Understanding High Street Performance

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

What's Next for Ukpound Shops?

February 3, 2015 February 3, 2015 What’s Next For UK Pound Shops? Major UK pound shop chains have seen revenues surge in the post-recession years. The economic slump and the Woolworths failure paved the way for this segment’s rapid expansion of stores. With further expansion expected, we think the segment is looking increasingly crowded. Some players are now eying international markets in their bid for growth. DEBORAH WEINSWIG Executive Director–Head Global Retail & Technology Fung Business Intelligence Centre [email protected] New york: 646.839.7017 Fung Business Intelligence Centre (FBIC) publication: UK POUND SHOPS 1 Copyright © 2015 The Fung Group, All rights reserved. February 3, 2015 What’s Next For UK Pound Shops? THE POUND SHOP BOOM Variety-store retailers have proliferated rapidly in the UK, mirroring the store-expansion boom of discount grocery chains (notably Aldi and Lidl), as the low-price, no-frills formula has found particular resonance in Britain’s era of sluggish economic growth. This retail segment encompasses chains like Poundland, 99p Stores and Poundworld, which sell all of their products at fixed price points. Similar to the dollar chains Dollar General and Family Dollar in the US, everything in the pound stores sells for £1 (or 99p) and the goods are bought cheaply in bulk. The group also includes chains with more flexible pricing schemes. Those include B&M Bargains, Home Bargains and Poundstretcher. For both types of stores, the offerings are heavy on beauty and personal care, household fast-moving consumer goods (FMCGs) and food and beverages (particularly confectionery). Other categories typically include do-it-yourself (DIY) and automotive accessories, pet products and seasonal goods. -

London Arches Brochure

13 A1-A4 Units To Let From 765 sq ft to 1,800 sq ft London Arches — Wood Lane Discover new character retail, restaurant and bar space in West London The White City Area is undergoing a transformation and as a part of this Transport for London are regenerating 31 railway Soho House arches to create a destination for eating, socialising, shopping and working. Over the next 10 years five major development projects will deliver 2.3m sq ft of retail, 2.2m sq ft of offices and 5,000 new homes to the area. The Wood Lane Arches are nestled right in the middle of this area, next to the new 230,000 sq ft full-line John Lewis and seconds away from Wood Lane tube station. Significant public realm improvements will provide pedestrianised access between Westfield London and White City Living by St James part of the Berkeley Group, as well as a Bluebird Cafe Bluebird better link from Stanhope & Mitsui Television Centre, Imperial College’s 23 acre campus and White City Place to Westfield London and Shepherd’s Bush. The Neighbourhood The Wood Lane Arches are located 150m from Wood Lane and White City Stations. The Arches are surrounded by some of London’s most exciting new developments making it the perfect spot for retailers, cafes, restaurants and bars looking to break the mould. Next to the site is a new John Lewis department store, part of the 750,000 sq ft Westfield extension that boasts a host of new flagship stores including Urban Revivo, H&M and Adidas, as well as a new restaurant and leisure offer centred around Westfield Square that includes All Star Lanes, Puttshack and Maple. -

