China's Cosmetics Market

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Annual Report 2002

ANNUAL REPORT 2002 Founded nearly a century ago by the chemist Eugène Schueller, L’Oréal has consistently applied its policy of investing in research, ensuring that its products meet the highest possible standards of quality, safety and innovation. Today, the group contributes to the beauty of women and men all over the world, providing everyday solutions that enhance their sense of well-being. CONTENTS 01 Board of Directors 02 Chairman’s message 06 Management Committee 08 Financial highlights L’Oréal over ten years 12 Brands 14 Research and Development 18 Production and Technology 20 Human Resources 22 Sustainable Development 24 COSMETICS 26 Professional Products 32 Consumer Products 40 Luxury Products 48 Active Cosmetics 52 DERMATOLOGY AND NUTRICOSMETICS 54 PHARMACEUTICALS The L’Oréal Annual Report comprises three separate 56 CORPORATE GOVERNANCE documents: 1 a general brochure; 2 the consolidated financial statements 58 Stock exchange and shareholders available on Thursday 3rd April 2003; 3 the Management Report of the Board of Directors, the L’Oréal parent company financial statements plus additional information for the Reference Document as required by law, available two weeks prior to the Annual General Meeting convened for Thursday 22nd May 2003. L’Oréal Annual Report 2002 BOARD OF DIRECTORS BOARD OF DIRECTORS Lindsay Owen-Jones CBE Chairman and Chief Executive Officer Jean-Pierre Meyers Rainer E. Gut Vice-Chairman Xavier Fontanet Liliane Bettencourt Director since 29th May 2002 Françoise Bettencourt Meyers Marc Ladreit de Lacharrière Peter Brabeck–Letmathe Olivier Lecerf Franck Riboud Francisco Castañer Basco Director since 29th May 2002 François Dalle Edouard de Royère Jean-Louis Dumas Michel Somnolet Director since 29th May 2002 Director up to 31st December 2002 Auditors The presentation of the directors is on page 57. -

Monthly Disclosure of Trading in Own Shares Carried out in March 2016

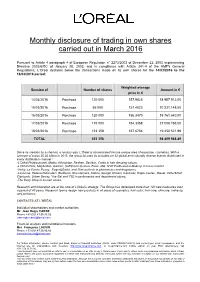

Monthly disclosure of trading in own shares carried out in March 2016 Pursuant to Article 4 paragraph 4 of European Regulation n° 2273/2003 of December 22, 2003 implementing Directive 2003/6/EC of January 28, 2003, and in compliance with Article 241-4 of the AMF's General Regulations, L’Oreal declares below the transactions made on its own shares for the 14/03/2016 to the 18/03/2016 period: Weighted average Session of Number of shares Amount in € price in € 14/03/2016 Purchase 120 000 157,9826 18 957 912,00 15/03/2016 Purchase 65 000 157,4023 10 231 149,50 16/03/2016 Purchase 120 000 156,3470 18 761 640,00 17/03/2016 Purchase 175 000 154,3358 27 008 765,00 18/03/2016 Purchase 123 358 157,6754 19 450 521,99 TOTAL 603 358 94 409 988.49 Since its creation by a chemist, a century ago, L’Oréal is concentrated on one unique area of expertise, cosmetics. With a turnover of euros 25.26 billion in 2015, the group focuses its activities on 32 global and culturally diverse brands distributed in every distribution channel : -L’Oréal Professionnel, Matrix, Kérastase, Redken, Decléor, Carita in hair dressing salons. -L’Oréal Paris, Maybelline, Garnier, SoftSheen·Carson, Essie, MG, NYX Professional Makeup in mass market. -Vichy, La Roche Posay, Roger&Gallet, and Skinceuticals in pharmacies and drugstores. -Lancôme, Helena Rubinstein, Biotherm, Shu Uemura, Kiehl’s, Giorgio Armani, Cacharel, Ralph Lauren, Diesel, Viktor&Rolf, Clarisonic, Urban Decay, Yue-Sai and YSL in perfumeries and department stores, -The Body Shop in its own stores. -

