Standard Operating Procedures

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

$Iwhu Gd\V ,Qgld Rshqv Zlwk Fdxwlrq

# ) A) 5 ? 7 7 7 VRGR $"#(!#1')VCEBRS WWT!Pa!RT%&!$"#1$# 9+;)9':& 640 0',-,0- 1 &0( !! /'0(2 !3 ? D 6@38/ 334?@6B)EB@03B6 06544?)*E38 546!60B3@+ ,!@?6,!0,34+* 5*+3+* F@)4)@53)64?@6B4 3@))@046F *3B!*?0* B!358*! 54!*503 !E54*,5F$E+5 6B 5%)8 1:<99: 1:: C 4 # 3# /2/2< 6 = #+ ,"",$#!-#,.###-/-%/((-0- Q L . 4* R M "" 34+546! L M R n a major development, ILieutenant Governor of 60B3@+ The HC bench had held detailed and exhaustive and Delhi Anil Baijal on Monday that there has been an ‘error’ in once it finds from records that overruled the two controversial he Lucknow bench of the the evaluation of question certain questions and answers orders of the AAP Government ! TAllahabad High Court on paper. In its appeals, the ERA were false and ambiguous, it — to reserve Delhi Monday reserved its order on pleaded that the single-bench could not shut its eyes,” argued Government-run and private ! three special pleas of the UP order was not sustainable as it the senior lawyers. hospitals in the national Capital # government challenging the did not consider the preliminary Taking up the written sub- for only Delhiites, and allowing $% O stay on the appointment of objection of maintainability in mission of Mishra, the division Covid-19 test of only sympto- 69,000 assistant basic teachers the right perspective as the writ bench directed other senior matic patients — terming that in the state. petitions were not maintainable lawyers to submit their sub- the City Government order '( The matter was heard by a because the petitioners had not missions on behalf of their were in contravention of the division bench of Justices PK arrayed all candidates who had clients by 10 am on Tuesday. -

Cachar District

[TO BE PUBLISHED IN THE GAZETTE OF INDIA, EXTRAORDINARY, PART II SECTION 3, SUB SECTION (II)] GOVERNMENT OF INDIA MINISTRY OF FINANCE (DEPARTMENT OF REVENUE) Notification No. 45/2010 - CUSTOMS (N.T.) 4th JUNE, 2010. 14 JYESTHA, 1932 (SAKA) S.O. 1322 (E). - In exercise of the powers conferred by clauses (b) and (c) of section 7 of the Customs Act, 1962 (52 of 1962), the Central Government hereby makes the following further amendment(s) in the notification of the Government of India in the Ministry of Finance (Department of Revenue), No. 63/94-Customs (NT) ,dated the 21st November, 1994, namely:- In the said notification, for the Table, the following Table shall be substituted, namely;- TABLE S. Land Land Customs Routes No. Frontiers Stations (1) (2) (3) (4) 1. Afghanistan (1) Amritsar Ferozepur-Amritsar Railway Line (via Railway Station Pakistan) (2) Delhi Railway Ferozepur-Delhi Railway Line. Station 2. Bangladesh CALCUTTA AND HOWRAH AREA (1) Chitpur (a) The Sealdah-Poradah Railway Line Railway Station passing through Gede Railway Station and Dhaniaghat and the Calcutta-Khulna Railway line River Station. passing through Bongaon (b) The Sealdah-Lalgola Railway line (c) River routes from Calcutta to Bangladesh via Beharikhal. (2) Jagannathghat The river routes from Calcutta to Steamer Station Bangladesh via Beharikhal. and Rajaghat (3) T.T. Shed The river routes from Calcutta to (Kidderpore) Bangladesh via Beharikhal. CACHAR DISTRICT (4) Karimganj (a) Kusiyara river Ferry Station (b) Longai river (c) Surma river (5) Karimganj (a) Kusiyara river Steamerghat (b) Surma river (c) Longai river (6) Mahisasan Railway line from Karimganj to Latu Railway Station Railway Station (7) Silchar R.M.S. -

