Global Radio UK Limited/ Gcap Media

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

RAJAR Comparative Report Q3 2003

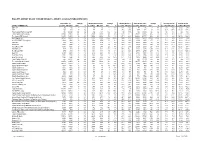

HALLETT ARENDT RAJAR TOPLINE RESULTS - WAVE 3 2003/LAST PUBLISHED DATA Population 15+ Change Weekly Reach 000's Change Weekly Reach % Total Hours 000's Change Average Hours Market Share LOCAL COMMERCIAL Last Pub W3 2003 000's % Last Pub W3 2003 000's % Last Pub W3 2003 Last Pub W3 2003 000's % Last Pub W3 2003 Last Pub W3 2003 Bath FM 82 82 0 0% 16 15 -1 -6% 19% 19% 88 95 7 8% 5.6 6.3 5.5% 5.8% 2BR 203 203 0 0% 77 78 1 1% 38% 38% 799 826 27 3% 10.3 10.6 18.3% 18.8% Total Capital Radio Group UK n/p 48384 n/a n/a n/p 7756 n/a n/a n/p 16% n/p 71888 n/a n/a n/p 9.3 n/p 6.8% Total Capital Radio Group 28097 28081 -16 0% 7600 7630 30 0% 27% 27% 70870 71265 395 1% 9.3 9.3 11.8% 11.9% The Capital FM Network 18951 18951 0 0% 5090 5016 -74 -1% 27% 26% 42282 41373 -909 -2% 8.3 8.2 10.3% 10.2% 95.8 Capital FM 10344 10343 -1 0% 2624 2269 -355 -14% 25% 22% 18991 15613 -3378 -18% 7.2 6.9 8.9% 7.0% 96.4 FM BRMB Birmingham 2004 2004 0 0% 588 555 -33 -6% 29% 28% 4339 4456 117 3% 7.4 8.0 9.8% 10.2% FOX FM 558 559 1 0% 208 214 6 3% 37% 38% 2289 2354 65 3% 11.0 11.0 19.2% 19.5% Invicta FM 1075 1075 0 0% 425 438 13 3% 39% 41% 4634 4984 350 8% 10.9 11.4 17.0% 18.3% 103.2 Power FM 1066 1066 0 0% 299 277 -22 -7% 28% 26% 2624 2326 -298 -11% 8.8 8.4 10.2% 9.7% Southern FM 949 949 0 0% 356 332 -24 -7% 38% 35% 4218 3679 -539 -13% 11.9 11.1 17.4% 16.3% Red Dragon FM 889 889 0 0% 301 311 10 3% 34% 35% 2789 2570 -219 -8% 9.3 8.3 13.3% 12.8% Beat 106 2599 2599 0 0% 415 447 32 8% 16% 17% 2976 3490 514 17% 7.2 7.8 5.8% 7.0% Beat 106 (East) 1101 1101 0 0% 199 198 -1 -1% 18% -

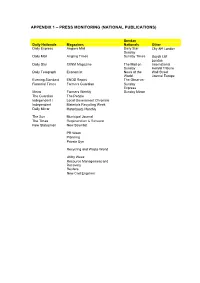

Appendix 1 – Press Monitoring (National Publications)

APPENDIX 1 – PRESS MONITORING (NATIONAL PUBLICATIONS) Sunday Daily Nationals Magazines Nationals Other Daily Express Anglers Mail Daily Star City AM London Sunday Daily Mail Angling Times Sunday Times Lloyds List London Daily Star CIWM Magazine The Mail on International Sunday Herald Tribune Daily Telegraph Economist News of the Wall Street World Journal Europe Evening Standard ENDS Report The Observer Financial Times Farmers Guardian Sunday Express Metro Farmers Weekly Sunday Mirror The Guardian The People Independent i Local Government Chronicle Independent Materials Recycling Week Daily Mirror Motorboats Monthly The Sun Municipal Journal The Times Regeneration & Renewal New Statesman New Scientist PR Week Planning Private Eye Recycling and Waste World Utility Week Resource Management and Recovery Reuters New Civil Engineer APPENDIX 2 – PRESS MONITORING (NATIONAL KEY WORDS) Keyword Keyword Description Agriculture - Environment Important mentions of farming or agriculture ICW the environment. Carbon Emissions All mentions of carbon emissions OICW climate change, global warming etc. Climate Change All mentions of climate change. Coastal Erosion All mentions of coastal erosion. DEFRA All mentions of Department for Environment, Food and Rural Affairs (DEFRA). Department of Energy & Climate All mentions of the Department of Energy & Climate Change Change (DECC) Drought Main focus mentions of droughts in the UK Environment All mentions of environmental issues Environment - Emissions Important mentions of emissions and their effect on the environment. Environment Agency All mentions of the Environment Agency. Fishing All mentions of fishing ICW the environment. Flooding - Environmental Impact Important Mentions of floods OICW effects on the environment and homes Fly Tipping All mentions of fly tipping Hosepipes All mentions of hosepipes Nuclear Power - Environmental Main focus mentions of environmental effects of nuclear power. -

