Assessing the Competitive Implications of Partial Ownership General Economic Framework and Its Application to the Bskyb/ITV Case

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Albuquerque Citizen, 04-12-1909 Hughes & Mccreight

University of New Mexico UNM Digital Repository Albuquerque Citizen, 1891-1906 New Mexico Historical Newspapers 4-12-1909 Albuquerque Citizen, 04-12-1909 Hughes & McCreight Follow this and additional works at: https://digitalrepository.unm.edu/abq_citizen_news Recommended Citation Hughes & McCreight. "Albuquerque Citizen, 04-12-1909." (1909). https://digitalrepository.unm.edu/abq_citizen_news/3047 This Newspaper is brought to you for free and open access by the New Mexico Historical Newspapers at UNM Digital Repository. It has been accepted for inclusion in Albuquerque Citizen, 1891-1906 by an authorized administrator of UNM Digital Repository. For more information, please contact [email protected]. TRAIiN ARRIVA S A TT WtAIHER FORECAST No. I 7.45 P. V No. 7 10.55 p. m t- - X1VIUBUQUERQUE CITIZEN Denver. Colo., April fair No. 8 6.40 p might and TaesJa. Colder south portion No. 9 1 1.45 p. 1-- WE GETT THE NEWS FIRST tonight. VOLUME 24. ALBUQUERQUE. NEW MEXICO. MONDAY. Al'ltIL 112. 1939. NUMIiEK 77 V WATERS-PIER- CONGRESS HAS STOPPED HOW ONE DAY'S VOTING ALllCH SAYS TARIFF RICH WIDOW, SLATED FOR CE CO. 10 NEXT PRbSIDENT OF D. A. R. THE DEEP WATERWAY CHANGED MAP OF MICHIGAN DUTIES Will BE PAY HEAVY FINE PROJECTS ORJIf Whole Work Will Walt Until Senate Finance. Committee Supreme Court Denies Ap- Commission Investigates Has Charge of Payne Bill plication for Re-Heari- and Makes Ke. Which Passed the In the Texas port. House. Cast?. M MWtM lAftW--J jj ARMY ENGINEERS jj j THE DECREASES ATTORNEYS CLAIM OUTNUMBER ADVANCES IT WILL ALSO HELP ISJONFISCATION. v :C g Lumber Duty Will Problem of Convt-rtln- Rivers and be Retained as Supreme Court Upholds Texas x v Lakes Into Transportation Passed by House. -

New News, Future News the Challenges for Television News After Digital Switch-Over

New News, Future News The challenges for television news after Digital Switch-over An Ofcom discussion document Publication date: 26 June 2007 Foreword The prospects for television news in a fully digital era are a central element in any consideration of the future of public service broadcasting (PSB). News is regarded by viewers as the most important of all the PSB genres, and television remains by far the most used source of news for UK citizens. The role of news and information as part of the democratic process is long established, and its status is specifically underpinned in the Communications Act 2003. This report, New News, Future News, is one of a series of Ofcom studies focussing on individual topics identified in the PSB Review of 2004/05, and further discussed in the Digital PSB report of July 2006. The others are on the provision of children’s programmes and on the prospects for a Public Service Publisher. All three studies are linked to areas of particular PSB concern for the future, and set out a framework for policy consideration ahead of the next full PSB review. Other Ofcom work of relevance includes the review of Channel 4’s funding. It has not been the role of this report to come up with solutions, and no policy recommendations are put forward. Instead, the report examines the environment in which television news currently operates, and assesses how that may change in future (after digital switch-over and, in 2014, the expiry of current Channel 3 and Channel 5 licences) . It identifies particular issues that will need to be addressed and suggests some specific questions that may need to be answered. -

