260664436529 800-435-9792, TX $25.00 4/13/2015 Amtrak .Com 1000706033940 Washington, DC $72.00 4/13/2015 Unique Lives Experien 416-449-8118, ON $254.00 4/13/2015 Cross Border Trans Fee $2.54 4/13/2015 Unique Lives Experien 416-449-8118, ON $63.50 4/13/2015 Cross Border Trans Fee $0.64 4/13/2015 Pizza Hut 000-0000000, CO $42.83 4/13/2015 Papa John'S 04224 303-371-7272, CO -

2020-21 Great Schools Enrollment Guide Secondary

2020-21 GREAT SCHOOLS ENROLLMENT GUIDE SECONDARY DPS VISION: EVERY CHILD SUCCEEDS! TABLE OF CONTENTS Choosing a School in DPS �������������� 5 Denver School of Innovation and SOUTHEAST����������������������������71 School Performance Sustainable Design 43 DELTA High School 72 Framework ���������������������������������������� 6 Dora Moore 43 Denver Green School Enrollment and SchoolChoice ������� 8 DSST: Cole High School 44 Southeast 72 School Programs���������������������������� 10 DSST: Cole Middle School 44 Denver Language School – Transportation ������������������������������� 14 DSST: Conservatory Green Whiteman Campus 73 Meeting Your Student’s Needs ���� 16 High School 45 DSST: Byers High School 73 District Map ����������������������������������� 20 DSST: Conservatory Green DSST: Byers Middle School75 Middle School 46 George Washington High School 75 FAR NORTHEAST �������������������23 DSST: Montview Grant Beacon Middle School 76 Collegiate Prep Academy24 High School 46 Hamilton Middle School 76 DCIS at Montbello 24 DSST: Montview Highline Academy Southeast 77 Dr Martin Luther King, Jr Middle School 47 Hill Campus of Arts Early College 25 East High School 47 and Sciences 78 DSST: Green Valley Ranch Emily Griffith High School 48 Merrill Middle School 78 High School 25 Manual High School 48 Place Bridge Academy 80 DSST: Green Valley Ranch McAuliffe International School 49 Middle School 27 Rocky Mountain School of McAuliffe Manual Expeditionary Learning 81 DSST Middle School at Middle School 49 Noel Campus 27 Slavens School 81 Morey