Everyday Giving in India Report

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Crowdfunding in Asia

Crowdfunding in Asia May 2018 Introducing the first free directory of crowdfunding platforms across Asia. The data is based on the AlliedCrowds Capital Finder, a database of over 7,000 alternative finance capital providers across emerging markets. Our data has been used by organizations like FSD Asia, UNDP, World Green Economy Organization, GIZ, World Bank, and others in order to provide unique, actionable insights into the world of emerging market alternative finance. This is the latest of our regular reports on alternative finance in emerging markets; you can find all previous reports here. Crowdfunding rose in prominence in the post-financial crisis years (starting in 2012), and for good reason: a global credit crunch limited the amount of funding available to entrepreneurs and small businesses. Since then, crowdfunding has grown rapidly around the world. Crowdfunding is especially consequential in countries where SMEs find it difficult to raise capital to start or grow their businesses. This is the case in many Asian countries; according to the SME Finance Forum, there is a $2.3 trillion MSME credit gap in East Asia and the Pacific. Crowdfunding can help to fill this gap by offering individuals and small businesses an alternative source of capital. This can come in the form of donation-based as well as lending-based (peer-to-peer or peer-to-business) crowdfunding. In order to help entrepreneurs and small business owners to find the crowdfunding platform that’s right for them, we are releasing the first publicly available list of all crowdfunding platforms across Asia. The report is split into two key sections: the first one is an overview of crowdfunding platforms, and how active they are across the largest markets on the continent. -

Charitable Crowdfunding: Who Gives, to What, and Why?

APRIL 2021 Charitable Crowdfunding: Who Gives, to What, and Why? RESEARCHED AND WRITTEN BY Indiana University Lilly Family School of Philanthropy RESEARCHED AND WRITTEN BY — Indiana University Lilly Family School of Philanthropy The Indiana University Lilly Family School of Philanthropy is dedicated to improving philanthropy to improve the world by training and empowering students and professionals to be innovators and leaders who create positive and lasting change. The school offers a comprehensive approach to philanthropy through its academic, research and international programs, and through The Fund Raising School, Lake Institute on Faith & Giving, Mays Family Institute on Diverse Philanthropy, and Women’s Philanthropy Institute. Learn more at www.philanthropy.iupui.edu INDIANA UNIVERSITY LILLY FAMILY SCHOOL OF PHILANTHROPY PROJECT TEAM — Una O. Osili, PhD Associate Dean for Research and International Programs Jonathan Bergdoll, MA Applied Statistician Andrea Pactor, MA Project Consultant Jacqueline Ackerman, MPA Associate Director of Research, Women’s Philanthropy Institute Peter Houston, MBA Visiting Research Associate With special thanks to Dr. Wendy Chen, Dr. Debra Mesch, and Dr. Pamala Wiepking for reviewing the survey questionnaire. The survey was fielded by AmeriSpeak at NORC. The report was designed by Luke Galambos at Galambos + Associates. This research was completed with funding from Facebook. The findings and conclusions contained within are those of the authors and do not necessarily reflect official positions or policies of Facebook. INDIANA UNIVERSITY LILLY FAMILY SCHOOL OF PHILANTHROPY — 301 University Boulevard, Suite 3000, Indianapolis, IN 46202 317.278.8902 / [email protected] / @IUPhilanthropy / www.philanthropy.iupui.edu Contents Introduction ................................................... 02 Key Findings ................................................. 02 Background ................................................... 05 What is Crowdfunding? ...................................... -

