Age 7-46 Pages 7- 46

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

M/S. Apollo Hospitals Ltd) (M/S.Stylrite Optical Industries) 1 13 Section Point 17 No Mention of PMOO's in the 1

Andhra Pradesh Medical Services & Infrastructure Development Corporation, plot no 9, survey no 49, IT Park, Mangalagiri, Guntur District 522503 Email: [email protected] **** Request for Proposal for Tele Ophthalmology Services Under PPP Mode in Andhra Pradesh Amendment No.2 dt: 25.02.2019 Tender Notice No.: 17.1/Equipment/2018-19, Dated:07.02.2019. Clarifications requested by the bidders during prebid meeting on 18.02.2019 Sl.no Page Clause Heading Tender requirements Bidder's request Bidder's request Can be read as No. no. (M/s. Apollo Hospitals Ltd) (M/s.Stylrite Optical Industries) 1 13 Section Point 17 No mention of PMOO's in the 1. PMOO's will be provided by Govt. for all centres (along with relievers) No IV; Manpower at table mentioned in the centre document. 2 2. PMOO's to be recruited by the service provider in how many centres. ? In Addition to the staff mentioned at point 17 in section IV, PMOO has to be recruited by the service provider at all center @ 1 per center. 3 3. Qualification of the PMOO's Paramedical Ophthalmic Assistant Course or equalent course 4 4. PMOO relievers needed. (without the PMOO centre will be non Yes operational) 5 23 Section General No mention of guidelines to Referral for ROP Patients requiring further management to be referred to VI be followed for the referrals nearest secondary vision centers of Govt for funds, ROP & high power /AH/DH/TH/Regional Eye Hospital prescription. Also no mention about the EMR guidelines to be followed. (patient health records, data management, etc.) 6 Referral for Fundus Patients requiring further management to be referred to nearest secondary vision centers of Govt /AH/DH/TH/Regional Eye Hospital 7 For High power and complex Rx sceptical prescription Patients requiring further management to be referred to nearest secondary vision centers of Govt /AH/DH/TH/Regional Eye Hospital 8 EMR Guidelines (What standards need to be followed) eHR Standards-2016 guidelines issued by GOI,MoHFW, ehealth section Sl.no Page Clause Heading Tender requirements Bidder's request Bidder's request Can be read as No. -

5 Common Review Mission Andhra Pradesh National Rural Health Mission

5th Common Review Mission Andhra Pradesh 9th to 15th November 2011 National Rural Health Mission Ministry of Health and Family Welfare Government of India 1 Table of Contents List of abbreviations: .............................................................................................. 4 Executive Summary: .............................................................................................. 6 Chapter I – Team – Andhra Pradesh for the 5th CRM .............................................. 9 Chapter II – Introduction to the State .................................................................. 11 Chapter III - Major findings of CRM ...................................................................... 15 Chapter IV Recommendations of the 5th CRM .................................................... 45 th Annexure 1: Data for the 5 CRM: ....................................................................... 49 2 3 List of abbreviations: AH Area Hospital ANM Auxiliary Nurse Midwife APVVP Andhra Pradesh Vaidya Vidhan Parishad ASHA Accredited Social Health Activist AYUSH Ayurveda, Yoga, Unani, Siddha and Homeopathy CAO Chief Administrative Officer CAS Civil Assistant SUrgeon CES Coverage Evaluation Survey CFO Chief Finance Officer CHC Community Health Center CHNC Community Health and Nutrition Cluster CPO Chief Programme Officer CRM Common Review Mission DCHS District Coordinator of Hospital Services DH District Hospital DHIS - 2 District Health Information Software - 2 DHS District Health Society DLHS-3 District Level Household -

