Valuation Report

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

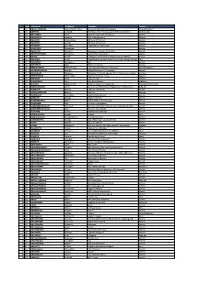

Department Town Address Postcode Telephone Etoloakarnania Agrinio

Department Town Address Postcode Telephone Etoloakarnania Agrinio 1, Eirinis square, Dimitrakaki street 301 00 2641046346 Etoloakarnania Mesologgi 45, Charilaou Trikoupi street 302 00 2631022487 Etoloakarnania Nafpaktos 1, Athinon street 303 00 2634038210 Etoloakarnania Amfilohia Vasileos Karapanou street 305 00 2642023302 Argolida Argos 12, Danaou street 212 00 2751069042 Argolida Nafplio 35, Argous street 211 00 2752096478 Argolida Porto Heli Porto Heli Argolidas 210 61 2754052102 Arkardia Megalopoli 15, Kolokotroni street 222 00 2791021131 Arkardia Tripoli 48, Ethinikis Antistaseos street 221 00 2710243770 Arta Arta 129, Skoufa street 471 00 2681077020 Attica Athens 316, Acharnon street & 26 Atlantos street 112 52 2102930333 Attica Agios Dimitrios 54, Agiou Dimitriou street 173 41 2109753953 Attica Agios Dimitrios 276, Vouliagmenis avenue 173 43 2109818908 Attica Agios Dimitrios 9 - 11, Agiou Dimitriou street 173 43 2109764322 Attica Agia Paraskevi 429, Mesogeion avenue 153 43 2106006242 Attica Athens - Piraeus 153, Piraeus Avenue 118 53 2104815333 Attica Athens - Aristeidou 1, Aristeidou street 105 59 2103227778 Attica Athens 79, Alexandras avenue 114 74 2106426650 Attica Athens - Plateia Viktorias 2, Victoria square 104 34 2108220800 Attica Athens - Stadiou 7, Stadiou street 105 62 2103316892 Attica Egaleo 266, Iera Odos street 122 42 2105316671 126, Vasilissis Sofias street & 2, Feidippidou Attica Abelokipoi street 115 27 2106461200 Attica Amfiali 32, Pavlou Fissa street 187 57 2104324300 Attica Palaio Faliro 82, Amfitheas avenue -

Archaic Eretria

ARCHAIC ERETRIA This book presents for the first time a history of Eretria during the Archaic Era, the city’s most notable period of political importance. Keith Walker examines all the major elements of the city’s success. One of the key factors explored is Eretria’s role as a pioneer coloniser in both the Levant and the West— its early Aegean ‘island empire’ anticipates that of Athens by more than a century, and Eretrian shipping and trade was similarly widespread. We are shown how the strength of the navy conferred thalassocratic status on the city between 506 and 490 BC, and that the importance of its rowers (Eretria means ‘the rowing city’) probably explains the appearance of its democratic constitution. Walker dates this to the last decade of the sixth century; given the presence of Athenian political exiles there, this may well have provided a model for the later reforms of Kleisthenes in Athens. Eretria’s major, indeed dominant, role in the events of central Greece in the last half of the sixth century, and in the events of the Ionian Revolt to 490, is clearly demonstrated, and the tyranny of Diagoras (c. 538–509), perhaps the golden age of the city, is fully examined. Full documentation of literary, epigraphic and archaeological sources (most of which have previously been inaccessible to an English-speaking audience) is provided, creating a fascinating history and a valuable resource for the Greek historian. Keith Walker is a Research Associate in the Department of Classics, History and Religion at the University of New England, Armidale, Australia. -