Chief Executive Agendas

the insider’s beauty bible A FAIRCHILD PUBLICATION Leaders Outline Plans for Changing Times Shiseido’s Shinzo Maeda Victoria’s Secret’s Christine Beauchamp N.V. Perricone’s Shashi Batra Jurlique’s Eli Halliwell Frédéric Fekkai’s Melisse Shaban PLUS Fall Fragrances CHIEF Edible Beauty Second Life EXECUTIVE AGENDAS L’Oréal’s Jean-Paul Agon Plots a New Course for Growth Contents DEPARTMENTS 16 People, Places & Lipsticks Inside-out beauty, the lighting guru and an unsual take on the manicure. 20 What’s In Store Beach-ready essentials, artistic cosmetics and relief for stressed-out strands. 26 A Closer Look: Fragrance The comeback of classic flowers, not to mention the return of more celebrity scents. 52 The It List: Beauty Still Life Photographers When these artists get behind the camera, the results are more than just a pretty picture. They’re money-making masterpieces. 58 Last Call: Second (Life) Coming In our tech-savvy times, more beauty brands are embracing the undeniable tug of marketing products in a virtual world. FEATURES 30 Agon In Command L’Oréal’s ceo sets the stage for a new era at the French beauty company. And the analysts weigh in. 38 Beauty CEO Pop Quiz What’s on William Lauder’s reading list? And how does Maureen Chiquet keep her cool? Beauty’s top brass reveal all. 40 Young & Royally Talented Say hello to four emerging beauty bosses who are taking the industry into new territory. Shiseido’s Heidi Manheimer and Carsten Fischer flank ceo Shinzo Maeda, whose sweeping changes will soon be felt 44 Quiet Giant beyond Japan’s borders. -

Color Theory and Cosmetics Emma E

Central Washington University ScholarWorks@CWU Undergraduate Honors Theses Student Scholarship and Creative Works Spring 2016 Color Theory and Cosmetics Emma E. Mahr Central Washington University, [email protected] Follow this and additional works at: http://digitalcommons.cwu.edu/undergrad_hontheses Part of the Photography Commons Recommended Citation Mahr, Emma E., "Color Theory and Cosmetics" (2016). Undergraduate Honors Theses. Paper 6. This Thesis is brought to you for free and open access by the Student Scholarship and Creative Works at ScholarWorks@CWU. It has been accepted for inclusion in Undergraduate Honors Theses by an authorized administrator of ScholarWorks@CWU. Color Theory and Cosmetics Emma Mahr Senior Thesis Submitted in Partial Fulfillment of the Requirements for Graduation Arts & Humanities Honors Program William O. Douglas Honors College Central Washington University May 2016 Accepted by: ___________________________________________________________ __________ Andrea Eklund, Associate Professor, Family & Consumer Sciences Dept. Date _________________________________________________________ __________ Katherine Boswell, Lecturer, English Department Date 2 Table of Contents Abstract 3 Introduction 4 Background 5 A Brief History of Modern Cosmetics 5 Terms Defined 8 Methods 9 Models 9 Consultations 10 Products 11 Sanitation 13 Process 13 Look One 14 Look Two 14 Look Three 15 Individualized Looks 16 Analysis 17 Look One 17 Look Two 18 Look Three 19 Individualized Looks 20 Reflection 21 References 23 Appendix Consent Forms 25 Face Templates 28 Photographs 35 3 Abstract In this research project, I attempted to discover what difference does color make on the perception of the face. I examined the effects of cosmetics on the appearance of the face using color theory. Three models were used for this project. -

