Market Study

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Baltlink Rider Guide-944004A2.Pdf

WHAT IS BALTIMORELINK? BaltimoreLink is a complete overhaul and rebranding of the core transit system operating within Baltimore City and the surrounding region. Many of MTA’s current bus routes are outdated, and BaltimoreLink will improve service through a more reliable and efficient network. BaltimoreLink also includes transfer facilities, dedicated bus lanes, signal priority, and improved bus stop signs, among many other improvements. To deliver an interconnected transit network, existing MTA bus and rail services will be restructured and renamed: • CityLink: Twelve new high-frequency, color-coded bus routes will connect with each other, as well as Metro SubwayLink, Light RailLink, MARC Train, Commuter Bus, Amtrak, and other services, into one integrated transit network. • LocalLink (currently Local Bus): LocalLink routes will provide comprehensive crosstown connections and improved connections to neighborhoods and communities throughout the system. • Express BusLink (currently Express Bus): Express BusLink will include several existing Express Bus services that provide suburb-to- city connections and recently launched routes providing suburb-to-suburb connections. Typically, Express Bus routes have fewer stops and use higher speed roads. • Light RailLink (currently Light Rail): Light Rail service will operate along the same line but with improved connections to buses. • Metro SubwayLink (currently Metro Subway): This service will not change but will have improved connections to buses. baltimorelink.com | 1 BETTER BUS STOPS BALTIMORELINK RESOURCE INFORMATION To create a better rider experience by providing information you can use, the MTA will be All MTA routes will change under installing new bus stop signs throughout the BaltimoreLink. Please look for Rider Alerts for entire MTA bus network. -

Film Production Activity Tax Credit Report 2014

Maryland Film Production Activity Tax Credit Annual Report Pursuant to Tax General Article §10-730 Submitted by Maryland Department of Business and Economic Development December 2014 Maryland Film Production Activity Tax Credit Overview CH 516 Acts of 2011 created the Film Production Activity Tax Credit (Film Tax Credit). The Act repealed the existing Film Production Rebate Program and replaced it with a tax credit for qualified direct costs of qualified film production activities including feature films and television series. Under the Film Tax Credit, the Department of Business and Economic Development (DBED) could award a maximum of $7.5 million in credits, in each fiscal year, beginning in FY 2012 through FY 2014. Qualifying production activities were eligible for a tax credit of up to 25% of the qualified direct costs for a feature film and 27% for a television series. If the amount of the tax credit exceeded the total tax liability in the tax year, the entity could claim a refund in the amount of the excess. The Act became effective on July 1, 2011 with a sunset date of June 30, 2014. A total of $22.5M ($7.5 per FY) in tax credits was available for FYs 2012 through 2014. All of those tax credits were committed to six productions by January 2012 to: House of Cards – Season 1; VEEP – Seasons 1 & 2; Jamesy Boy; Better Living through Chemistry; and, Ping Pong Summer. In order to retain the filming of the two television series House of Cards and VEEP in Maryland, CH 28 Acts of 2013 increased the Film Tax Credit by $32.5M over three years and extended the sunset through FY 2016. -

