Let's Play! 2020

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

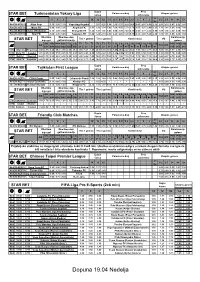

Dopuna 19.04 Nedelja

Dupla Prvo Poluvreme-kraj Ukupno golova STAR BET Turkmenistan Yokary Liga šansa poluvreme 2+ 1 X 2 1X 12 X2 1-1 X-1 X-X X-2 2-2 1 X 2 0-2 2-3 3+ 4+ 5+ 1p. Ned 14:00 5232 Altyn Asyr 1.15 5.90 13.0 Kopetdag Asgabat - 1.07 4.25 1.54 3.90 9.75 28.0 24.0 1.49 2.65 8.50 2.12 2.55 2.15 1.41 2.12 3.65 Pon 13:30 5709 Merw FK 2.90 3.00 2.25 Asgabat FK 1.51 1.29 1.31 5.00 7.00 4.55 5.70 3.70 3.55 1.97 2.80 2.95 1.70 1.91 1.96 3.60 7.60 Pon 14:00 5707Nebitci (FK Balkan) 2.15 2.80 3.40 Energetik FK 1.24 1.33 1.56 3.65 5.00 3.80 7.40 6.10 2.90 1.77 4.25 3.90 1.39 1.96 2.62 5.60 13.0 Pon 15:30 5708 Ahal FK 1.60 3.30 5.45 Sagadam FK 1.09 1.24 2.10 2.50 4.25 4.85 12.0 9.75 2.15 2.03 5.20 2.90 1.70 1.91 1.95 3.55 7.50 Oba tima Oba tima daju Kombinacije Tim 1 golova Tim 2 golova Kombinacije VG STAR BET daju gol gol kombinacije golova GG GG GG1& GG1/ 1 & 2 & T1 T1 T1 T2 T2 T2 1 & 2 & 1 & 2 & 1-1& 2-2& 1-1& 2-2& 1+I& 1+I& 2+I& GG 1>2 2>1 &3+ &4+ GG2 GG2 GG GG 2+ I 2+ 3+ 2+ I 2+ 3+ 3+ 3+ 4+ 4+ 3+ 3+ 4+ 4+ 1+II 2+II 2+II 5232 Altyn As Kopetdag 2.08 2.35 3.20 18.0 2.30 2.80 23.0 2.80 1.21 1.80 20.0 6.60 28.0 1.49 28.0 2.22 60.0 1.96 50.0 2.75 80.0 3.00 1.85 1.37 2.10 3.70 5709 Merw FK Asgabat 1.76 2.25 3.80 17.0 2.25 6.10 4.55 9.25 2.85 8.00 7.00 2.22 5.35 5.35 4.00 11.0 9.00 9.00 6.50 18.0 13.0 3.10 2.00 1.74 3.20 6.80 5707 Nebitci Energeti 2.22 3.10 5.90 29.0 2.90 5.80 9.00 9.00 2.62 7.00 14.0 4.15 14.0 4.75 7.90 13.0 19.0 7.70 14.0 17.0 35.0 3.25 2.07 2.15 4.50 11.0 5708 Ahal FK Sagadam 2.00 2.55 4.15 21.0 2.45 3.75 11.0 5.10 1.73 3.45 15.0 4.75 18.0 2.75 12.0 5.60 27.0 3.95 21.0 7.10 55.0 3.10 2.00 1.73 3.15 6.75 Dupla Prvo Poluvreme-kraj Ukupno golova STAR BET Tajikistan First League šansa poluvreme 2+ 1 X 2 1X 12 X2 1-1 X-1 X-X X-2 2-2 1 X 2 0-2 2-3 3+ 4+ 5+ 1p. -

Mistrzostwa Call of Duty World League (Cwl) Championship 2017, Prezentowane Przez Playstation® 4 Zaczynają Sie Już Dziś W Orlando