Final List EMD2015 02062015

N° Title LastName FirstName Company Country 1 Dr ABDUL RAHMAN Noorul Shaiful Fitri Universiti Malaysia Terengganu United Kingdom 2 Mr ABSPOEL Lodewijk Nl Ministry For Infrastructure And Environment Netherlands 3 Mr ABU-JABER Nizar German Jordanian University Jordan 4 Ms ADAMIDOU Despina Een -Praxi Network Greece 5 Mr ADAMOU Christoforos Ministry Of Tourism Greece 6 Mr ADAMOU Ioannis Ministry Of Tourism Greece 7 Mr AFENDRAS Evangelos Independent Consultant Greece 8 Mr AFENTAKIS Theodoros Greece 9 Mr AGALIOTIS Dionisios Vocational Institute Of Piraeus Greece 10 Mr AGATHOCLEOUS Panayiotis Cyprus Ports Authority Cyprus 11 Mr AGGOS Petros European Commission'S Representation Athens Greece 12 Dr AGOSTINI Paola Euro-Mediterranean Center On Climate Change (Cmcc) Italy 13 Mr AGRAPIDIS Panagiotis Oss Greece 14 Ms AGRAPIDIS Sofia Rep Ec In Greece Greece 15 Mr AHMAD NAJIB Ahmad Fayas Liverpool John Moores University United Kingdom 16 Dr AIFANDOPOULOU Georgia Hellenic Institute Of Transport Greece 17 Mr AKHALADZE Mamuka Maritime Transport Agency Of The Moesd Of Georgia Georgia 18 Mr AKINGUNOLA Folorunsho Nigeria Merchant Navy Nigeria 19 Mr AKKANEN Mika City Of Turku Finland 20 Ms AL BAYSSARI Paty Blue Fleet Group Lebanon 21 Dr AL KINDI Mohammed Al Safina Marine Consultancy United Arab Emirates 22 Ms ALBUQUERQUE Karen Brazilian Confederation Of Agriculture And Livesto Belgium 23 Mr ALDMOUR Ammar Embassy Of Jordan Jordan 24 Mr ALEKSANDERSEN Øistein Nofir As Norway 25 Ms ALEVRIDOU Alexandra Euroconsultants S.A. Greece 26 Mr ALEXAKIS George Region Of Crete -

ESDY-NSPH), Athens from the Airport

Access to the National School of Public Health (ESDY-NSPH), Athens from the Airport The ESDY-NSPH can easily be accessed by the Metro (underground blue line M3). From Athens International Airport (Eleftherios Venizelos Airport) you can take: 1. the metro (ticket cost 10.00 € one way, service every half hour) and get off at Ambelokipi Station (no change required, both the Airport Metro Station and Ambelokipoi Metro Station are on the blue line (M3)). Get out of Ambelikipi Station through the Alexandras/Soutsou Exit and walk at the direction of the cars. After 270 m (3 minutes walk) you arrive at the School. 2. the X95 Airport Bus (departs outside the Εxit 5 of the airport (arrivals level), ticket to be bought at the Bus Booth just outside the exit, ticket cost 6.00 € one way), and get off at Ambelokipi Platia Bus Stop (around 45 minutes journey). Then walk up, by a small garden/park, and turn left to get to Leoforos Alexandras to arrive at the NSPH. 3. a taxi (from the Taxi Station outside Exits 2 and 3 of airport arrivals level). The cost of the taxi is fixed if your destination is within the Inner Circle of Athens (daktylios) and amounts to: 38.00 € (hours 05:00 – 24:00) 54.00 € (hours 24:00 – 05:00) If your destination is outside the Inner Circle (daktylios) then you pay by the taximeter. The ESDY-NSPH, is right on the Inner Circle. Leaving from the National School of Public Health (ESDY-NSPH), Athens to the Airport From the ESDY-NSPH to Athens International Airport (Eleftherios Venizelos Airport) you can take: 1. -

Registration Certificate

1 The following information has been supplied by the Greek Aliens Bureau: It is obligatory for all EU nationals to apply for a “Registration Certificate” (Veveosi Engrafis - Βεβαίωση Εγγραφής) after they have spent 3 months in Greece (Directive 2004/38/EC).This requirement also applies to UK nationals during the transition period. This certificate is open- dated. You only need to renew it if your circumstances change e.g. if you had registered as unemployed and you have now found employment. Below we outline some of the required documents for the most common cases. Please refer to the local Police Authorities for information on the regulations for freelancers, domestic employment and students. You should submit your application and required documents at your local Aliens Police (Tmima Allodapon – Τμήμα Αλλοδαπών, for addresses, contact telephone and opening hours see end); if you live outside Athens go to the local police station closest to your residence. In all cases, original documents and photocopies are required. You should approach the Greek Authorities for detailed information on the documents required or further clarification. Please note that some authorities work by appointment and will request that you book an appointment in advance. Required documents in the case of a working person: 1. Valid passport. 2. Two (2) photos. 3. Applicant’s proof of address [a document containing both the applicant’s name and address e.g. photocopy of the house lease, public utility bill (DEH, OTE, EYDAP) or statement from Tax Office (Tax Return)]. If unavailable please see the requirements for hospitality. 4. Photocopy of employment contract. -

