Banking E-Bulletin

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Influence of Merger on Performance of Indian Banks: a Case Study

Journal of Poverty, Investment and Development www.iiste.org ISSN 2422-846X An International Peer-reviewed Journal Vol.32, 2017 Influence of Merger on Performance of Indian Banks: A Case Study Gopal Chandra Mondal Research Scholar, Dept. of Economics, Vidyasagar University, India& Chief Financial Officer,IDFC Foundation,New Delhi, India Dr Mihir Kumar Pal Professor,Dept. Of Economics, Vidyasagar University, India Dr Sarbapriya Ray* Assistant Professor, Dept. of Commerce, Vivekananda College, Under University of Calcutta, Kolkata,India Abstract The study attempts to critically analyze and evaluate the impact of merger of Nedungadi bank and Punjab National Bank on their operating performance in terms of different financial parameters. Most of the financial indicators of Nedungadi bank and Punjab National Bank display significant improvement in their operational performance during post merger period. Therefore, the results of the study reveal that average financial ratios of sampled banks in Indian banking sector showed a remarkable and significant improvement in terms of liquidity, profitability, and stakeolders wealth. Keywords: Merger, India, Nedungadi bank, Punjab National Bank. 1. Introduction: Concept of merger and acquisition has become very trendy in present day situation, especially, after liberalization initiated in India since 1991. The emergent tendency towards mergers and acquisitions (M&As) world-wide, has been ignited by intensifying competition. Mergers and acquisitions have been taking place in corporate as well as banking sector to abolish financial, operation and managerial weakness as well as to augment growth and expansion , to create shareholders value, stimulate health of the organization with a view to confront challenges in the face of stiff competitive in globalized environment. -

State Bank of India

State Bank of India State Bank of India Type Public Traded as NSE: SBIN BSE: 500112 LSE: SBID BSE SENSEX Constituent Industry Banking, financial services Founded 1 July 1955 Headquarters Mumbai, Maharashtra, India Area served Worldwide Key people Pratip Chaudhuri (Chairman) Products Credit cards, consumer banking, corporate banking,finance and insurance,investment banking, mortgage loans, private banking, wealth management Revenue US$ 36.950 billion (2011) Profit US$ 3.202 billion (2011) Total assets US$ 359.237 billion (2011 Total equity US$ 20.854 billion (2011) Owner(s) Government of India Employees 292,215 (2012)[1] Website www.sbi.co.in State Bank of India (SBI) is a multinational banking and financial services company based in India. It is a government-owned corporation with its headquarters in Mumbai, Maharashtra. As of December 2012, it had assets of US$501 billion and 15,003 branches, including 157 foreign offices, making it the largest banking and financial services company in India by assets.[2] The bank traces its ancestry to British India, through the Imperial Bank of India, to the founding in 1806 of the Bank of Calcutta, making it the oldest commercial bank in the Indian Subcontinent. Bank of Madras merged into the other two presidency banks—Bank of Calcutta and Bank of Bombay—to form the Imperial Bank of India, which in turn became the State Bank of India. Government of Indianationalised the Imperial Bank of India in 1955, with Reserve Bank of India taking a 60% stake, and renamed it the State Bank of India. In 2008, the government took over the stake held by the Reserve Bank of India. -

