Integrated Annual Report of PJSC FGC UES for 2018

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Annual Report ‘06 Contents

ANNUAL REPORT ‘06 CONTENTS MESSAGE TO SHAREHOLDERS ————————————————————————————— 4 MISSION AND STRATEGY ———————————————————————————————— 7 COMPANY OVERVIEW ————————————————————————————————— 13 ² GENERAL INFORMATION 13 ² GEOGRAPHIC LOCATION 14 ² CALENDAR OF KEY 2006 EVENTS 15 ² REORGANIZATION 16 CORPORATE GOVERNANCE —————————————————————————————— 21 ² PRINCIPLES AND DOCUMENTS 21 ² MANAGEMENT BODIES OF THE COMPANY 22 ² CONTROL BODIES 39 ² AUDITOR 40 ² ASSOCIATED AND AFFILIATED COMPANIES 40 ² INTERESTED PARTY TRANSACTIONS 41 SECURITIES AND EQUITY ——————————————————————————————— 43 ² CHARTER CAPITAL STRUCTURE 43 ² STOCK MARKET 44 ² DIVIDEND HISTORY 48 ² REGISTRAR 49 OPERATING ACTIVITIES. KEY PERFORMANCE INDICATORS ——————————————— 51 ² GENERATING FACILITIES 51 ² FUEL SUPPLY 52 ² ELECTRICITY PRODUCTION 56 ² HEAT PRODUCTION 59 ² BASIC PRODUCTION ASSETS REPAIR 59 ² INCIDENT AND INJURY RATES. OCCUPATIONAL SAFETY 60 ² ENVIRONMENTAL SAFETY 61 ELECTRICITY AND HEAT MARKETS ——————————————————————————— 65 ² COMPETITIVE ENVIRONMENT. OVERVIEW OF KEY MARKETS 65 ² ELECTRICITY AND HEAT SALES 67 FINANCIAL OVERVIEW ————————————————————————————————— 73 ² FINANCIAL STATEMENTS 73 ² REVENUES AND EXPENSES BREAKDOWN 81 INVESTMENT ACTIVITIES ———————————————————————————————— 83 ² INVESTMENT STRATEGY 83 ² INVESTMENT PROGRAM 84 ² INVESTMENT PROGRAM FINANCING SOURCES 86 ² DEVELOPMENT PROSPECTS 87 INFORMATION TECHNOLOGY DEVELOPMENT —————————————————————— 89 PERSONNEL AND SOCIAL POLICY. SOCIAL PARTNERSHIP ———————————————— 91 INFORMATION FOR INVESTORS AND SHAREHOLDERS —————————————————— -

HEDGE EFFECTIVENESS of the RTS INDEX FUTURES Anastasia Musorgina a Thesis Submitted to the University of North Carolina in Part

HEDGE EFFECTIVENESS OF THE RTS INDEX FUTURES Anastasia Musorgina A Thesis Submitted to the University of North Carolina in Partial Fulfillment of the Requirements for the Degree of Master of Business Administration Cameron School of Business University of North Carolina Wilmington 2011 Approved by Advisory Committee Nivine Richie Rob Burrus Cetin Ciner Chair Accepted by _____________________________ Dean, Graduate School TABLE OF CONTENTS ABSTRACT ............................................................................................................................. iii DEDICATION .......................................................................................................................... iv ACKNOWLEDGEMENTS ....................................................................................................... v LIST OF TABLES .................................................................................................................... vi LIST OF FIGURES ................................................................................................................. vii INTRODUCTION ..................................................................................................................... 1 Hedging .................................................................................................................................. 1 Russian Derivatives Market ................................................................................................... 2 Moscow Interbank Currency Exchange ................................................................................ -

