Spark Starts Here

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Danone Premium Review 2013 V2

Pierre-André Terisse Chief Financial Officer Société Générale – The Premium Review Paris – December 4 th , 2013 Disclaimer This document contains certain forward-looking statements concerning DANONE. Although DANONE believes its expectations are based on reasonable assumptions, these forward-looking statements are subject to numerous risks and uncertainties, which could cause actual results to differ materially from those anticipated in these forward-looking statements. For a detailed description of these risks and uncertainties, please refer to the section “Risk Factors” in DANONE’s Annual Report (which is available on www.danone.com). DANONE undertakes no obligation to publicly update or revise any of these forward-looking statements. This document does not constitute an offer to sell, or a solicitation of an offer to buy, Danone shares. 2 A unique model of development 3 Our priorities today Europe Adapt & fix Growth markets Invest & leverage 2 tier momentum 9M sales growth : +5.5% 9M 2013 Sales figures Growth Markets Sales breakdown Europe Sales Sales 10.1 bn 38% 6.2 bn +11.7% like-for-like (1) 62% -3.0% like-for-like (1) (1) Like-for-like : Based on constant scope of consolidation and constant exchange rates 555 Q3 2013 : Strong underlying dynamics impacted however by the Fonterra crisis Clear priorities Strong underlying growth trends H1 2012 H2 2012 H1 2013 Q3 2013 Europe (1.7)% (4.5)% (4.0)% (0.9)% Europe : Adapt & fix – Savings & competitiveness CIS & 11,1% 8,2% 9,3% – Value for consumers NORAM 5,3% H1 2012 H2 2012 H1 2013 Q3 -

Moment of Truth

COUNTDOWN MOMENTTO EXTINCTIONOF WILL GLOBALTRUTH BRANDS CLEAN UP THE PALM OIL TRADE BEFORE 2020? TIME FOR BRANDS TO COME CLEAN ABOUT THEIR LINKS TO FOREST DESTRUCTION FOR PALM OIL A FROM? COMES PALM OIL WHO THEIR DISCLOSE BRANDS WHICH TRADERS/ SUPPLIERS MILLS/ PRODUCERS 100% CLEAN PALM OIL CONTENTS CRUNCH TIME FOR CLIMATE COMMITMENTS 1 THE HIGH PRICE OF CHEAP PALM OIL 5 ARE CORPORATE COMMITMENTS MORE THAN HOT AIR? 9 HOW TRADERS SCORED ON NDPE IMPLEMENTATION 11 BRANDS ADMIT LINKS TO RAINFOREST DESTRUCTION 12 CONFRONTING THE BRANDS WITH EVIDENCE 15 HOW CONSUMER BRANDS ARE LINKED TO FOREST DESTROYERS 16 FELDA/FELDA GLOBAL VENTURES (FGV) 18 SALIM GROUP 20 SAMLING GROUP 22 TIME FOR ACTION 24 BRANDS MUST DISCLOSE WHERE THEIR PALM OIL COMES FROM... 26 ...AND TAKE CONTROL OF THEIR SUPPLY CHAINS 27 COUNTDOWN TO 2020 29 DEMANDS 31 APPENDIX 1: HOW COMPANIES PERFORM ON TRANSPARENCY 32 APPENDIX 2: LITERATURE REVIEW 42 ENDNOTES 48 REFERENCES 52 ‘ Whilst the causes of deforestation are complex, it is generally acknowledged that the biggest drivers are the cultivation of soya and palm oil, logging for the production of paper and board and the rearing of cattle. All of these commodities are major ingredients in the supply chains of most consumer goods companies. Our member companies drive the demand for these commodities and have an opportunity to ensure that the sourcing of these ingredients does not contribute to deforestation.’1 CONSUMER GOODS FORUM ‘The unsustainable use of natural resources has caused a dramatic decline of Bornean orangutans ... Our findings suggest that more than 100,000 individuals have been lost in the 16 years between 1999 and 2015.’2 MARIA VOIGHT, RESEARCHER AT THE MAX PLANCK INSTITUTE FOR EVOLUTIONARY ANTHROPOLOGY D 11 DECEMBER 2016, 1°3 0 46́ ̋ S 110°15 28́ ̋ E: DRONE FOOTAGE REVEALS A NEW CANAL CUTTING INTO PEATLAND FOREST FROM THE PT DAMAI AGRO SEJAHTERA (PT DAS) OIL PALM CONCESSION WITHIN THE SUNGAI PUTRI PEATLAND LANDSCAPE OF KETAPANG DISTRICT, WEST KALIMANTAN. -