MISTRZOSTWA CALL OF DUTY WORLD LEAGUE (CWL) CHAMPIONSHIP 2017, PREZENTOWANE PRZEZ PLAYSTATION® 4 ZACZYNAJĄ SIE JUŻ DZIŚ W ORLANDO W pierwszych mistrzostwach w Call of Duty od Activision – obecnie najpopularniejszą konsolową dyscyplinę esportu – zmierzą się 32 najlepsze zespoły z Ameryki Północnej, Europy i Azji. Stawką rozgrywek toczących się w Amway Center będzie pula nagród wynoszącą 1,5 miliona dolarów. Będzie to kulminacja zmagań z całego sezonu o łączną pulę 4 milionów dolarów, największą jak dotąd w esportowj historii Call of Duty Bądź na bieżąco dzięki transmisjom online, 9 – 13 Sierpnia, tylko w MLG Santa Monica, Calif. – 10 sierpnia 2017 – Ponad 19000 graczy Call of Duty, najpopularniejszą konsolową dyscyplinę esportu – rywalizowało ze sobą przez cały rok, lecz tylko 32 zespoły mają szansę zmierzyć się w mistrzostwach Call of Duty World League (CWL) Championship, prezentowanych przez PlayStation 4 i rozpoczynających się już dziś w Amway Center w Orlando na Florydzie. W turnieju zorganizowanym przez Major League Gaming Corp. (MLG) przy współpracy z Activision Publishing, Inc. najlepsze zespoły na świecie z rejonów Ameryki Północnej, Europy i Azji (regionu APAC) będą walczyć o swoją cześć puli 1,5 miliona dolarów, tytuł Mistrzów CWL 2017 i miano najlepszej drużyny w Call of Duty na świecie. Rozgrywki z tego tygodnia wliczają się także do rocznej puli nagród, która jest najwyższą w historii turniejów Call of Duty i wynosi łącznie 4 miliony dolarów. “To był wspaniały rok dla Światowej Ligi Call of Duty, z jeszcze większą ilością graczy mierzących się ze sobą, zarówno tych profesjonalnych jak i dopiero zaczynających swoją esportową karierę,” powiedział Rob Kostich, wiceprezes i dyrektor naczelny Call of Duty. -

Gridiron Football League Draft Results 06-Feb-2007 12:51 PM Eastern

www.rtsports.com Gridiron Football League Draft Results 06-Feb-2007 12:51 PM Eastern Gridiron Football League Draft Sun., Aug 27 2006 5:52:00 PM Rounds: 20 Time Limit: Unlimited Round 1 Round 6 #1 St. Louis River Rats - Larry Johnson, RB, KAN #1 Boston Bulldogs - Plaxico Burress, WR, NYG #2 Reno Reservoir Dogs - LaDainian Tomlinson, RB, SDG #2 Minnesota Leftovers - Randy McMichael, TE, MIA #3 New York Mafia - Shaun Alexander, RB, SEA #3 Houston Outlaws - Matt Hasselbeck, QB, SEA #4 Oklahoma Wildcats - Tiki Barber, RB, NYG #4 Las Vegas Aces - Musa Smith, RB, BAL #5 Atlanta Grillz - Edgerrin James, RB, ARI #5 Miami Swamp Stompers - Alge Crumpler, TE, ATL #6 Miami Swamp Stompers - Ronnie Brown, RB, MIA #6 Atlanta Grillz - Jason Witten, TE, DAL #7 Las Vegas Aces - Carnell Williams, RB, TAM #7 Oklahoma Wildcats - Dallas Clark, TE, IND #8 Houston Outlaws - Rudi Johnson, RB, CIN #8 New York Mafia - Joey Galloway, WR, TAM #9 Minnesota Leftovers - Peyton Manning, QB, IND #9 Reno Reservoir Dogs - Donovan McNabb, QB, PHI #10 Boston Bulldogs - Steven Jackson, RB, STL #10 St. Louis River Rats - Braylon Edwards, WR, CLE Round 2 Round 7 #1 Boston Bulldogs - Reggie Bush, RB, NOR #1 St. Louis River Rats - Vince Young, QB, TEN #2 Minnesota Leftovers - LaMont Jordan, RB, OAK #2 Reno Reservoir Dogs - Warrick Dunn, RB, ATL #3 Houston Outlaws - Steve Smith, WR, CAR #3 New York Mafia - Tony Gonzalez, TE, KAN #4 Las Vegas Aces - Torry Holt, WR, STL #4 Oklahoma Wildcats - Jerramy Stevens, TE, SEA #5 Miami Swamp Stompers - Randy Moss, WR, OAK #5 Atlanta Grillz - Keyshawn Johnson, WR, CAR #6 Atlanta Grillz - Willie Parker, RB, PIT #6 Miami Swamp Stompers - Matt Jones, WR, JAC #7 Oklahoma Wildcats - Brian Westbrook, RB, PHI #7 Las Vegas Aces - Terry Glenn, WR, DAL #8 New York Mafia - Marvin Harrison, WR, IND #8 Houston Outlaws - Pittsburgh Steelers, Def, PIT #9 Reno Reservoir Dogs - Clinton Portis, RB, WAS #9 Minnesota Leftovers - Laurence Maroney, RB, NWE #10 St. -