November 2020 Prices Continue to Climb

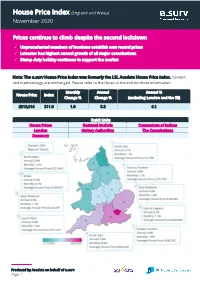

(England and Wales) House Price Index November 2020 Prices continue to climb despite the second lockdown ✓ Unprecedented numbers of locations establish new record prices ✓ Leicester has highest annual growth of all major conurbations ✓ Stamp duty holiday continues to support the market Note: The e.surv House Price Index was formerly the LSL Acadata House Price Index. Content and methodology are unchanged. Please refer to the Notes at the end for more information. Monthly Annual Annual % House Price Index Change % Change % (excluding London and the SE) £319,816 311.0 1.0 5.8 6.1 Quick Links House Prices Regional Analysis Comparison of Indices London Unitary Authorities The Conurbations Summary Produced by Acadata on behalf of e.surv Page 1 House Price Index (England and Wales) November 2020 Table 1. Average House Prices in England and Wales for the period November 2019 – November 2020 Link to source Excel Month Year House Price Index Monthly Change % Annual Change % November 2019 £302,368 294.3 0.4 1.5 December 2019 £302,886 294.6 0.2 1.5 January 2020 £304,088 295.7 0.4 1.7 February 2020 £306,012 297.6 0.6 1.9 March 2020 £305,457 297.1 -0.2 2.0 April 2020 £301,658 293.4 -1.2 1.0 May 2020 £298,672 290.5 -1.0 0.0 June 2020 £298,727 290.5 0.0 0.1 July 2020 £302,912 294.6 1.4 1.7 August 2020 £307,802 299.3 1.6 3.4 September 2020 £312,475 303.9 1.5 4.4 October 2020 £316,543 307.8 1.3 5.1 November 2020 £319,816 311.0 1.0 5.8 Note: The e.surv House Price Index provides the “average of all prices paid for domestic properties”, including those made with cash. -

Regeneration NI Creating 21St Century Town and City Centres

Regeneration NI Creating 21st Century Town and City Centres NEW THINKING FRESH LEADERSHIP AMBITIOUS INITIATIVES 1 The wholesale change needed to revitalise our town centres and give them a fighting chance of survival will only come, however, when there is an acceptance that the old order of things is crumbling before our eyes. We still rely on old models that are not fit for the 21st century and this is holding back change.” Grimsey Review, 2018 2 3 INTRODUCTION For nearly twenty years, Retail NI and its membership have been champions for our town centres and high streets, bringing forward new ideas and policy solutions to decision-makers at all levels of government. Our members are entrepreneurs who provide an important service to their local communities and believe in real and genuine partnerships with their local Councils. They champion strong, vibrant and diverse town centres, which are in themselves, centres of both retail and hospitality excellence. We have already successfully lobbied for the introduction of the Small Business Rate Relief Scheme, the Town Centre First Planning Policy, legislation for Business Improvement schemes, five hours for £1 off-street car parking discount and much more. The theme of this report is regeneration and how to create 21st century town and city centres. With the Local Government Elections in 2019, we believe it is time to update our policy priorities and introduce some new ideas. I look forward to engaging with members, stakeholders and political representatives across Northern Ireland in the months ahead, asking for their support to initiate the process of regenerating our high streets, regenerating our workforce, regenerating our infrastructure and regenerating our political structures. -

Chapter 11 Kensington High Street

Chapter 11 Kensington High Street building, Kensington Town Hall adjacent to the High Chapter 11 Kensington Street,as well as Sony and Warners and other High Street smaller offices. 11.1 Introduction 11.1.7 The centre has benefited from comprehensive public realm improvements, that 11.1.1 Kensington High Street has been one of have gained international acclaim. This has put in London’s top retail streets for the last 100 years. place high-quality, York-stone paving, created a The centre lost some of its original raison d’être as central reservation bike park and removed street the biggest concentration of department stores clutter, particularly guard railing. These outside Oxford Street with the closure of Pontings improvements have made crossing the street much and Derry and Tom’s in the early 1970s, and more easier, the pedestrian environment more recently Barker’s. In the seventies Derry and Tom’s comfortable and encouraged higher footfall on the became the home of the legendary Biba emporium northern side of the street (previously footfall was (once described as ‘the most beautiful store in the heavily concentrated on the southern side). world’), making Kensington High Street a fashion 11.1.8 Despite the public realm improvements, destination. With the closure of Biba in the mid people still perceive traffic congestion and the seventies, this role was continued by Hyper Hyper irregularity of the District and Circle Lines to be in the eighties and Kensington Market, which issues. High Street Kensington Station is a major survived until comparatively recently, and remains public transport interchange and the High Street is reflected today in the cluster of young fashion also served by a large number of buses. -

