Annual Audit Report on the Municipality of Tomas Oppus

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Pdf | 596.03 Kb

2. Drowning Incident in Southern Leyte • On or about 8:00 PM, 12 September 2012, a fisherman named Arsenio P. Boncales, 75 years old, a resident of Brgy. Bugo, Tomas Oppus, Southern Leyte went fishing and never went back home. • At around 12:00 noon, 14 September 2012, the dead body of the victim was found off the shore of Brgy. Kawayan, Libangon, Southern Leyte. 3. Flashflood in Malaybalay City, Bukidnon • At about 3:00 PM 10 September 2012, a flashflood occurred in Purok 4A Brgy Aglayan and Purok 5 Brgy Cabangahan, Malaybalay City due to heavy rains brought about by the Active Low Pressure Area (ALPA) East of Mindanao. • Fifty three (53) families were evacuated of which forty-six (46) were from Aglayan Purok 4A and seven (7) from Cabangahan Purok. • The evacuees returned to their homes after an hour when the flashflood subsided. • No casualties and damages reported. B. CASUALTIES NAME AGE ADRESS REMARKS Arsenio P. Bongcales Went fishing on September Brgy. Bugo, Tomas (previously reported as 75 14, then found dead after Oppus, Southern Leyte Juan Cabales) two days C. FLOODED AREAS (TAB A) • As of 8:00 PM, 16 September 2012, a number of Barangays in the cities of Makati, San Juan, Valenzuela, Malabon and Muntinlupa were flooded and not passable to all types of vehicles. • Areas in Region III are also reported flooded. D. AFFECTED POPULATION (As of 10:00 PM 15 September 2012) AFFECTED No. of Inside Evacuation Centers Region/Province Evacuation Mun/City Brgys Fam Persons Fam Persons Centers GRAND TOTAL 14 137 511 3 55 181 NCR 14 137 511 3 55 181 Quezon City 6 66 210 - - - San Juan City 7 40 160 1 30 70 Valenzuela City 1 31 141 2 25 111 San Fernando 4 419 1739 289 1234 • All evacuees in Quezon City returned to their homes. -

Philippines Arterial Road Link Development Project (1) (2) External Evaluator: Taro Tsubugo Field Survey: November 2004 1

Philippines Arterial Road Link Development Project (1) (2) External Evaluator: Taro Tsubugo Field Survey: November 2004 1. Project Profile and Japan’s ODA Loan Bagiuo Manila Project site Cebu City Philippines Davao Project site location map One of the arterial roads improved via the project 1.1 Background From its independence through the 1980s, the Philippines invested heavily in the expansion of road network in order to respond to a rapid increase in the number of vehicles and, inevitably, demand for road transportation. Extension of the national network of arterial roads was achieved during this period. Function and quality, however, were given a secondary consideration, which ultimately impeded the efficiency and economic effects of the country’s road infrastructure. Thus, with a view to ensure an efficient and reliable road network, qualitative improvements (i.e. increase in the paved road ratio, reconstruction from temporary bridges to permanent structures, etc.), were identified as a priority issue for the road sector in the 1990s. 1.2 Objectives This project’s objective was to increase the efficiency of road transportation on the islands of Leyte, Samar and Bohol by developing their arterial road networks, thereby contributing to regional economic stimulation and improvements in the living standards of local residents. 1.3 Borrower/Executing Agency Government of the Philippine Republic/Department of Public Works and Highways (DPWH) 1 1.4 Outline of Loan Agreement Phase 1 Phase 2 Total Loan Amount/ 11,754 million yen/ 4,765 million yen/ 16,519 million yen/ Disbursed Amount 11,752 million yen 3,846 million yen 15,598 million yen Exchange of Notes/ Nov. -

Invitation to Bid for the Concreting of Hinapu Barangay Road Tomas Oppus, Southern Leyte Contact ID # - 2021-02-17-009CW