Dodatok Za 13.04. Ponedelnik Конечен Рез

Двојна Прво Полувреме-крај Вкупно голови Sport Life Belarus 1 шанса полувреме 2+ 1 X 2 1X 12 X2 1-1 X-1 X-X X-2 2-2 1 X 2 0-2 2-3 3+ 4+ 5+ 1п. Пон 16:30 3537 Slavia-Mozyr 1.92 3.053.75 Rukh Brest 1.19 1.29 1.71 3.154.75 4.30 8.25 6.60 2.62 1.88 4.33 3.35 1.52 1.92 2.25 4.45 10.0 Двата тима Двата тима Комбиниран Тим 1 голови Тим 2 голови Комбинирани типови ППГ Sport Life даваат гол даваат гол комб. тип голови ГГ ГГГГ1& ГГ1/ 1 & 2 & T1 T1 T1 T2 T2 T2 1 & 2 & 1 & 2 & 1-1& 2-2& 1-1& 2-2& 1+I& 1+I& 2+I& ГГ 1>2 2>1 &3+ &4+ ГГ2 ГГ2 ГГ ГГ 2+ I 2+ 3+ 2+ I 2+ 3+ 3+ 3+ 4+ 4+ 3+ 3+ 4+ 4+ 1+II 2+II 2+II 3537Slavia-M Rukh Bre 2.04 2.70 4.8523.0 2.60 4.65 9.00 7.10 2.20 5.25 13.0 4.00 14.0 3.70 8.00 8.50 18.0 5.80 14.0 11.0 35.0 3.15 2.04 1.93 3.80 8.75 Двојна Прво Полувреме-крај Вкупно голови Sport Life Nicaragua Premiera Division шанса полувреме 2+ 1X2X 2 1X 12 1-1 X-1 X-X X-2 2-2 1 X 2 0-2 2-3 3+ 4+ 5+ 1п. -

Sports & Esports the Competitive Dream Team

SPORTS & ESPORTS THE COMPETITIVE DREAM TEAM JULIANA KORANTENG Editor-in-Chief/Founder MediaTainment Finance (UK) SPORTS & ESPORTS: THE COMPETITIVE DREAM TEAM 1.THE CROSSOVER: WHAT TRADITIONAL SPORTS CAN BRING TO ESPORTS Professional football, soccer, baseball and motor racing have endless decades worth of experience in professionalising, commercialising and monetising sporting activities. In fact, professional-services powerhouse KPMG estimates that the business of traditional sports, including commercial and amateur events, related media as well as education, academic, grassroots and other ancillary activities, is a US$700bn international juggernaut. Furthermore, the potential crossover with esports makes sense. A host of popular video games have traditional sports for themes. Soccer-centric games include EA’s FIFA series and Konami’s Pro Evolution Soccer. NBA 2K, a series of basketball simulation games published by a subsidiary of Take-Two Interactive, influenced the formation of the groundbreaking NBA 2K League in professional esports. EA is also behind the Madden NFL series plus the NHL, NBA, FIFA and UFC (Ultimate Fighting Championship) games franchises. Motor racing has influenced the narratives in Rockstar Games’ Grand Theft Auto, Gran Turismo from Sony Interactive Entertainment, while Psyonix’s Rocket League melds soccer and motor racing. SPORTS & ESPORTS THE COMPETITIVE DREAM TEAM SPORTS & ESPORTS: THE COMPETITIVE DREAM TEAM In some ways, it isn’t too much of a stretch to see why traditional sports should appeal to the competitive streaks in gamers. Not all those games, several of which are enjoyed by solitary players, might necessarily translate well into the head-to-head combat formats associated with esports and its millions of live-venue and online spectators. -