Banking Laws in India

Course: CBIL-01 Banking Laws In India Vardhaman Mahaveer Open University, Kota 1 Course: CBIL-01 Banking Laws In India Vardhaman Mahaveer Open University, Kota 2 Course Development Committee CBIL-01 Chairman Prof. L. R. Gurjar Director (Academic) Vardhaman Mahaveer Open University, Kota Convener and Members Convener Dr. Yogesh Sharma, Asso. Professor Prof. H.B. Nanadwana Department of Law Director, SOCE Vardhaman Mahaveer Open University, Kota Vardhaman Mahaveer Open University, Kota External Members: 1. Prof. Satish C. Shastri 2. Prof. V.K. Sharma Dean, Faculty of law, MITS, Laxmangarh Deptt.of Law Sikar, and Ex. Dean, J.N.Vyas University, Jodhpur University of Rajasthan, Jaipur (Raj.) 3. Dr. M.L. Pitaliya 4. Prof. (Dr.) Shefali Yadav Ex. Dean, MDS University, Ajmer Professor & Dean - Law Principal, Govt. P.G.College, Chittorgarh (Raj.) Dr. Shakuntala Misra National Rehabilitation University, Lucknow 5. Dr Yogendra Srivastava, Asso. Prof. School of Law, Jagran Lakecity University, Bhopal Editing and Course Writing Editor: Course Writer: Dr. Yogesh Sharma Dr Visvas Chauhan Convener, Department of Law State P. G. Law College, Bhopal Vardhaman Mahaveer Open niversity, Kota Academic and Administrative Management Prof. Vinay Kumar Pathak Prof. L.R. Gurjar Vice-Chancellor Director (Academic) Vardhaman Mahaveer Open University, Kota Vardhaman Mahaveer Open University, Kota Prof. Karan Singh Dr. Anil Kumar Jain Director (MP&D) Additional Director (MP&D) Vardhaman Mahaveer Open University, Kota Vardhaman Mahaveer Open University, Kota Course Material Production Prof. Karan Singh Director (MP&D) Vardhaman Mahaveer Open University, Kota Production 2015 ISBN- All right reserved no part of this book may be reproduced in any form by mimeograph or any other means, without permission in writing from the V.M. -

Mergers and Acquisitions of Banks in Post-Reform India

SPECIAL ARTICLE Mergers and Acquisitions of Banks in Post-Reform India T R Bishnoi, Sofia Devi A major perspective of the Reserve Bank of India’s n the Reserve Bank of India’s (RBI) First Bi-monthly banking policy is to encourage competition, consolidate Monetary Policy Statement, 2014–15, Raghuram Rajan (2014) reviewed the progress on various developmental and restructure the system for financial stability. Mergers I programmes and also set out new regulatory measures. On and acquisitions have emerged as one of the common strengthening the banking structure, the second of “fi ve methods of consolidation, restructuring and pillars,” he mentioned the High Level Advisory Committee, strengthening of banks. There are several theoretical chaired by Bimal Jalan. The committee submitted its recom- mendations in February 2014 to RBI on the licensing of new justifications to analyse the M&A activities, like change in banks. RBI has started working on the framework for on-tap management, change in control, substantial acquisition, licensing as well as differentiated bank licences. “The intent is consolidation of the firms, merger or buyout of to expand the variety and effi ciency of players in the banking subsidiaries for size and efficiency, etc. The objective system while maintaining fi nancial stability. The Reserve Bank will also be open to banking mergers, provided competi- here is to examine the performance of banks after tion and stability are not compromised” (Rajan 2014). mergers. The hypothesis that there is no significant Mergers and acquisitions (M&A) have been one of the improvement after mergers is accepted in majority of measures of consolidation, restructuring and strengthening of cases—there are a few exceptions though. -

Sup Voice Sep-Oct 2013.Pmd

SEP.-OCT. 2013 SUP-VOICE FEDERATION NEWS CHECK-OFF: CONTEMPT CASE BY AISBOF JUSTICE AT LAST…… 10th September, 2013; as we stood in the Court with further plans to attack, demoralize, putdown and Hall No.11 of the Madras High Court, we had mixed humiliate people. “Ask them to express remorse!” “I feelings. Mr.Pratip Choudhuri, the former Chairman will dismiss all of them”, “I will meet you all in was to make a personal appearance in the contempt Supreme court” were some of the utterances, all proceedings in the Check – Off case filed by the filled with venom. The series of violations in Transfer Federation. And he appeared in person in the Policies and attacks on officers which have presence of the Hon’ble Justice. inconvenienced many need not be repeated. Lady Officers, who are 59 years, who were sick, who had 2. However much we all tried to forget, still, images problems were also mercilessly transferred of the past came flashing by. On the 4th of October, thousands of kilometers away. The word 2012 when the Federation leaders met him amidst compassion and mercy had lost its significance. a huge gathering of MD’s, DMD’s and CGM’s of all Indiscriminate transfers violating all agreed bilateral the circles, a pre-arranged audience to demonstrate policies took place. It was only fear and fear and his arrogance and dictatorship, he shouted and said fear all the way. “apologise and publish it in your website, make it public”. The intention was to embarrass and to insult. 3. Such a person, arrogance personified, stood Today, standing in the Court hall, when an in front of the Hon’ble Justice apologetically. -