(Public Pack)Agenda Document for Planning Applications Committee

PLANNING APPLICATIONS COMMITTEE Date: Tuesday 9 February 2016 Time: 7.00 pm Venue: Main Hall - Karibu Education Centre, 7 Gresham Road, SW9 7PH Copies of agendas, reports, minutes and other attachments for the Council’s meetings are available on the Lambeth website. www.lambeth.gov.uk/moderngov Members of the Committee Councillor Malcolm Clark, Councillor Bernard Gentry, Councillor Diana Morris (Deputy Chair), Councillor Sally Prentice, Councillor Mohammed Seedat, Councillor Joanne Simpson and Councillor Clair Wilcox (Chair) Substitute Members Councillor Liz Atkins, Councillor Anna Birley, Councillor Jennifer Brathwaite, Councillor Tim Briggs, Councillor Marcia Cameron, Councillor Jane Edbrooke, Councillor Nigel Haselden, Councillor Robert Hill, Councillor Jack Hopkins, Councillor Louise Nathanson, Councillor Jane Pickard and Councillor Sonia Winifred Further Information If you require any further information or have any queries please contact: Henry Langford, Telephone: 020 7926 1065; Email: [email protected] Members of the public are welcome to attend this meeting. If you have any specific needs please contact Facilities Management (020 7926 1010) in advance. Queries on reports Please contact report authors prior to the meeting if you have questions on the reports or wish to inspect the background documents used. The contact details of the report author are shown on the front page of each report. @LBLdemocracy on Twitter http://twitter.com/LBLdemocracy or use #Lambeth Lambeth Council – Democracy Live on Facebook http://www.facebook.com/ Digital engagement We encourage people to use Social Media and we normally tweet from most Council meetings. To get involved you can tweet us @LBLDemocracy. Audio/Visual Recording of meetings Everyone is welcome to record meetings of the Council and its Committees using whatever, non- disruptive, methods you think are suitable. -

I Itfirap Privileges

: \ - TBIBB m ir ASSOCIATEDm-mESS-mw8PAPEBBB IN TWIN F A L tS COI!OUNTT _________ THI T O FALLS i L Y N l UKMriKK A iiniT nt;nRAtJ IO C [,KAHK[> WlUR MEMREIl 01 VOL. 8. NO. 139. OK cinct;i.ATiONa TWIN FALLS, IDAHO,O^THUESDAY ' MORNINCNG, SEPTEMBER 24, 192,5,U h . ^ a M A T BP..m M . Times ^u are Scenc NO PEACE MOVE YET MADE DEATH CAUSE UNDECIDEDJE D Beer Runners Before of Liquor -Raid _in,;in ,; . .. i*Ai ra, -.so(.(. a-1, • i ’llU w nO , S.-p(. 2.1 eor. Federal Grand Jury DECISiWl k e n ^ e n rh ................. bni.lereiv..,| “nii HHillD" oner*, jury tndar wna unnblo (n • ■ Which 10 are Taker ,1“l,‘H,ii»o Iho rxafl niannrr in]; to Tell of LibertiestJIHleE: . IM-UOO |iro|m.i,|,. fr».ni Ab-l-rl-Kriin, whirh lllllll l-Vhn ••Hilvpr Dollnr” Tederal Prohibition AgontiOntS iM'l-'r of Ihl' Itiffinii' rebrl, In Mor- Tctry Dtnjgati nnd FunWo . Swoop Down on Hearti o f ‘^ ‘■0. i' offn'ially •lalo.l Indnv. D ■ Tabot, lUMKlitfv.uf tln.'lnti’ WonalMIiit Lttko Qucotlonod as to Why • •Tnbor of (\,Inr,i,|„, pi,me In hrr M m iis Theatrical'District. Tlio (!<lVcTnitu-nl |.-:i lv I....... Irr-I iTFirap Privileges. tain any I.M„;,ri.|,- nn.vo In.vnrd .lonlh in hrr a|'arin,ont ............md... e P iE W - _ rral ,lny, Kh.- wij, fo.... 1 Sp . ' ,-n, ... , ‘,‘r file Aaaoclaled rreai) 11 1 ----------~-nI.|o.|-it.-ilo:ith-n;irt-thr-jnrT-itr-- NKW YOIIK. -

An Introductory History of British Broadcasting

An Introductory History of British Broadcasting ‘. a timely and provocative combination of historical narrative and social analysis. Crisell’s book provides an important historical and analytical introduc- tion to a subject which has long needed an overview of this kind.’ Sian Nicholas, Historical Journal of Film, Radio and Television ‘Absolutely excellent for an overview of British broadcasting history: detailed, systematic and written in an engaging style.’ Stephen Gordon, Sandwell College An Introductory History of British Broadcasting is a concise and accessible history of British radio and television. It begins with the birth of radio at the beginning of the twentieth century and discusses key moments in media history, from the first wireless broadcast in 1920 through to recent developments in digital broadcasting and the internet. Distinguishing broadcasting from other kinds of mass media, and evaluating the way in which audiences have experienced the medium, Andrew Crisell considers the nature and evolution of broadcasting, the growth of broadcasting institutions and the relation of broadcasting to a wider political and social context. This fully updated and expanded second edition includes: ■ The latest developments in digital broadcasting and the internet ■ Broadcasting in a multimedia era and its prospects for the future ■ The concept of public service broadcasting and its changing role in an era of interactivity, multiple channels and pay per view ■ An evaluation of recent political pressures on the BBC and ITV duopoly ■ A timeline of key broadcasting events and annotated advice on further reading Andrew Crisell is Professor of Broadcasting Studies at the University of Sunderland. He is the author of Understanding Radio, also published by Routledge. -