MIBS Glyfada Elite

GLYFADA ELITE ATHENS SEASIDE THE AREA Live in Glyfada, a neighborhood whose unique geography, public spaces, and revitalized natural beauty inspire fresh thinking, real engagement, and deep relaxation. Located in the luxurious southern suburbs of Athens, Glyfada is only about a half-hour drive from the city center. With lovely beaches, Michelin stars restaurants and many high-end stores, this is where many dream of moving in order to combine the best of city-living with all that the coast has to offer. GLYFADA ELITE Glyfada Elite consists of eight two-bedroom apartments delivering a premium living experience to its residents by having communal spaces such as swimming pool and rooftop terrace to enjoy the panoramic sea view. Glyfada Elite is a mix of comfortable modernism and highest level of finishes and technology. All residents benefit from a private outdoor space within each apartment, a communal rooftop terrace and a swimming pool with a lounge area on the Ground floor. The top floor residents may take relaxation to another level on their private rooftop terrace with an optional Jacuzzi and lingering sea views. 11 To SN Cultural Centre PRIME LOCATION km Situated in a prime area with convenient 2.2km Police Station 2.2km transport links, Glyfada Elite provides quick and Elliniko Metro Station 1.5km efficient transport connections across Athens. Public Schools Post Office 450m 1.5km Public Sport Facilities Leof. Vouliagmenis 1km ATHENS Private College Private School INSPIRE 2.6 km Hellinikon Metropolitan Park 1.5km 2.8km 200m Private Gym Golf Club Leof. Posidonos 13km Syntagma Sqaure 1.3km City Plaza Shopping Centre 15km Piraeus Chief Port 26.5km Athens International Airport 2.8km 2.7km Swimming Pool Hondos Centre 2.8km Dim. -

Networking UNDERGROUND Archaeological and Cultural Sites: the CASE of the Athens Metro

ing”. Indeed, since that time, the archaeological NETWORKING UNDERGROUND treasures found in other underground spaces are very often displayed in situ and in continu- ARCHAEOLOGICAL AND ity with the cultural and archaeological spaces of the surface (e.g. in the building of the Central CULTURAL SITES: THE CASE Bank of Greece). In this context, the present paper presents OF THE ATHENS METRO the case of the Athens Metro and the way that this common use of the underground space can have an alternative, more sophisticated use, Marilena Papageorgiou which can also serve to enhance the city’s iden- tity. Furthermore, the case aims to discuss the challenges for Greek urban planners regarding the way that the underground space of Greece, so rich in archaeological artifacts, can become part of an integrated and holistic spatial plan- INTRODUCTION: THE USE OF UNDERGROUND SPACE IN GREECE ning process. Greece is a country that doesn’t have a very long tradition either in building high ATHENS IN LAYERS or in using its underground space for city development – and/or other – purposes. In fact, in Greece, every construction activity that requires digging, boring or tun- Key issues for the Athens neling (public works, private building construction etc) is likely to encounter an- Metropolitan Area tiquities even at a shallow depth. Usually, when that occurs, the archaeological 1 · Central Athens 5 · Piraeus authorities of the Ministry of Culture – in accordance with the Greek Archaeologi- Since 1833, Athens has been the capital city of 2 · South Athens 6 · Islands 3 · North Athens 7 · East Attica 54 cal Law 3028 - immediately stop the work and start to survey the area of interest. -