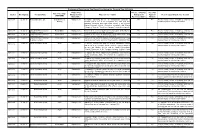

Votes Cast Data for F.Y. 2019-20

Disclosure of Vote Cast by Tata Mutual Fund during the Financial Year 2019-2020 Proposal by Investee company’s Vote (For/ Type of meetings Quarter Meeting Date Company Name Management or Proposal's description Management Against/ Reason supporting the vote decision (AGM/EGM) Shareholder Recommendation Abstain) April-June 02-Apr-19 Piramal Enterprise Ltd Court Convened Management Resolution approving Scheme of Amalgamation pursuant to For For This is normal course of business and has no Meeting Sections 230 to 232 of the Companies Act, 2013 and other material impact for minority shareholders applicable provisions and Rules made thereof, if any, between Piramal Phytocare Limited (˜Transferor Company") and Piramal Enterprises Limited ("Transferee Company") and their respective Shareholders April-June 11-Apr-19 GlaxoSmithKline Consumer Postal Ballot Management Revision in the terms of payment of remuneration to Mr. Navneet For For This is normal course of business and has no Healthcare Limited Saluja, Managing Director (DIN: 02183350) material impact for minority share holders April-June 11-Apr-19 GlaxoSmithKline Consumer Postal Ballot Management Revision in the terms of payment of remuneration to Mr. Anup For For This is normal course of business and has no Healthcare Limited Dhingra, Director - Operations (DIN: 07602670) material impact for minority share holders April-June 11-Apr-19 GlaxoSmithKline Consumer Postal Ballot Management Revision in the terms of payment of remuneration to Mr. Vivek For For This is normal course of business and -

Tuesday, 2-2-1971. a Meeting of the Governing Board of the Stock

Tuesday, 2-2-1971. A meeting of the Governing Board of the Stock Exchange was held today at S.T. 3.00 pm under the Chairmanship of Seth Dhirajlal Maganlal, wherein the undermentioned members of the Board were present: Seth Dhirajlal Maganlal Seth Gordhandas Bhagwandas Seth Phiroze J. Jeejeebhoy Seth Hiralal Girdharlal Seth Jayant Amerchand Seth Babubhai M. Gandhi Seth Vasantlal Kantilal Shah Seth Bharatkishore Begraj Gupta Seth Mathradas Samaldas Seth Vasantlal Jivatlal Seth Jasvantlal Chhotalal Seth Jivanchand Ratanchand Motishaw Seth Rasiklal Maneklal Seth Vasantlal Champaklal Seth Navinchandra Chhaganlal Kampani Government Nominees Shri M.N. Deshmukh. The following business was transacted in the meeting: 1. Resolved that this Board takes note of the sad demise of one of the oldest and leading members, members of the Governing Board and Trustee of the Stock Exchange, Shri Kantilal Ishwarlal and expresses it grief and sorrow. The Board also takes note of the selfless and invaluable services rendered by him for a long tie as a member of the Governing Board, Hon. Treasurer, member of the Defaulters’ Committee and its Chairman and as a Vice-President, President and the Trustee of the Exchange. The Board shares the deep grief and pain with the family members of the deceased and requests the President to send a copy of this Resolution to them as a token of its condolences. 2. Resolved that the undermentioned notices regarding cum right and ex-right transactions in the shares of the undermentioned concerned companies are confirmed: 1. Hindustan Motors Ltd. Notice No:35/71 dt.8-1-71 2. -

Restructuring of Indian Public Sector Banks: Genesis and the Challenges

INTERNATIONAL JOURNAL OF RESEARCH CULTURE SOCIETY ISSN: 2456-6683 Volume - 4, Issue - 5, May – 2020 Monthly, Peer-Reviewed, Refereed, Indexed Journal Scientific Journal Impact Factor: 5.245 Received on : 02/05/2020 Accepted on : 17/05/2020 Publication Date: 31/05/2020 Restructuring of Indian Public Sector Banks: Genesis and the Challenges PARMOD K. SHARMA Ph.D Scholar, Mittal School of Business Lovely Professional University, Phagwara (Punjab) Email - [email protected] Abstract: Banking industry has been facing difficulties worldwide. The problems have been common though scale might be different at different places. The major issues that have confronted them are providing customer delight by way of ‘wow’banking and to keep themselves afloat. There is abundant expectation by the public from the industry to provide state of the art technology at competitive pricing and products which give them their value for money. The regulators want these banks to be adequately capitalised to mitigate the enormous risks they undertake by financing borrowers who are genuine and need bank money for growth of their businesses and the unscrupulous ones who borrow money to divert it to their unfunded projects or in real estate to make a quick buck. The banks also on daily basis face the operational risks(frauds by public and employees, looting of ATMs and robberies etc).There is pressure on them to earn good profits by safe lending and expanding the reach by adding new customers. There is good competition between Public Sector Banks (PS Banks) among themselves and PS Banks and the private sector banks. Many private sector banks in past faced liquidity issues due to management failure and bad lending. -