Republic of the Philippines PROVINCE OF SOUTHERN LEYTE Maasin City Invitation to Bid for the Concreting of Hinapu Barangay Road Tomas Oppus, Southern Leyte Contact ID # - 2021-02-17-009CW 1. The Provincial Government of Southern Leyte, through the 20% EDF intends to apply the sum of P 4,923,054.38 being the Approved Budget for the Contract (ABC) to payments under the contract for the Concreting of Hinapu Barangay Road. Bids received in excess of the ABC shall be automatically rejected at bid opening. 2. The Provincial Government of Southern Leyte now invites bids for Concreting of Hinapu Barangay Road. Completion of the Works is required to be completed within 120 calendar days from the date of receipt of the Notice to Proceed. Bidders should have completed a contract within two years prior to the date of submission and receipt of bids, similar to the Project. The description of an eligible bidder is contained in the Bidding Documents, particularly, inError! Reference source not found.. 3. Bidding will be conducted through open competitive bidding procedures using non- discretionary “pass/fail” criterion as specified in the 2016 Revised Implementing Rules and Regulations (IRR) of Republic Act 9184 (RA 9184), otherwise known as the “Government Procurement Reform Act.” Bidding is restricted to Filipino citizens/sole proprietorships, cooperatives, and partnerships or organizations with at least seventy five percent (75%) interest or outstanding capital stock belonging to citizens of the Philippines. 4. Interested bidders may obtain further information from the Provincial Government of Southern Leyte and inspect the Bidding Documents at the address given below during regular office hours. -

Region VIII: Geographically Isolated and Disadvantaged Areas (GIDA) and Gap Areas

Region VIII: Geographically Isolated and Disadvantaged Areas (GIDA) and Gap Areas BIRIBIRI LAOANG BIRI BIRI LAVEZARES LAVEZARES ROSARIOSAN JOSE LAVEZARES PALAPAG ALLEN ROSARIOSAN JOSE LAOANG SAN ROQUEPAMBUJAN µ CATARMAN (Capital) MAPANAS CAPUL VICTORIA BOBON MONDRAGON SAN ANTONIO CATUBIG SAN VICENTE GAMAY SAN VICENTE SAN ISIDRO SAN VICENTE LOPE DE VEGA LAS NAVAS LAPINIG SAN VICENTE SILVINO LOBOS JIPAPAD ARTECHE SAN POLICARPO CALBAYOG CITY MATUGUINAO ORAS MASLOG GANDARA DOLORES TAGAPUL-AN SANTA MARGARITA SAN JOSE DE BUAN CAN-AVID SANTO NIÑO PAGSANGHANSAN JORGE PAGSANGHAN ALMAGRO TARANGNAN SANTO NIÑO TARANGNAN MOTIONGPARANAS (WRIGHT) TAFT CITY OF CATBALOGAN (Capital)JIABONG MARIPIPI SULAT SAN JULIAN DARAM HINABANGAN KAWAYAN SAN SEBASTIAN ZUMARRAGA ALMERIACULABA DARAM CALBIGA NAVAL (Capital) CITY OF BORONGAN (Capital) CAIBIRAN VILLAREALPINABACDAO BILIRAN CALUBIAN CABUCGAYAN TALALORA SANTA RITA MAYDOLONG SANTA RITA SAN ISIDRO BALANGKAYAN BABATNGON BASEY LLORENTE HERNANI TABANGOLEYTE BARUGOSAN MIGUEL TUNGATACLOBAN CITY (Capital) GENERAL MACARTHUR CAPOOCAN CARIGARA MARABUT VILLABA ALANGALANG LAWAANBALANGIGA SANTA FE QUINAPONDAN KANANGA JARO SALCEDO PALO GIPORLOS MATAG-OB PASTRANA TANAUAN MERCEDES DAGAMI ORMOC CITY GUIUANGUIUAN PALOMPON TABONTABONTOLOSA JULITA GUIUAN GUIUAN MERIDA BURAUEN DULAG ISABEL ALBUERA LA PAZMAYORGA MACARTHUR JAVIER (BUGHO) GUIUAN CITY OF BAYBAY ABUYOG MAHAPLAG INOPACAN SILAGO Legend HINDANG SOGOD HILONGOS HINUNANGAN BONTOC GIDA_Areas BATO LIBAGON HINUNDAYAN SAINT BERNARD MATALOMTOMAS OPPUS ANAHAWAN SAN JUAN (CABALIAN) Municipality CITY OF MAASIN (Capital) MALITBOG LILOAN MACROHON 0 90 Kilometers PADRE BURGOSSAN FRANCISCO SAN RICARDO PINTUYAN LIMASAWA 08 April 2014. -

