Power Play: Canada's Role in the Electric Vehicle Transition

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Investor Presentation

Investor Presentation NOVEMBER 2019 WHO IS NFI? Bus Design and Manufacture Part Fabrication Aftermarket and Service Carfair Composites is a leader in North America’s most The North American Leader in fiber-reinforced plastic (FRP) comprehensive parts Heavy-Duty Transit buses design and composites organization, providing technology parts, technical publications, training, and support for its OEM Started in 1941 in Winnipeg, NFI’s dedicated internal parts- product lines North America’s largest fabrication facility launched in manufacturer of Motor Coaches 2017 in Shepherdsville, KY UK’s leading bus parts distributor and aftermarket service Tracing its roots to 1892 with the support network Dennis, Alexander and Plaxton companies, ADL is a global manufacturer of double deck Supports eMobility and single deck buses and projects from start to motor coaches headquartered in finish Larbert, Scotland Founded in 2008 in Middlebury, Indiana ARBOC is a leader in low- floor cutaway and medium-duty shuttles 2 OUR MISSION OUR VISION To design and deliver To enable the future of exceptional transportation mobility with innovative solutions that are safe, and sustainable solutions accessible, efficient and reliable WHY INVEST IN NFI Track Record Our Differentiators • Trusted business partner with nearly 400 years of combined • Exclusively focused on bus & coach with market leading bus and motor coach design and manufacturing experience positions in multiple jurisdictions • 5 year Q3 2019 LTM Revenue CAGR of 13.3% and Adj. • ~75% of revenue driven by public customers EBITDA CAGR of 22.3% • A market technology leader with a track record of • 11.3% Q3 2019 LTM Adj. EBITDA margin innovation offering all types of propulsion options • History of sustainable dividends: 13.3% annual growth in • Vertically integrated North American part fabrication to annual dividend in 2019 with 49.6% Q3 2019 LTM payout ratio control cost, time and quality. -

Invest in Canada an Overview Canada: Your Gateway to North America and the World

2017 ELECTRONIC UPDATE INVEST IN CANADA AN OVERVIEW CANADA: YOUR GATEWAY TO NORTH AMERICA AND THE WORLD THROUGH NAFTA, INVESTORS IN CANADA GAIN PREFERENTIAL ACCESS TO A CONTINENTAL MARKET OF OVER US $21 TRILLION (GDP) WITH NEARLY 490 MILLION CONSUMERS EACH DAY, MORE THAN $2.4 BILLION WORTH OF TRADE CROSSES THE CANADA-US BORDER KEY FACTS ABOUT CANADA (2016) Population 36.5 million GDP $2.113 trillion GDP per capita $57,885 Exports of goods and services $628.7 billion Imports of goods and services $676.7 billion Consumer price inflation 1.6% Stock of Foreign Direct Investment in Canada $825.7 billion Stock of Canadian Direct Investment Abroad $1,049.6 billion Sources: Statistics Canada and International Monetary Fund. INVEST IN CANADA WHERE WE DELIVER BEST BUSINESS ENVIRONMENT IN THE G20 According to recent rankings from both Forbes1 and US News,2 Canada is the best country in the G20 for establishing business operations, and the Economist Intelligence Unit asserts that Canada is expected to be the second best country in the G7 for doing business over the next five-year period, from 2017 to 2021.3 Canada also holds the distinction of being the easiest location in the G20 to start a business, with the process requiring only two procedures and less than two days, according to the World Bank.4 For investors, Canada’s high global rankings demonstrate an environment that nurtures business growth. 1 Forbes.com LLC. Best Countries for Business 2017. 2 US News. Open for Business Rankings 2017. 3 Economist Intelligence Unit. Business Environment Rankings, 2017. -

March 2020 After 28 Years of Service with the Company, Fifteen of Which As CFO

NFI GROUP INC. Annual Information Form March 16, 2020 TABLE OF CONTENTS BUSINESS OF THE COMPANY ............................................................................................................................... 2 CORPORATE STRUCTURE ..................................................................................................................................... 3 GENERAL DEVELOPMENT OF THE BUSINESS .................................................................................................. 4 Recent Developments ........................................................................................................................................... 4 DESCRIPTION OF THE BUSINESS ......................................................................................................................... 7 Industry Overview ................................................................................................................................................ 7 Company History ............................................................................................................................................... 10 Business Strengths .............................................................................................................................................. 10 Corporate Mission, Vision and Strategy ............................................................................................................. 13 Environmental, Social and Governance Focus .................................................................................................. -