Laxmichand Golwala Coleege of Commerce & Economics

LAXMICHAND GOLWALA COLEEGE OF COMMERCE & ECONOMICS M.G Road Ghatkopar-East, Mumbai-400077 (NAAC Accredited ‘B’ Grade with CGPA 2.81) Internal Quality Assurance Cell Organizes ONE DAY STUDENT’S RESEARCH NATIONAL CONCLAVE On 9 th December, 2017 (Saturday) ‘‘RECENT REFORMS IN TAXATION, REAL ESTATE AND BANKING SECTORS IN INDIA’’ Special Issue of an International SCHOLARLY RESEARCH JOURNAL FOR INTERDISCIPLINARY STUDIES IMPACT FACTOR SJIF 2016-6.177 UGC APPROVED SR. NO. 49366, ISSN-2278-8808 Dr. A. D. Vanjari Conference Chairperson Prin. Dr. Swati Desai Conference Secretary Copyright © Authors, December 2017 ISSN: 2278-8808 IMPACT FACTOR SJIF 2016- 6.177 Special Issue on Issues of ‘‘Recent Reforms in Taxation, Real Estate and Banking Sectors in India’’ Jan-Feb, 2018, Volume - 5, Issue – 44 Disclaimer: We do not warrant the accuracy or completeness of the Information, text, graphics, links or other items contained within these articles. We accept no liability for any loss, damage or inconvenience caused as a result of reliance on such content. Only the author is the authority for the subjective content and may be contacted. Any specific advice or reply to query on any content is the personal opinion of the author and is not necessarily subscribed to by anyone else. Warning: No part of this book shall be reproduced, reprinted, or translated for any purpose whatever without prior written permission of the Editor. There will be no responsibility of the publisher if there is any printing mistake. Legal aspect is in Mumbai jurisdiction only in Favor of Editor in Chief for this Special Issue on ‘‘Recent Reforms in Taxation, Real Estate and Banking Sectors in India’’ Published & Printed By SCHOLARLY RESEARCH JOURNALS TCG’S Sai Datta Niwas, D - Wing, F.No-104, Nr Telco Colony & Blue Spring Society, Jambhulwadi Road, Datta Nagar, Ambegaon (Kh), Pune-46 Website- www.srjis.com, Email- [email protected] Editorial Board One Day Students’ Research National Conclave 9th Dec 2017 Dr. -

TILAK MAHARASHTRA UNIVERSITY, PUNE Dissertation

TILAK MAHARASHTRA UNIVERSITY, PUNE Dissertation submitted for the partial fulfillment of M.Phil (Vidyanishnat) Degree “THE ANALYSIS OF THE PERFORMANCE OF MAJOR BANKS AFTER FINANCIAL SECTOR REFORMS” Researcher Mr Jeevan J Nagarkar M.A.(Eco), PGDFM Guide Dr. Santosh Dastane M.A.(Eco) Ph.D. Director, Neville Wadia Institute of Management Studies and Research NEHRU SAMAJIKSHASTRA VIDYASTHAN TILAK MAHARASHTRA UNIVERSITY Gultekdi, Pune – 411037 July - 2008 CERTIFICATE This is to certify that the work incorporated in the M.Phil (Vidyanishnat) Dissertation titled as, “The Analysis of the Performance of Major Banks After Financial Sector Reforms”, submitted by Mr. Jeevan Jayant Nagarkar has been carried out under my guidance. Such material as has been duly acknowledged is authentic with best of my knowledge, in this dissertation. DECLARATION I declare on oath that the references and literature, which are used in my dissertation, entitled, “The Analysis of the Performance of Major Banks After Financial Sector Reforms”, are from original sources and are acknowledged at the appropriate places in the dissertation. I declare further that I have not used this information for any other purpose, other than my research. Date – July 1, 2008 Place: Pune (NAGARKAR J J) ACKNOWLEDGEMENT I take great privilege to thank my research guide Dr. Santosh Dastane, Director N. Wadia Institute of Management Studies and Research, Pune, for accepting me as his research student of M Phil & for the help and support he extended towards me. I am grateful to him for his valuable guidance throughout my research, right from the collection of the data to its analysis. I also take the opportunity to thank Dr Praveen Jadhav, HOD, Dept of Economics TMV & Prof Jyoti Patil for their continuous support & guidance during the period of my research. -