Supplementary Materials

Supplementary Materials Figure S1. Temperature‐mortality association by sector, using the E‐OBS data. Municipality ES (95% CI) CENTER Athens 2.95 (2.36, 3.54) Subtotal (I-squared = .%, p = .) 2.95 (2.36, 3.54) . EAST Dafni-Ymittos 0.56 (-1.74, 2.91) Ilioupoli 1.42 (-0.23, 3.09) Kessariani 2.91 (0.39, 5.50) Vyronas 1.22 (-0.58, 3.05) Zografos 2.07 (0.24, 3.94) Subtotal (I-squared = 0.0%, p = 0.689) 1.57 (0.69, 2.45) . NORTH Aghia Paraskevi 0.63 (-1.55, 2.87) Chalandri 0.87 (-0.89, 2.67) Galatsi 1.71 (-0.57, 4.05) Gerakas 0.22 (-4.07, 4.70) Iraklio 0.32 (-2.15, 2.86) Kifissia 1.13 (-0.78, 3.08) Lykovrisi-Pefki 0.11 (-3.24, 3.59) Marousi 1.73 (-0.30, 3.81) Metamorfosi -0.07 (-2.97, 2.91) Nea Ionia 2.58 (0.66, 4.54) Papagos-Cholargos 1.72 (-0.36, 3.85) Penteli 1.04 (-1.96, 4.12) Philothei-Psychiko 1.59 (-0.98, 4.22) Vrilissia 0.60 (-2.42, 3.71) Subtotal (I-squared = 0.0%, p = 0.975) 1.20 (0.57, 1.84) . PIRAEUS Aghia Varvara 0.85 (-2.15, 3.94) Keratsini-Drapetsona 3.30 (1.66, 4.97) Korydallos 2.07 (-0.01, 4.20) Moschato-Tavros 1.47 (-1.14, 4.14) Nikea-Aghios Ioannis Rentis 1.88 (0.39, 3.39) Perama 0.48 (-2.43, 3.47) Piraeus 2.60 (1.50, 3.71) Subtotal (I-squared = 0.0%, p = 0.580) 2.25 (1.58, 2.92) . -

Supporting Material for Greece's Offer to Host the European Medicines

Relocation of the European Medicines Agency Supporting Material for Greece’s offer to host the European Medicines Agency Athens Hellenic Republic Greece’s candidacy to host the “European Medicines Agency” in Athens 1 Table of Contents A.Introduction ................................................................................................................................ 4 B.Executive summary ..................................................................................................................... 7 C.Facilitating the establishment of the EMA and its staff to Athens –Legal framework and general provisions .................................................................................................................... 9 D.Criteria for the relocation of the European Medicines Agency .................................................... 10 1. The assurance that the Agency can set up on site and take up its functions at the date of UK’s withdrawal from the Union ............................................................................................ 10 1.1 Presentation of EMA’s future premises ........................................................................................ 10 1.1.1 Location ....................................................................................................................................... 10 1.1.2 Accessibility .................................................................................................................................. 12 1.1.3 Brief description of the -

Office & Retail Markets

savills.grkentriki.gr | savills.gr Basic Aspects of the Greek Economy (source: Focus Economics, March 2017, ELSTAT) 2015 2016 2017 2018f GDP (Annual change -0.2 0 1.4 2.1 %) Private consumption -0.2 1.4 0.9 1.3 (Annual change %) Exports (Annual -4.8 -1.4 5.7 5.8 change %) Industrial production (Annual 1.0 2.5 1.6 2.0 change %) Unemployment (% of the economically 25.0 23.5 20.8 20.0 active population) Current Situation and Prospect . The GDP presented marginal growth (0.3%) during the first quarter (y-o-y). This marks the first time since 2006 that the Greek economy has grown for three consecutive quarters. In real terms the GDP amounted to 187.1 bn Euros demonstrating positive change 1.4% compared to 2016 (1st estimate). This is due to the revival in the investment climate and to the respective changes that recorded in components of GDP. Budgetary and financial situation is improving, with the closing of the review being crucial not only for the disbursement of the last bailout tranches, but also for the possible Greek Bailout Program exit. The Greek Government, under IMF instructions, has made steps in the direction of reducing the tax-free amount and reforming the National Insurance system. As Greek banks accelerate the process of restructuring and subsequently disposing of their non performing loan (NPL) portfolios, favorable conditions are created for the viability of the banking system. Basic markets of Attica North Precinct Grade A+B stock 1,000,000 m2 West Precinct Vacancy rate 7-13% Grade A+B stock 160,000 m2 Rental levels 10-15 -