GCLC-BT Conference 5 December 2005, London Competition Law and Media Content

GCLC-BT Conference 5 December 2005, London Competition Law and Media Content I. MORNING SESSION 9:00 – 9:10 General introduction to the conference Damien Geradin Director of the GCLC Paolo Palmigiano Head of Competition and Regulatory Law, BT Retail 9:10 – 9:30 Welcome words Dan Marks CEO TV Services, BT Paolo Palmigiano Head of Competition and Public Law, BT Retail SESSION 1: THE LAW AND ECONOMICS OF MEDIA CONTENT 9:30 – 10:00 The economics of media content Stefan Szymanski Professor of Economics, Tanaka Business School, Imperial College London 10:00 – 10:30 Overview of the legal framework applicable to the media content Romano Subiotto Partner, Cleary Gottlieb 10:30 – 10:50 Coffee break SESSION 2: REGULATORY AND COMPETITION LAW APPROACHES TO MEDIA CONTENT IN THE EU, THE UK, AND THE US 10:50 – 11:10 The situation in the EU Speaker from the European Commission to be advised 11:10 – 11:30 The situation in the UK Becket McGrath Partner, Berwin Leighton Paisner 11:30 – 11:50 The situation in the US John Thorne Deputy General Counsel, Verizon 11:50 – 12:20 Roundtable discussion 12:20 – 13:30 Lunch break II. AFTERNOON SESSION 13:30 – 13:50 Tomorrow’s world – How will the media content industry look like in the future SESSION 3: CURRENT ISSUES REGARDING MEDIA CONTENT Chairman: Bernard Amory, Partner, Jones Day 13:50 – 14:10 Competition law issues raised by exclusivity Didier Théophile Partner, Darrois, Villey, Maillot et Brochier 14:10 – 14:30 Cross platform bundling of rights Andrea Appella Vice President & Associate General Counsel - Time Warner Europe 14:30 – 14:50 Collective selling and buying of premium content rights Helmut Brockelman Partner, Martinez Lage & Associados 14: 50 – 15:20 Commentators Dr. -

1 Electrifying Medium-Duty Vehicles in Minnesota Capstone Paper In

Electrifying Medium-Duty Vehicles in Minnesota Capstone Paper In Partial Fulfillment of the Master's Degree Requirements The Hubert H. Humphrey School of Public Affairs The University of Minnesota Christov Churchward, Jacob Herbers, Ben Picone, Drew Turro Client: Minnesota Pollution Control Agency Capstone Instructor: Fred Rose Date of Oral Presentation: 5/6/2019 Approval Date of Final Paper: 1 Executive Summary State of the Market Medium-duty electric vehicles (MDEVs) are still in the early stages of adoption across the U.S. Cost- parity on the initial purchase price of these vehicles relative to their conventional counterparts is not expected until the mid-2020s. A lack of organizational experience operating and maintaining EVs and a dearth of charging infrastructure present challenges to the early deployment of all types of EVs. Furthermore, most test cases for MDEVs are in California, whose warmer climate makes it difficult to draw accurate operational comparisons to Minnesota. Despite this, manufacturers are entering the market and providing a greater variety of vehicle choices. The number of class three through six (5-13 tons) electric vehicles on the market increased by a factor of six from 2013 to 2018, going from four to 24. Utilities, recognizing customer demand for EVs, are developing specialized programs and electricity rates for their customers to keep the costs of EV charging low. Furthermore, MDEVs operate with half the fuel cost per mile versus a comparable diesel vehicle. For fleet owners able and willing to take on the -