Resolution #20-9

BALTIMORE METROPOLITAN PLANNING ORGANIZATION BALTIMORE REGIONAL TRANSPORTATION BOARD RESOLUTION #20-9 RESOLUTION TO ENDORSE THE UPDATED BALTIMORE REGION COORDINATED PUBLIC TRANSIT – HUMAN SERVICES TRANSPORTATION PLAN WHEREAS, the Baltimore Regional Transportation Board (BRTB) is the designated Metropolitan Planning Organization (MPO) for the Baltimore region, encompassing the Baltimore Urbanized Area, and includes official representatives of the cities of Annapolis and Baltimore; the counties of Anne Arundel, Baltimore, Carroll, Harford, Howard, and Queen Anne’s; and representatives of the Maryland Departments of Transportation, the Environment, Planning, the Maryland Transit Administration, Harford Transit; and WHEREAS, the Baltimore Regional Transportation Board as the Metropolitan Planning Organization for the Baltimore region, has responsibility under the provisions of the Fixing America’s Surface Transportation (FAST) Act for developing and carrying out a continuing, cooperative, and comprehensive transportation planning process for the metropolitan area; and WHEREAS, the Federal Transit Administration, a modal division of the U.S. Department of Transportation, requires under FAST Act the establishment of a locally developed, coordinated public transit-human services transportation plan. Previously, under MAP-21, legislation combined the New Freedom Program and the Elderly Individuals and Individuals with Disabilities Program into a new Enhanced Mobility of Seniors and Individuals with Disabilities Program, better known as Section 5310. Guidance on the new program was provided in Federal Transit Administration Circular 9070.1G released on June 6, 2014; and WHEREAS, the Federal Transit Administration requires a plan to be developed and periodically updated by a process that includes representatives of public, private, and nonprofit transportation and human services providers and participation by the public. -

Realty • 2012 Annual Report

Kimco Realty • 2012 Annual Report REALTY REALTY 3333 New Hyde Park Road New Hyde Park, NY 11042 Tel: 516-869-9000 blog.kimcorealty.com / kimcorealty.com 2012 Annual Report REALTY 247947KIM_Cvr_R1.indd 1 REALTY 3/12/13 1:42 PM Corporate Directory REALTY Board of Directors v Milton Cooper Philip E. Coviello (1)(2)(3) Richard G. Dooley (1)(2)(3 ) Executive Chairman Partner * Lead Independent Director Kimco Realty Corporation Latham & Watkins LLP Executive Vice President & Chief Investment Officer * Massachusetts Mutual Life Insurance Company Joe Grills (1)(2v)(3) David B. Henry F. Patrick Hughes (1v)(2)(3) Chief Investment Officer * Vice Chairman, President President IBM Retirement Fund & Chief Executive Officer Hughes & Associates LLC * Retired Kimco Realty Corporation (1) Audit Committee (2) Executive Compensation Committee Frank Lourenso Colombe M. Nicholas (2)(3) Richard Saltzman (2)(3) (3) Nominating and Corporate Executive Vice President Consultant President Governance Committee v JPMorgan Chase & Co. Financo Global Consulting Colony Capital LLC Chairman REALTY Executive Management Milton Cooper David B. Henry Michael V. Pappagallo Glenn G. Cohen Executive Chairman Vice Chairman, President Executive Vice President Executive Vice President, & Chief Executive Officer & Chief Operating Officer Chief Financial Officer & Treasurer Corporate Management David F. Bujnicki Adam M. Cohen Raymond Edwards Fredrick Kurz Leah Landro Vice President, Vice President, Vice President, Vice President Vice President, Investor Relations & Tax Retailer Services & General Manager, Human Resources Corporate Communications Risk Management Scott G. Onufrey Bruce Rubenstein Thomas R. Taddeo Paul Westbrook Senior Vice President, Senior Vice President, Vice President, Vice President, Acquisitions & Investment General Counsel & Chief Information Officer Chief Accounting Officer Management Secretary U.S. -