United Kingdom Distribution Points

United Kingdom Distribution to national, regional and trade media, including national and regional newspapers, radio and television stations, through proprietary and news agency network of The Press Association (PA). In addition, the circuit features the following complimentary added-value services: . Posting to online services and portals with a complimentary ReleaseWatch report. Coverage on PR Newswire for Journalists, PR Newswire's media-only website and custom push email service reaching over 100,000 registered journalists from 140 countries and in 17 different languages. Distribution of listed company news to financial professionals around the world via Thomson Reuters, Bloomberg and proprietary networks. Releases are translated and distributed in English via PA. 3,298 Points Country Media Point Media Type United Adones Blogger Kingdom United Airlines Angel Blogger Kingdom United Alien Prequel News Blog Blogger Kingdom United Beauty & Fashion World Blogger Kingdom United BellaBacchante Blogger Kingdom United Blog Me Beautiful Blogger Kingdom United BrandFixion Blogger Kingdom United Car Design News Blogger Kingdom United Corp Websites Blogger Kingdom United Create MILK Blogger Kingdom United Diamond Lounge Blogger Kingdom United Drink Brands.com Blogger Kingdom United English News Blogger Kingdom United ExchangeWire.com Blogger Kingdom United Finacial Times Blogger Kingdom United gabrielleteare.com/blog Blogger Kingdom United girlsngadgets.com Blogger Kingdom United Gizable Blogger Kingdom United http://clashcityrocker.blogg.no Blogger -

Completed Acquisition by Global Radio Uk Ltd of Gcap Media Plc

COMPLETED ACQUISITION BY GLOBAL RADIO UK LTD OF GCAP MEDIA PLC UNDERTAKINGS TO BE GIVEN BY GLOBAL RADIO UK LTD TO THE OFFICE OF FAIR TRADING PURSUANT TO SECTION 73 OF THE ENTERPRISE ACT 2002 WHEREAS: (a) On 6 June 2008 Global acquired GCAP; (b) It appears to the OFT that, as a consequence of that transaction, a relevant merger situation has been created in the UK; (c) The OFT has a duty to refer a completed merger to the CC for further investigation where it believes that it is or may be the case that the creation of that merger situation has resulted or may be expected to result in a substantial lessening of competition within any market or markets in the UK for goods or services; (d) Under section 73 of the Act the OFT may, instead of making such a reference and for the purpose of remedying, mitigating or preventing the substantial lessening of competition concerned or any adverse effect which may be expected to result from it, accept undertakings to take such action as it considers appropriate, from such of the parties concerned as it considers appropriate, in particular having regard to the need to achieve as comprehensive a solution as is reasonable and practicable to the substantial lessening of competition and any adverse effects resulting from it; (e) The OFT considers that, in the absence of appropriate undertakings, it would be under a duty to refer the acquisition of GCAP to the CC; and (f) The OFT further considers that the undertakings given below by Global are appropriate to remedy, mitigate or prevent the substantial lessening of competition, or any adverse effect which has or may have resulted from it, or may be expected to result from it, as specified in the Decision. -

Bernard Magee's Acol Bidding Quiz

Number: 172 UK £3.95 Europe €5.00 April 2017 Bernard Magee’s Acol Bidding Quiz This month we are dealing with responding to an opening one-level bid. You are West in the auctions BRIDGEbelow, playing ‘Standard Acol’ with a weak no-trump (12-14 points) and four-card majors. 1. Dealer East. Love All. 4. Dealer East. Love All. 7. Dealer East. Love All. 10. Dealer East. N/S Game. ♠ K 6 3 ♠ A K Q J 10 4 ♠ A K 7 6 ♠ K Q 7 5 4 ♥ ♥ ♥ ♥ Q 4 2 N 8 N 5 N A 4 3 N ♦ 8 7 6 W E ♦ K 9 4 W E ♦ 6 3 W E ♦ K 6 4 2 W E ♣ K Q 8 6 S ♣ 6 5 3 S ♣ A Q 8 6 5 4 S ♣ 2 S West North East South West North East South West North East South West North East South 1♣ Pass 1♦ Pass 1♥ Pass 1♠ Pass ? ? ? ? 2. Dealer East. Love All. 5. Dealer East. Love All. 8. Dealer East. Love All. 11. Dealer East. N/S Game. ♠ 9 8 7 6 5 ♠ A 8 7 ♠ 8 4 ♠ 7 6 ♥ K 4 3 N ♥ 8 2 N ♥ K 9 4 N ♥ Q J 2 N W E W E W E W E ♦ J 8 3 2 ♦ A Q 8 4 2 ♦ A 7 6 5 2 ♦ 7 S S S S ♣ 4 ♣ K 3 2 ♣ 8 4 3 ♣ A 8 7 6 5 4 3 West North East South West North East South West North East South West North East South 1♣ Pass 1♦ Pass 1♥ Pass 1♠ Pass ? ? ? ? 3. -