Nzbpt News December 2018

Issue 10 NZBPT NEWS DECEMBER 2018 TO ADVANCE AND ENCOURAGE BUSINESS UNDERSTANDING OF PARLIAMENT AND PARLIAMENTARIANS UNDERSTANDING OF THE BUSINESS COMMUNITY OF NEW ZEALAND Lisa King, social entrepreneur, CEO and Founder of Eat My Lunch was our guest speaker at the Spring Business Overview on 7 November. Here are highlights of her inspirational story. INSIDE THIS ISSUE BUSINESS SPRING PAGE 1 - 5 Business Spring Overview OVERVIEW PAGE 6 - 7 Schools Funding CEO Visit To IPT in London New Corporate Member Lisa King, social entrepreneur, CEO and Founder of Eat My Lunch was our guest speaker at the Spring PAGE 8 - 9 Our Presenters Business Overview on 7 November. Here are highlights of her inspirational story. PAGE 10 - 11 Presidents Dinners PAGE 12 - 13 Parliamentary Seminars It had never occurred to me know that if you are hungry, that in NZ, there are kids you cannot learn. Kids cannot PAGE 14 - 15 Business Attachments going to school with no food. concentrate, participate in Of the 290,000 children class and often misbehave BACK PAGE Changes Afoot currently living in poverty in when they haven’t eaten all NZ, we estimate that there are day. Without an education, 25,000 going to school every what chance do they have of day without lunch. And we all breaking the poverty cycle? BUSINESS SPRING OVERVIEW CONTINUED... As a working mum with 2 with a few charities, I also this type of business in young kids, I didn’t know knew that a lot of time and NZ and 3 years ago, the what I as one person could resource goes into getting concept barely existed in do to help solve this issue. -

FY21 Results Overview

Annual Report 2021 01 Chorus Board and management overview 14 Management commentary 24 Financial statements 60 Governance and disclosures 92 Glossary FY21 results overview Fixed line connections1 Broadband connections1 FY21 FY20 FY21 FY20 1,340,000 1,415,000 1,180,000 1,206,000 Fibre connections1 Net profit after tax FY21 FY20 FY21 FY20 871,000 751,000 $47m $52m EBITDA2 Customer satisfaction Installation Intact FY21 FY20 FY21 FY21 $649m $648m 8.2 out of 10 7.5 out of 10 (target 8.0) (target 7.5) Dividend Employee engagement score3 FY21 FY20 FY21 FY20 25cps 24cps 8.5 out of 103 8.5 This report is dated 23 August 2021 and is signed on behalf of the Board of Chorus Limited. Patrick Strange Mark Cross Chair Chair Audit & Risk Management Committee 1 Excludes partly subsidised education connections provided as part of Chorus’ COVID-19 response. 2 Earnings before interest, income tax, depreciation and amortisation (EBITDA) is a non-GAAP profit measure. We monitor this as a key performance indicator and we believe it assists investors in assessing the performance of the core operations of our business. 3 Based on the average response to four key engagement questions. Dear investors Our focus in FY21 was to help consumers especially important because fixed wireless services don’t capitalise on the gigabit head start our fibre provide the same level of service as fibre - or even VDSL in network has given New Zealand. We knocked most cases – and these service limitations often aren’t made clear to the customer. on about a quarter of a million doors and supported our 100 or so retailers to connect As expected, other fibre companies continued to win copper customers in those areas where they have overbuilt our another 120,000 consumers to fibre. -