Wiiw Research Report 367: EU Gas Supplies Security

f December Research Reports | 367 | 2010 Gerhard Mangott EU Gas Supplies Security: Russian and EU Perspectives, the Role of the Caspian, the Middle East and the Maghreb Countries Gerhard Mangott EU Gas Supplies Security: Gerhard Mangott is Professor at the Department Russian and EU of Political Science, University of Innsbruck. Perspectives, the Role of This paper was prepared within the framework of the Caspian, the the project ‘European Energy Security’, financed from the Jubilee Fund of the Oesterreichische Na- Middle East and the tionalbank (Project No. 115). Maghreb Countries Contents Summary ......................................................................................................................... i 1 Russia’s strategic objectives: breaking Ukrainian transit dominance in gas trade with the EU by export routes diversification ............................................................... 1 1.1 Nord Stream (Severny Potok) (a.k.a. North European Gas Pipeline, NEGP) ... 7 1.2 South Stream (Yuzhnyi Potok) and Blue Stream II ......................................... 12 2 The EU’s South European gas corridor: options for guaranteed long-term gas supplies at reasonable cost ............................................................................... 20 2.1 Gas resources in the Caspian region ............................................................. 23 2.2 Gas export potential in the Caspian and the Middle East and its impact on the EU’s Southern gas corridor ................................................................. -

Russian Ecm November 6, 2006

1 Russian ecm November 6, 2006 1. Investment banks index wars 2. 35 companies will raise $19bn in 2007, Deutsche Bank 3. RTS to launch a Russian NASDAQ 4. Market players to be licensed 5. Gazprombank finally to sell off media, petrochemical assets in IPO 6. Owner of the Chelyabinsk zinc plant (CZP) will sell 3% of their shares 7. Chemical firm share price collapses after dilutive share issue 8. Dymov Sausage to IPO 9. Eastern Property Holdigns increases capital by $125m 10. Far Eastern Sea Shipping Company will IPO 11. Mosenergo places in favour of Gazprom 12. OGK-5 sale a big success 13. Pharmaceutical producer to IPO 14. Pipemaker TMK IPOs 15. Russian commodity exchange plans to launch wheat futures 16. Severstal sets IPO price 17. Sistema-Hals IPO price range set 18. Uralkaliy decreases 9-month dividends by a third following flood 19. Uranium company to IPO 20. WBD owners sell small stake Investment banks index wars Monday, November 6, 2006 A veritable war of indexes is breaking out as Two of Russia's top investment banks launched new indexes, better to track Russia's increasingly sophisticated growth, that will compete with the proliferating number of indexes tracking Russia. Renaissance Capital has teamed up with emerging market gurus Morgan Stanley that puts together the widely quoted MSCI index - a benchmark for emerging market stock market preformace - to produce the MSCI http://businessneweurope.eu 2 Renaissance Index of TOP Liquid Russian Stocks (the MSCI Rencap Index, for short). Likewise, Troika Dialog launched a third tier index that tracks 50 companies that are on the up and up but currently fall below all the investment bank's radar screens. -

Годовой Отчет Annual Report

годовой отчет 2 0 0 6 annual report STATEMENT OF THE offices. The Bank continues with regional CHIEF EXECUTIVE expansion, and has already in place 13 branch% es in Russian cities in 2006 compared to 7 branches by the year end 2005. MBRD's Dear shareholders, customers and partners regional network comprises 54 offices regis% of the Bank: tered with the Bank of Russia and located in 22 Today, the banking sector dramatically shows most industrialised federal constituencies of it can be a development engine not only for home the Russian Federation. In so doing, the Bank financial system, but also for the Russian econo% intends to step up efforts in further building up my at large. By meeting demands of domestic the banking chain in the future. companies, deposit%taking institutions are MBRD, no doubt, notably strengthened its becoming, in essence, national circulatory sys% positions in the Russian financial market over the tem giving access to financing. To comply with reporting year. To illustrate, net assets increased such an important role, Russian banks should by nearly RUR23.28 billion, while capital rose have adequate capital, technologies, diversified more than by RUR1.7 billion. Total income was network and quality products. RUR5.154 billion against 2.9 billion in 2005, and Presently, Moscow Bank for Reconstruction net profit increased by 65% to RUR442 million. and Development strategically focuses on retail In March 2006, a US$60m 10%year subordi% business development. It means expanding the nated eurobond issue placed on the Luxembourg existent spectrum of services, implementing Stock Exchange was an important event. -