City Wise Progress

CITY wise details of PMAY(U) Financial Progress (Rs in Cr.) Physical Progress (Nos) Sr. Central Central State /City Houses Houses Houses No. Investment Assistance Assistance Sanctioned Grounded* Completed* Sanctioned Released A&N Island 1 Port Blair 151.59 8.96 0.46 598 38 25 Andhra Pradesh 1 Penukonda 200.68 62.43 - 4162 3 0 2 Thallarevu 0.58 0.35 0.15 23 23 12 3 Pendurthi 268.45 120.57 28.37 8038 1030 264 4 Naidupeta 288.43 68.84 36.18 4592 3223 2430 5 Amaravati 360.24 76.27 76.36 5069 5069 5069 6 Hukumpeta 0.19 0.02 0.02 1 1 1 7 Palakonda 83.36 35.55 9.40 2364 1218 969 8 Tekkali 515.94 219.62 13.61 14641 93 0 9 Anandapuram 0.29 0.02 0.02 1 1 1 10 Anandapuram 0.12 0.03 0.03 1 1 1 11 Kothavalasa 0.26 0.01 0.01 2 2 2 12 Thotada 0.60 0.06 0.06 3 3 3 13 Thotada 0.55 0.06 0.06 3 3 3 14 jammu 0.15 0.01 0.01 1 1 1 15 Gottipalle 0.25 0.02 0.02 1 1 1 16 Narasannapeta 329.42 149.11 17.88 9939 2108 237 17 Boddam 0.14 0.03 0.03 1 1 1 18 Ragolu 0.22 0.02 0.02 1 1 1 19 Patrunivalasa 0.70 0.11 0.11 5 5 5 20 Peddapadu 0.20 0.02 0.02 1 1 1 21 Pathasrikakulam 3.58 0.29 0.29 13 13 13 22 Balaga(Rural) 2.44 0.21 0.21 10 10 10 23 Arsavilli(Rural) 2.51 0.19 0.19 9 9 9 24 Ponduru 0.32 0.02 0.02 1 1 1 25 Jagannadharaja Puram 0.50 0.08 0.08 4 4 4 26 Ranastalam 0.15 0.02 0.02 1 1 1 27 Tekkali 0.15 0.02 0.02 1 1 1 28 Shermahammadpuram 0.95 0.12 0.12 6 6 6 29 Pudivalasa 0.27 0.02 0.02 1 1 1 30 Kusalapuram 2.23 0.16 0.16 7 7 7 31 Thotapalem 0.79 0.10 0.10 4 4 4 32 Etcherla 227.17 121.97 25.56 8130 3904 276 33 Yegulavada 0.32 0.05 0.05 2 2 2 34 Kurupam 109.03 49.32 -

EUPHC- RFP Zone-II.Pdf

DEPARTMENT OF HEALTH & FAMILY WELFARE GOVERNEMNT OF ANDHRA PRADESH Request for Proposal (RFP) For Electronic Urban Primary Health Centers (e-UPHC) operations and management on PPP mode under National Urban Health Mission, Andhra Pradesh Disclaimer The information contained in this Request for Proposal (“RFP”) Document or subsequently provided to Bidder, whether verbally or in documentary form by or on behalf of the Department of Health & Family Welfare Society, Government of Andhra Pradesh (“Government Representative”) or any of their employees is provided to the Bidder on the terms and conditions set out in this RFP Document and any other terms and conditions subject to which such information is provided. This RFP Document is not an agreement and is not an offer or invitation by the Government Representative to any party other than the Bidders who are short-listed in pre-qualification to submit the Proposal (Bidders). The purpose of this RFP Document is to provide the Bidder with information to assist the formulation of their Proposals. This RFP Document does not purport to contain all the information each Bidder may require. This RFP Document may not be appropriate for all persons, and it is not possible for the Government Representative, their employees or advisors to consider the investment objectives, financial situation and particular needs of each party who reads or uses this RFP Document. Each Bidder should conduct its own investigations and analysis and should check the accuracy, reliability and completeness of the information in this RFP Document and where necessary obtain independent advice from appropriate sources. The Government Representative, their employees and advisors make no representation or warranty and shall incur no liability under any law, statute, rules or regulations as to the accuracy, reliability or completeness of the RFP Document. -