Multiple Year Bus Procurement Program

Customer Services, Operations, and Safety Committee Board Action/Action Item III-A September 13, 2007 Multiple Year Bus Procurement Program Washington Metropolitan Area Transportation Authority Board Action/Information Summary Action MEAD Number: Resolution: Information 99828 Yes No PURPOSE Obtain Board approval to award a one-year base with four one-year options competitive procurement of hybrid electric buses and a procurement of 22 articulated Compressed Natural Gas (CNG) buses utilizing piggy-back options available from Los Angeles County Metropolitan Transportation Authority. DESCRIPTION On May 4, 2006, staff presented to the Planning and Development Committee the Bus Technology selection for FY08-12 and requested approval to initiate and award a one-year base with four one-year options competitive procurement of hybrid electric buses. This contract includes 100 buses a year for five years with options for an additional 100 buses each year assignable to other agencies. The Committee requested staff return to the Committee for final approval of the selected vendor. On June 19, 2006, the Board approved funding and authority to initiate the contracting action. Additionally, staff is requesting Board approval to purchase 22 articulated CNG buses as replacement buses. These 22 articulated CNG buses will be procured in accordance with Federal Transit Administration (FTA) Circular 4220 1.E “Assignabilty” options available from Los Angeles County Metropolitan Transportation Authority for CNG Bus Rapid Transit (BRT) style buses. FUNDING IMPACT There is no further impact on funding. Funding approved June 2006. RECOMMENDATION Board approval to award a one-year base with four one-year options competitive procurement of hybrid electric buses and procure 22 articulated CNG buses utilizing piggy-back options available from Los Angeles County Metropolitan Transportation Authority for CNG Bus Rapid Transit (BRT) style buses. -

Consult the Reporting Issuer List

AUTORITÉ DES MARCHÉS FINANCIERS Reporting Issuers List This list is updated at the date indicated below and takes into account all documents filed on the previous date. Defaults Various default codes are used on the list of reporting issuers. The codes appear under the heading “Defaults” and refer to the Default Nomenclature below. The AMF will make every effort to ensure the accuracy of the list. However, reporting issuers should promptly contact the AMF if they do not appear on the list of reporting issuers in Québec or if they are inadvertently identified as being in default. Last update : &[Date]2021-09-24 Default Nomenclature 1a. Failure to file the annual financial statements. 1b. Failure to file the interim financial report. Failure to file the annual or interim management’s discussion and analysis (MD&A) or the annual or interim 1c. management report of fund performance (MRFP). 1d. Failure to file the Annual Information Form (AIF). Failure to file the certification of annual or interim filings required by Regulation 52-109 respecting Certification of 1e. Disclosure in Issuers’ Annual and Interim Filings (“Regulation 52-109”). 1f. Failure to file the required proxy materials or the required information circular. 1g. Failure to file the issuer profile supplement on the System for Electronic Disclosure by Insiders (SEDI). 1h. Failure to file the material change report. 1i. Failure to provide the written update after filing a confidential report of a material change. 1j. Failure to file the business acquisition report. Failure to file the annual oil and gas disclosure prescribed by Regulation 51-101 respecting Standards of Disclosure of 1k. -

1 2021 Electric Truck & Bus Update, Part 2

2021 Electric Truck & Bus Update, Part 2: Buses By John Benson September 2021 1. Introduction This is Part 2 and focuses on buses. Battery-electric buses are being deployed more rapidly that medium and heavy battery-electric trucks, mainly because of federal and state incentives. A major consideration, especially for electric utility professionals, is that battery-electric buses take a huge amount of energy to charge them. Also many of these vehicles will perform depot recharging en masse. This will be mostly overnight in transit depots. These facilities are currently not prepared for the massive load increase as their vehicles transition to electric operation. The flowing is a description of and link to part 1 of this series: https://energycentral.com/c/ec/2021-electric-truck-bus-update-part-1-trucks The following was the last paper on this subject, which was posted in January. Electric Refuse Trucks & Battery-Electric Buses: This post is a review of both of these two-vehicle types and considerations as they electrify. https://energycentral.com/c/cp/electric-refuse-trucks-battery-electric-buses Section 2 of this report will describe all major manufacturers of buses, their offerings and any new developments by those firms. Section 3 will describe how fleet managers can evaluate and remedy the overload risk described above. 2. Buses A few of the big players in the large-to-medium truck market are also players in the bus market – see the first two below, for instance (see part 1 of this series for truck models for these two manufacturers). Also the third firm below is not only the largest player in the bus market, and a technology leader, but is starting to spin their technologies off into other markets, including trucks 2.1. -