US Sanctions on Russia

U.S. Sanctions on Russia Updated January 17, 2020 Congressional Research Service https://crsreports.congress.gov R45415 SUMMARY R45415 U.S. Sanctions on Russia January 17, 2020 Sanctions are a central element of U.S. policy to counter and deter malign Russian behavior. The United States has imposed sanctions on Russia mainly in response to Russia’s 2014 invasion of Cory Welt, Coordinator Ukraine, to reverse and deter further Russian aggression in Ukraine, and to deter Russian Specialist in European aggression against other countries. The United States also has imposed sanctions on Russia in Affairs response to (and to deter) election interference and other malicious cyber-enabled activities, human rights abuses, the use of a chemical weapon, weapons proliferation, illicit trade with North Korea, and support to Syria and Venezuela. Most Members of Congress support a robust Kristin Archick Specialist in European use of sanctions amid concerns about Russia’s international behavior and geostrategic intentions. Affairs Sanctions related to Russia’s invasion of Ukraine are based mainly on four executive orders (EOs) that President Obama issued in 2014. That year, Congress also passed and President Rebecca M. Nelson Obama signed into law two acts establishing sanctions in response to Russia’s invasion of Specialist in International Ukraine: the Support for the Sovereignty, Integrity, Democracy, and Economic Stability of Trade and Finance Ukraine Act of 2014 (SSIDES; P.L. 113-95/H.R. 4152) and the Ukraine Freedom Support Act of 2014 (UFSA; P.L. 113-272/H.R. 5859). Dianne E. Rennack Specialist in Foreign Policy In 2017, Congress passed and President Trump signed into law the Countering Russian Influence Legislation in Europe and Eurasia Act of 2017 (CRIEEA; P.L. -

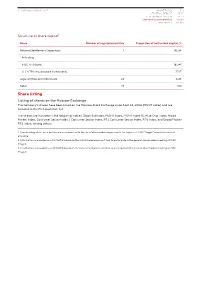

Share Listing

Annual Report 2018 | MAGNIT MAGNIT TODAY 3-11 99 STRATEGIC REPORT 13-27 PERFORMANCE REVIEW 29-53 CORPORATE GOVERNANCE 55-113 APPENDICES 115-189 Structure of share capital1 Name Number of registered entities Proportion of authorized capital, % National Settlement Depositary 1 95.54 Including: PJSC VTB Bank 18.342 LLC VTB Infrastructure Investments 7.723 Legal entities and individuals 24 4.46 Total: 25 100 Share listing Listing of shares on the Moscow Exchange The Company’s shares have been listed on the Moscow Stock Exchange since April 24, 2006 (MGNT ticker) and are included in the first quotation list. The shares are included in the following indices: Stock Subindex, MOEX Index, MOEX Index 10, Blue Chip Index, Broad Market Index, Consumer Sector Index / Consumer Sector Index, RTS Consumer Sector Index, RTS Index, and Broad Market RTS Index, among others. 1. Shareholding structure is provided in accordance with the list of shareholders registered in the register of PJSC “Magnit” shareholders as of 31.12.2018 2. Information is provided as of 12.11.2018 based on the list of shareholders entitled to participate in the general shareholders meeting of PJSC “Magnit 3. Information is provided as of 12.11.2018 based on the list of shareholders entitled to participate in the general shareholders meeting of PJSC “Magnit 100 101 Weight of shares in indices Ticker Index name Weight in index, % RDXUSD Russian Depositary Index USD 2.85 RDX Russian Depositary Index EUR 2.85 NU137529 MSCI EM IMI (VRS Taxes) Net Return USD Index 0.09 RIOB FTSE Russia IOB -