42010001 Meruga Nirmala H NO 5-12-36/41-1 NEAR

Final List of the Candidates Registered in ONLINE to appear for UGC NET to be held on 24-12-2011 at NAGARJUNA UNIVERSITY CAMPUS, NAGARJUNA NAGAR ADMISSION CARDS were POSTED to all the Following Candidates. Subject Subject Roll No Name Address Code 1. Economics(01) Meruga Nirmala H NO 5-12-36/41-1 NEAR SRINIVASA THEATER,GIDDALUR VIL & 42010001 POST &MANDAL,PRAKASAM 2. Economics(01) B Srinivasa Rao 37-5-8, 1ST FLOOR,,PATNALA VARI STREET, MARKET 42010002 AREA,KAKINADA 3. Economics(01) Sailaja Maddela D.NO.15-13-123/44,ZIYAUDDIN NAGAR, NEAR RTC 42010003 COLONY,GUNTUR 4. Economics(01) Vijaya Babu chiluvuru CHILUVURU (P.O) DUGGIRALA (M.D) GUNTUR 42010004 (D.T),CHILUVURU,GUNTUR 5. Economics(01) 42010006 Anuradha Seelam T-29A/1,ROAD NO.20 BALJEET NAGAR,NEWDELHI 6. Economics(01) Karumuri Kishore Kumar LH-2,ROOM NO-122,P.O.CENTRAL UNIVERSITY,GACHIBOWLI, 42010007 HYDERABAD. 7. Economics(01) Ramesh Settipalli INAPURU,NEAR BRIDGE,,PAMIDIMUKKALA MANDAL,,KRISHNA 42010008 DISTRICT 8. Economics (01) 42010009 G.Lakshmipathi 24-5-49/1,JANARDHANA COLONY,KANDUKURU 9. Economics(01) 42010010 Rajendra Babu Gudiri DOOR NO-27-3-44,,SRIRAM PURAM,BHIMAVARAM 10. Economics(01) Srinivasarao Gudipudi H.NO.8-94-1A, KOTHAPETA,,NEAR PENTHECOSTAL 42010011 CHURCH,,KANIGIRI 11. Economics(01) Aravind Swamy Pappala KUNKALAGUNTA(PO&VILL), NEKARIKALLU(MD),H.NO-5-122,NEAR 42010012 AKKAMA GUDI TEMPLE,GUNTUR 12. Economics(01) 42010013 Paleena D NO:17-2-22,SAMATANAGAR, AKIVIDU,AKIVIDU 13. Economics(01) Marella Yedukondala Rao E.PALEENA , H.NO - 19-3-1/1/A,MARKANDEYACOLONY , VVV HIGH 42010014 SCHOOL BESIDE,GODAVARIKHANI , KARIMNAGAR 14. -

To Address List Enclosed

OFFICE OF THE REGIONAL DIRECTOR OF MEDICAL AND HEALTH SERVICES, GUNTUR, SELECTION COMMITTEE FOR ZONAL LEVEL CADRE POSTS Rc.No.396/B1/SN-REC/2016 Dated:22.11.2016 Sub:- Estt – APM&HS - ACSR Medical College, Nellore – Appointment of Paramedical, Nursing and other posts in ACSR Government Medical College, Nellore on contract basis – Interview fixed on 05.12.2016 by 10.00AM in the O/o.Director of Medical Education, Andhra Pradesh, Old, GGH., Hanumanpeta, Vijayawada - Intimation - Reg. Ref:- 1. G.O.Ms.No.18 HM&FW (A1) Dept., Dated:04.03.2016. 2. G.O.Ms.No.28 HM&FW (A1), Dept., Dated:30.03.2016. 3. Rc.No.30375/P1/2015, Dated:01.04.2016 of the Director of Medical Education, A.P., Hyderabad. <<<>>> The candidate having DGNM qualification for the selection post of Staff Nurse noted in the address entry is informed to attend for physical verification of original certificates and Interview on 05.12.2016 by 10.00 AM in the O/o Director of Medical Education, Andhra Pradesh, Old, GGH., Hanumanpeta, Vijayawada. She / He should produce the following certificates in Original at the time of physical verification and Interview. 1. Evidence of Date of Birth (SSC or Equivalent examination ) 2. Intermediate or 10+2 Examination. 3. DGNM Examination Pass Certificates (Provisional / Original Degree) 4. Marks Memos of all the years (DGNM) 5. Registration certificate in the A.P. nursing counsel both Nursing & Midwifery. 6. Caste Certificate (in case of SC/ST/BC issued by the Revenue authorities). 7. Study Certificates from 4th to 10th class. -