L'oréal Returns to Growth

Clichy, 22 October 2020 at 6.00 p.m. SALES AT 30 SEPTEMBER 2020 L’ORÉAL RETURNS TO GROWTH Sales: 20.11 billion euros 1 o -7,4% like-for-like o -6,9% at constant exchange rates o -8,6% based on reported figures Growth in the third quarter: +1.6% like-for-like 1 Exceptional growth of the Active Cosmetics Division: +15.2% like-for-like 1 Power and growth in e-commerce 2: 23.7% of sales, +61.6% 1 Strong growth in mainland China: +20.8% like-for-like 1 Commenting on the figures, Mr Jean-Paul Agon, Chairman and Chief Executive Officer of L'Oréal, said: “In the context of the ongoing epidemic crisis, L’Oréal’s absolute priority continues to be to protect the health of all its employees worldwide. The Group was able to return to growth as soon as this third quarter thanks to the determination and the relevance of the strategic choices taken in all Divisions and geographic Zones. After a first half marked by a crisis of supply, linked to the closure of points of sale around the world, L’Oréal put everything in place, as early as June, to stimulate demand for its brands and products and to re-engage all its business drivers. All of the launches initially planned went ahead, business drivers and media investments were strengthened, and “Back to Beauty” plans were deployed with our distribution partners everywhere, in brick-and-mortar and e-commerce, to stimulate the return to consumption. This return to growth is evidence of consumers’ robust appetite for beauty products and our innovations. -

Hello & Goodbye

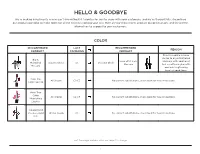

HELLO & GOODBYE We’re making investments in new can’t-live-without-it favorites for you to share with your customers, and we’ve thoughtfully streamlined our product portfolio to make room for all the newness coming your way. Here are our most recent product discontinuations and the perfect alternatives to suggest to your customers. COLOR DISCONTINUED LAST RECOMMENDED REASON PRODUCT CAMPAIGN PRODUCT Gives incredible volume, similar to Big & Multiplied Big & Love at 1st Lash Mascara, with additional Multiplied Blackest Black C5 Blackest Black Mascara lash conditioning benefits Mascara and lash lengthening heart-shaped fibers Avon True All Shades C2-C5 No current substitutions, check back for new innovations Color Lipstick Avon True Color All Shades C2-C5 No current substitutions, check back for new innovations Nourishing Lipstick Superextend Precise Liquid Brown Suede C5 No current substitutions, check back for new innovations Pen Last Campaign available dates are subject to change. 1 COLOR DISCONTINUED LAST RECOMMENDED REASON PRODUCT CAMPAIGN PRODUCT N20 Neutral Light The Face Shop Ink Lasting W20 Ivory C6 No current substitutions, check back for new innovations Foundation Slim Fit N70 Deep Living Coral The Face Shop Pure Red Ink Serum C5 No current substitutions, check back for new innovations Lip Tint Hug Red Tempting Pink The Face Shop Rogue All Shades C5 No current substitutions, check back for new innovations Satin Moisture Lipstick The Face Shop Rogue Powder All Shades C5 No current substitutions, check back for new innovations Matte Lipstick The Face Shop Flat Velvet Pink Moment C7 No current substitutions, check back for new innovations Lipstick Last Campaign available dates are subject to change. -

Deloitte Global Powers of Luxury Goods 2018

Global Powers of Luxury Goods 2018 Shaping the future of the luxury industry Contents Foreword 3 Top 100 quick statistics 4 Shaping the future of the luxury industry 5 Global Economic Outlook 9 Top 100 highlights 13 Global Powers of Luxury Goods Top 100 15 Top 10 highlights 23 Fastest 20 27 Product sector analysis 29 Geographic analysis 37 Newcomers 45 Study methodology and data sources 47 Endnotes 50 Contacts 51 Luxury goods in this report focuses on luxury for personal use, and is the aggregation of designer clothing and footwear (ready-to-wear), luxury bags and accessories (including eyewear), luxury jewellery and watches and premium cosmetics and fragrances. Foreword Welcome to the fifthGlobal Powers of Luxury Goods. The report examines and lists the 100 largest luxury goods companies globally, based on the consolidated sales of luxury goods in FY2016 (which we define as financial years ending within the 12 months to 30 June 2017). It also discusses the key trends shaping the luxury market and provides a global economic outlook. The world’s 100 largest luxury goods companies generated personal luxury goods sales of US$217 billion in FY2016. At constant currency, the growth rate was 1 per cent, 5.8 percentage points lower than the 6.8 per cent currency-adjusted growth achieved by these companies in the previous year. The average luxury goods annual sales for a Top 100 company is now US$2.2 billion. The luxury market has bounced back from economic uncertainty and geopolitical crises, edging closer to annual sales of US $1 trillion at the end of 2017. -