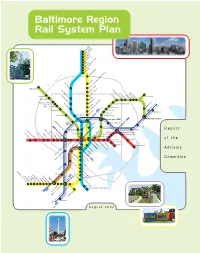

Baltimore Region Rail System Plan Report

Baltimore Region Rail System Plan Report of the Advisory Committee August 2002 Advisory Committee Imagine the possibilities. In September 2001, Maryland Department of Transportation Secretary John D. Porcari appointed 23 a system of fast, convenient and elected, civic, business, transit and community leaders from throughout the Baltimore region to reliable rail lines running throughout serve on The Baltimore Region Rail System Plan Advisory Committee. He asked them to recommend the region, connecting all of life's a Regional Rail System long-term plan and to identify priority projects to begin the Plan's implemen- important activities. tation. This report summarizes the Advisory Committee's work. Imagine being able to go just about everywhere you really need to go…on the train. 21 colleges, 18 hospitals, Co-Chairs 16 museums, 13 malls, 8 theatres, 8 parks, 2 stadiums, and one fabulous Inner Harbor. You name it, you can get there. Fast. Just imagine the possibilities of Red, Mr. John A. Agro, Jr. Ms. Anne S. Perkins Green, Blue, Yellow, Purple, and Orange – six lines, 109 Senior Vice President Former Member We can get there. Together. miles, 122 stations. One great transit system. EarthTech, Inc. Maryland House of Delegates Building a system of rail lines for the Baltimore region will be a challenge; no doubt about it. But look at Members Atlanta, Boston, and just down the parkway in Washington, D.C. They did it. So can we. Mr. Mark Behm The Honorable Mr. Joseph H. Necker, Jr., P.E. Vice President for Finance & Dean L. Johnson Vice President and Director of It won't happen overnight. -

6 12 14 18 Proposal Would Bring Walmart Supercenter to Owings

INSIDE THIS ISSUE SEPTEMBER 2016 A free publication serving Owings Mills, Pikesville, Randallstown, Reisterstown, Windsor Mill, Woodlawn and Catonsville 6 A speaker at the Aug. 31 Seeking Justice community input meeting in Randallstown protests plans for Korryn for Kimco Realty to bring Gaines the area’s third Walmart to Owings Mills Mall. 12 Community Gives Input on New Courthouse 14 Will Macy’s Close at Security Proposal Would Bring Mall? Walmart Supercenter to Owings Mills Mall Community gets vocal Owings Mills Mall is in demolition mode, as heavy equipment is taking down the 30-year-old mall to rubble. While the community has lamented the slow decline of the mall, which 18 closed in January and once catered to upscale shoppers with a Saks Fifh Event Gets Avenue, Lord and Taylor and Macy’s as anchors, residents are looking forward Students Ready to a new shopping experience. Te redevelopment plan, they were told, was to for School replace the property with an open-air shopping center similar to Hunt Valley “I WILL DO EVERYTHING IN Towne Centre and the Avenue at White Marsh. Many looked forward a robust MY POWER TO MAKE SURE Be among the first to mix of department and big box stores, smaller national discount retailers and THE RANDALLSTOWN be in the know. Sign up boutique shops. WALMART DOES NOT Tose expectations were dashed when District 4 Councilman Julian Jones CLOSE.” for news updates from sent an email inviting constituents to two community input meetings to weigh nwvoicenews.com. Julian Jones, District 4 continued on page 20 Baltimore County Councilman Page 2 Northwest Voice September 2016 From the Publisher, Kenneth Brown What is the Role of Developers, the Community in Retail Success? I attended the community input meetings held opportunity to get involved sooner, either by their Boulevard to analyze the situation and start last month in Owings Mills and Randallstown own proactivity or by elected ofcials or business communicating with mall and business owners and concerning the future redevelopment of the leaders soliciting their input. -