Annual Report 2020

NEW HATTHA BANK TOWER PROJECT ANNUAL REPORT 2020 BUILDING A BRIGHT FUTURE TOGETHER CONTENT A. OPERATIONAL HIGHLIGHTS 2 32 Modernize Hattha Mobile B. FINANCIAL HIGHLIGHTS 4 33 Products and Services C. SOCIAL PERFORMANCE HIGHLIGHTS 5 37 Call Center D. CAMBODIA’S KEY ECONOMIC INDICATORS 6 37 Human Resources E. BUSINESS PARTNERS 7 39 The Spirit and The Letter F. COVERAGE AND DISTRIBUTION NETWORKS 8 40 I. INTERNAL CONTROL AND INTERNAL AUDIT G. CORPORATE INFORMATION 9 40 Internal Audit Shareholder 9 41 Risk Management About Hattha Bank 11 42 Compliance Vision, Mission and Core Values 12 43 J. SOCIAL PERFORMANCE MANAGEMENT Hattha Bank Milestones 13 44 Corporate Social Responsibility Message from Chairman 14 45 Environmental Performance Indicators Message from President & CEO 16 45 K. BOARD OF DIRECTORS REPORT H. BUSINESS REVIEW 17 51 L. AUDITED STATEMENTS FROM INDEPENDENT AUDITOR Board of Directors 17 51 Balance Sheet Board of Directors Meeting 20 53 Income Statement Executive Committee Members 23 54 Statement of Changes in Equity Organizational Structure 28 55 Statement of Cash Flows Key Accomplishment in 2020 29 57 M. THREE YEARS FINANCIAL SUMMARY The Change of Logo 31 ANNUAL REPORT 1 2020 A. OPERATIONAL HIGHLIGHTS LOAN PORTFOLIO Change Change Description (USD) 2018 2019 2020 (Amount) (%) Total Loan 757,326,744 1,050,928,838 1,322,729,009 271,800,171 26% Loan in KHR 72,363,197 160,299,247 219,051,919 58,752,672 37% Loan in USD 657,518,847 852,453,574 1,056,319,548 203,865,974 24% Loan in THB 27,444,700 38,176,017 47,357,541 9,181,525 24% Hattha Bank offers loan to a customer with 3 currency types such as: Khmer Riel, United States Dollar and Thai Baht. -

1 an Introduction to Indian Banking System

CHAPTER – 1 AN INTRODUCTION TO INDIAN BANKING SYSTEM INTRODUCTION The banking sector is the lifeline of any modern economy. It is one of the important financial pillars of the financial sector, which plays a vital role in the functioning of an economy. It is very important for economic development of a country that its financing requirements of trade, industry and agriculture are met with higher degree of commitment and responsibility. Thus, the development of a country is integrally linked with the development of banking. In a modern economy, banks are to be considered not as dealers in money but as the leaders of development. They play an important role in the mobilization of deposits and disbursement of credit to various sectors of the economy. The banking system reflects the economic health of the country. The strength of an economy depends on the strength and efficiency of the financial system, which in turn depends on a sound and solvent banking system. A sound banking system efficiently mobilized savings in productive sectors and a solvent banking system ensures that the bank is capable of meeting its obligation to the depositors. In India, banks are playing a crucial role in socio-economic progress of the country after independence. The banking sector is dominant in India as it accounts for more than half the assets of the financial sector. Indian banks have been going through a fascinating phase through rapid changes brought about by financial sector reforms, which are being implemented in a phased manner. The current process of transformation should be viewed as an opportunity to convert Indian banking into a sound, strong and vibrant system capable of playing its role efficiently and effectively on their own without imposing any burden on government.