Garden Bridge Conditions Report, Item 3. PDF 4 MB

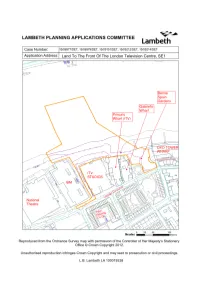

IBM ITV Address: Land To The Front Of The London Television Centre, Queen's Walk And Potential Construction Access Routes From Upper Ground London, SE1 Application Numbers: 15/05151/DET; Case Officers: Richard McFerran and 15/05212/DET; 15/05214/DET; 15/06977/DET; Dale Jones 15/06979/DET Ward: Bishops Dates Validated: 11th September 2015 (Conditions 24, 25 and 29) and 4th December 2015 (Conditions 21 and 23) Proposal: Approval of details pursuant to Condition 21 (Detailed Design of South Landing Building) 15/06977/DET Condition 23 (Internal Layout of South Landing Building) 15/06979/DET Condition 24 (Delivery and Servicing Plan) 15/05151/DET Condition 25 (Waste Management Plan) 15/05212/DET Condition 29 (Coach and Taxi Management Plan) 15/05214/DET of planning permission 14/02792/FUL (Erection of a pedestrian bridge with incorporated garden, extending for a length of 366m over the River Thames from land adjacent to The Queens Walk on South Bank (in the London Borough of Lambeth) to land above and in the vicinity of Temple London Underground Station on the north bank, the structure of the bridge having a maximum height of 14.3m above Mean High Water and a maximum width of 30m; the development also comprising the erection of 2 new piers in the River Thames; erection of a single-storey landing building (incorporating maintenance, management and welfare facilities and up to 410sqm A1, A3 and/or D1 floorspace with additional ancillary service and plant) on land adjacent to The Queens Walk, opposite the ITV building; associated public realm works; works to trees (including the removal of trees); associated construction work (including laying out of a construction access from Upper Ground) and works sites; and works within the River Thames (including temporary and permanent scour protection, relocation of moorings and erection of temporary structures) granted on 19.12.2014 (herein referred to as ‘the Garden Bridge’). -

Garage Owner Slain

L e a d e r Garage Owner Slain Two Men Enter Auto Sales Garage, And Shoot Frank PaofiDo, Proprietor, i In Gang Vengeance A brief, stacatto message was written into gangland's hi*- Th* new tax rate will be ***’* tory books last Friday night when ax revolver shots toppled fS.77 ** oompared witt1 $».29 Frank PaoliUo. 40, bloody and dead to the floor (4 h i s Lynd^ ol Ha hurst Auto Sales showroom at 50 Park Avenue. jjj ^ tjj.ij>Up ■ t** Today, Prosecutor John J. Breslin, Jr., was moving with all w w p lny wfll be given restor- *O j" possible swiftness to avert the opening of a new, terrorizing atlon oi 50 per cent ol their “ P™ the thirty-dvr K ang war. > '" ^1 " 1 SOtaftea. Seven men arc held in Bergen -— ■ ... Finance Officer Favier said the P . ounty Jail. Da CllfA YOU A rt Prosecutor Breelin'a promise ia “*'• w dal oondWona lor Lyndhurst and the extremely valuable assistance •*1 will put under arrest and un- Registered! ,!« hifh l«il U ) nnfSU r «v«n --------- of Hie refunding program." . niotcly coiinMWd with thi» affair. -far**.--------- Mayor Horace R. Bogle said: •vnrer County will k»v. no n u - t"0* 'Tn °* * * ? "The 1937-38 budget comes at a time when It should be ol ten la now la vreateat aid to Lyndhurst. Thi" leHvered Ma •s a time when recovery la mrt< Se fore he M L on the Saturday preceding Ike Ing Itself lelt. Confidence la ex election will be eatttM to -we'eel on every aide Lnvdhurs' 'ote. -