FSU/CEE Insight: Russia Special

Analytics. Studies. Modelling.The Oil and Gas Market’s Independent Research Centre. FSU/CEE Insight: Russia Special Issue 17 | 2-May-19 Weekly Report Editorial Nightmare Supply Scenario for FSU/CEE Refiners A full halt on Druzhba flows has refiners along the line scrambling to find alternative crude supplies Outage to affect Poland and Germany much less than Belarus A prolonged Druzhba outage would put an estimated 600,000 b/d of refining capacity at risk s we write this, flows along crude imported via the Druzhba have also been affected. However, it one of the oldest, longest, and pipeline always remained the also means that flows to Russia’s A most important pieces of oil baseload crude in these refineries. biggest export terminal, the Baltic pipeline infrastructure in the world Hence the current outage is an port of Primorsk, have not been are severely disrupted. We are of extremely significant event, contaminated. course referring to Russia’s Druzhba particularly as it may take months (Friendship) pipeline, which remains rather than weeks for the pipeline to A note on the contamination. We the lifeline to several Eastern return to normal operations. understand that the strategy being European and FSU refineries. The employed by the Russians is to northern leg of the pipe supplies Flows stopped after it became blend the crude down to levels Belarus, Poland, and eastern evident that the crude flowing along where the organic chlorides are no Germany, while the southern leg the pipeline was contaminated by longer high enough to cause serves refineries in Hungary, organic chloride in concentrations of problems. -

St Petersburg City & Leningrad Orphanage Addresses

St Petersburg & Leningrad Oblast orphanages from Yell.Ru – already translated, in Russian starts page 7 http://www.yell.ru/spbeng/index.php?company&p=1&ri=1925 ALMUS, Orphanage, Social & Rehabilitation Centre Tel. 568-33-52 192174, Ul. Shelgunova, 25 Fax 568-33-52 Map BLAGODAT, Children's Home № 41 Tel. 370-08-01 196191, Novoizmaylovskiy Prospekt, 40, build 3 Map CHILDREN'S ARK, Social Orphanage Tel. 700-55-56 192177, Pribrezhnaya Ul., 10, build 1 Fax 700-55-56 Map Children's Home Tel. 750-10-04 198260, Prospekt Narodnogo Opolcheniya, 155 Map Children's Home & School № 27 Tel. 461-45-80 196650, Kolpino, Ul. , 6 Map Children's Home & School № 46, English Tel. 430-32-51 197183, Ul. Savushkina, 61 Map Children's Home & School № 9 Tel. 772-46-53 192286, Bukharestskaya Ul., 63 Fax 772-58-47 Map Children's Home № 1 Tel. 377-36-61 198216, Schastlivaya Ul., 6 Fax 377-36-61 Map Children's Home № 1, Kingisepp Tel. (81375)273- 188485, Leningrad Region, Kingisepp, APTEKARSKIJ Pereulok, 14 90 Fax (81375)277-25 Children's Home № 10 Tel. 252-49-94 198095, Ul. Ivana Chernykh, 11-а Map Children's Home № 11 Tel. 360-02-71 192071, Bukharestskaya Ul., 37, build 2 Fax 360-02-71 Map Children's Home № 14 Tel. 232-58-06 197198, Syeszhinskaya Ul., 26/28 Map Children's Home № 19 Tel. 524-51-44 195298, derevnya Zanevka Children's Home № 2 for Retarded Children (Age 4-18) Tel. 450-52-70 198504, Stary Petergoff, Petergofskaya Ul., 4/2 Children's Home № 20 Tel. -