Digital One’S Response to the Ofcom Consultation “Future Pricing of Spectrum Used for Terrestrial Broadcasting”

Digital One’s Response to the Ofcom Consultation “Future pricing of spectrum used for terrestrial broadcasting” 1. Digital One operates the UK’s only national commercial DAB digital radio multiplex. Its shareholders are GCap Media (63%) and Arqiva (37%). Digital One’s transmission network (which is operated by Arqiva) is the world’s biggest DAB digital radio network with coverage well in excess of 85% of the British population. Digital One’s multiplex broadcasts: - the three INRs (Classic FM, Virgin Radio and talkSPORT); - four digital-only national stations (Capital Life, Core, Oneword and Planet Rock) with a further station being launched in the next few months; - TV channels and an Electronic Programme Guide broadcast as part of BT Movio. Digital One is a leading stakeholder in the UK’s Digital Radio Development Bureau and the WorldDAB Forum (which is responsible for the DAB digital radio standard and works to coordinate the international roll-out of Eureka 147 based technologies). 2. Digital One is licensed under the 1996 Broadcasting Act, and has licence obligations which help deliver public policy benefits. These limit Digital One’s ability to use the spectrum it has been allocated in the most efficient manner (in economic terms). For example: - the obligation to operate a transmitter network which delivers high population coverage; - the obligation (at the direction of the Secretary of State for the Department of Culture, Media and Sport) to carry the three INRs and to offer each INR an amount of capacity dictated by the regulator; -

Houndsgate 30/34 Hounds Gate | Nottingham | NG1 7AB Gva.Co.Uk/3144 M6

City Centre Office Investment HOUNDSGATE 30/34 Hounds Gate | Nottingham | NG1 7AB gva.co.uk/3144 M6 HULL M6 M62 M62 M18 VICTORIA BUS M180 STATION MANCHESTER A60 THE M57 NOTTINGHAM TRENT HOUNDSGATE A1(M) UNIVERSITY A15 SHEFFIELD Glasshouse St City Centre M56 A60 M1 THEATRE VICTORIA Office Investment CENTRE ROYAL Lower Parliment St A610 Derby Rd A60 Upper Parliment St Huntingdon St A60 MANSFIELD A16 A60 A17NOTTINGHAM COUNCIL HOUSE M1 A46 PLAYHOUSE OLD MARKET SQ STOKE- Fletcher Gate NATIONAL ON-TRENON-TRENTT ICE CENTRE Hounds Gate & TRENT FM DERBDERBYY ARENA A50 NOTTINGHAM Maid Marian Way A60 MARKS & THE LACE A1 SPENCER MARKET A60 Hounds Gate Bellar Gate A6008 A612 M6 A38 A46 Castle Gate A42 Middle Hill NORWICH BROADMARSH SHOPPING A47 A612 NOTTINGHAM CENTRE A47 LEICESTER CASTLE M42 M54 Castle Rd A47 A6008 M6 Toll A47 A6008 BUS STATION Canal St M69 A6 L M6 Canal St CANA A11 M1 Castle Blvd A60 M6 A6005 A140 A43 A1(M) Station St BIRMINGHAM A10 London Rd A453 ION A14 WAY STAT M42 COVENTRY A43 Wilford Rd RAIL A11 M40 NORTHAMPTON A14 Queens Rd A12 A14 A6019 A14 A428 A46 M1 A11 IPSWICH M5 A43Location M11 M40 Nottingham is regarded as the regional capital of the East MidlandsCOLCHESTER and is located M50 A5 approximatelyMILTON 203 km (126 miles)A1(M) north of London, 26 km (16 miles) to the north east ofKEYNES Derby and 48 km (30 miles) north of Leicester.A10 The city has excellentLUTO communicationN links being situated directly east of the M1 A41 A12 OXFORDOXFORD Motorway (with Junctions 24 to 26 serving the city), providing access from north to GLOUCESTER M1 M11 south, with the A52 providing direct links to Derby to the east and Grantham to the west. -