2021 Q3 Report Combined

MEGA GUIDE: CHINA E-COMMERCE AND DIGITAL MARKETING Q3 2021 2021 Q3 E : [email protected] W : www.chozan.co W : www.alarice.com.hk 2 HELLO! In Q3 of 2021 China’s digital space was retransformed by new regulations, rules and consumers demands. While China’s major economic indicators keep showing positive growth, Covid-19 caused shifts in consumers behaviour towards which companies need to keep close attention to. In this report ChoZan team monitor latest insights in Q3 of 2021 to help companies identify new opportunities and act on it. You’ll also find opinion of over 50 China experts about China’s economy, modern Chinese consumers, e-commerce, social media and New Retail. A big thanks to all of them. Let's go get them! Ashley Galina Dudarenok Founder, Alarice and ChoZan, LinkedIn Top Voice Follow my LinkedIn for daily China insights Sign up to my bi-weekly China Digest https://chozan.co/ https://alarice.com.hk/ https://ashleydudarenok.com/ E : [email protected] W : www.chozan.co W : www.alarice.com.hk 3 CONTENTS 1. OVERVIEW 05 5. NEW CONSUMPTION 237 Weibo 412 China's Digital Economy 06 Douyin 421 Overview of Digital China 35 5. KEY CONSUMPTION ECONOMIES 251 RED 440 Bilibili 464 2. KEY CHINA TRENDS 53 6. E-COMMERCE 272 Zhihu 483 Overview 273 Kuaishou 508 3. CONSUMER INSIGHTS 62 Alibaba 294 Weitao 528 China’s Consumers Overview 63 JD.com 306 Toutiao 539 Millennials 70 Pinduoduo 311 Baidu 563 Gen Z 78 Kuaishou 320 The Silver-haired Generation 97 9. Q2 MARKETING CALENDAR 578 Chinese Men 117 7. -

DEEP DIVE: Have Had a Growing Influence on the Global Beauty Market in Recent Years, Leading to a K-Beauty Trend

NOVEMBER 16, 2016 Korean beauty brands have seen strong growth in sales volume, with eXports reaching US$2.45 billion in 2015. Korean brands DEEP DIVE: have had a growing influence on the global beauty market in recent years, leading to a K-Beauty trend. Korean In this report, we eXamine the factors that underpin the successful ascent of Korean beauty, with a focus on the product, process and technology innovations they have brought Innovation to the market. Here are our key takeaways. 1) Korean beauty brands have adopted a “fast fashion” product development cycle and gained recognition for in Beauty innovative formulas, ingredients, manufacturing processes and packaging. However, the sophisticated and demanding customers in the local Korean market have also been one of the major drivers. 2) Korean beauty brands have embraced the digital transformation age and have taken advantage of the cultural influence of the Korean wave to come up with innovative marketing strategies that have driven growth. 3) Korean beauty brands were also fast to adopt in-store technologies, some of which are on par with other technology developed by international beauty brands, while others are ahead of the international market. DEBORAH WEINSWIG 4) A number of Korean beauty startups have emerged that Managing Director, Fung Global Retail & Technology have brought Korean beauty products overseas with e- [email protected] commerce, or created innovative beauty products with US: 646 .839.7017 HK: 852.6119.1779 the latest technologies. CN: 86.186.1420.3016 DEBORAH WEINSWIG, MANAGING DIRECTOR, FUNG GLOBAL RETAIL & TECHNOLOGY 1 [email protected] US: 917.655.6790 HK: 852.6119.1779 CN: 86.186.1420.3016 Copyright © 2016 The Fung Group. -