Fiorelli Et Al V. Volkswagen Group of America, Inc

Case 2:15-cv-07330-JLL-JAD Document 1 Filed 10/06/15 Page 1 of 98 PageID: 1 Joseph F. Rice James E. Cecchi Jodi Westbrook Flowers CARELLA, BYRNE, CECCHI, WOLF Kevin R. Dean OLSTEIN, BRODY &ANGELO, P.C. MOTLEY RICE LLC 5 Becker Farm Road 28 Bridgeside Blvd. Roseland, NJ 07068 Mt. Pleasant, SC 29464 (973) 994-1700 (843) 216-9000 Christopher M. Placitella, Esquire Michael Coren, Esquire COHEN, PLACITELLA & ROTH, P.C. 127 Maple Ave. Red Bank, NJ, 07701 (732) 747-9003 Attorneys for Plaintiffs UNITED STATES DISTRICT COURT FOR THE DISTRICT OF NEW JERSEY KAREN FIORELLI, STEVEN C. ) MENDOZA, MARTIN SCHMIDT, ) Case No. PAUL SACAMANO, DEBORAH ) MCCROHON and WENDY ) BRANZBURG, Individually and on ) behalf of others similarly situated, ) ) CLASS ACTION Plaintiffs, ) ) CLASS ACTION COMPLAINT v. ) ) JURY TRIAL DEMANDED VOLKSWAGEN GROUP OF AMERICA, ) INC., A New Jersey Corporation, and ) VOLKSWAGEN AG, A German ) Corporation. ) ) ) Defendants. ) ______________________________________ Case 2:15-cv-07330-JLL-JAD Document 1 Filed 10/06/15 Page 2 of 98 PageID: 2 Plaintiffs Karen Fiorelli, Steven C. Mendoza, Martin Schmidt, Paul Sacamano, Deborah McCrohon and Wendy Branzburg (“Plaintiffs”), individually and on behalf of all others similarly situated (the “Class”), allege the following: I. INTRODUCTION 1. As Volkswagen USA CEO, Michael Horn, publicly admitted on September 21, 2015, “Volkswagen has broken the trust of our customers, and the public here in America.” Horn further publicly admitted on behalf of Volkswagen: “So let's be clear about this: our company was dishonest with the EPA and the California Air Resources Board, and with all of you," Horn continued. -

The Hours of Service (HOS) Rule for Commercial Truck Drivers and the Electronic Logging Device (ELD) Mandate

The Hours of Service (HOS) Rule for Commercial Truck Drivers and the Electronic Logging Device (ELD) Mandate March 18, 2020 Congressional Research Service https://crsreports.congress.gov R46276 SUMMARY R46276 The Hours of Service (HOS) Rule March 18, 2020 for Commercial Truck Drivers and the David Randall Peterman Analyst in Transportation Electronic Logging Device (ELD) Mandate Policy In response to the COVID-19 outbreak, on March 13, 2020, the Department of Transportation (DOT) issued a national emergency declaration to exempt from the Hours of Service (HOS) rule through April 12, 2020, commercial drivers providing direct assistance in support of relief efforts related to the virus. This includes transport of certain supplies and equipment, as well as personnel. Drivers are still required to have at least 10 consecutive hours off duty (eight hours if transporting passengers) before returning to duty. It has been estimated that up to 20% of bus and large truck crashes in the United States involve fatigued drivers. In order to promote safety by reducing the incidence of fatigue among commercial drivers, federal law limits the number of hours a driver can drive through the HOS rule. Currently the HOS rule allows truck drivers to work up to 14 hours a day, during which time they can drive up to 11 hours, followed by at least 10 hours off duty before coming on duty again; also, within the first 8 hours on duty drivers must take a 30-minute break in order to continue driving beyond 8 hours. Bus drivers transporting passengers have slightly different limits. Approximately 3 million drivers are subject to the federal HOS rule. -