Sattva Publications Report ATE Matching Contributions in India

MATCHING CONTRIBUTIONS IN INDIA A case to boost formal giving and amplify social impact SUPPORTED BY RESEARCH BY Delivering High Impact MATCHING CONTRIBUTIONS IN INDIA A case to boost formal giving and amplify social impact Acknowledgements Published by A.T.E. Chandra Foundation in partnership with Sattva Consulting in March 2020. Copyright © A.T.E. Chandra Foundation 2019 & Sattva 2020. Study commissioned by A.T.E. Chandra Foundation Research and writing Aashika Ravi, Abhineet Nayyar, Ambika Jugran, Shivani Desai, Yashasvi Murali (Sattva Research) Editing Aarti Mohan Project advisors Deepa Varadarajan and Manasa Acharya (Pramiti Philanthropy Partners), Komal Goyal and Priyaka Dhingra (A.T.E. Chandra Foundation) Design and typesetting Bhakthi Dakshinamurthy (HolyF Design), [email protected] Contact [email protected] This work is licensed under the Attribution-NonCommercial-ShareAlike 4.0 International License: Table of Contents Foreword 1 About the report and toolkit 2 Executive summary 3 Background and context 4 Definition of a matching contribution 6 Global evidence in support of matching campaigns 7 Successful matching campaigns in India 8 Benefits of matching campaigns 10 Enablers to matching in India 11 Matching in India: Some exemplars 12 Barriers to matching 27 Key takeaways 28 Research methodology and limitations 29 List of interviewees 30 Foreword knowledge that their donation would automatically double during that period. Often, the fact that someone the donor knows is matching their donation also increases credibility and therefore encourages donor participation. My wife Archana and I have been match-funders for over a decade and our personal experience has been very encouraging. The first time we ran a campaign over a decade ago, was done anonymously, during the India Giving Challenge run by GiveIndia. -

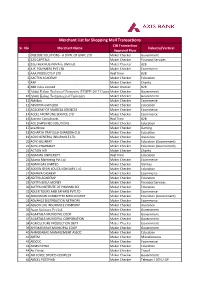

Merchant List for Shopping Mall Transactions CIB Transaction Sr

Merchant List for Shopping Mall Transactions CIB Transaction Sr. No Merchant Name Industry/Vertical Approval Flow 1 (N)CODE SOLUTIONS - A DIVN. OF GNFC LTD. Maker Checker Government 2 123 CAPITALS Maker Checker Financial Services 3 2GETHER HUB PRIVATE LIMITED Maker Checker B2B 4 A.R. POLYMERS PVT LTD Maker Checker Ecommerce 5 AAA PRODUCTS P LTD Real Time B2B 6 AACTEN ACADEMY Maker Checker Education 7 AAP Maker Checker Charity 8 ABB India Limited Maker checker B2B 9 Abdul Kalam Technical University (UPSEE-2017 Counselling)Maker Checker Government 10 Abdul Kalam Technological University Maker Checker Government 11 Abhibus Maker Checker Ecommerce 12 ABVIIITM-GWALIOR Maker Checker Education 13 ACADEMY OF MAGICAL SCIENCES Maker Checker Ecommerce 14 ACCEL FRONTLINE SERVICE LTD Maker Checker Ecommerce 15 Accrete Consultants Real Time B2B 16 ACE SIMPLIFIED SOLUTIONS Maker Checker Education 17 ace2three Maker Checker Gaming 18 ACHARYA PRAFULLA CHANDRA CLG Maker Checker Education 19 ACKO GENERAL INSURANCE LTD Maker Checker Insurance 20 ACPC-GUJARAT Maker Checker Education (Government) 21 ACPC-PHARMACY Maker Checker Education (Government) 22 ACTION AID Maker Checker Charity 23 ADAMAS UNIVERSITY Real Time Education 24 Adams Marketing Pvt Ltd Maker Checker Ecommerce 25 ADANI GAS LIMITED Maker Checker Utilities 26 ADDON GYAN EDUCATION SERV LTD Maker Checker Education 27 ADHAVA CASHEW Maker Checker Ecommerce 28 ADITYA ACADEMY Maker Checker Education 29 ADITYA BIRLA MONEY Maker Checker Financial Services 30 ADITYA INSTITUTE OF PHARMA SCI Maker Checker -

Crowdfunding Prospects in New Emerging Markets: the Cases of India and Bangladesh