Westfield London

Westfield London Constructing Excellence 3 July 2013 Westfield Group The Westfield Group is an internally managed, vertically integrated, shopping centre group undertaking ownership, development, design, construction, funds/asset management, property management, leasing and marketing activities and employing approximately 4,000 staff worldwide. The Westfield Group has interests in and operates one of the world’s largest shopping centre portfolios with investment interests in 118 shopping centres across Australia, the United States, the United Kingdom, New Zealand and Brazil, encompassing approximately 24,300 retail outlets across 10.6m sq m (114m sq ft) of retail space and total assets under management of £42bn. Stratford City London Westfield is a long-term investor with investment interests in 100 shopping centres across Australia, the United States, New Zealand, Brazil and the United Kingdom In the UK, Westfield owns and manages a number of operational shopping centres including Westfield London, Stratford City and now Croydon San Francisco Bondi Junction Sydney City Introducing Westfield Overview / Key Facts • Aspiration : Best of the West End • 43 acres; Gross Area: 1.85m sqft (171,869 sqm) • Mixed Use: Retail, Offices, Leisure, Housing, Community Services • 3 miles from Marble Arch and 10 minutes on the underground • 25 minute drive from Heathrow airport • £1.7bn development • Over 300 retail, leisure and lifestyle stores; over 700 brands • Over 60 places to dine • All-digital 17 screen, all-digital, 3D state of the art cinema • Connectivity: 4 tube stations, 2 bus stations, overground train station • 4,500 car parking spaces • Premium Services • The Village: 40 Luxury Brands • 28m visits and close to £1bn in sales Agenda • Westfield’s overall challenge to understand and meet its users’ facilities needs. -

Anticipated Acquisition of 99P Stores Limited by Poundland Group Plc

Non-confidential ANTICIPATED ACQUISITION OF 99P STORES LIMITED BY POUNDLAND GROUP PLC RESPONSE TO PHASE II STATEMENT OF ISSUES 9 JULY 2015 LON37045457/6 163772-0005 POUNDLAND GROUP PLC Response to the CMA’s Statement of Issues This document is Poundland Group plc’s (Poundland) response to the UK Competition and Markets Authority’s (CMA) statement of issues of 25 June (Statement of Issues) regarding Poundland’s proposed acquisition of 99p Stores Ltd (99p Stores) (the Transaction). Please note that this document contains Poundland confidential information and should not be shared with third parties absent Poundland’s express prior written consent. 1. Executive Summary 1.1 Poundland welcomes the opportunity to provide the CMA with its input on the CMA’s Statement of Issues. 1.2 Poundland believes that the evidence strongly supports the view that this transaction does not pose any risk to competition. On the contrary, Poundland considers that the merger will be pro-competitive – bringing a superior proposition to 99p Stores’ customers, and further enhancing competition along the High Street. 1.3 In particular, the evidence shows that: (a) Poundland competes in a competitive marketplace everywhere it operates. Poundland competes all along the High Street: all of the products that Poundland sells are either available at a supermarket, at a limited assortment discounter (LAD), at another value general merchandiser (VGM), at a specialist retailer or at an independent discounter. Customers are value conscious – they want more for less, can easily switch retailers and do not display any ‘fascia loyalty’ in their quest for value. (b) There is no variation of the offer across the Poundland estate. -