Download Full Text

International Journal of Social Science and Economic Research ISSN: 2455-8834 Volume:03, Issue:01 "January 2018" TOURISM STATUS OF SOUTHERN LEYTE PROVINCE: BASIS FOR WEB-BASED TOURISM MARKETING STRATEGY DEVELOPMENT Jenny May T. Cinco Instructor I, Leyte Normal University, Paterno Street, Tacloban City 6500 Leyte ABSTRACT Tourism is undeniably a paramount piece in the economy. Different sectors subsist all together and play different roles but with the same aspiration of gaining substantial income. Social, cultural and educational constituencies are affected positively as tourism status arises in distinct areas of the country. This study assessed the status of Southern Leyte Tourism Industry regarding the tourism attractions, tourism services, and products that support the tourism industry to develop an advance tourism marketing strategy through the use of Information Technology concept. Tourist market of Southern Leyte’s tourism and the problems exist that affect the province tourism industry were also determined. Researcher-made questionnaire and series of surveys were carried out to perceive the actual location and condition of the different tourist attractions in the province. Personal interviews were done with the Department of Trade and Industry and the Southern Leyte Tourism, Investment, and Promotions Center. Keywords: Information Technology, tourism marketing strategy, tourist attractions, tourism services, tourism status, Southern Leyte. INTRODUCTION The current wave of global situation is impacting the tourism industry worldwide, and few places become immune. The tourism industry is at peak is one of the largest industries in the world provoked by the increase in cross-border trade, more open policies and technology change. This is a new phase, the tourism epoch. -

SOIL FERTILITY MAP ( Key Rice Areas ) Province of Abra PROVINCE of SOUTHERN LEYTE

Silago Province of Leyte HIN UNGAN BAY Hinunangan Sogod Bontoc Hinundayan SURIGAO ST RAIT Libagon Saint Bernard Anahawan San Juan Tomas Oppus CABALIAN BAY Malitbog SOGO D BAY Liloan Maasin Macrohon B O H O L S E A San Francisco R E P U B L II C O F T H E P H II L II P P II N E S D E P A R T M E N T O F A G R II C U L T U R E BUREAU O F SOILS AND Padre Burgos WATER M ANAGEMENT Elliptical Road,cor.Visayas Ave.,Diliman,Quezon City SOIL FERTILITY MAP ( Key Rice Areas ) Province of Abra PROVINCE OF SOUTHERN LEYTE SCALE 1 : 180,000 0 0.75 1.5 3 4.5 6 Kilometers Pintuyan Projection : Transverse Mercator Datum : PRS 1992 DISCLAIMER: All political boundaries are not authoritative Limasawa San Ricardo LOCATION MAP 20° Le yt e 10°30' PRO VINCE OF SO UTHE RN L EY TE LU ZO N 15° LEGEND AREA VIS AY AS 10° MAPPING UNIT DESCRIPTION ha % 10° M IN D AN A O 5° Low 1 06 1.36 125° 115° 120° 125° Moderately Low 5,332 68.29 CONVENTIONAL SIGNS MISCELL ANEOUS INFORM AT ION SOURCES OF INFORMATION:Topographic information taken from NAMRIA Topographic Moderately High 2,351 30.11 Map at a scale of 1:50,000. Elevation data taken from SRTM 1 arc-second global datase ROADS BOUNDARY HYDROLOGY (2015). Bathymetry information taken from British Oceanographic Centre Fertility data gathered through the Soil Health Assessment-National Soil Sampling andTesting Project Expressway Regional Rivers / Lake Phase II led by the Bureau of Soils and Water Management in partnership with the DA- Regional Field Offices (RFOs) and Local Government Units (LGUs). -