13 Crowdfunding Prospects in New Emerging Markets: The Cases of India and Bangladesh Krishnamurthy Suresh, Stine Øyna, and Ziaul Haque Munim Introduction In 2013, the World Bank published a report on crowdfunding’s potential in emerging markets, which estimated a market opportunity for South Asia alone of close to USD 5 billion (The World Bank 2013). The South Asia region consists of predominantly collectivist societies (Hofstede Insights 2019)—India, Bangladesh, Sri Lanka, Pakistan, Bhutan, and Nepal—where helping others through donations is an integral part of K. Suresh (*) Indian Institute of Management Bangalore (IIM B), Bangalore, India S. Øyna School of Business and Law, University of Agder, Kristiansand, Norway e-mail: [email protected] Z. H. Munim Faculty of Technology, Natural Sciences and Maritime Sciences, University of South-Eastern Norway, Horten, Norway e-mail: [email protected] © The Author(s) 2020 297 R. Shneor et al. (eds.), Advances in Crowdfunding, https://doi.org/10.1007/978-3-030-46309-0_13 298 K. Suresh et al. prevailing religious obligations and societal norms. Thus, these countries share certain cultural and religious traits that are highly consistent with the principles of crowdfunding. Yet, by 2017, the alternative finance activity in the region amounted to no more than USD 269 million, 96% of which was related to the Indian market (see Table 13.1), indicating a vast untapped potential in the Asian economies. In the current chapter, we explore the history, ongoing activity, and future prospects of crowdfunding in new emerging markets. Specifically, we look into the cases of India and Bangladesh. -

Crowdfunding Platforms in India - Facts Based Comparison

© 2018 JETIR July 2018, Volume 5, Issue 7 www.jetir.org (ISSN-2349-5162) CROWDFUNDING PLATFORMS IN INDIA - FACTS BASED COMPARISON Prof. Rohini Sajjan1, Dr. H R Venkatesha2 Research Scholar1 , Professor & Director2 Department of Studies & Research inBusiness Administration1 Tumkur University, Tumkur, India Abstract: Crowdfunding is the employment of tiny funds from a big number of individuals to finance a new business enterprise. Mainly there are 3 parties involved in the process of Crowdfunding viz Investors, Fundraisers & Crowdfunding Platforms. Crowdfunding platforms acts as an intermediaries between fundraisers & investors and provides all services. The prime aim of this paper is to review &compare few top Indian Crowdfunding platforms. Crowdfunding industry is growing at a faster rate & many new platforms are emerging in the market to cater the personal, social, medical and other needs. They have raised crores of funds in a short span of time form their inception and served the society according to its requirements. IndexTerms: Crowdfunding, Crowdfunding Platforms, Crowdfunding Models, Funds, Investments. INTRODUCTION Crowdfunding is the employment of tiny funds from a big number of individuals to finance a new business enterprise. Crowdfunding can also be a fast and trouble-free way to meet unexpected, critical needs. Today, anyone with a smartphone can take part in making a difference with great ease. More and more people are now raising funds online with efficiently. Increasing digital access and the handiness of online payments are pushing more and more Indians to take the digital route to mobilize greater support for pressing needs on time. Mainly there are three parties involved in the process of Crowdfunding viz Investors, Fundraisers & Crowdfunding Platorms. -

A. Intellectual Disability (ID) 38 B

1 ChildRaise Resource Guide for Children with Special Needs Journey to Empowerment Kavita Shanbhag B.A (Psychology), B.Ed (Special Education), M.S (Counselling), Arts based Therapist. 2 © Kavita Shanbhag- 2018, Mumbai No part of this Publication maybe reproduced or transmitted by any means, electronic or mechanical, including photocopying, recording, or by any information storage and retrieval system, without written permission from the publisher and the author. I Edition – 2004 (Published by: English Edition) II Edition (Revised) -2010, Reprint- 2012 (Published by: ChildRaise Trust) III Edition (Revised) -2018 (Published by: ChildRaise Trust) ChildRaise Trust Regd.Office-E /15, Karnatak Bldgs, Mogal Lane, Mahim, Mumbai- 400016, India. Admin.Office-B wing, Block No. 9, Jaldevi Niwas, New Karnatak Bldg, Mogal Lane, Matunga Road (West), Mumbai-400016, India. +91-22-24386767. ‘DISHA’- Toll Free No: 1800-22-1203 For Copies Contact: Author- Kavita Shanbhag: 09820256731, 08898785000 Founder & Managing Trustee- ChildRaise Trust E Mail- [email protected] Rs. 500/- Disclaimer The Author has taken utmost care and efforts to ensure the completeness and accuracy of information presented in this resource guide, but there may be some omissions and errors due to changes in telephone numbers and addresses. The author is not responsible for the authenticity of description of the institutions or services provided. 3 This book is dedicated To You, the Traveler of “Journey to Empowerment.” 4 FOREWORD This Resource Guide 'Journey to Empowerment' serves as a light-house amidst the unclear waters of ignorance, feeling of being lost, confused or unguided. Dissemination of information regarding certain handicapping conditions in simple words is effective in enabling people to understand the condition from all perspectives. -