The Oxford Democrat

GOVERNED TOO MUCH.* ONE DOLLAR AND FIFTY CENTS IN ADVANCE. TERVS, TWO DOLLARS PER YEAR. "THE WORLD IS VOLUME NO. 28- NEW SERIES, VOL 'J. NO. IS. 1 'A I {IS, 31E. F1UI )AY, J UN E 4, 1858. OLD SERIES. 25, «• uii A t<T that, thinka I to •• cu*t IoU.uikI llm l.ii loll lite •t.iMurJ; "Now, Kim ih* Uliw CuhiiaUii. •horter,Ina beautiful, ami tin refol* thicker, Root M I SCH V. uijaalf, Crops Turnips LI,AN * turn •>i we •town!—" Capinn Jom-a, it four ami a pretty arr anj Uii« the uf tlio There ar» varieties of cul- Hereford Cattle.-How Etteem especially through region n»»nj turnip* 11 • In* lor or nam* thry II u».n, Mr. lUrkuin !" Ml Hint it'll *ou, iuj ain't rd where are Best vital «>r^ itta, lit) ln\»rt, lun^«, etc, in.it.<1 our farmer*, hul cipe- A SHIP 8 COMPANY. pinners' they Known upon t»jr general PACKET " I win'l in no manner of hur« Department «« Mini-Inn." \r», iuim, intt«<sl. We atAwrU the •uc ati<l actual uf wliicli rienc" ha* the to iwn kind* Th« extent of whm ll»<* ! power depend* given preference \Vi> Inl thffi it f irtni/'it on Iktard the for I knew "iriiB mi now." country rvdmj liia H« was iho rv. \ou mu»t MmfBiVr, hi tlm of tlio conatituti ii, tlio willt their »ul>-v«rietict—for »tiK*k Itaxti*—Wellington*. top* of lltrcf rd* ut lea* vitality ability let-ding mill k' t on our h >m from the and I knew h« {retail*, oiu>|>ria» |..n way leti'l'r< »t. -

Written Evidence Submitted by ITN

Written evidence submitted by ITN DCMS Committee inquiry into the impact of Covid-19 on DCMS sectors – June 2020 About ITN ITN is one of the world's leading news and multimedia content companies. We create, package and distribute news, entertainment, factual, sports, commercials and corporate content on multiple platforms to customers around the globe. We make the award-winning public service broadcast news programmes for ITV, Channel 4 and Channel 5, reaching around 10 million people every day and providing comprehensive and impartial news to the British public. ITN Productions, ITN’s independent production company, produces high quality creative content across four distinct business areas: television production, sports production, advertising and digital content. The immediate impact of Covid-19 on the sector Operational The impact of Covid-19 on ITN has varied by business area. Whilst some productions have been suspended including sports events, advertising, industry news and some television programmes, we have been able to find ways for other productions to continue under lockdown. Our news programmes for ITV, Channel 4 and Channel 5 as well as our current affairs programmes (including Jeremy Vine on Channel 5) form part of the broadcasters’ public service requirements and at this unprecedented and challenging time, ITN has had a critical role in providing the public with accurate, up to date information. As such, staff working on public service journalism were helpfully classified as key workers. As the country was put into lockdown, ITN played a vital role in getting across public health messages quickly, reliably and accurately. Whilst it was imperative that we allowed the messaging to be heard, we also analysed and interrogated the government strategy and position, asking difficult questions where necessary without compromising plurality across our services. -