2021 Placement Record

2021 Placement Record Package Lakhs Parent Phone Eamcet/ ECET / ICET Name and Address of the Student Photo Branch Selected Company per Number Rank Annum DASARI AMRUTHA CHOWDARY CSE TCS Digital 7 9441650671 15504 SANGADI GUNTA, GUNTUR KANNEGANTI TEJASWI CSE TCS Digital 7 7416709879 14559 TANK BUND ROAD, ITHANAGAR DEEPAK REDDY KOLAGATLA CSE Wiley Next, Virtusa Polaris 7, 4 7730052939 11632 BRODIPET GUNTUR VISWANATH SAI VENKATESH TCS Digital, Global Edge CSE 7, 3.5 9885646180 36600 ARUNDALPET GUNTUR Software Package Lakhs Parent Phone Eamcet/ ECET / ICET Name and Address of the Student Photo Branch Selected Company per Number Rank Annum SURAPARAJU DURGA ANUSHA CSE TCS Digital, TechM 7, 3.5 9985263502 31409 TARAKA RAMA NAGAR, 2ND LINE GUNTUR GOPINADH CHENNAM ECE ACS Solutions, Revature 5.16, 5 9295450402 14266 BHAVANIPURAM, GUNTUR NAKKANABOINA RAJESH ECE ACS Solutions, Accenture 5.16, 4.5 9491297579 51603 SIMHADRIPURAM MUSUNURU VAKKAPATLA GAYATHRI ECE ACS Solutions, Accenture 5.16, 4.5 9441692691 67106 MORRISPET TENALI JONNADULA NAGA ROHIT ECE ACS Solutions, TechM 5.16, 3.5 9290509560 37073 CHINARAVURU THOTA TENALI SK.JAKEER SANA CSE ADP, Revature 5.05, 5 9390636558 39501 GOPI DESI VARI STREET TENALI M.THULASI IT ADP, Revature 5.05, 5 9963776316 32514 MAINROAD MADDIPADU JANAPALA SUKANYA EEE Revature 5 9502089258 35653 VENGALAYA PALEM GUNTUR Package Lakhs Parent Phone Eamcet/ ECET / ICET Name and Address of the Student Photo Branch Selected Company per Number Rank Annum PALLE MALLIKARJUNA -