Banerjee, Shonali Ayesha.Pdf

A University of Sussex PhD thesis Available online via Sussex Research Online: http://sro.sussex.ac.uk/ This thesis is protected by copyright which belongs to the author. This thesis cannot be reproduced or quoted extensively from without first obtaining permission in writing from the Author The content must not be changed in any way or sold commercially in any format or medium without the formal permission of the Author When referring to this work, full bibliographic details including the author, title, awarding institution and date of the thesis must be given Please visit Sussex Research Online for more information and further details Intimate Technologies for Development: Micro-Philanthropy, Crowdfunding Platforms, and NGO Fundraising in India Shonali Ayesha Banerjee Submitted for the Degree of Doctor of Philosophy in International Development April 2020 I hereby declare that this thesis has not been and will not be, submitted in whole or in part to another University for the award of any other degree. Signature: Friday 3 April, 2020 2 Executive Summary of Thesis This thesis presents an account of my research on crowdfunding platforms and their non- governmental organization (NGO) partners in India. The current era of increasing reliance on technological advancement pressures the international development sector to innovate and digitize its programs and aid delivery. Crowdfunding platforms evolved in this technological climate to fill certain gaps between individuals and social projects. NGOs are compelled to diversify and innovate their fundraising strategies to keep up with industry standards and appeal to wider networks of individual donors. The primary research question addressed in this thesis is whether new fundraising models like crowdfunding are changing the overall landscape of development aid and NGO practice, particularly in India. -

5.483 Peer Reviewed & Indexed Journal

Research Paper IJMSRR Impact Factor: 5.483 E- ISSN - 2349-6746 Peer Reviewed & Indexed Journal ISSN -2349-6738 CROWD FUNDING PLATFORMS IN INDIA N. Vani* Dr. A. Srihari Krishna** *Research Scholar, Mewar University, Rajasthan. **Research Supervisor, Mewar University, Rajasthan. Abstract Crowd funding is not so popular in India. The concept of crowd funding is not new in India. Collecting the funds as a donation for some social causes is in practice in the country from ages together. Though the concept of collecting the fund form the crowd is same but in crowd funding the collection should be though a platforms (internet). The present paper highlights the various crowd funding platforms which exists in India. Introduction Globally the crowd funding industry has generated $ 40 billion But India has contributed a negligible fraction of it though the country is now the world’s second largest internet market with more than 400 million mobile users and many online payment options that make it easy to give money. Crowd funding is limited to giving donations and loans. The Securities and Exchange Board of India (SEBI) claims the Indian public lacks adequate investment knowledge or experience and requires strict protection. Crowd funding platforms in India, though not as popular as in other countries are slowly catching up and are playing a big role in fund raising. Many crowd funding platforms are emerging in India which help the fundraisers to raise funds for causes in various fields including cultural causes, entrepreneurship, medical causes, social causes etc. Crowd funding platforms Wish berry Wish berry is a donations-for-rewards crowd funding platform founded in 2010 in Mumbai and is exclusively dedicated to funding creative projects – music, stand-up comedy, film production, art, dance, design, photography, publishing, theatre. -

