Goldman, Sachs & Co

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

2.22.21 Laredo Petroleum Announces Fourth-Quarter 2020 Financial and Operating Results

15 West 6th Street, Suite 900 · Tulsa, Oklahoma 74119 · (918) 513-4570 · Fax: (918) 513-4571 www.laredopetro.com Laredo Petroleum Announces Fourth-Quarter and Full-Year 2020 Financial and Operating Results Provides 2021 Capital Budget and Production Expectations TULSA, OK - February 22, 2021 - Laredo Petroleum, Inc. (NYSE: LPI) ("Laredo" or the "Company") today announced its fourth-quarter and full-year 2020 financial and operating results. Full-Year 2020 Highlights • Fully transitioned development operations to Howard County acreage and successfully completed the Company's first well package • Added 4,000 net acres in Howard County at an average price of $7,200 per net undeveloped acre • Produced an average of 87,750 barrels of oil equivalent ("BOE") per day and 26,849 barrels of oil per day ("BOPD"), an increase of 8% and a decrease of 6%, respectively, from full-year 2019, while reducing capital expenditures by 27% over the same period • Reduced drilling and completions costs during the year by 21%, to $540 per foot from $680 per foot • Reduced unit lease operating expenses ("LOE") by 17% from full-year 2019 • Reduced unit general and administrative expenses ("G&A"), excluding long-term incentive plan expenses ("LTIP"), by 21% from full-year 2019 • Reduced volume of flared/vented natural gas by 58% from full-year 2019, flaring/venting only 0.71% of the Company's produced natural gas during full-year 2020 • Received $234.1 million from settlements of matured/terminated derivatives • Extended all term-debt maturities to 2025 and 2028 and repurchased $61 million of term-debt in open market purchases for 62.5% of par "Despite the unprecedented challenges of COVID and the resulting energy demand and commodity price weakness during 2020, the Laredo team adapted to working remotely and executed on the transformational strategy we communicated in November 2019," stated Jason Pigott, President and Chief Executive Officer. -

Athabasca Oil Corporation Takes Further Actions in Response to The

FOR IMMEDIATE RELEASE ‐ April 2, 2020 Athabasca Oil Corporation Takes Further Actions in Response to the Current Environment CALGARY – Athabasca Oil Corporation (TSX: ATH) (“Athabasca” or the “Company”) is taking further immediate actions in response to the significant decline in global oil prices to bolster balance sheet strength and corporate resiliency. Shut‐in of Hangingstone Asset Due to the significant decline in oil prices combined with the economic uncertainty associated to the ongoing COVID crisis, Athabasca has decided to suspend the Hangingstone SAGD operation. This suspension was initiated on April 2, 2020 and will involve shutting in the well pairs, halting steam injection to the reservoir, and taking measures to preserve the processing facility and pipelines in a safe manner so that it could be re‐started at a future date when the economy has recovered. The Hangingstone asset has an operating break‐even of approximately US$37.50 Western Canadian Select and this action is expected to significantly improve corporate resiliency in the current environment. As part of this action, Athabasca is reducing its corporate staff count by 15%. Hangingstone was Athabasca’s first operated oil sands project that began construction in 2013 and was commissioned in 2015. The Company would like to thank all staff that have worked hard over the years to bring this asset on stream. It is unfortunate that made‐in‐Alberta assets like Hangingstone cannot continue operations under current prices. Revised 2020 Guidance Annual corporate guidance is 30,000 – 31,500 boe/d and reflects a ~2,500 boe/d reduction related to the shut‐in. -