Annual Report

08 Annual Report iinet.net.au iiNet Limited ACN 068 628 937 ABN 48 068 628 937 Contents Financial Calendar and Corporate Information 1 About iiNet 3 iiNet History 17 Financial Highlights 19 Operational Highlights 20 Corporate Highlights 21 Education and Community Outreach 23 Chairman’s Review 25 Managing Director’s Report 29 Directors’ Report 35 Corporate Governance Statement 65 Financial Report 71 Directors’ Declaration 139 Independent Auditor’s Report 141 Shareholder Information 143 Financial Calendar Annual General Meeting The Annual General Meeting of iiNet Limited will be held at the Sheraton Hotel, 297 Adelaide Terrace, Perth, Western Australia, on Monday the 24th of November, 2008 at 10:30am. Other key dates in the 2009 financial year: • Annual report and Notice of Annual General Meeting mailed to shareholders October 2008 • Half-year results February 2009 • Full-year results August 2009 Corporate Information Directors Michael Smith Chairman Michael Malone Managing Director Andrew Milner Director (non-executive) Peter James Director (non-executive) Paul Broad Director (non-executive) Tony Grist Director (non-executive) David Grant Director (non-executive) Company Secretary David Buckingham Principal Place of Business and Registered Office iiNet Limited Durack Centre, Level 6 263 Adelaide Terrace Perth WA 6000 Share Registry Computershare Investor Services Pty Ltd Level 2 Reserve Bank Building 45 St George’s Terrace Perth WA 6000 Telephone: +61 8 9323 2000 Internet: www.computershare.com.au Stock Exchange Listings iiNet Limited’s ordinary shares are quoted on the Australian Stock Exchange Limited (ASX: IIN). Auditors Ernst & Young The Ernst & Young Building 11 Mounts Bay Road Perth WA 6000 1 iiNet Annual Report 2008 Financial Calendar and Corporate Information 2 08 About iiNet We’ve come a long way since our days of working out of a suburban garage in the early 90s. -

TPG Telecom Limited and Its Controlled Entities ABN 46 093 058 069

TPG Telecom Limited and its controlled entities ABN 46 093 058 069 Annual Report Year ended 31 July 2016 2 TPG Telecom Limited and its controlled entities Annual report For the year ended 31 July 2016 Contents Page Chairman’s letter 3 Directors’ report 5 Lead auditor’s independence declaration 34 Consolidated income statement 35 Consolidated statement of comprehensive income 36 Consolidated statement of financial position 37 Consolidated statement of changes in equity 38 Consolidated statement of cash flows 39 Notes to the consolidated financial statements 40 Directors’ declaration 91 Independent auditor’s report 92 ASX additional information 94 3 TPG Telecom Limited and its controlled entities Chairman’s letter For the year ended 31 July 2016 Dear Shareholders On behalf of the Board of Directors, I am pleased to present to you the TPG Telecom Limited Annual Report for the financial year ended 31 July 2016 (“FY16”). Financial Performance FY16 was another successful year for the Group. Continued organic growth and the integration of iiNet into the business have resulted in further increases in revenue, profits and dividends for shareholders. FY16 represents the eighth consecutive year that this has been the case. A detailed review of the Group’s operating and financial performance for the year is provided in the Operating and Financial Review section of the Directors’ Report starting on page 7 of this Annual Report, and set out below are some of the key financial highlights and earnings attributable to shareholders from the year. FY16 FY15 Movement Revenue ($m) 2,387.8 1,270.6 +88% EBITDA ($m) 849.4 484.5 +75% NPAT ($m) 379.6 224.1 +69% EPS (cents/share) 45.3 28.2 +61% Dividends (cents/share) 14.5 11.5 +26% iiNet Acquisition At the beginning of FY16 we completed the acquisition of iiNet and consequently there has been significant focus during the year on integrating the businesses to improve the efficiency of the combined organisation. -