Monthly Coverage Dossier August 2018

Monthly Coverage Dossier August 2018 Prepared by IIT Madras is a campus of choice for high ranking JEE students Date: 30th August 2018 Publication: The Economic Times Edition: Delhi/Mumbai/Pune/Bangalore/Kolkata Page No: 22 Journalist: Sreeradha Basu Professor: Prof Manu Santhanam Headline: Pre-placement offers at IITs set for record high this year URL: https://economictimes.indiatimes.com/jobs/pre-placement-offers-at-iits-set-for-record-high-this- year/articleshow/65601308.cms IIT Madras is a multi-cultural campus Date: 4th August 2018 Publication: Times of India Edition: Kochi Page No: 9 Journalist: Manash Gohain Professor: Prof. R. Nagarajan Headline: IITs to form collective front to recruit foreign faculty URL: https://timesofindia.indiatimes.com/home/education/iits-to-form-collective-front-to-recruit- foreign-faculty/articleshow/65250989.cms Date: 3rd August 2018 Publication: The Times of India Edition: Kolkata/Ahemdabad Page No: 11 Journalist: Manash Pratim Gohain Professor: Prof R Nagarajan Headline: IITs to form collective front to recruit foreign faculty URL: https://timesofindia.indiatimes.com/home/education/iits-to-form-collective-front-to-recruit- foreign-faculty/articleshow/65250989.cms Date: 15th August 2018 Publication: The Times of India -Chennai Times Edition: Chennai Page No:10 Journalist: Ms Purnima Sah Students: Susanth Lavuya, Bhanu Mitra B,Anagh Sonam,A Venu Madhuri,Chandna Bhukya and Nikhil Bharadwaj Headline: Students and their idea of Independence IIT Madras is an Industry Friendly Institute Date: 1st August 2018 Publication: Indian Web Edition: Online Journalist: NA Headline: J. Mitra in Collab with IIT-Madras Launches ‘iQuant’, India’s First Portable Diagnostics Solution Device URL: https://www.indianweb2.com/2018/07/31/j-mitra-in-collab-with-iit-madras-launches-iquant- indias-first-portable-diagnostics-solution-device/ J. -

Annual Report 2017 - 18 Apollo Hospitals’ Mission Is “To Bring Healthcare of International Standards Within the Reach of Every Individual

# YouFirst Annual Report 2017 - 18 Apollo Hospitals’ Mission is “to bring healthcare of international standards within the reach of every individual. We are committed to the achievement and maintenance of excellence in education, research, and healthcare for the benefit of humanity.” CONTENTS 2 From the Chairman 4 Corporate Review Business Review 133 4 Business Snapshot Management Discussion and Analysis 133 10 Our Value Proposition Clinical Governance 165 12 We are uncompromising in our quality practices 16 We offer differentiated patient care across our facilities Financial Statements 175 Auditors’ Report on 36 We are responsive to our patients’ needs Standalone Financial Statements 175 48 We invest in cutting-edge technology Standalone Financial Statements 182 to enhance patient care Statement pursuant to Section 129 of the 52 Well positioned to provide the healthcare of tomorrow Companies Act, 2013 256 56 Statutory Section Auditors’ Report on Consolidated Financial Statements 258 56 Board Members Consolidated Financial Statements 264 57 Corporate Information 58 Directors’ Report to the Shareholders 99 Corporate Governance Report — Business Responsibility Report* * Business Responsibility Report is a separate enclosure and forms a part of this Annual Report. Note: Patient names have been withheld from all case studies and patient testimonials in this report in order to protect patient privacy. The Attendance Slip/Proxy Form and AGM Notice are being sent by speed post/email separately. We believe good health is paramount to your happiness. We believe equally that no matter who you are or where you come from, east, west, north or south, that you deserve the best care to preserve and sustain your well-being. -

Getting on Board

GETTING ON BOARD WHY PHILANTHROPY MUST SUPPORT CROWDFUNDING IN INDIA Rohini Nilekani is the Founder-Chairperson of Arghyam, a foundation she personally endowed to fund initiatives in Safe, Sustainable Water for All. In 2004, she co-founded and funded Pratham Books, a non-profit children’s publisher, which aims to democratize the joy of reading through their vision of seeing ‘a book in every child’s hands. In 2014, together with her husband, Nandan Nilekani, she co-founded—and is a Director of—EkStep, an education non-profit that has created a technology platform for early learning.’ As a committed philanthropist, she continues to fund work in areas such as governance and accountability, independent media, education and research, and environmental sustainability. CONTENTS Executive Summary...................................................................1 Introduction..............................................................................4 Chapter 1 Crowdfunding and Giving.................................................................5 A quick tour of crowdfunding platforms.....................................................8 Crowdfunding platforms across the world..................................................9 FOREWORD Chapter 2 Since the beginning of this decade, crowdfunding has enabled an ever-growing number of projects, All board: the case for crowdfunding in India.........................................10 from films to products to charitable work, to be successfully funded through online platforms. The Tapping into