Conservation Status of Bengal Florican Houbaropsis Bengalensis

Cibtech Journal of Zoology ISSN: 2319–3883 (Online) An Online International Journal Available at http://www.cibtech.org/cjz.htm 2013 Vol. 2 (1) January-April, pp.61-69/Harish Kumar Research Article CONSERVATION STATUS OF BENGAL FLORICAN HOUBAROPSIS BENGALENSIS IN DUDWA TIGER RESERVE, UTTAR PRADESH, INDIA *Harish Kumar WWF-India, Dehradun Program Office, 32-1/72 Pine Hall School Lane, Rajpur Road, Dehradun, Uttarakhand-248001. *Author for Correspondence ABSTRACT Surveys for Bengal Florican were conducted in 2000 and 2001to assess the status and distribution of the species in Dudhwa National Park and Kishanpur WLS. The different grasslands were surveyed and from 26 different grassland sites 36 floricans were recorded. Males were most of the time in display and females were recorded from four different grasslands walking in Saccharum narenga and Sachharum sponteneum grass patches. The present study also recorded 36 different individuals thus a population of 72 floricans in the Dudwa Tiger Reserve The grasslands in Dudhwa after burning practices provides a good display ground for the floricans and a mosaic of upland grasslands Impreta cylindrica – Sacchrum spontaneum and low land Sacchrum narenga – Themeda arundancea provides ideal habitat for floricans in the Dudhwa NP and Kishanpur WLS. INTRODUCTION The Bengal Florican, Houbaropsis bengalensis (Gmelin 1789) is identified as critically endangered among the bustards by IUCN and global population is estimated at fewer than 400 individuals in the Indian subcontinent (Anon 2011). The Bengal Florican is listed in the Schedule I of the Indian Wildlife Protection Act. Distributed in the subcontinent in Assam, Bangladesh, Bhutan, Nepal, West Bengal and the terai of Bihar and Uttar Pradesh (Ali and Ripley 1987), it is now considered one of the most endangered bustards of the world. -

LCS Gauriphanta LCS Nepalganj Road Promoted to Supdt. & Joined

HISTORY OF POSTING OF SUPERINTENDENTS OF CUS (P) LUCKNOW AS ON DATE Name of the Date of HOP Sl. officer DOB Joining in No. Formation From To (S/Shri) Customs Central Excise ,Sitapur 15.09.86 05.04.89 Central Excise Div. Gorakhpur 06.04.89 13.07.90 Customs (P) Div. Gorakhpur 13.07.90 05.06.92 Customs CMPU Nichlaul 16.09.92 06.05.94 LCS Gauriphanta 07.05.94 26.07.95 Central Excise Div. Gorakhpur 27.07.95 17.11.95 (Range Salempur) DRI Gorakhpur 18.11.95 30.10.98 Central Excise Div., Faizabad 31.10.98 11.06.99 Customs (P) Hq Lucknow 12.06.99 01.08.99 Customs (P) Circle, Pithoragarh 02.08.99 04.05.2000 Customs (P) Circle, Azamgarh 05.05.2000 23.03.01 Achal Kr. Customs (P) Div. Gorakhpur 24.03.01 30.06.03 1 03.09.60 03.04.13 Agarwal Promoted to Supdt. & joined on 24.09.02 Customs (P) Div., Bareilly 01.07.03 18.12.03 Customs (P) Div., Gorakhpur 19.12.03 13.06.05 Central Excise HQ Allahabad 14.06.05 31.05.07 Central Excise Div., Gorakhpur 01.06.07 12.05.11 Central Excise Range, Basti 13.05.11 02.04.13 Posting in Customs during Current tenure Customs (P) Hq Lucknow 03.04.13 10.05.13 MPP Nichlaul 11.05.13 19.05.14 LCS Nepalganj Road 20.05.14 20.05.16 Customs (P) Circle, Behraich 21.05.16 26.07.16 Customs (P) Hq Lucknow (Prev.) 27.07.16 31.07.17 Customs (P) Div., Gorakhpur 01.08.17 till date Customs (P) Lucknow (As Insp) Jan'94 June'98 Promoted as Superintendent R-Deoria,C.Ex. -