The Speakers and Chairs 2017

WEDNESDAY 23 FESTIVAL AT A GLANCE THE SPEAKERS AND CHAIRS 2017 FROM 09:00 FROM 09:30 10:00-11:00 BREAK 11:45-12:45 BREAK 13:45-14:45 BREAK 15:30-16:30 BREAK 17:30-18:15 18:15-21:00 SB Artisan SA Incognito F Nothing will be 11:00-11:45 P Edinburgh 12:45-13:45 P Meet the 14:45-15:30 P Meet the 16:30-17:30 L The Free coaches to Shane Allen Hannah Chambers Evan Davis Mark Gordon Christian Howes Jarmo Lampela Charlotte Moore Dani Rayner Chris Shaw Jane Turton Tea and Coffee provide a musical Televised: Have Does...Blue Peter Controller: Jay Controller: Kevin T SA MacTaggart The Museum of T Ones to Watch T Break Out FS Aidan Farrell, SA Plus Break Out Aperol Thursday 09:30 - 10:30 Friday 11:30 - 12:30 Thursday 13:30 - 14:30 Wednesday 13:45 - 14:45 Wednesday 10:00 - 11:00 Friday 11:05 - 11:50 Thursday 09:30 - 10:30 Wednesday 10:45 - 11:45 Friday 13:00 - 14:00 09:00 - 11.00 welcome to the Young People Hunt, Channel 4 Lygo, ITV Lecture: Scotland depart Wednesday 10:00 - 11:00 Random Acts S Satire! What is it Session: Show Star Colourist Meet the Sky Session: Delivering Spritzers The Pentland The Sidlaw The Pentland The Sidlaw The Moorfoot/Kilsyth The Tinto The Pentland The Tinto The Fintry Sky Arts Zone Switched Off? Jon Snow from the EICC The Fintry CB Corney & Live Pitch Good For? me the Money! F Nick Bell, 14:40–17:00 Commissioners F Top Of The Pods: Diversity: From & Jazz with Friday 13:00 - 14:00 Thursday 13:30 - 14:30 Friday 13:00 - 14:00 09:30 10:45 - 11:45 Winning Audiences 14:45 - 15:30 90210 to E20 New Focus 18:15 until 19:00 Pinki Chambers -

ITV Plc Full Year Results for the Year Ended 31 Dec 2020

ITV plc Full year results for the year ended 31 Dec 2020 Carolyn McCall, Chief Executive, said: “Throughout this last year, we have all been dealing with the effects of the pandemic. As the UK’s largest commercial network, we’ve worked hard to fulfil our responsibility as a source of reliable and trusted news and to deliver some of the best entertainment into the country’s homes. “I’m proud of the work of all our colleagues and thank them for their dedication, creativity and hard work to successfully manage our way through the crisis while continuing to invest in our strategy. Our production teams were very innovative in restarting productions quickly and safely in the UK and internationally, while our commercial colleagues inspired advertisers to restart their marketing campaigns. “Good progress has been made in delivering our strategic priorities with the rollout of our programmatic addressable advertising platform, Planet V, to agencies to a very positive response; the acceleration of the transformation of the ITV Hub; BritBox UK is ahead of plan hitting half a million subscriptions in January 2021; and BritBox US increased its subscriptions by 50% over the year - we now have over 2.6m subscriptions globally across all our SVOD services. “While total revenues and profits were down our financial performance was ahead of expectations driven by a strong end to Q4 and our firm control over costs. “We are encouraged by the roadmap out of lockdown. We are seeing more positive trends in the advertising market in March and April and the majority of our programmes are now back in production. -

RACHAEL SHERLOCK 07581541185 [email protected]

RACHAEL SHERLOCK 07581541185 [email protected] I love working in a multi-camera studio environment where I am currently a Senior Studio Technician hoping to someday direct live events and extreme sporting competitions. My most recent role at ITV requires me to work with a team of multi-skilled technicians to provide quality support across four shows. Before joining ITV, I was shortlisted for Best Music Show twice at the National Student Television Awards and was part of the winning team for Best Broadcaster. SENIOR STUDIO TECHNICIAN January 2016 – PRESENT In this role I help manage a team that provides quality assistance to Sound, ITV Day Time Camera, Lighting and Scenic departments. My favorite tasks involve setting up radio mics and talk back for presenters and guests, as well as stepping up to operate ped cameras. SOUND EXPERIENCE June 2018 Floor Sound’s Assistant to a one-off special of Good Evening Britain, a live Good Evening Britain late-night version of the ITV breakfast show with Piers Morgan and Susanna Reid. CAMERA EXPERIENCE (INSIDE ITV) 2017 Ped operator for an interview with Alan Shearer, one of the Premier This Morning League's all-time top goal scorers. I also operate a ped during cooking and demo items. 2017 Camera 4 experience as the main presenter single. When not operating this Loose Women ped I operate the Green Room camera which becomes a 4 shot of presenters once back in the studio. 2017 Camera 6 operator which can also go hand held. Good for Green Room Lorraine shots, studio wides and group shots when there is a big chat.