LONDON Cushman & Wakefield Global Cities Retail Guide

LONDON Cushman & Wakefield Global Cities Retail Guide Cushman & Wakefield | London | 2019 0 For decades London has led the way in terms of innovation, fashion and retail trends. It is the focal location for new retailers seeking representation in the United Kingdom. London plays a key role on the regional, national and international stage. It is a top target destination for international retailers, and has attracted a greater number of international brands than any other city globally. Demand among international retailers remains strong with high profile deals by the likes of Microsoft, Samsung, Peloton, Gentle Monster and Free People. For those adopting a flagship store only strategy, London gives access to the UK market and is also seen as the springboard for store expansion to the rest of Europe. One of the trends to have emerged is the number of retailers upsizing flagship stores in London; these have included Adidas, Asics, Alexander McQueen, Hermès and Next. Another developing trend is the growing number of food markets. Openings planned include Eataly in City of London, Kerb in Seven Dials and Market Halls on Oxford Street. London is the home to 8.85 million people and hosting over 26 million visitors annually, contributing more than £11.2 billion to the local economy. In central London there is limited retail supply LONDON and retailers are showing strong trading performances. OVERVIEW Cushman & Wakefield | London | 2019 1 LONDON KEY RETAIL STREETS & AREAS CENTRAL LONDON MAYFAIR Central London is undoubtedly one of the forefront Mount Street is located in Mayfair about a ten minute walk destinations for international brands, particularly those from Bond Street, and has become a luxury destination for with larger format store requirements. -

Hot and Cold Seasons in the Housing Market∗

Hot and Cold Seasons in the Housing Market L. Rachel Ngai Silvana Tenreyro London School of Economics, CEP, and CEPR April 2013 Abstract Every year housing markets in the United Kingdom and the United States experience system- atic above-trend increases in both prices and transactions during the second and third quarters (the “hot season”) and below-trend falls during the fourth and first quarters (the “cold sea- son”). House price seasonality poses a challenge to existing models of the housing market. To explain seasonal patterns, this paper proposes a matching model that emphasizes the role of match-specific quality between the buyer and the house and the presence of thick-market effects in housing markets. It shows that a small, deterministic driver of seasonality can be amplified and revealed as deterministic seasonality in transactions and prices, quantitatively mimicking the seasonal fluctuations observed in the United Kingdom and the United States. Key words: housing market, thick-market effects, search-and-matching, seasonality, house price fluctuations, match quality For helpful comments, we would like to thank James Albrecht, Robert Barro, Francesco Caselli, Tom Cunningham, Morris Davis, Steve Davis, Jordi Galí, Christian Julliard, Peter Katuscak, Philipp Kircher, Nobu Kiyotaki, John Leahy, Francois Ortalo-Magné, Denise Osborn, Chris Pissarides, Richard Rogerson, Kevin Sheedy, Jaume Ventura, Randy Wright, and seminar participants at the NBER Summer Institute, SED, and various universities and central banks. For superb research assistance, we thank Jochen Mankart, Ines Moreno-de-Barreda, and Daniel Vernazza. Tenreyro acknowledges financial support from the European Research Council under the European Community’s ERC starting grant agreement 240852 Research on Economic Fluctuations and Globalization, Bank of Spain through CREI’sAssociate Professorship, and STICERD starting grant. -

High Streets & Town Centres: Adaptive Strategies Guidance

HIGH STREETS & TOWN CENTRES ADAPTIVE STRATEGIES GOOD GROWTH BY DESIGN A BUILT ENVIRONMENT FOR ALL LONDONERS A BUILT ENVIRONMENT FOR ALL LONDONERS CONTENTS Mayor's Foreword 7 Introduction 9 About this guidance 1. Investing in high streets 15 The value in London's high streets Cross-cutting areas for intervention A case for investment 2. Adapting to the challenges 29 High street challenges 3. Learning from London's high streets 79 Harlesden, LB Brent – The high street experience 85 West End, LB Westminster – Retail retrofit 95 Old Kent Road, LB Southwark – Intense mixed uses 111 Church Street, LB Westminster – Retaining community value 123 Dalston High Street, LB Hackney – Data insights 137 Tottenham High Road, LB Haringey – Social value 151 Stratford High Street, LB Newham – High road to high street 167 Sutton High Street, LB Sutton – Place of work 181 Walthamstow, LB Waltham Forest – Civic and cultural institution 193 South Norwood, LB Croydon – Sustainable community network 203 4. Developing adaptive strategies 217 Adaptive strategies The mission Principles and practices Structure of an adaptive high street strategy Appendices – published online at london.gov.uk Appendix 1: Evaluation and monitoring Appendix 2: Relevant data sources Appendix 3: Relevant literature MAYOR'S FOREWORD London’s high streets and town centres have shaped the fabric of our great city. They are a focal point for our culture, communities and everyday economies. They support the most sustainable models of living and working, including active travel and shorter commutes. And they are where new ideas, new ways of living, new businesses and new experiences are made. Our high streets and town centres face many challenges, but our research shows how much Londoners value them as places to meet, socialise, access services, shop, work and live. -