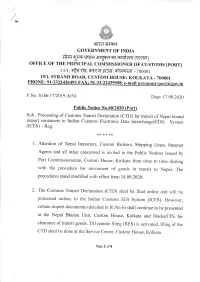

(CTD) for Transit of Nepal Bound Import Container in Indian Custom

.\ ,( ,;i i*-ii:::. il.t(:i' \\ . li:ll' '' "1'Y", :"&:t.:^'l:*,w-'',"1 -'rukt/ u- ",, f?\ ' ;"'r- ETITflH{frR GOVERNMENT OF INDIA €rfi r gffi TtrFI Jryf, 6r fl-qlilq trral OFFICE OF THB PRINCIPAL COMMISSIONER OF CUSTOMS [PORTI r 5 I t,FF ltE, mErr St r{r: mtf,firdT - 70000 1 l5ll, STRAND ROAD, cusroM HousE: KOLKATA - 700001 PHONE : 91-3322436493 FAX; 9I-33-22435998. e-mail [email protected] F.No. S 186-1712019 A(N) Date: 17 "09.202A Public Notice No.60/2020 (port) Sub : Processing of Customs Transit Declaration (CTD) for transit of Nepal bound import containers in Indian Customs Electronic Data Interchange(EDl) System (ICES) - Res. ** ** ** 1. Attention of Nepal Importers, Custom Brokers, Shipping Lines, Steamer Agents and all other concerned is invited to the Public Notices issued by Port Commissionerate, Custom House, Kolkata from time to time dealing with the procedure for movement of goods in transit to Nepal. The procedures stand modified with effect from 19.09.2020. 2. The Customs Transit Declaration (CTD) shall be filed online and will be processed online, in the Indian Customs EDI System (ICES). However, certain import documents (detailed in S1.No.6) shall continue to be presented at the Nepal Bhutan Unit, Custom House, Kolkata and Docks/CFS for clearance of transit goods. Till remote filing (RES) is activated, filing of the crD shall be done at the Service centre, custom House, Kolkata. Page 1 of 8 .t 3. : Shipping Lines/ Agent should Y / register themselves in ICES. No re-registration is required for those Shipping Lines/ Agent, who have already registered themselves in the ICES. -

Village Survey Monograph No-II, Village Bankati, Part VI, Vol-XV

CENSUS OF INDIA 1961 VOLUME XV UTT AR PRADESH PART VI VILLAGE SURVEY MONOGRAPH No. 11 General Editor P. P. BHATNAGAR 0/ t~ Indian Adminirtrative Service Superintendent 0/ Census Operati~ Uttar Pradesh VILLAGE BANKATI (TAHSIL NIGHASAN, DISTRICT KHERI) BY, R. C. SHARMA, M. A. 0/ the Uttar Pradesh Civil Service Deputy Superintendent 0/ Census Operations CENSUS OF INDIA, 1961 Central Government Publications Census Report, Volume XV-Uttar Pradesh is published in the following parts: I-A(i-ii) General Report. I-B Report on Vital Statistics. I-C(i-vi) Subsidiary Tables (in 6 books). II-A General Population Tables. II-B(i-vi) General Economic Tables (in 6 books). II-C(i-v'i) Cultural and Migration Tables (in 6 books). III-A Household Economic 'rabies. III-B Household Economic Tables (concluded). IV-A Report on Housing and Establishments and Housing' and Establishment Tables (E-seties Tables---except E-I1n. IV-B Housing and Establishment Tables (E-III). V-A Special Tables for Scheduled Castes. V-B Reprints from old Census Reports and Ethnographic Notes. VI Village Survey Monographs (Monograph~'on selected Villages). VII-A Handicraft Survey Reports. VII-B Fairs and Festivals in Uttar Pradesh. VIII-A Administration Report-Enumeration (for official use only). VIU-B Administration Report-Tabulation (for official use only). IX Census Atlas of Uttar Pradesp. X Special Report on Kanpur. State Government Publications 54 Volumes of District Census Handbooks. CONT.ENTS Page Foreword i Preface v I. The Village 1 II. The People and their Material Equipment 4 III. Economy 15 IV. Social and Cultural Life 27 V. -