U.S.-Canada Cross- Border Petroleum Trade

U.S.-Canada Cross- Border Petroleum Trade: An Assessment of Energy Security and Economic Benefits March 2021 Submitted to: American Petroleum Institute 200 Massachusetts Ave NW Suite 1100, Washington, DC 20001 Submitted by: Kevin DeCorla-Souza ICF Resources L.L.C. 9300 Lee Hwy Fairfax, VA 22031 U.S.-Canada Cross-Border Petroleum Trade: An Assessment of Energy Security and Economic Benefits This report was commissioned by the American Petroleum Institute (API) 2 U.S.-Canada Cross-Border Petroleum Trade: An Assessment of Energy Security and Economic Benefits Table of Contents I. Executive Summary ...................................................................................................... 4 II. Introduction ................................................................................................................... 6 III. Overview of U.S.-Canada Petroleum Trade ................................................................. 7 U.S.-Canada Petroleum Trade Volumes Have Surged ........................................................... 7 Petroleum Is a Major Component of Total U.S.-Canada Bilateral Trade ................................. 8 IV. North American Oil Production and Refining Markets Integration ...........................10 U.S.-Canada Oil Trade Reduces North American Dependence on Overseas Crude Oil Imports ..................................................................................................................................10 Cross-Border Pipelines Facilitate U.S.-Canada Oil Market Integration...................................14 -

Canadian Crude Oil and Natural Gas Production and Supply Costs Outlook (2016 – 2036)

Study No. 159 September 2016 CANADIAN CANADIAN CRUDE OIL AND NATURAL GAS ENERGY PRODUCTION AND SUPPLY COSTS OUTLOOK RESEARCH INSTITUTE (2016 – 2036) Canadian Energy Research Institute | Relevant • Independent • Objective CANADIAN CRUDE OIL AND NATURAL GAS PRODUCTION AND SUPPLY COSTS OUTLOOK (2016 – 2036) Canadian Crude Oil and Natural Gas Production and Supply Costs Outlook (2016 – 2036) Authors: Laura Johnson Paul Kralovic* Andrei Romaniuk ISBN 1-927037-43-0 Copyright © Canadian Energy Research Institute, 2016 Sections of this study may be reproduced in magazines and newspapers with acknowledgement to the Canadian Energy Research Institute September 2016 Printed in Canada Front photo courtesy of istockphoto.com Acknowledgements: The authors of this report would like to extend their thanks and sincere gratitude to all CERI staff involved in the production and editing of the material, including but not limited to Allan Fogwill, Dinara Millington and Megan Murphy. *Paul Kralovic is Director, Frontline Economics Inc. ABOUT THE CANADIAN ENERGY RESEARCH INSTITUTE The Canadian Energy Research Institute is an independent, not-for-profit research establishment created through a partnership of industry, academia, and government in 1975. Our mission is to provide relevant, independent, objective economic research in energy and environmental issues to benefit business, government, academia and the public. We strive to build bridges between scholarship and policy, combining the insights of scientific research, economic analysis, and practical experience. For more information about CERI, visit www.ceri.ca CANADIAN ENERGY RESEARCH INSTITUTE 150, 3512 – 33 Street NW Calgary, Alberta T2L 2A6 Email: [email protected] Phone: 403-282-1231 Canadian Crude Oil and Natural Gas Production and Supply Costs Outlook iii (2016 – 2036) Table of Contents LIST OF FIGURES ............................................................................................................ -

PUBLIC DISCLOSURE DOCUMENT Proposed Development Plan OPTI

PUBLIC DISCLOSURE DOCUMENT Proposed Development Plan OPTI Canada Inc. & Nexen Inc. Long Lake Phase 2 SAGD Project July 2005 1.0 INTRODUCTION OPTI Canada Inc. and Nexen Inc. (OPTI/Nexen) are proposing to expand our Steam Assisted Gravity Drainage (SAGD) bitumen production at our Long Lake Project. This document has been prepared to inform you about our preliminary plans related to the proposed Long Lake Phase 2 SAGD Project (Phase 2). We encourage and welcome your input on this plan and your participation in the regulatory process. OPTI Canada and Nexen Inc. are joint-venture partners developing the Long Lake Project in the Athabasca oil sands region of northern Alberta. The Long Lake Project (Phase 1) is located on Lease 27, approximately 40 kilometres southeast of Fort McMurray, Alberta. Throughout the life of the Long Lake Project, we are committed to: • Understanding & addressing stakeholder concerns • Enhancing local employment & business development • Investing in communities to build capacity & self-sufficiency • Developing the Project in a safe & environmentally responsible manner Under the Memorandum of Understanding (IL 96-7) between the Alberta Energy and Utilities Board (EUB) and Alberta Environment (AENV) with respect to Oil Sands Developments, OPTI/Nexen will be filing a joint application related to the Long Lake Phase 2 SAGD Project to amend the following approvals: • Environmental Protection and Enhancement Act Approval No. 137467-00-00 • Oil Sands Conservation Act Approval No. 9151 We view the consultation process for the OPTI/Nexen Phase 2 Project as building on an ongoing co-operative approach with stakeholders that addresses such regional issues as fresh water conservation and protection, and air quality management. -