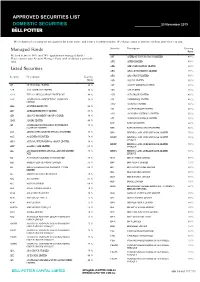

Approved Securities List

APPROVED SECURITIES LIST DOMESTIC SECURITIES 23 November 2019 The inclusion of a security on our approval list is not advice and is not a recommendation. We change ratios at any time without prior notice to you. Security Description Gearing Managed Funds Ratio We lend between 50% and 70% against most managed funds. APT AFTERPAY TOUCH GROUP LIMITED 40 % Please contact your Account Manager if you wish to discuss a particular fund. APX APPEN LIMITED 40 % Listed Securities ARB ARB CORPORATION LIMITED. 60 % ARG ARGO INVESTMENTS LIMITED 75 % Security Description Gearing ARQ ARQ GROUP LIMITED 50 % Ratio ASB AUSTAL LIMITED 50 % 3PL 3P LEARNING LIMITED.. 40 % AST AUSNET SERVICES LIMITED 65 % A2B A2B AUSTRALIA LIMITED 50 % ASX ASX LIMITED 70 % A2M THE A2 MILK COMPANY LIMITED NZ 40 % AUB AUB GROUP LIMITED 40 % AAC AUSTRALIAN AGRICULTURAL COMPANY 50 % AVJ AVJENNINGS LIMITED 40 % LIMITED. AWC ALUMINA LIMITED 70 % ABA AUSWIDE BANK LTD 40 % AX1 ACCENT GROUP LIMITED 50 % ABC ADELAIDE BRIGHTON LIMITED 65 % AYS AMAYSIM AUSTRALIA LIMITED 50 % ABP ABACUS PROPERTY GROUP STAPLED 50 % AZJ AURIZON HOLDINGS LIMITED 70 % ADH ADAIRS LIMITED 40 % BAP BAPCOR LIMITED 60 % AFI AUSTRALIAN FOUNDATION INVESTMENT 75 % COMPANY LIMITED BBN BABY BUNTING GROUP LIMITED 50 % AGI AINSWORTH GAME TECHNOLOGY LIMITED 55 % BEN BENDIGO AND ADELAIDE BANK LIMITED 70 % AGL AGL ENERGY LIMITED. 70 % BENPE BENDIGO AND ADELAIDE BANK LIMITED 70 % LPYR6UT AHG AUTOMOTIVE HOLDINGS GROUP LIMITED. 50 % BENPF BENDIGO AND ADELAIDE BANK LIMITED 70 % AHY ASALEO CARE LIMITED 65 % LPYR6UT AIA AUCKLAND INTERNATIONAL AIRPORT LIMITED 70 % BENPG BENDIGO AND ADELAIDE BANK LIMITED 70 % NZX LPYR3UT ALF AUSTRALIAN LEADERS FUND LIMITED 50 % BGA BEGA CHEESE LIMITED 60 % ALG ARDENT LEISURE GROUP LIMITED 55 % BHP BHP GROUP LIMITED 75 % ALI ARGO GLOBAL LISTED INFRASTRUCTURE 60 % BIN BINGO INDUSTRIES LIMITED 50 % LIMITED BKL BLACKMORES LIMITED 60 % ALL ARISTOCRAT LEISURE LIMITED 70 % BKW BRICKWORKS LIMITED 60 % ALQ ALS LIMITED 65 % BLD BORAL LIMITED. -