Classic FM Relocates

Classic FM Relocates Lawrie Hallett MIBS reports on Classic FM’s move last year to GCAP’s London Radio Centre. Classic FM’s production studio at Leicester Square n 9 May 2006 the UK’s two largest only when this rival group was unable to June/July 1999 edition of Line Up.) commercial radio companies – the raise the considerable pre-launch capital Classic FM enhanced its presence on O Capital Radio Group and the GWR needed for its proposed service that the FM (it now has 42 transmitters across the Group – completed their merger to form contract was awarded instead to Classic FM country) as well as raising its profile GCap Media plc. Soon after its formation, as the runner-up in the contest. through involvement in the ‘Digital 1’ and doubtless recognising the potential cost Once it had the green-light, Classic FM national DAB multiplex. It has also savings and operational synergies which wasted little time in getting on-air in 1993, broadcast via the Sky satellite TV system should arise, it was decided to consolidate and its transmitter network quickly since 1999 and the same service is available the London departments under a single expanded to cover 82% of the total on Virgin’s digital cable system, the Tiscali roof. The chosen location was what had population – just over the 80% required by (formerly Home Choice) network and, of been the Capital Group’s Leicester Square the INR1 licence. The old GWR Group had course, via the Internet. headquarters, so the former GWR broadcast provided technical expertise and support stations as well as a newly combined for the fledgling national broadcaster, and in Location, Location, Location national sales team have all taken up 1997 it bought out the entire company. -

Radio Evolution: Conference Proceedings September, 14-16, 2011, Braga, University of Minho: Communication and Society Research Centre ISBN 978-989-97244-9-5

Oliveira, M.; Portela, P. & Santos, L.A. (eds.) (2012) Radio Evolution: Conference Proceedings September, 14-16, 2011, Braga, University of Minho: Communication and Society Research Centre ISBN 978-989-97244-9-5 Live and local no more? Listening communities and globalising trends in the ownership and production of local radio 1 GUY STARKEY University of Sunderland [email protected] Abstract: This paper considers the trend in the United Kingdom and elsewhere in the world for locally- owned, locally-originated and locally-accountable commercial radio stations to fall into the hands of national and even international media groups that disadvantage the communities from which they seek to profit, by removing from them a means of cultural expression. In essence, localness in local radio is an endangered species, even though it is a relatively recent phenomenon. Lighter- touch regulation also means increasing automation, so live presentation is under threat, too. By tracing the early development of local radio through ideologically-charged debates around public-service broadcasting and the fitness of the private sector to exploit scarce resources, to present-day digital environments in which traditional rationales for regulation on ownership and content have become increasingly challenged, the paper also speculates on future developments in local radio. The paper situates developments in the radio industry within wider contexts in the rapidly-evolving, post-McLuhan mediatised world of the twenty-first century. It draws on research carried out between July 2009 and January 2011for the new book, Local Radio, Going Global, published in December 2011 by Palgrave Macmillan. Keywords: radio, local, public service broadcasting, community radio Introduction: distinctiveness and homogenisation This paper is mainly concerned with the rise and fall of localness in local radio in a single country, the United Kingdom. -