Premium and Convenience Opportunities

Premium and Convenience Opportunities UK FOOD MARKET Please insert a suitable picture in this size OFFICIAL PROGRAM PARTNER UK FOOD MARKET CONVENIENCE & PREMIUM OPPORTUNITIES Date: 24.08.15 Language: ENGLISH Number of pages: 19 Author: JANE MILTON Other sectorial Reports: Are you interested in other Reports for other sectors and countries? Please find more Reports here: s-ge.com/reports DISCLAIMER The information in this report were gathered and researched from sources believed to be reliable and are written in good faith. Switzerland Global Enterprise and its network partners cannot be held liable for data, which might not be complete, accurate or up-to-date; nor for data which are from internet pages/sources on which Switzerland Global Enterprise or its network partners do not have any influence. The information in this report do not have a legal or juridical character, unless specifically noted. Contents 5.2.5. Harvey Nichols _______________________ 14 1. FOREWORD____________________________ 4 5.2.6. Selfridges ____________________________15 2. INTRODUCTION ________________________ 5 5.2.7. Fortnum and Mason ____________________15 5.2.8. Wholefoods Market _____________________15 3. FOOD & DRINK MARKET KEY TRENDS _____ 6 5.3. Distribution Channels ___________________15 3.1. Clean eating __________________________ 6 5.4. Opportunities for Swiss Businesses in the Premium 3.2. Rise in online food shopping _______________ 6 Sector ______________________________15 3.3. Sugar backlash ________________________ 7 6. KEY TRADE SHOWS AND EVENTS FOR THE 4. CONVENIENCE MARKET _________________ 8 SECTOR ______________________________ 16 4.1. MARKET DEVELOPMENT _______________ 8 6.1. Speciality and Fine Food Fair, London _______ 16 4.2. MAIN PLAYERS ______________________ 10 6.2. -

Older Generations to Rescue the High Street

Older generations to rescue the high street Sponsored by Perspectives centreforfuturestudies strategic futures consultancy The Centre for Future Studies (CFS) is a strategic futures consultancy enabling organisations to anticipate and manage change in their external environment. Our foresight work involves research and analysis across the spectrum of political, economic, social and technological themes. Our clients include national and international companies, not-for-profit organisations, government departments and agencies. Centre for Future Studies Innovation Centre Kent University Canterbury, Kent CT2 7FG +44 (0) 800 881 5279 [email protected] www.futurestudies.co.uk November 2017 ________________________________________________________________ 2 centreforfuturestudies strategic futures consultancy Acknowledgements This report builds on the findings of the work undertaken by the International Longevity Centre – UK (ILC-UK); in particular: . “The Missing £Billions: The economic cost of failing to adapt our high street to respond to demographic change.” December 2016. “Understanding Retirement Journeys: Expectations vs reality.” November 2015. Future of ageing conference. November 2015 . “Financial Wellbeing in Later Life. Evidence and policy. March 2014 Key data sources: Age UK British Independent Retailers Association British Retail Consortium Communities & Local Government Centre for Retail Research Council of Shopping Centres Department for Business Innovation & Skills Department for Communities & Local Government Friends of the Elderly Innovate UK Institute for Public Policy Research Ipsos Retail Performance Kings Fund KPMG NatCen - the English Longitudinal Study of Ageing (2014/15) Office for National Statistics The English Longitudinal Study of Ageing (ELSA), The UK Household Longitudinal Study (UKHLS, now known as Understanding Society) UK Data Service World Health Organisation ________________________________________________________________ 3 centreforfuturestudies strategic futures consultancy Contents 1.