Page 1 Front Front 09.Qxd

y k y cm VOLUME 10, ISSUE 132 | www.orissapost.com BHUBANESWAR | WEDNESDAY, AUGUST 12 | 2020 12 PAGES | `4.00 y k my c SHAWN ASHMORE JOINS ANTONIO BANDERAS TESTS WEDNESDAY | AUGUST 12 | 2020 | BHUBANESWAR THE BOYS-SEASON 2 COVID +VE ON HIS B’DAY Actor Shawn Ashmore is all set to join Actor Antonio Banderas has tested the satire superhero series, The Boys. positive for Covid-19. The Original The X-Men fame actor will be seen in Sin actor shared the health update the role of Lamplighter in the upcoming on Twitter, on the occasion of his y second season of the web show. leisure 60th birthday. k y cm FORTUNE FORECAST BHUMI BELIEVES IN Jacqueline misses her family MUMBAI: Actress Jacqueline Fernandez is spend- my loved ones through the day. I’m terribly miss- ing her birthday Tuesday here all ing my family back home so spending quality time alone, and she sure is miss- with them would be the best thing for me,” she said. ARIES REPEATING CLOTHES ing her family. “But given the situation we are all in now, You will be resolute and “This year there we will make do with video calls. Hopefully, unswerving in your work MUMBAI: Actress people might see me wearing the are no celebra- will be able to hug my parents and sib- today. By afternoon, Bhumi Pednekar be- same clothes because as an actress tory birthday lings super soon,” she added. you'll see results. Love lieves in repeating her you are told to wear different and plans, I will Over the years, the Sri Lankan will lighten your workload in the clothes. -

1 Village Kathera, Block Akrabad, Sasni to Nanau Road , Tehsil Koil

Format for Advertisement in Website Notice for appointment of Regular / Rural Retail Outlet Dealerships Bharat Petroleum Corporation Limited (BPCL) proposes to appoint Retail Outlet dealers in Uttar Pradesh, as per following details: Fixed Fee / Security Estimated monthly Type of Minimum Dimension (in M.)/Area of Mode of Minimum Bid Sl. No Name of location Revenue District Type of RO Category Finance to be arranged by the applicant Deposit (Rs. Sales Potential # Site* the site (in Sq. M.). * Selection amount (Rs. In In Lakhs) Lakhs) 1 2 3 4 5 6 7 8 9a 9b 10 11 12 SC, SC CC-1, SC PH ST, ST CC-1, ST PH OBC, OBC CC- CC / DC / Estimated fund Estimated working Draw of Regular / 1, OBC PH CFS required for MS+HSD in Kls Frontage Depth Area capital requirement Lots / Rural development of for operation of RO Bidding infrastructure at RO OPEN, OPEN CC- 1, OPEN CC- 2,OPEN-PH Village Kathera, Block Akrabad, Sasni to Nanau Road , Draw of 1 Tehsil Koil, Dist Aligarh ALIGARH RURAL 90 SC CFS 30 30 900 0 0 Lots 0 2 Village Dhansia, Block Jewar, Tehsil Jewar,On Jewar to GAUTAM BUDH Draw of 2 Khurja Road, dist GB Nagar NAGAR RURAL 160 SC CFS 30 30 900 0 0 Lots 0 2 Village Dewarpur Pargana & Distt. Auraiya Bidhuna Auraiya Draw of 3 Road Block BHAGYANAGAR AURAIYA RURAL 150 SC CFS 30 30 900 0 0 Lots 0 2 Village Kudarkot on Kudarkot Ruruganj Road, Block Draw of 4 AIRWAKATRA AURAIYA RURAL 100 SC CFS 30 30 900 0 0 Lots 0 2 Draw of 5 Village Behta Block Saurikh on Saurikh to Vishun Garh Road KANNAUJ RURAL 100 SC CFS 30 30 900 0 0 Lots 0 2 Draw of 6 Village Nadau, -

Integrated Law Enforcement Centres

Integrated Law Enforcement Centres A Futuristic Border Management Institution for India Santosh Mehra, IPS Additional Director General Bureau of Police Research & Development (formerly IG, BSF). 1. Introduction / Background: 1.1 The all-pervasive phenomenon of globalization across the world has posed both opportunities as well as challenges. While it enables the developing and least developed countries to ride the tide of economic openness towards greater employment, market and prosperity; it also poses threat of cross border and trans-national crimes and terrorism. Though no country can afford to ignore the benefits of globalisation as means of economic development and prosperity; its full benefit can be drawn only if proper safeguard measures are placed against its associated evils. The old institutional safeguards may not be effective and / or efficient to check the associated cross border and trans-national crimes. There is need for revisiting the existing institutional safeguards and, if required, to explore alternatives which may be sufficiently effective and efficient. 2.0 Overview: This Project Report is an attempt to assess the nature and extent of cross border and trans-national crimes on the borders of India, highlight its impact on national security, map the existing institutional arrangement in addressing them, identify the limitations in the existing set up, explore the arrangements around the globe and suggest viable short term and long term solutions for India. 1 2.1 Project Title –: Integrated Law Enforcement Centres – A Futuristic Approach for Strengthening National Security 2.2 Vision: The vision of this project report is to promote Integrated Border Management in a holistic and comprehensive manner. -