Region VIII OPERATION TIMBANG RESULTS 2012

Region VIII OPERATION TIMBANG RESULTS 2012 Free Powerpoint Templates Page 1 ComparativeOPT COVERAGE OPT 2011-2012% PREVALENCE Results (based on 2000 proj. pop) PROVINCES 2011 2012 2011 2012 BILIRAN 75.69 77.93 13.11 12.38 E. SAMAR 75.94 11.83 10.82 79.60 LEYTE 69.25 15.73 15.12 70.50 N. SAMAR 80.43 17.69 15.80 76.30 SAMAR 62.76 21.54 17.88 69.30 So. LEYTE 69.21 7.95 7.82 73.40 Free Powerpoint Templates Page 2 OPT COVERAGE % PREVALENCE (based on 2000 proj. pop) CITIES 2011 2012 2011 2012 BAYBAY 63.73 62.27 13.97 13.56 BORONGAN 61.95 63.48 14.05 11.47 60.81 CALBAYOG 80.78 11.76 12.31 CATBALOGAN 73.57 67.57 27.75 18.31 MAASIN 74.84 5.03 4.69 62.90 93.70 12.57 11.99 ORMOC 93.77 TACLOBAN 71.38 9.88 8.51 66.92 14.98 13.68 REGION VIII 73.15 Free71.71 Powerpoint Templates Page 3 Southern Eastern Visayas: 25.7 Leyte: Free Powerpoint Templates 21.6 Page 4 Southern Leyte: 37.1 Free Powerpoint Templates Eastern Visayas: Page 5 41.7 Phil. Ave. 7.3 Eastern Visayas: Free Powerpoint Templates 7.8 Page 6 Comparative OPT 2011-2012 Results Province/ City 2011 Prev (%) 2012 Prev (%) % Change Biliran 13.11 12.38 0.73 Eastern Samar 11.83 10.82 1.01 Leyte 15.73 15.12 0.61 Northern Samar 17.69 15.80 1.89 Samar 21.54 17.88 3.66 Southern Leyte 7.95 7.82 0.13 Baybay City 13.97 13.56 0.41 Borongan City 14.05 11.47 2.58 Calbayog City 11.76 12.31 -0.55 Catbalogan City 27.75 18.31 9.44 Maasin City 5.03 4.69 0.34 Ormoc City 12.57 11.99 0.58 Tacloban City 9.88 8.51 1.37 Region VIII 14.98Free Powerpoint13.68 Templates 1.30 Page 7 Prevalence of Underweight According to -

Philippines: Landslides and Floods; Appeal No

PHILIPPINES: Emergency appeal n° MDRPH001 GLIDE n° 2006-000024-PHL Operations update n° 8 Landslides and 13 March 2008 Floods Period covered by this Operations Update: 1 July 2007 – 31 January 2008 Appeal target (current): CHF 2.80 million1 (USD 2.79 million or EUR 1.78 million) Appeal coverage: 100%; <click here to go directly to the interim financial report, or here to link to contact details > Appeal history: • A preliminary appeal was launched on 17 February 2006 for CHF 2.13 million (USD 1.73 million or EUR 1.29 million) for six months. • On 8 March 2006, the appeal was revised to CHF 2.59 million to assist 8,000 beneficiaries for 18 months, to 31 August 2007, focusing on recovery and rehabilitation. • On 22 June 2006, the appeal budget was increased to CHF 2.66 million (USD 2.17 million or EUR 1.62 million) as recorded in Operations Update no. 5. • In June 2007, the budget was revised to CHF 2.83 million, taking into consideration support from the Geneva secretariat in programming and fundraising, and documented in Operations Update no. 6. • Disaster Relief Emergency Funds (DREF) allocated: CHF 200,000 (USD 162,602 or EUR 121,212). Summary: During the reporting period, the Philippine National Red Cross (PNRC), with support from the International Federation, focused its efforts on completing the construction of the 96 duplex units (192 single housing units) in Catmon. The duplex units are constructed for the families who were affected by the landslide in St Bernard, Southern Leyte. These families are from the barangays (villages) of Hinabin, Kauswagan and Magatas. -