Quarterly Investment Update Antares High Growth Shares Fund – June 2021

Quarterly Investment Update Antares High Growth Shares Fund – June 2021 For adviser use only Highlights for the quarter Performance: The Fund returned 9.6% (net of fees) for the June quarter, outperforming its benchmark by 1.3%. Contributors to performance: Positive contributors – Aristocrat Leisure, Telix Pharmaceuticals, Megaport, Boral, Woodside (not owned); Negative contributors – Incitec Pivot, Qantas, ANZ, Resmed (not owned) and Altium (not owned). Stock activity: Buys/additions – Ansell, Downer and TPG Telecom ; Sells/reductions – BlueScope Steel, Boral, Endeavour Group and Worley Fund snapshot Inception date 7 December 1999 Benchmark S&P/ASX 200 Total Return Index To outperform the benchmark (after fees) over rolling Investment objective 5-year periods Investment returns as at 30 June 20211 Period 3 months 1 year 3 years pa 5 years pa 10 years pa Since inception pa Net return2 % 9.6 39.9 9.2 12.6 10.0 11.0 Gross return3 % 9.9 41.9 10.5 13.9 11.2 12.5 Benchmark return % 8.3 27.8 9.6 11.2 9.3 8.5 Net excess return % 1.3 12.1 -0.4 1.4 0.7 2.5 Gross excess return % 1.6 14.1 0.9 2.7 1.9 4.0 1 Past performance is not a reliable indicator of future performance. Returns are not guaranteed and actual returns may vary from any target returns described in this document. 2 Investment returns are based on exit prices, and are net of management fees and assume reinvestment of all distributions. Contributors to performance Pleasingly the Fund enjoyed another strong quarter, returning 9.6% (net of fees) vs the benchmark return of 8.3%. -

Bringing the Future Faster

6mm hinge Bringing the future faster. Annual Report 2019 WorldReginfo - 7329578e-d26a-4187-bd38-e4ce747199c1 Bringing the future faster Spark New Zealand Annual Report 2019 Bringing the future faster Contents Build customer intimacy We need to understand BRINGING THE FUTURE FASTER and anticipate the needs of New Zealanders, and Spark performance snapshot 4 technology enables us Chair and CEO review 6 to apply these insights Our purpose and strategy 10 to every interaction, Our performance 12 helping us serve our Our customers 14 customers better. Our products and technology 18 Read more pages 7 and 14. Our people 20 Our environmental impact 22 Our community involvement 24 Our Board 26 Our Leadership Squad 30 Our governance and risk management 32 Our suppliers 33 Leadership and Board remuneration 34 FINANCIAL STATEMENTS Financial statements 38 Notes to the financial statements 44 Independent auditor’s report 90 OTHER INFORMATION Corporate governance disclosures 95 Managing risk framework roles and 106 responsibilities Materiality assessment 107 Stakeholder engagement 108 Global Reporting Initiative (GRI) content 109 index Glossary 112 Contact details 113 This report is dated 21 August 2019 and is signed on behalf of the Board of Spark New Zealand Limited by Justine Smyth, Chair and Charles Sitch, Chair, Audit and Risk Management Committee. Justine Smyth Key Dates Annual Meeting 7 November 2019 Chair FY20 half-year results announcement 19 February 2020 FY20 year-end results announcement 26 August 2020 Charles Sitch Chair Audit and Risk Management Committee WorldReginfo - 7329578e-d26a-4187-bd38-e4ce747199c1 Create New Zealand’s premier sports streaming business Spark Sport is revolutionising how New Zealanders watch their favourite sports events. -

Paving the Way for a Truly Globa Lized Economy

WINNER OF THE NETWORK TRANSFORMATION AWARDS 2018 Paving the way for a truly globa lized economy Editorial ngena – business alliance of the 21st century Leading international telecommunication on the one hand they get a global network companies have formed the Next Genera- service which is faster to implement, highly tion Enterprise Network Alliance – ngena. secure and reliable, and more flexible and Enterprise customers benefit from network scalable than many current solutions compa- Marcus Hacke Alessandro Adriani services, realized on complementary partner nies use today; on the other hand, business networks around the globe. Established in customers profit from the local access and early 2016, ngena has seen so far 21 strong local care of regional telecommunication Dear reader, international partners around the globe joining providers. the alliance. Founded by Deutsche Telekom, Enterprises today are facing a huge range of challenges as CenturyLink, Reliance Jio and SK Telecom, the ngena – paving the way for a truly digitalization, globalization and new IT solutions call for inno- alliance has now grown to include a number of globa lized economy vative network solutions. Companies need to interconnect new telecom partners such as A1, Altice with sites and workforces around the globe with greater flexibility SFR and Portugal Telecom, British Telecom, ngena comes with a completely new and agility than ever before. New cloud-based applications China Unicom, Expereo, KPN, MTN, Neutrona, business model and a new technology in a are driving demand for greater connectivity and higher band- Starhub, Sunrise, Telus, PCCW Global, VEON greenfield setting, sharing network assets widths with premium network performance and security. -