International Passenger Survey in India 2015-16

INTERNATIONAL PASSENGER SURVEY IN INDIA 2015-16 Study Commissioned by: Ministry of Tourism, Government of India Prepared by: PROF. ASHIS SENGUPTA, PRINCIPAL INVESTIGATOR & MEMBERS OF THE CORE IPS TEAM Indian Statistical Institute, Kolkata Contents Page List of Abbreviations ............................................................................................................. II Forewords ........................................................................................................................... III Executive Summary ....................................................................................................................... 3 Chapter A - Introduction Genesis of IPS ......................................................................................................................... 11 Aims and their Formalizations ............................................................................................... 15 Chapter B - Sampling Scheme & Estimation Methodology Definitions ............................................................................................................................. 19 Sampling Design ..................................................................................................................... 20 Scrutiny, Lot Quality Sampling for Error Reduction ............................................................... 23 Packages Developed and Accessed for Data and Error Analyses .......................................... 23 Chapter C - International Recommendation, Other -

Structure and Enforcement of Sales Tax in Uttar Pradesh Was Entrusted to This Institute by the Finance Department, Government of Uttar Pradesh in June 1990

STRUCTURE AND ENFORCEMENT OF SALES TAX IN UTTAR PRADESH Mahesh C Purohit Gautam Naresh O.P. Bohra March 1993 NATIONAL INSTITUTE OF PUBLIC FINANCE & POLICY NEW DELHI FOREWORD The National Institute of Public Finance and Policy is an autonomous non-profit organization whose major functions are to carry out research, undertake consultancy work and impart training in the area of public finance and policy. The study of Structure and Enforcement of Sales Tax in Uttar Pradesh was entrusted to this Institute by the Finance Department, Government of Uttar Pradesh in June 1990. The team which underlook the Study was headed by Mahesh C. Purohit. The other members of the team were: Gautam Naresh and O.P. Bohra. The study was planned and conducted by Mahesh C. Purohit. As the association of O.P. Bohra with the Study Team was for a short period, most of the field work relating to the Study was carried out by Gautam Naresh under the overall supervision, planning and guidance of the Team Leader. An interim report indicating sources of evasion of sales tax with a few major recommendations suggesting improvements in the tax system was submitted in November 1991. The Interim Report with some modifications is incorporated into relevant parts of different chapters of this Report. The Governing body of the Institute does not take responsibility for views expressed in this Report- The responsibility belongs to the staff of the Institute and more particularly to the authors of the Report. Raja J. Chelliah Chairm an M arch, 1993 PREFACE As in all the other States, in Uttar Pradesh too sales tax has been buoyant and yielding larger resources during the successive Plans. -

Support Structures and Services in Delhi-NCR, Uttar Pradesh and Haryana Disclaimer

Helping Victims become Survivors: A Resource Directory of Support Structures and Services in Delhi-NCR, Uttar Pradesh and Haryana Disclaimer This report was funded by The Asia Foundation. The views expressed in this report do not necessarily reflect those of the funders or The Asia Foundation. The information provided in this Resource Directory has been collected from various sources including websites, telephonic interviews, face to face meetings and internet searches. While all efforts have been made to verify the particulars provided in the Directory, mistakes arising out of human error cannot be ruled out. The addresses of offices of Government departments, telephone numbers, email IDs and activities change from time to time. WPC does not take responsibility for any inadvertent errors. Helping Victims become Survivors: A Resource Directory of Support Structures and Services in Delhi-NCR, Uttar Pradesh and Haryana Contents List of Abbreviations .................................................................................................................................v About WomenPowerConnect (WPC) .....................................................................................................vi About The Asia Foundation ...................................................................................................................vii Foreword .................................................................................................................................................viii Acknowledgments ...................................................................................................................................ix