Draft Harris County – Houston Sports Authority

DRAFT HARRIS COUNTY – HOUSTON SPORTS AUTHORITY MINUTES OF THE BOARD OF DIRECTORS MEETING JUNE 24, 2020 STATE OF TEXAS } HARRIS COUNTY – HOUSTON } SPORTS AUTHORITY } A meeting of the Board of Directors (the “Board”) of the Harris County – Houston Sports Authority (the “Authority”), a sports and community venue district, was held virtually commencing at 10:00 a.m. on Wednesday, June 24, 2020. Written notices of the meeting, including the date, hour, place, agenda, and detailed instructions for connecting to the virtual meeting using Zoom Meetings, were posted in Harris, Fort Bend and Montgomery Counties in accordance with the Texas Open Meetings Act, and an electronic copy of the Agenda was posted on the Authority’s website, as well. Due to health and safety concerns related to COVID-19, this meeting was conducted virtually in accordance with the provisions of Section 551.127 of the Texas Government Code that have not been suspended by order of the Governor. The following Directors participated in the meeting: Chairman J. Kent Friedman, Directors Willie Alexander, Chad Burke, Joseph Callier, Lawrence Catuzzi, Cindy Clifford, Zina Garrison, Martye Kendrick, Dr. Juan Sanchez Munoz, Dr. Laura Murillo, Bruce Oakley, Tom Sprague and Robert Woods. Ms. Janis Burke, CEO for the Authority; Mr. Tom Waggoner, Controller for the Authority; Mr. Mark Arnold, Hunton Andrews Kurth LLP, Counsel for the Authority; Mr. Trey Cash and Ms. Tina Peterman, Masterson Advisors LLC, Financial Advisors for the Authority, were also present. Guests in attendance were: Commissioner Adrian Garcia, Harris County Precinct 2; Mr. Robert Belt, Mr. Mike Brotherton and Mr. Daniel Hebert from Belt Harris Pechachek LLLP, the Authority’s audit firm; Mr. -

GAMING ESPORT Trend Book

GAMING ESPORT & Trend book Wstęp właścicielami drużyn) i w końcu stworzyć i zre- dagować tekst. W ten sposób członkowie projek- W czerwcu 2017 zorganizowana została konfe- tu uczyli się pracy zespołowej, przekonywali jak rencja Esport & Gaming Forum. Organizatorom, ważna jest skrupulatność, punktualność i reali- MediaCom Beyond Advertising i sawik.tv udało zacja powierzonych zadań. Być może najważ- się dotrzeć z wydarzeniem do ponad pół tysią- niejsza była możliwość poznania innych osób ca osób z branży reklamowej, zainteresowa- o podobnych zainteresowaniach i celach. To nie- nych zdobyciem unikatowej wiedzy gamignowej wątpliwie będzie owocować w przyszłości. i esportowej. Finalnie dzięki wspólnemu wysił- kowi wszystkich prelegentów udało się nie tylko Musicie mieć państwo na względzie, że dokument stworzyć jedno z najważniejszych i największych tworzony był przez amatorów, z niewielkim do- tego typu wydarzeń na polskiej arenie, ale także świadczeniem, ale z wielką ambicją. Konsekwen- ustanowić pewne standardy na najbliższy czas. cją jest bardzo nierówny poziom merytoryczny W efekcie powstała także ta publikacja. artykułów. Niektóre teksty mają również wyraźne braki warsztatowe i językowe. Zdecydowaliśmy Raport, który trafia w Państwa ręce to dokument się jednak na publikację raportu w tej formie, bo o szczególnym, eksperymentalnym charakterze. charakter projektu jest eksperymentalny. Ważniejszy bowiem od samej treści jest proces jego powstawania. Prace nad tekstami, research, redakcja, skład, trwały przez ponad 6 miesięcy. W tym czasie -