ITW Global Leaders' Forum Demonstrates How Blockchain Can Transform Inter-Carrier Settlement

ITW Global Leaders’ Forum demonstrates how blockchain can transform inter-carrier settlement The successful Proof of Concept shows how blockchain-enabled settlement between multiple carriers can revolutionize wholesale telecoms sector by streamlining complex transactions HKT (SEHK:6823) – HONG KONG / LONDON, October 23, 2018 – ITW Global Leaders’ Forum (GLF) has announced the successful completion of a multi-lateral blockchain Proof of Concept (PoC) involving several of its members. The PoC, led by PCCW Global and Colt Technology Services, in collaboration with BT, Orange, Telefonica and Telstra, has demonstrated the viability of a platform that can settle voice transactions between multiple carriers in minutes rather than hours. The breakthrough is the latest in a series of blockchain PoCs carried out by GLF members and supported by technology partner and blockchain specialist Clear. The trial just completed is the first to involve a multi-lateral series of relationships among the wholesale telecommunications industry, and points to a future of secure and frictionless settlement across the sector. The GLF is now reviewing options around a potential governance structure to develop the technology further and implement a solution for the industry that replaces existing and cumbersome processes for settlement of voice as well as other types of transactions, examples such as mobile roaming or data on demand. Mr. Marc Halbfinger, Chief Executive Officer of PCCW Global and the Chairman of the GLF, said, “We are very pleased that this latest Proof of Concept has expanded to include more carriers. It has been a strong belief within the GLF that innovative technologies such as blockchain can be harnessed to improve the overall efficiency of the industry, and it is now clear that the industry can look forward to the benefit of becoming further aligned. -

Spark People 38 Community and Environment 40

ASX Market Announcements Australian Securities Exchange 4th Floor, 20 Bridge Street Sydney NSW 2000 Australia 21 August 2015 SPARK NEW ZEALAND LIMITED H2 FY15 RESULTS AND ANNUAL REPORT Dear Sir/Madam In accordance with ASX Listing Rules 4.3A and 4.7, I enclose the following for release to the market in relation to Spark New Zealand Limited’s H2 FY15 results: 1. Appendix 4E 2. Annual Report 3. Section 209 notice 4. Appendix 7 (NZX form) The following information will follow: 5. Appendix 3A.1 6. Corporate Governance Statement 7. Appendix 4G 8. Media release 9. Investor presentation (containing FY16 earnings and dividend guidance) 10. Detailed financial information Spark New Zealand’s Managing Director, Simon Moutter, and Chief Financial Officer, Jolie Hodson, will discuss the H2 FY15 Results at 10:00am New Zealand time today. Spark New Zealand’s 2015 Annual Report is now available at: investors.sparknz.co.nz. This announcement will also be released to the New Zealand Stock Exchange. Yours sincerely Charlotte Swan Company Secretary For personal use only Spark New Zealand Limited ARBN 050 611 277 Spark City, 167 Victoria Street West, Private Bag 92028, Auckland, New Zealand Spark New Zealand Limited Results for announcement to the market Information given to ASX under Listing Rule 4.3A. This information should be read in conjunction with Spark New Zealand Limited’s 30 June 2015 Annual Report. Reporting Period: 12 months to 30 June 2015 Previous Reporting Period: 12 months to 30 June 2014 Twelve Percentage months ended change 30 June 2015