Community-Based Marine Sanctuaries in the Philippines: a Report on Focus Group Discussions

COMMUNITY-BASED MARINE SANCTUARIES in the PHILIPPINES:A REPORT on FOCUS GROUP DISCUSSIONS Brian Crawford, Miriam Balgos and Cesario R. Pagdilao June 2000 Coastal Resources Center Philippine Council for Aquatic and University of Rhode Island Marine Research and Development Community-Based Marine Sanctuaries in the Philippines: A Report on Focus Group Discussions Brian Crawford Coastal Resources Center University of Rhode Island Miriam Balgos Graduate College of Marine Studies University of Delaware Cesario R. Pagdilao Philippine Council for Aquatic and Marine Research and Development Department of Science and Technology June 2000 Acknowledgments The authors of this paper would like to thank the numerous individuals who assisted with this effort. Over fifty participants from a diverse mix of institutions participated in a series of four focus group discussions whose inputs, comments and explanations about their respective experience contributed substantially to the contents of this report. A list of participating individuals and institutions is provided in Annex 5. We particularly appreciated the participation of individuals who traveled long distances from locations outside the city venues to attend, especially the representatives of local people’s organizations. We are grateful to the many participants who provided lists of community-based marine sanctuary sites for possible inclusion in the field investigation, as well as related secondary data and references. We greatly appreciated the assistance of the Marine Science Institute (MSI) of the University of the Philippines and the Silliman University Marine Laboratory (SUML) and Center of Excellence in Coastal Resources Management, for serving as venue hosts in Manila and Dumaguete respectively, and particularly the assistance of Porfirio Aliño, Charina Conte and Maricar Samson of MSI, and Hilconida Calumpung, Roy Olsen de Leon, Pacita Raterta, and Julieta Luchavez of SUML. -

Institutional Frameworks for Community-Based Coastal Resources Management and Marine Conservation in the Eastern Visayas Region

I NSTITUTIONAL F RAMEWORKS FOR C OMMUNITY- BASED C OASTAL R ESOURCES M ANAGEMENT AND M ARINE C ONSERVATION IN THE E ASTERN V ISAYAS R EGION Baybay, Leyte, Philippines March 2002 Editors: Cesario Pagdilao Bernardita Germano Glenn Ricci Ester Zaragoza On the cover: Coastal dwellers in Inopacan, Leyte, cooking pandan leaves for mat weaving Divers participating in resource and ecological assessment studies in Guimaras Island, Philippines Children poised at Nipa House in Cuartro Islas, Inopocan, Leyte PROCEEDINGS Institutional Frameworks for Community-based Coastal Resources Management and Marine Conservation in the Eastern Visayas Region Baybay, Leyte, Philippines March 2002 Editors Cesario R. Pagdilao Bernardita P. Germano Glenn M. Ricci Ester C. Zaragoza This undertaking was a collaborative effort between the Coastal Resources Center at the University of Rhode Island and the Philippine Council for Aquatic and Marine Research and Development of the Department of Science and Technology, in conjunction with the Institute of Tropical Ecology at Leyte State University. October 2002 CRC Coastal Management Report #2237 PCAMRD Book Series No. 36 ISBN# 1-885454-46-5 COASTAL RESOURCES CENTER Leyte State University of Rhode Island University PCAMRD-DOST ACRONYMS ADB Asian Development Bank AFMA Agriculture and Fisheries Modernization Act BFAR Bureau of Fisheries and Aquatic Resources BFARMC Barangay Fisheries and Aquatic Resources Management Council CAFC City Agriculture and Fisheries Councils CEP Coastal Environment Program CEMRINO Center for the -