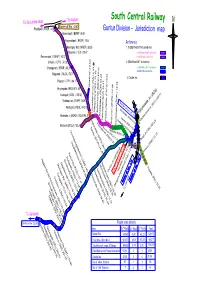

Evolution of Guntur Division

To Kazipet South Central Railway Border at Km. 4.50 Pagidipalli ( PGDP ) 4.02 Guntur Division - Jurisdiction map Bommaipalli ( BMMP ) 8.60 Nagireddipalli ( NRDP ) 19.44 Reference Mamdapur Halt ( MNDP ) 26.35 1. Sr.DEN/North/GNT Jurisdiction Valigonda ( VLG ) 29.47 a. ADEN/North/GNT Jurisdiction Ramannapet ( RMNP ) 42.12 b. ADEN/NLDA Jurisdiction Chityala ( CTYL ) 51.08 2. DEN/West/GNT Jurisdiction Srirampuram ( SRMR ) 66.31 c. ADEN/West/GNT Jurisdiction d. ADEN/NDL Jurisdiction Nalgonda ( NLDA ) 76.71 3. Double line Thipparti ( TPPI ) 94.11 Miryalaguda (MRGA)114.40 Janpahad (10.64) Kodrapol ( KDGL ) 125.56 Vishnupuram (VNUP) 134.97 Border at km. 25.36 Pondugala (PDGL) 143.78 Mangalagiri (MAG) 20.28 Piduguralla (PGRL) 74.10 Bellamkonda (BMKD) 60.42 Tummalacheruvu (TMLU) 83.34 Vijayawada Jn..(BZA) Nadikude Jn.(NDKD) 152.69/95.25 Reddigudem (REM) 54.29 Nambur (NBR) 8.67 Sattenapalli (SAP) 42.37 Nudurupadu (NDPU) 28.19 Pedakurapadu (PKPU) 29.64 Reddipalem (REP) 2.47 Krishna canal Jn..(KCC) 423.71 Phirangipuram (PPM) 21.07Siripuram (SRPM) 22.96 Macherla (MCLA) 130.26 Bandarupalli (BDPL) 13.58 Satulur (STUR) 34.29 Perecherla (PRCA) 11.26 Cheekateegalapalem ( CEM ) 89.55 Nallapadu (NLPD) 5.00 Gundlakamma (GKM) 95.85 Tenali Jn.(TEL) 397.25 Kurichedu (KCD) 107.27 Vemuru (VMU) 13.77 Potlapadu (POO) 113.85 Jaggam Bhotla Krishnapuram (JBK) 176.94 Donakonda (DKD) 120.08 Gajjalakonda (GJJ) 130.78 Narasaraopet (NRT) 45.30 Markapur Rd. (MRK) 143.97 Munumaka (MUK) 52.99 Repalle (RAL) 33.85 Santhamagulur (SAB) 61.51 Savalyapuram (SYM) 72.84 Guntur Jn.(GNT)0.00GNT atVejendla km.25.47 (VJA) 14.00 Tarlupadu (TLU) 156.44 Vinukonda (VKN) 82.85 Cumbum (CBM) 170.04 Somidevipalli (SDV) 188.94 Sangam jagarlamudi (SJL) 8.27 Yadavalli (YADA) 196.03 To Chennai Giddalur (GID) 203.78 To Guntakal Border at km. -

Dj15052015rcell.Pdf

HIGH COURT OF JUDICATURE AT HYDERABAD FOR THE STATE OF TELANGANA AND THE STATE OF ANDHRA PRADESH STATEMENT SHOWING THE LIST OF ELIGIBLE CANDIDATES WHO ARE APPLIED FOR THE 6 POSTS OF DISTRICT JUDGE UNDER DIRECT RECRUITMENT, NOTIFIED FOR THE YEAR 2014 SL Appl. NAME OF THE APPLICANT No. No.. ADDRESS 1. Venkata Narasimha Raju Krovvidi Plot No.44, Port Colony, 1 Back side of Nookambica Temple, Kasimkota Mandal, Kasimkota, Visakhapatnam District 531031 2. Suhasini Makina Dr.No.63-3-22/5, Flat No.202, 2 Dwarakamani Residence, Jawahar Nagar, Sriharipuram, Visakhapatnam 530011 3. Fareed Khan 3 4-10-6/1, Rajampet, Sanga Reddy Town, Medak District. 502001 4. Tejovathi Machisrajau Flot No.401, 4th Floor, 4 1-2-607/23/1/D, Om Nagar, Indira Park Road, Ashok Nagar, Hyderabad. 500080 5. Venkata Ratnakar Kondiparthi D.No.18-10-34, Zero Lane, 5 Kedareswarapet, Vijayawada, Krishna District 520003 6. Taruna Kumar Pillalamarri Door No.21-14-12-20/2A, Thota Vari 6 Street, 2nd Line, Ramalingeswarapet, Tenali, Guntur District. 522201 7. 7 Chandra Mohan Karumuru D.No.60-97-1, Nabikota, R.V.Nagar Post, Kadapa City and District 516003 8. Kasi Viswanadha Raju Alakunta 8 Dr.No.27-3-2, Rweddys Bazar, Near B.C. Colony, Burripalem Road, Tenali, Guntur District 522201 9. Subbalakshmi Nimmakayala C/o. V.Purushothama Rao, 10 Ramakrishna Homeo Hospita D.No.5-3-58, Konddappa Street, Pithapuram, East Godavari District 533450 10. Sreenivasulu Chennaiah Gari 11 H.No.87-1066, Ganesh Nagar-I, Kurnool Post, Kurnool Distrtict. 518002 11. Venkateshwarlu Vinjamuri H.No.8-2-338/1, Panchavati Co-Op 12 HSG Society, Road No3, Banjara Hills, Hyderabad. -