Realty • 2012 Annual Report

Kimco Realty • 2012 Annual Report REALTY REALTY 3333 New Hyde Park Road New Hyde Park, NY 11042 Tel: 516-869-9000 blog.kimcorealty.com / kimcorealty.com 2012 Annual Report REALTY 247947KIM_Cvr_R1.indd 1 REALTY 3/12/13 1:42 PM Corporate Directory REALTY Board of Directors v Milton Cooper Philip E. Coviello (1)(2)(3) Richard G. Dooley (1)(2)(3 ) Executive Chairman Partner * Lead Independent Director Kimco Realty Corporation Latham & Watkins LLP Executive Vice President & Chief Investment Officer * Massachusetts Mutual Life Insurance Company Joe Grills (1)(2v)(3) David B. Henry F. Patrick Hughes (1v)(2)(3) Chief Investment Officer * Vice Chairman, President President IBM Retirement Fund & Chief Executive Officer Hughes & Associates LLC * Retired Kimco Realty Corporation (1) Audit Committee (2) Executive Compensation Committee Frank Lourenso Colombe M. Nicholas (2)(3) Richard Saltzman (2)(3) (3) Nominating and Corporate Executive Vice President Consultant President Governance Committee v JPMorgan Chase & Co. Financo Global Consulting Colony Capital LLC Chairman REALTY Executive Management Milton Cooper David B. Henry Michael V. Pappagallo Glenn G. Cohen Executive Chairman Vice Chairman, President Executive Vice President Executive Vice President, & Chief Executive Officer & Chief Operating Officer Chief Financial Officer & Treasurer Corporate Management David F. Bujnicki Adam M. Cohen Raymond Edwards Fredrick Kurz Leah Landro Vice President, Vice President, Vice President, Vice President Vice President, Investor Relations & Tax Retailer Services & General Manager, Human Resources Corporate Communications Risk Management Scott G. Onufrey Bruce Rubenstein Thomas R. Taddeo Paul Westbrook Senior Vice President, Senior Vice President, Vice President, Vice President, Acquisitions & Investment General Counsel & Chief Information Officer Chief Accounting Officer Management Secretary U.S. -

“Get on the Bus” Transportation to Places of Interest from UMBC

“Get on the Bus” Transportation to Places of Interest from UMBC BWI and Light Rail Towson Town Center/Towson University Take UMBC Shuttle Bus BWI MARC Line to Take MTA bus #35 to Baltimore and Charles BWI MARC/Amtrak Station and take the free Streets. On Baltimore Street, transfer to MTA shuttle bus from there to BWI airport or to the bus #8 which goes to Towson University. BWI Light Rail Station. Hunt Valley Inner Harbor Take the UMBC Shuttle Bus BWI MARC Take MTA Bus #35 to downtown. Exit at Line to the BWI MARC/Amtrak Station (Mon- corner of Pratt and Charles Streets. Proceed Frie) and take the free shuttle to the BWI Light East on Pratt Street to Inner Harbor. Rail Station. Take the Blue Light Rail north to Hunt Valley, or: Arundel Mills Mall Take the MTA bus #35 to Pratt St. and Take UMBC Shuttle Bus BWI MARC Line Howard St. Then, take the Light Rail north to (Mon-Fri) to BWI MARC/Amtrak Station. Hunt Valley. From there, take MTA Bus #17 to Arundel Mills Mall, or: Greenbelt Metro Station Fri-Sun, take the UMBC Shuttle Bus Arundel Take the UMBC Shuttle Bus Mills Line to the Arundel Mills Mall. Halethorpe/Satellite Line to the Halethorpe MARC station. From Halethorpe, take the Security Square Mall Penn Line Marc Train to BWI MARC/Amtrak Take MTA Bus #77 to Security Blvd. and Station and take the free shuttle bus from there Belmont Avenue. to BWI airport. Proceed to the bus stop at Pier E on the lower level of the international Westview Shopping Center terminal. -