Valorant Tournament Guidelines/Ruleset

Valorant Tournament Guidelines/Ruleset This competition is not affiliated with or sponsored by Riot Games, Inc. or VALORANT Esports. 1. Player Eligibility 1.1. Participating collegiate player(s) must fall under ALL of the listed criteria(s) to compete during CF1’s Collegiate Valorant tournament. 1.1.1. Players must be enrolled in classes full time at an accredited college or university. Graduate students are also eligible to participate as long as they also meet the university’s credit requirements for each semester. 1.1.2. Each player must maintain good academic standing at their college or university. If a player does not meet their schools academic requirements, they will be deemed ineligible for CF1 league play. Players must be verified eligible to participate by their appointed administrator contact. 1.1.3. Each player must be a minimum age of 18 years old. Players must be verified eligible to participate by their appointed administrator contact. 1.1.4. In order to be eligible to play in CF1, students must have residency or proof of enrollment in either the U.S. or Canada. Players must be verified eligible to participate by their appointed administrator contact. 1.2. In order to be approved for CF1 name usage and photographs, all players must sign a Media Release Form that confirms players name and likeness will be used solely for the promotion and broadcast of CF1 competition. 1.2.1. Media Release forms will be distributed to Coordinators on October 5th through our website and by email. 1.3. All players must agree to follow CF1’s Code of Conduct. -

Situación Actual Y Posición De La Industria

LOS ESPORTS EN ESPAÑA: SITUACIÓN ACTUAL Y POSICIÓN DE LA INDUSTRIA Índice 1. Presentación 5 2. Los esports en España 9 3. Los actores de los esports 17 4. Los esports y la COVID-19 25 5. Retos de los esports en España 29 Anexo: Posicionamiento común de la industria 33 del videojuego y de los esports 3 1. Presentación 5 Presentación La Asociación Española de Videojuegos (AEVI) es la asociación nacional de la industria del videojuego y de los esports. En ella se integran los principales actores de la industria de los esports en España: publishers (casas editoras) como Activision-Blizzard, Electronic Arts, Ubisoft o Riot Games; los propietarios de plata- formas de juego como Sony Interactive Entertainment (PlaySta- tion), Microsoft (Xbox) o Nintendo (Nintendo Switch); así como los principales organizadores de torneos a nivel español: LVP, ESL y GGTech, entre otros. AEVI tiene como objetivo el correcto desarrollo de la industria es- pañola del videojuego. Desde promover el desarrollo de la indus- tria a nivel local para favorecer la inversión, ayudar a las Adminis- traciones Públicas e instituciones para el impulsar el sector, velar por un modelo económico sostenible y de futuro, así como crear una imagen positiva de los videojuegos buscando promover un consumo plural y responsable. Con esta finalidad, AEVI ha presen- tado distintos documentos como el Libro blanco de los esports en España publicado en 2018 o el Posicionamiento común de la industria de los videojuegos y de los esports, actualizado en 2020, que se anexa a este documento. Entre los principales retos detectados, la industria ha señalado la necesidad de una mejora de las infraestructuras tecnológicas y en particular un mejor acceso a la banda ancha y a la tecnología 5G. -

Comunicacion Y Videojuegos.Pdf

COMUNICACIÓN Y VIDEOJUEGOS. REFLEJANDO LA SOCIEDAD A TRAVÉS DEL OCIO INTERACTIVO — Colección Comunicación y Pensamiento — COMUNICACIÓN Y VIDEOJUEGOS. REFLEJANDO LA SOCIEDAD A TRAVÉS DEL OCIO INTERACTIVO Editor Guillermo Paredes-Otero Autores (por orden de aparición) Guillermo Paredes-Otero Antonio César Moreno Cantano Carlos Álvarez Barroso Jesús Albarrán Ligero Antonio Fco. Campos Méndez Sergio Jesús Villén Higueras Augusto David Beltrán Poot Fernando Martínez López Rafael Jaén Pozo COMUNICACIÓN Y VIDEOJUEGOS. REFLEJANDO LA SOCIEDAD A TRAVÉS DEL OCIO INTERACTIVO Ediciones Egregius www.egregius.es Diseño de cubierta y maquetación: Francisco Anaya Benítez © de los textos: los autores © de la presente edición: Ediciones Egregius N.º 65 de la colección Comunicación y Pensamiento 1ª edición, 2020 ISBN 978-84-18167-35-5 NOTA EDITORIAL: Las opiniones y contenidos publicados en esta obra son de responsabilidad exclusiva de sus autores y no reflejan necesariamente la opinión de Ediciones Egregius ni de los editores o coordinadores de la publicación; asimismo, los autores se responsabilizarán de obtener el permiso correspondiente para incluir material publicado en otro lugar. Colección: Comunicación y Pensamiento Los fenómenos de la comunicación invaden todos los aspectos de la vida cotidiana, el acontecer contemporáneo es imposible de comprender sin la perspectiva de la comu- nicación, desde su más diversos ámbitos. En esta colección se reúnen trabajos acadé- micos de distintas disciplinas y materias científicas que tienen como elemento común la comunicación y el pensamiento, pensar la comunicación, reflexionar para com- prender el mundo actual y elaborar propuestas que repercutan en el desarrollo social y democrático de nuestras sociedades. La colección reúne una gran cantidad de trabajos procedentes de muy distintas partes del planeta, un esfuerzo conjunto de profesores investigadores de universidades e ins- tituciones de reconocido prestigio. -