Surplus Property Inventory

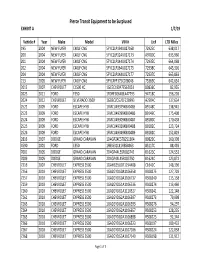

Pierce Transit Equipment to be Surplused EXHIBIT A 1/7/19 Vehicle # Year Make Model VIN # Lic# LTD Miles 195 2004 NEW FLYER C40LF CNG 5FYC2LP194U027168 72925C 638,017 200 2004 NEW FLYER C40LF CNG 5FYC2LP124U027173 A9780C 633,960 201 2004 NEW FLYER C40LF CNG 5FYC2LP144U027174 72935C 664,068 202 2004 NEW FLYER C40LF CNG 5FYC2LP164U027175 72938C 645,301 204 2004 NEW FLYER C40LF CNG 5FYC2LP1X4U027177 72937C 665,863 213 2005 NEW FLYER C40LF CNG 5FYC4FP175C028046 75369C 642,634 2012 2007 CHEVROLET C1500 XC 1GCEC19047E562051 80836C 82,955 2023 2011 FORD F350 1FDRF3G64BEA47793 94718C 156,201 2024 2012 CHEVROLET SILVERADO 3500 1GB3CZCG2CF228993 A2904C 137,634 2522 2009 FORD ESCAPE HYB 1FMCU49379KB00485 89148C 138,941 2523 2009 FORD ESCAPE HYB 1FMCU49399KB00486 89149C 175,408 2524 2009 FORD ESCAPE HYB 1FMCU49309KB00487 89180C 170,458 2525 2009 FORD ESCAPE HYB 1FMCU49329KB00488 89182C 123,724 2526 2009 FORD ESCAPE HYB 1FMCU49349KB00489 89181C 152,819 2816 2007 DODGE GRAND CARAVAN 1D4GP24E57B251304 80829C 160,398 4590 2001 FORD E350 1FBSS31L81HB58963 85117C 88,493 7001 2005 DODGE GRAND CARAVAN 2D4GP44L55R183742 B1623C 124,553 7009 2005 DODGE GRAND CARAVAN 2D4GP44L45R183750 B1624C 123,872 7216 2007 CHEVROLET EXPRESS 3500 1GAHG35U071194408 C1642C 148,396 7256 2010 CHEVROLET EXPRESS 3500 1GA2GYDG0A1106558 RS08275 127,703 7257 2010 CHEVROLET EXPRESS 3500 1GA2GYDG0A1106737 RS08240 115,158 7259 2010 CHEVROLET EXPRESS 3500 1GA2GYDG1A1106536 RS08274 113,460 7260 2010 CHEVROLET EXPRESS 3500 1GA2GYDG1A1110327 RS08241 122,148 7261 2010 CHEVROLET EXPRESS 3500 -

H3 AP201607080016477620 1.Pdf

Global Research 6 July 2016 Geely Automobile Equities Driving into a fast lane China Automobile Manufacturers 12-month rating Buy Upgrade to Buy on better than expected sales of Boyue and Emgrand GS Prior: Neutral We upgrade our 16/17 earnings estimates for Geely by 24% to reflect faster than 12m price target HK$5.00 expected sales momentum of Boyue and Emgrand GS which sales have already reached Prior: HK$4.10 over 8k/4.6k units in June, higher than UBSe of 6k/ 4k units. We expect the current Price HK$4.30 strong industry SUV growth (45% in 5M) to continue in 2H 2016, thus we are less concerned about the competition from intensive product launches. We expect Boyue's RIC: 0175.HK BBG: 175 HK monthly sales to reach 20k units once Baoji factory commenced production in Oct. Trading data and key metrics Meanwhile, we also forecast the Emgrand GS's monthly sales to reach 10k units by end 52-wk range HK$4.46-2.51 of 2016 given its strong performance to price. Market cap. HK$37.8bn/US$4.88bn High earnings visibility in 2016; 2 more new models to be launched in 2H16 Shares o/s 8,801m (ORD) Besides from Boyue and Emgrand GS, Geely will also launch the new Yuanjing SUV Free float 60% (Compact SUV) in Aug with MSRP of Rmb80-100k and Emgrand GL (A-class sedan) in Avg. daily volume ('000) 44,376 Q4. We have concerns over the high procurement cost for Boyue, however we believe Avg.