RUSSIA INTELLIGENCE Politics & Government

N°85 - October 9 2008 Published every two weeks / International Edition CONTENTS FINANCIAL CRISIS P. 1-3 Politics & Government c FINANCIAL CRISIS The game of massacre in Moscow c The game of massacre in The financial crisis has turned into a game of massacre in Moscow. October 6, 7 and 8, the Rus- Moscow sian stock market had to suspend operations several times, which did not prevent some shares from ARMY plunging by unimaginable proportions. Gazprom lost close to a quarter of its value in one session, No- c Serdyukov draws the lessons from the war in rilsk Nickel close to 40%, these two firms being probably the worst hit because they are the indus- Georgia trial standard-bearers of the Moscow marketplace and are especially the most “liquid” assets. The ALERT entirity of the listed Russian oil sector (including Transneft and Novatek) is worth today a bit less c Russia-Iceland : the than 130 billion dollars, or the equivalent of the value of the Brazilian company Petrobras according underside of a loan with to simulations by Russian analysts, which gives an idea of the price that Russia is paying in the cur- interest rent financial crisis. Even if the collapse of the Russian markets is totally exaggerated, investors consi- FOCUS der that Russia combines three major risks : a liquidity crisis in the banking sector despite massive c Anti- corruption campaign, support by the public authorities, a heavy indebtedness by the major industrial and energy compa- national cause or lost cause nies and the drop in oil prices and most of the primary commodities, on which the economic activity BEHIND THE SCENE is based. -

Subject of the Russian Federation)

How to use the Atlas The Atlas has two map sections The Main Section shows the location of Russia’s intact forest landscapes. The Thematic Section shows their tree species composition in two different ways. The legend is placed at the beginning of each set of maps. If you are looking for an area near a town or village Go to the Index on page 153 and find the alphabetical list of settlements by English name. The Cyrillic name is also given along with the map page number and coordinates (latitude and longitude) where it can be found. Capitals of regions and districts (raiony) are listed along with many other settlements, but only in the vicinity of intact forest landscapes. The reader should not expect to see a city like Moscow listed. Villages that are insufficiently known or very small are not listed and appear on the map only as nameless dots. If you are looking for an administrative region Go to the Index on page 185 and find the list of administrative regions. The numbers refer to the map on the inside back cover. Having found the region on this map, the reader will know which index map to use to search further. If you are looking for the big picture Go to the overview map on page 35. This map shows all of Russia’s Intact Forest Landscapes, along with the borders and Roman numerals of the five index maps. If you are looking for a certain part of Russia Find the appropriate index map. These show the borders of the detailed maps for different parts of the country. -

An Overview of Boards of Directors at Russia's Largest

An Overview of Boards of Directors at Russia’s Largest Public Companies Andrei Rakitin Milena Barsukova Arina Mazunova Translated from Russian August 2020 Key Results According to information disclosed by 109 of Russia’s largest public companies: • “Classic” board compositions of 11, nine, and seven seats prevail • The total number of persons on Boards of the companies under study is not as low as it might seem: 89% of all Directors were elected to only one such Board • Female Directors account for 12% and are more often elected to the audit, nomination, and remuneration committees than to the strategy committee • Among Directors, there are more “humanitarians” than “techies”, while the share of “techies” among chairs is greater than across the whole sample • The average age for Directors is 53, 56 for Chairmen, and 58 for Independent Directors • Generation X is the most visible on Boards, and Generation Y Directors will likely quickly increase their presence if the development of digital technologies continues • The share of Independent Directors barely reaches 30%, and there is an obvious lack of independence on key committees such as audit • Senior Independent Directors were elected at 17% of the companies, while 89% of Chairs are not independent • The average total remuneration paid to the Board of Directors is RUR 69 million, with the difference between the maximum and minimum being 18 times • Twenty-four percent of companies disclosed information on individual payments made to their Directors. According to this, the average total remuneration is approximately RUR 9 million per annum for a Director, RUR 17 million for a Chair, and RUR 11 million for an Independent Director The comparison of 2020 findings with results of a similar study published in 2012 paints an interesting dynamic picture.