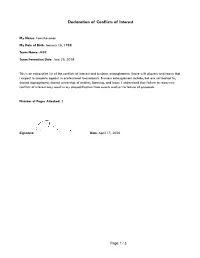

Declaration of Conflicts of Interest

Declaration of Conflicts of Interest My Name: Tomi Kovanen My Date of Birth: January 16, 1988 Team Name: MIBR Team Formation Date: June 23, 2018 This is an exhaustive list of the conflicts of interest and business entanglements I have with players and teams that I expect to compete against in professional tournaments. Business entanglement include, but are not limited to, shared management, shared ownership of entities, licensing, and loans. I understand that failure to report my conflicts of interest may result in my disqualification from events and/or forfeiture of proceeds. Number of Pages Attached: 2 Signature: Date: April 17, 2020 Page 1 / 3 Other party: ENCE Nature of conflict: IGC SVP Finance and Business Development Tomi Kovanen, who is among the senior leadership of the company overseeing the MIBR brand, is also a minority shareholder in ENCE, who were qualified for ESL One Rio de Janeiro and now compete in the RMR qualification system in Europe. Other party: YeaH Gaming Nature of conflict: MIBR parent company IGC has an agreement with YeaH. In exchange for a set annual fee payable regardless of actual roster changes, IGC has an option to buy out at most 2 players from YeaH Gaming’s roster in a calendar year at an agreed upon price. Other party: BLAST Premier and its partner teams (Natus Vincere, Astralis, Liquid, FaZe, Vitality, NiP, 100 Thieves, OG, G2, Evil Geniuses, Complexity) Nature of conflict: IGC (MIBR’s parent company) has a broad agreement for participation in BLAST Premier together with many other teams that are competing in various RMR regions to qualify for the Major. -

Welcome, We Have Been Archiving This Data for Research And

Welcome, To our MP3 archive section. These listings are recordings taken from early 78 & 45 rpm records. We have been archiving this data for research and preservation of these early discs. ALL MP3 files can be sent to you by email - $2.00 per song Scroll until you locate what you would like to have sent to you, via email. If you don't use Paypal you can send payment to us at: RECORDSMITH, 2803 IRISDALE AVE RICHMOND, VA 23228 Order by ARTIST & TITLE [email protected] H & H - Deep Hackberry Ramblers - Crowley Waltz Hackberry Ramblers - Tickle Her Hackett, Bobby - New Orleans Hackett, Buddy - Advice For young Lovers Hackett, Buddy - Chinese Laundry (Coral 61355) Hackett, Buddy - Chinese Rock and Egg Roll Hackett, Buddy - Diet Hackett, Buddy - It Came From Outer Space Hackett, Buddy - My Mixed Up Youth Hackett, Buddy - Old Army Routine Hackett, Buddy - Original Chinese Waiter Hackett, Buddy - Pennsylvania 6-5000 (Coral 61355) Hackett, Buddy - Songs My Mother Used to Sing To Who 1993 Haddaway - Life (Everybody Needs Somebody To Love) 1993 Haddaway - What Is Love Hadley, Red - Brother That's All (Meteor 5017) Hadley, Red - Ring Out Those Bells (Meteor 5017) 1979 Hagar, Sammy - (Sittin' On) The Dock Of The Bay 1987 Hagar, Sammy - Eagle's Fly 1987 Hagar, Sammy - Give To Live 1984 Hagar, Sammy - I Can't Drive 55 1982 Hagar, Sammy - I'll Fall In Love Again 1978 Hagar, Sammy - I've Done Everything For You 1978 1983 Hagar, Sammy - Never Give Up 1982 Hagar, Sammy - Piece Of My Heart 1979 Hagar, Sammy - Plain Jane 1984 Hagar, Sammy - Two Sides