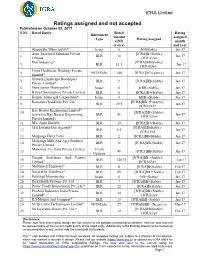

Ratings Assigned and Not Accepted Published on October 03, 2017 S.No Rated Entity Rated Rating Instrument Amount Assigned Type Rating Assigned (INR Month

ICRA Limited Ratings assigned and not accepted Published on October 03, 2017 S.No Rated Entity Rated Rating Instrument Amount assigned Type Rating assigned (INR month crores) and year 1 Alappuzha Municipality* Issuer 0 IrB(Stable) Jan-17 Aster Structural Solutions Private [ICRA]B-(Stable)/ 2 BLR 10 Jan-17 Limited [ICRA]A4 Dolf Industries* [ICRA]BB(Stable)/ 3 BLR 11.5 Jan-17 [ICRA]A4+ Fortis Healthcare Holdings Private 4 NCD/Debt 140 [ICRA]A(Negative) Jan-17 Limited* Grotech Landscape Developers 5 BLR 2 [ICRA]BB(Stable) Jan-17 Private Limited* 6 Guruvayoor Municipality* Issuer 0 IrBB-(Stable) Jan-17 7 Kalya Constructions Private Limited BLR 6 [ICRA]B+(Stable) Jan-17 8 Kannur Municipal Corporation* Issuer 0 IrBB+(Stable) Jan-17 Karnataka Roadlines Pvt. Ltd. [ICRA]BB+(Positive)/ 9 BLR 29.5 Jan-17 [ICRA]A4+ Kay Bouvet Engineering Limited* 10 [ICRA]BB-(Stable)/ (erstwhile Kay Bouvet Engineering BLR 41 Jan-17 [ICRA]A4 Private Limited) 11 M/s. Aone Enclave BLR 10 [ICRA]B+(Stable) Jan-17 M/S.Dwarka Das Agarwal* [ICRA]BB(Stable)/ 12 BLR 6.5 Jan-17 [ICRA]A4 13 Malganga Dairy Farm BLR 2 [ICRA]BB(Stable) Jan-17 Malganga Milk And Agro Products 14 BLR 11 [ICRA]BB-(Stable) Jan-17 Private Limited Manomay Tex India Private Limited Credit 15 49 [ICRA]BB(Stable) Jan-17 Opinion Unique Structures And Towers [ICRA]BB+(Stable)/ 16 BLR 120.31 Jan-17 Limited* [ICRA]A4+ 17 Multimech Engineers* BLR 8 [ICRA]B(Stable) Feb-17 18 Navalakha Translines* BLR 25 [ICRA]BB+(Stable) Feb-17 19 Palakkad Municipality Issuer 0 IrB+(Stable) Jan-17 20 Park Health Systems Pvt. -