BUREAU of SOILS and WATER MANAGEMENT ( Key Rice Areas

Silago Province of Leyte HIN UNGAN BAY Hinunangan Sogod Bontoc Hinundayan SURIGAO ST RAIT Libagon Saint Bernard Anahawan San Juan Tomas Oppus CABALIAN BAY Malitbog SOGO D BAY Liloan Maasin Macrohon B O H O L S E A San Francisco R E P U B L I C O F T H E P H I L I P P I N E S R E P U B L I C O F T H E P H I L I P P I N E S Padre Burgos D E P A R T M E N T O F A G R II C U L T U R E BUREAU O F SOILS AND WATER M ANAGEMENT Elliptical Road,cor.Visayas Ave.,Diliman,Quezon City NUTRIENT STAUS MAP : NITROGEN ( Key Rice Areas ) Province of Abra PROVINCE OF SOUTHERN LEYTE SCALE 1 : 180,000 Pintuyan 0 0.75 1.5 3 4.5 6 Kilometers Projection : Transverse Mercator Datum : PRS 1992 Limasawa DISCLAIMER: All political boundaries are not authoritative San Ricardo LOCATION MAP 20° Le yt e 10°30' PRO VINCE OF SO UTHE RN L EY TE LU ZO N 15° VIS AY AS 10° 10° LEGEND M IN D AN A O ORGANIC MATTER NITROGEN AREA 5° MAPPING UNIT DESCRIPTION ( OM ) % ( N ) % ha % 125° 115° 120° 125° Low 0 - 2 0 - 0.10 1,200 15.37 MISCELL ANEOUS INFORM AT ION SOURCES OF INFORMATION:Topographic information taken from NAMRIA Topographic Map at a scale of 1:50,000. Elevation data taken from SRTM 1 arc-second global datase CONVENT IONA L SIGNS Moderately Low 2.1 - 3.5 0.105 - 0.175 5,090 65.19 (2015). -

Executive Summary

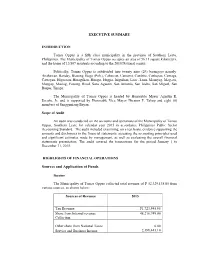

EXECUTIVE SUMMARY INTRODUCTION Tomas Oppus is a fifth class municipality in the province of Southern Leyte, Philippines. The Municipality of Tomas Oppus occupies an area of 56.11 square kilometers, and the home of 15,807 residents according to the 2010 National census. Politically, Tomas Oppus is subdivided into twenty nine (29) barangays namely: Anahawan, Banday, Biasong, Bogo (Pob.), Cabascan, Camansi, Cambite, Canlupao, Carnaga, Cawayan, Higosoan, Hinagtikan, Hinapo, Hugpa, Iniguihan, Looc, Luan, Maanyag, Mag-ata, Mapgap, Maslog, Ponong, Rizal, Sana Agustin, San Antonio, San Isidro, San Miguel, San Roque, Tinago. The Municipality of Tomas Oppus is headed by Honorable Mayor Agustin R. Escaño, Jr. and is supported by Honorable Vice Mayor Nicanor F. Tahup and eight (8) members of Sangguniang Bayan. Scope of Audit An audit was conducted on the accounts and operations of the Municipality of Tomas Oppus, Southern Leyte for calendar year 2015 in accordance Philippines Public Sector Accounting Standard. The audit included examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements, assessing the accounting principles used and significant estimates made by management, as well as evaluating the overall financial statements presentation. The audit covered the transactions for the period January 1 to December 31, 2015. HIGHLIGHTS OF FINANCIAL OPERATIONS Sources and Application of Funds Income The Municipality of Tomas Oppus collected total revenue of P 52,329,138.05 from various sources, as shown below: Sources of Revenue 2015 Tax Revenue P1,723,945.95 Share from Internal revenue 48,216,749.00 Collection Other share from National Taxes 0.00 Service and Business Income 2,388,443.10 Shares, Grants and Donations 0.00 Gains 0.00 Other Income 0.00 Total P52,329,138.05 Appropriations Appropriations for the current year amounted to P 57,664,166.00.