Global Mba with Major in Luxury Brand Management

GLOBAL MBA WITH MAJOR IN LUXURY BRAND MANAGEMENT CV BOOK 2021 26TH ANNIVERSARY YEAR INTERNATIONAL RANKINGS BUSINESS #6 #3 #4 #5 EDUCATION 2020 European Master in Master in Executive Business School Management Finance Education Programs ESSEC BUSINESS SCHOOL Key fi gures ESSEC is a business school with ESSEC is a school with French Roots programs ranging from Bachelor that trains responsible leaders. to PhD, a wide range of Masters Being a responsible leader means programs including our fl agship Master being able to see beyond business in Management and Global MBA as usual. Responsible leaders are programs. ESSEC also o ers executive able to value long-term benefi ts education and custom training over short-term profi ts; they are able 62,OOO 7,O5O designed and developed on-demand to blend corporate performance graduates worldwide students in full-time undergraduate for our partners from the private with employees’ well-being. To and graduate programs sector. ESSEC holds the “Triple crown” prepare its students for the world of of accreditations for global business tomorrow, ESSEC’s pedagogy seeks education: EQUIS, AACSB and AMBA. to awaken and develop creative and critical thinking, together with 4 +1 39% +1oo Vincenzo Vinzi At the core of the ESSEC learning the learning-by-doing method. campuses in augmented international nationalities Dean and President experience is a combination of Responsible leaders are those who Cergy, Paris-La Défense, digital students represented of ESSEC Business School excellence and distinctiveness. can see the broader picture. Singapore and Rabat campus ESSEC’s unique educational model is based on education by experiences, ESSEC is a full ecosystem at the that foster the acquisition of crossroad of rigorous and relevant partner universities +1oo76 CREATED IN 19O7, ESSEC cutting-edge knowledge with the research, innovation, business and in 42 countries development of know-how and life society. -

Bonjour Cosmetic and Beauty Cashback Rates

Bonjour Cosmetic and Beauty Cashback Rates Brand Rate Brand Rate Brand Rate Brand Rate 4711 Standard Amie Standard B&B Standard Beauty Quick Standard 17茶 Standard Amilok Standard Baby Face Standard Beauty Republic Standard Chicks Standard Andrea Standard Baby Foot Standard Beauty Synergy Standard ~H2O+ Standard Angry Bird Standard Baby Mopiko Standard BeautyMate Standard 2B Alternative Standard Anna Sui Standard Baby-Mo Standard BeauuGreen Standard 3 Concept Eyes Standard Annie's Way Standard Bad Air Sponge Standard BeBe Standard 3M Standard Ans Standard Baille Standard Beijing Tong Ren Tang Standard 3W CLINIC Standard Apieu Standard Banana Boat Standard Beinisesi Standard 4+4 Standard APL Standard Banana Republic Standard Belif Standard A By Bom Standard Apother Standard Bandai Standard Bench Bamboo Standard A.S.P Standard April Skin Standard Bandi Standard Benefit Standard AB Standard Aquolina Standard Banila Co Standard Benetton Standard Actress Standard Aramis Standard Bao Shu Tang Standard Benico Standard Adidas Standard Ardell Standard Barbie Standard Berrisom Standard Adin Standard Armand Basi Standard Barbie Standard Bettina Barty Standard ADJUSTE Standard Aroma Field Standard Barielle Standard Beyond Standard Admiring Standard Asahi Standard Batise Standard Bigen Standard Affinity Bay Standard Asana Wellness Standard Batiste Standard Bihada Standard Ag Standard askin Dr. Standard Baviphat Standard Bio Standard AHC Standard ASTY Standard Bawang Standard Bio Oil Standard Aigner Standard Asunaro Standard Bayer Standard Bio28 Standard -

China Consumer Market

China Consumer Market February 2019 Contents Summary ................................................................................................... 1 Objective .................................................................................................................... 1 Figures, Graphics and Indicators ............................................................ 2 Consumer Trends ..................................................................................... 4 Consumption Characteristics of the New Generation ........................................... 4 Consumer Segments ................................................................................................ 6 Market Trends ........................................................................................... 7 Future Prospects ...................................................................................................... 7 Changes of Attitude to Brand Origin ....................................................................... 9 Marketing Trends .................................................................................... 10 Mobile Usage ........................................................................................................... 10 Major Sales and Promotion Seasons .................................................................... 12 Key Consumer Product Sectors ............................................................ 14 Contents Baby Products ........................................................................................................