Guntur Division - Jurisdiction Map Bommaipalli ( BMMP ) 8.60

To Kazipet South Central Railway Border at Km. 4.50 Pagidipalli ( PGDP ) 4.02 Guntur Division - Jurisdiction map Bommaipalli ( BMMP ) 8.60 Nagireddipalli ( NRDP ) 19.44 Reference 1. Sr.DEN/North/GNT Jurisdiction Valigonda ( VLG ) 29.47 a. ADEN/North/GNT Jurisdiction Ramannapet ( RMNP ) 42.12 Nalgonda b. ADEN/NLDA Jurisdiction Chityala ( CTYL ) 51.08 Telangana 2. DEN/West/GNT Jurisdiction Srirampuram ( SRMR ) 66.31 c. ADEN/West/GNT Jurisdiction d. ADEN/NDL Jurisdiction Nalgonda ( NLDA ) 76.71 3. Double line Thipparthi ( TPPI ) 94.11 Krishna River crossing @ Km. 138.75 Miryalaguda (MRGA)114.40 Janpahad(JNPD)(10.64) Kodrapol ( KDGL ) 125.92 Vishnupuram (VNUP) 134.97 Border at km. 25.36 Pondugala (PDGL) 143.78 Mangalagiri (MAG) 20.28 Piduguralla (PGRL) 74.10 Bellamkonda (BMKD) 60.42 Tummalacheruvu (TMLU) 83.34 Reddigudem (REM) 54.29 Namburu (NBR) 8.97 Vijayawada Jn..(BZA) Nadikude Jn.(NDKD) 152.69/95.25 Pedakakani (PDKN) 6.13 Gurajala (GZA) 106.98 Sattenapalli (SAP) 42.37 Pedakurapadu (PKPU) 29.64 Reddipalem (REP) 2.47 Rentachintala (RCA) 115.16 Nudurupadu (NDPU)Gudipudi (GPDE) 35.71 28.19 Lingamguntla (LIM) 26.56 Krishna canal Jn..(KCC) 423.71 Phirangipuram (PPM) 21.07Siripuram (SRPM) 22.96 Macherla (MCLA) 130.26 Narasaraopet (NRT) 45.30 Mandapadu Halt (MDPD) 18.84 Bandarupalli (BDPL) 13.58 Satulur (STUR) 34.29Perecherla (PRCA) 11.26 Mahabubnagar Cheekateegalapalem ( CEM ) Munumaka89.55 (MUK) 52.99 Nallapadu (NLPD) 5.00 Gundlakamma (GKM) 95.85 Tenali Jn.(TEL) 397.25 Chinaravuru (CIV) 2.91 Guntur Zampani (ZPI) 9.80 Kurichedu (KCD) 107.27 Vemuru (VMU) 13.77 Potlapadu (POO) 113.85 Jaggam Bhotla Krishnapuram (JBK) 176.94 Donakonda (DKD) 120.08 Gajjalakonda (GJJ) 130.78 Markapur Rd. -

Tenali Municipality

TENALI MUNICIPALITY E-NEWS LETTER March 2016 I wish to state that the Tenali Town in Guntur District is constituted into Municipality in the year 1909 with population of around 18,000. Tenali is also well known as ‘Andhra Paris’. The Archeological monuments revealed that the village ‘Teravali’ gradually became Tenali and it is also reputed for devotees, intellectuals, orators, artists and educationalists from ancient days. Tenali is one of the oldest Municipalities formed in 1909 and now is Special Grade Municipality with a population of 164937 as per 2011 census. The Municipality at present having an area of 16.63 Sq.kms. Tenali town is the 5th biggest urban centre in this region after Vijayawada, Guntur, Nellore and Ongole. The biggest Sangam dairy, Co-operative Sugar factory, Continental Coffee works, are situated very close to the town. The floating population to the town is at very high rate since Tenali is marketing place for Agriculture, Entertainment, Employment & Medical facilities etc. Tenali is located on the eastern coast of Andhra Pradesh at a distance of about 30 Kms from sea (Bay of Bengal) and lies at 16.250 North Latitude and 80.580 East Longitude. Tenali is located in the midst of wet lands irrigated under the Krishna Western Delta Canal System. Eastern Ghats lie on West and the town is in plain land. The average altitude above Mean Sea Level (MSL) is 11.00m. The annual average rainfall is 869.00mm receiving both North-East and South-West Monsoons. It is generally hot and humid during summer with temperatures ranging between 32-450 C.