Hallett Arendt Rajar Topline Results - Wave 1 2020/Last Published Data

HALLETT ARENDT RAJAR TOPLINE RESULTS - WAVE 1 2020/LAST PUBLISHED DATA Population 15+ Change Weekly Reach 000's Change Weekly Reach % Total Hours 000's Change Average Hours Market Share STATION/GROUP Last Pub W1 2020 000's % Last Pub W1 2020 000's % Last Pub W1 2020 Last Pub W1 2020 000's % Last Pub W1 2020 Last Pub W1 2020 Bauer Radio - Total 55032 55032 0 0% 18160 17986 -174 -1% 33% 33% 155537 154249 -1288 -1% 8.6 8.6 15.9% 15.7% Absolute Radio Network 55032 55032 0 0% 4908 4716 -192 -4% 9% 9% 34837 33647 -1190 -3% 7.1 7.1 3.6% 3.4% Absolute Radio 55032 55032 0 0% 2309 2416 107 5% 4% 4% 16739 18365 1626 10% 7.3 7.6 1.7% 1.9% Absolute Radio (London) 12260 12260 0 0% 715 743 28 4% 6% 6% 5344 5586 242 5% 7.5 7.5 2.7% 2.8% Absolute Radio 60s 55032 55032 0 0% 136 119 -17 -13% *% *% 359 345 -14 -4% 2.6 2.9 *% *% Absolute Radio 70s 55032 55032 0 0% 212 230 18 8% *% *% 804 867 63 8% 3.8 3.8 0.1% 0.1% Absolute 80s 55032 55032 0 0% 1420 1459 39 3% 3% 3% 7020 7088 68 1% 4.9 4.9 0.7% 0.7% Absolute Radio 90s 55032 55032 0 0% 851 837 -14 -2% 2% 2% 3518 3593 75 2% 4.1 4.3 0.4% 0.4% Absolute Radio 00s 55032 55032 0 0% 217 186 -31 -14% *% *% 584 540 -44 -8% 2.7 2.9 0.1% 0.1% Absolute Radio Classic Rock 55032 55032 0 0% 740 813 73 10% 1% 1% 4028 4209 181 4% 5.4 5.2 0.4% 0.4% Hits Radio Brand 55032 55032 0 0% 6657 6619 -38 -1% 12% 12% 52607 52863 256 0% 7.9 8.0 5.4% 5.4% Greatest Hits Network 55032 55032 0 0% 1264 1295 31 2% 2% 2% 9347 10538 1191 13% 7.4 8.1 1.0% 1.1% Greatest Hits Radio 55032 55032 0 0% 845 892 47 6% 2% 2% 6449 7146 697 11% 7.6 8.0 0.7% -

Radio – Preparing for the Future Phase 1: Developing a New Framework

Radio – Preparing for the future Phase 1: Developing a new framework Appendix B: Results of audience research Research Study conducted by MORI on behalf of Ofcom Radio – Preparing for the future Contents Section B1 Executive summary B2 Background and objectives B3 The role of radio B4 Current trends in radio listening Radio listening Popular stations Frequency of listening Listening patterns Importance of radio services Developments in radio technology B5 Localness and local radio What is localness? Which media do people think of as local? What do people need / want to know about their local area? How ‘local’ does radio need to be? Reactions to community radio Key times for local coverage Location of news compilation Importance of radio coverage of local issues Satisfaction with services Improvements to local radio B6 Digital radio Awareness of digital radio and DAB Barriers to adoption Digital radio platforms DAB user's experiences The future of DAB B7 Nations and Regions – key differences Annexes Segmentation analysis Statistical reliability Definition of social grades Appendix B: Results of audience research B1 Executive Summary Key Questions Ofcom commissioned MORI to inform three key topic areas of Ofcom’s Radio Review. The key questions within each topic area are summarised below: • Current Trends - the role of radio in people’s lives; - to understand listening patterns, such as where radio users listen, what they listen to and when they listen; and - audience perceptions of current radio provision including satisfaction levels and possible improvements. • Localness - to understand the importance of localness to listeners – and how they define the concept; - the role of radio in the provision of localness versus other media; - audience satisfaction with current local radio services; and - thoughts on specific issues such as news compilation and location of local stations. -

Bauer Media Group Phase 1 Decision

Completed acquisitions by Bauer Media Group of certain businesses of Celador Entertainment Limited, Lincs FM Group Limited and Wireless Group Limited, as well as the entire business of UKRD Group Limited Decision on relevant merger situation and substantial lessening of competition ME/6809/19; ME/6810/19; ME/6811/19; and ME/6812/19 The CMA’s decision on reference under section 22(1) of the Enterprise Act 2002 given on 24 July 2019. Full text of the decision published on 30 August 2019. Please note that [] indicates figures or text which have been deleted or replaced in ranges at the request of the parties or third parties for reasons of commercial confidentiality. SUMMARY 1. Between 31 January 2019 and 31 March 2019 Heinrich Bauer Verlag KG (trading as Bauer Media Group (Bauer)), through subsidiaries, bought: (a) From Celador Entertainment Limited (Celador), 16 local radio stations and associated local FM radio licences (the Celador Acquisition); (b) From Lincs FM Group Limited (Lincs), nine local radio stations and associated local FM radio licences, a [] interest in an additional local radio station and associated licences, and interests in the Lincolnshire [] and Suffolk [] digital multiplexes (the Lincs Acquisition); (c) From The Wireless Group Limited (Wireless), 12 local radio stations and associated local FM radio licences, as well as digital multiplexes in Stoke, Swansea and Bradford (the Wireless Acquisition); and (d) The entire issued share capital of UKRD Group Limited (UKRD) and all of UKRD’s assets, namely ten local radio stations and the associated local 1 FM radio licences, interests in local multiplexes, and UKRD’s 50% interest in First Radio Sales (FRS) (the UKRD Acquisition).