How to Reach Alexandros Hotel

HOW TO REACH ALEXANDROS HOTEL Alexandros hotel is accessible by private vehicle or public transportation, from the Athens International Airport El. Venizelos, Piraeus, Larissis Station, Kifissos and Liosion bus stations and through the national highways Athens-Lamia and Athens - Corinth, in the following ways: ATHENS INTERNATIONAL AIRPORT ELEFTHERIOS VENIZELOS By Car • Distance from the airport: 30,7 km • Duration: ~35 minutes Enter Attiki Odos and get the exit Y1 (Katehaki), which leads to Kifisias Avenue. Turn left on Kifisias Av. and continue straight ahead for 2 km. Turn right at Timoleontos Vassou Str. where you will find our hotel. Alternatively, enter Attiki Odos and take exit 11 (Kifisias Avenue). Go straight for about 8 km towards Athens, and turn right onto Timoleontos Vassou Str. where you will find our hotel. • Distance from the airport: 31,8 km • Duration: ~35 minutes You can park for free in our hotel parking. (Parking is available upon request). By taxi • Distance from the airport: 30,7 km • Duration: ~35 minutes • The cost is around 38€ from 05:00 to 00:00 and around 54€ from 00:00 until 5:00. In case you want to have a taxi driver waiting for you in airport arrivals click here to reserve your taxi . By Express bus X95 • Distance from the airport: 30,7 km • Duration: ~40 minutes • Cost per person is 6,00€ The bus operates around the clock. It departs every 15 minutes from the terminal of the airport and stops at Mavili square, at Vasilissis Sofias Str. Upon getting off the bus, walk to your right and you will find us on the 3rd street on your left. -

ANNUAL REPORT 2004 Piraeusuk 1 26.Qxd 13/04/05 14:39 “ Æ1

Cover_UK.qxd 07/04/05 13:25 “ Æ2 ANNUAL REPORT 2004 PiraeusUK_1_26.qxd 13/04/05 14:39 “ Æ1 CONTENTS BRIEF OVERVIEW 2 PIRAEUS GROUP: A DYNAMIC GROWTH COURSE 3 CHAIRMAN’S REPORT 5 DEVELOPMENTS IN THE INTERNATIONAL AND GREEK ECONOMIES 9 CONSOLIDATED FIGURES OF PIRAEUS GROUP 10 FIGURES OF PIRAEUS BANK 11 ANALYSIS OF FIGURES AND RESULTS OF PIRAEUS GROUP 12 RETAIL BANKING 18 CORPORATE BANKING 23 E-BANKING (WINBANK, ATM) 29 INTERNATIONAL ACTIVITIES 30 INVESTMENT BANKING 35 ASSET MANAGEMENT 39 REAL ESTATE DEVELOPMENT AND MANAGEMENT 42 TECHNOLOGY AND INFRASTRUCTURES 44 RISK MANAGEMENT 47 HUMAN RESOURCES 51 CORPORATE GOVERNANCE 55 SOCIETY AND ENVIRONMENT 59 CUSTOMER RELATIONS 65 SHARE PRICE DEVELOPMENT AND PERFORMANCE 67 ADOPTION OF THE INTERNATIONAL FINANCIAL REPORTING STANDARDS 70 GROWTH GOALS AND PROSPECTS OF PIRAEUS BANK GROUP 72 CONSOLIDATED FINANCIAL STATEMENTS AS AT 31 DECEMBER 2004 74 ANALYSIS OF FIGURES AND RESULTS OF PIRAEUS BANK 78 FINANCIAL STATEMENTS AS AT 31 DECEMBER 2004 82 DOMESTIC BRANCH NETWORK 86 DOMESTIC SUBSIDIARIES 93 NETWORK OF BRANCHES AND SUBSIDIARIES ABROAD 94 PiraeusUK_1_26.qxd 13/04/05 14:39 “ Æ2 BRIEF OVERVIEW 1916 ñ Establishment of Piraeus Bank 1918 ñ The shares of Piraeus Bank were listed in the Athens Stock Exchange 1963 ñ Piraeus Bank was integrated into Emporiki Bank Group in Greece 1975 ñ Piraeus Bank came under state control within Emporiki Bank Group 1991 ñ Privatisation of Piraeus Bank 1992 ñ Year of restructuring, reform and growth ñ Participation in Private Investment SA, which was renamed Piraeus Investment