Radio Shack Closing Locations

Radio Shack Closing Locations Address Address2 City State Zip Gadsden Mall Shop Ctr 1001 Rainbow Dr Ste 42b Gadsden AL 35901 John T Reid Pkwy Ste C 24765 John T Reid Pkwy #C Scottsboro AL 35768 1906 Glenn Blvd Sw #200 - Ft Payne AL 35968 3288 Bel Air Mall - Mobile AL 36606 2498 Government Blvd - Mobile AL 36606 Ambassador Plaza 312 Schillinger Rd Ste G Mobile AL 36608 3913 Airport Blvd - Mobile AL 36608 1097 Industrial Pkwy #A - Saraland AL 36571 2254 Bessemer Rd Ste 104 - Birmingham AL 35208 Festival Center 7001 Crestwood Blvd #116 Birmingham AL 35210 700 Quintard Mall Ste 20 - Oxford AL 36203 Legacy Marketplace Ste C 2785 Carl T Jones Dr Se Huntsville AL 35802 Jasper Mall 300 Hwy 78 E Ste 264 Jasper AL 35501 Centerpoint S C 2338 Center Point Rd Center Point AL 35215 Town Square S C 1652 Town Sq Shpg Ctr Sw Cullman AL 35055 Riverchase Galleria #292 2000 Riverchase Galleria Hoover AL 35244 Huntsville Commons 2250 Sparkman Dr Huntsville AL 35810 Leeds Village 8525 Whitfield Ave #121 Leeds AL 35094 760 Academy Dr Ste 104 - Bessemer AL 35022 2798 John Hawkins Pky 104 - Hoover AL 35244 University Mall 1701 Mcfarland Blvd #162 Tuscaloosa AL 35404 4618 Hwy 280 Ste 110 - Birmingham AL 35243 Calera Crossing 297 Supercenter Dr Calera AL 35040 Wildwood North Shop Ctr 220 State Farm Pkwy # B2 Birmingham AL 35209 Center Troy Shopping Ctr 1412 Hwy 231 South Troy AL 36081 965 Ann St - Montgomery AL 36107 3897 Eastern Blvd - Montgomery AL 36116 Premier Place 1931 Cobbs Ford Rd Prattville AL 36066 2516 Berryhill Rd - Montgomery AL 36117 2017 280 Bypass -

Michael P. Tanczyn, Pa

IN THE MATTER OF * BEFORE THE THE APPLICATION OF SECURITY SQUARE ASSOCIATES * COUNTY BOARD OF APPEALS - PETITIONER FOR A ZONING VARIANCE ON PROPERTY LOCATED * OF ON THE SOUTHWEST SIDE SECURITY BOULEVARD AT 1-695, 1374' * BALTIMORE COUNTY EAST OF BELMONT AVENUE (6901 SECURITY BOULEVARD) * CASE NO. 98-297-A 1ST ELECTION DISTRICT 1ST COUNCILMANIC DISTRICT * * * * * * * * * * o PIN ION This case comes to the County Board of Appeals of Baltimore County based upon an appeal by People's Counsel for Baltimore County from a .decision of the Deputy Zoning Commissioner in which a Petition for Variance was granted in part and dismissed in part as moot. A public hearing was held on Thursday, September 3, 1998. Peter Max Zimmerman,. People's Counsel for Baltimore County was the Appellant; and Michael P. Tanczyn, Esquire, represented the Petitioner. Public deliberation was held on September 17, 1998. Subsequent to opening statements by Mr. Zimmerman and Mr. Tanczyn, the Petitioners offered three witnesses in support of their request for variance. Mr. John C. Mellema, Jr., a licensed property line surveyor, testified as to his qualifications, familiarity with Baltimore County Zoning Regulations, and was accepted without objection as an expert in the field of land surveying. A number of exhibits were offered into evidence. Petitioner's No. I, a plat of the subject property, and petitioner's Exhibit No.2, a detail of the current signage along with a substantial number of other photographs which reflected the site and various roadway systems which provided entry either into or around the shopping mall. Mr. Mellema described the general area of the Social Security mall and surrounding area. -

Leesburg Corner Premium Outlets® the Simon Experience — Where Brands & Communities Come Together

LEESBURG CORNER PREMIUM OUTLETS® THE SIMON EXPERIENCE — WHERE BRANDS & COMMUNITIES COME TOGETHER More than real estate, we are a company of experiences. For our guests, we provide distinctive shopping, dining and entertainment. For our retailers, we offer the unique opportunity to thrive in the best retail real estate in the best markets. From new projects and redevelopments to acquisitions and mergers, we are continuously evaluating our portfolio to enhance the Simon experience - places where people choose to shop and retailers want to be. We deliver: SCALE Largest global owner of retail real estate including Malls, Simon Premium Outlets® and The Mills® QUALITY Iconic, irreplaceable properties in great locations INVESTMENT Active portfolio management increases productivity and returns GROWTH Core business and strategic acquisitions drive performance EXPERIENCE Decades of expertise in development, ownership, and management That’s the advantage of leasing with Simon. PROPERTY OVERVIEW LEESBURG CORNER PREMIUM OUTLETS® LEESBURG, VA LEESBURG CORNER PREMIUM OUTLETS LEESBURG, VA 15 7 Leesburg For t E MAJOR METROPOLITAN AREAS SELECT TENANTS vans Gaithersburg Rd. White's 107 15 Ferry (Bypass) Tysons Corner: 23 miles Saks Fifth Avenue OFF 5TH, adidas, Ann Taylor Factory Store, Armani D u S 15 y 270 l c Frederick Exit 1B l Take 2nd right es o l Exit 15N l G i 28 n r Washington, D.C.: 35 miles Outlet, Banana Republic Factory Store, Barneys New York Warehouse, ee R 7 n d . Leesburg w Rockville 95 ayr Baltimore, MD: 75 miles Brooks Brothers Factory Store, Burberry, Calvin Klein Company Store, Baltimore Pot om acR Coach Factory Outlet, DKNY Company Store, Elie Tahari Outlet, HUGO D iver u ll es BOSS Factory Store, J.Crew Factory, Jones New York, kate spade new G RETAIL r ee york, LACOSTE Outlet, Michael Kors Outlet, Nautica, NikeFactoryStore, nw ay 7 GLA (sq. -

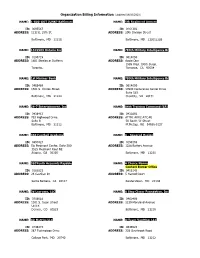

Organization Billing Information (Updated 08/03/2020)

Organization Billing Information (Updated 08/03/2020) NAME: 1-800-GOT JUNK? Baltimore NAME: 5th Regiment Armory ID: 0695567 ID: 0161302 ADDRESS: 1212 E. 25th St. ADDRESS: 29th Division Street Baltimore, MD 21218 Baltimore, MD 212012288 NAME: 1315903 Ontario Inc NAME: 780th Military Intelligence Br ID: 0196719 ID: 0614050 ADDRESS: 1881 Steeles at Dufferin ADDRESS: Apple One 1999 West 190th Street Toronto, Torrance, CA 90504 NAME: 1st Mariner Bank NAME: 780th Military Intelligence Br ID: 0468469 ID: 0614050 ADDRESS: 1501 S. Clinton Street ADDRESS: 14900 Conference Center Drive Suite 525 Baltimore, MD 21224 Chantilly, VA 20151 NAME: 24-7 Entertainment, Inc NAME: 84th Training Command (LR) ID: 0438413 ID: 0432892 ADDRESS: 703 Highwood Drive ADDRESS: ATTN: ARRC-ATC-PE Suite B 50 South 'O' Street Baltimore, MD 21212 Ft.McCoy, WI 54656-5137 NAME: 360 Football Academy NAME: A - Squared Design ID: 0497427 ID: 0199169 ADDRESS: Six Piedmont Center, Suite 500 ADDRESS: 1228 Battery Avenue 3525 Piedmont Roat NE Atlanta, GA 30305 Baltimore, MD 21230 NAME: 360Youth Accounts Payable NAME: A Choice Nanny Contact Bursar Office ID: 0182831 ID: 0418143 ADDRESS: 26 Castilian Dr ADDRESS: 5 Harrod Court Santa Barbara, CA 93117 Reisterstown, MD 21136 NAME: 3d Lacrosse, LLC NAME: A Step Closer Foundation, Inc ID: 0708088 ID: 0460409 ADDRESS: 1301 S. Jason Street ADDRESS: 2219 Maryland Avenue Unit K Denver, CO 80223 Baltimore, MD 21218 NAME: 4D Metrics LLC NAME: A-Team Vaulting, LLC ID: 0746473 ID: 0646523 ADDRESS: 387 Technology Drive ADDRESS: 328 Overbrook Road College Park, MD 20740 Baltimore, MD 21212 Organization Billing Information (Updated 08/03/2020) NAME: A.C.