Negativliste. Fossil Energi

Negativliste. Fossil energi Maj 2021 Udstedende selskab 1 ABJA Investment Co Pte Ltd 2 ABM Investama Tbk PT 3 Aboitiz Equity Ventures Inc 4 Aboitiz Power Corp 5 Abraxas Petroleum Corp 6 Abu Dhabi National Energy Co PJSC 7 AC Energy Finance International Ltd 8 Adams Resources & Energy Inc 9 Adani Electricity Mumbai Ltd 10 Adani Power Ltd 11 Adani Transmission Ltd 12 Adaro Energy Tbk PT 13 Adaro Indonesia PT 14 ADES International Holding PLC 15 Advantage Oil & Gas Ltd 16 Aegis Logistics Ltd 17 Aenza SAA 18 AEP Transmission Co LLC 19 AES Alicura SA 20 AES El Salvador Trust II 21 AES Gener SA 22 AEV International Pte Ltd 23 African Rainbow Minerals Ltd 24 AGL Energy Ltd 25 Agritrade Resources Ltd 26 AI Candelaria Spain SLU 27 Air Water Inc 28 Akastor ASA 29 Aker BP ASA 30 Aker Solutions ASA 31 Aksa Akrilik Kimya Sanayii AS 32 Aksa Enerji Uretim AS 33 Alabama Power Co 34 Alarko Holding AS 35 Albioma SA 36 Alexandria Mineral Oils Co 37 Alfa Energi Investama Tbk PT 38 ALLETE Inc 1 39 Alliance Holdings GP LP 40 Alliance Resource Operating Partners LP / Alliance Resource Finance Corp 41 Alliance Resource Partners LP 42 Alliant Energy Corp 43 Alpha Metallurgical Resources Inc 44 Alpha Natural Resources Inc 45 Alta Mesa Resources Inc 46 AltaGas Ltd 47 Altera Infrastructure LP 48 Altius Minerals Corp 49 Altus Midstream Co 50 Aluminum Corp of China Ltd 51 Ameren Corp 52 American Electric Power Co Inc 53 American Shipping Co ASA 54 American Tanker Inc 55 AmeriGas Partners LP / AmeriGas Finance Corp 56 Amplify Energy Corp 57 Amplify Energy Corp/TX 58 -

Form 8-K Laredo Petroleum, Inc

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 8-K CURRENT REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 Date of report (Date of earliest event reported): January 6, 2020 LAREDO PETROLEUM, INC. (Exact Name of Registrant as Specified in Charter) Delaware 001-35380 45-3007926 (State or Other Jurisdiction of Incorporation or (Commission File Number) (I.R.S. Employer Identification No.) Organization) 15 W. Sixth Street, Suite 900, Tulsa, Oklahoma 74119 (Address of Principal Executive Offices) (Zip Code) Registrant’s telephone number, including area code: (918) 513-4570 Not Applicable (Former Name or Former Address, if Changed Since Last Report) Check the appropriate box below if the Form 8-K filing is intended to simultaneously satisfy the filing obligation of the registrant under any of the following provisions: ¨ Written communications pursuant to Rule 425 under the Securities Act (17 CFR 230.425) ¨ Soliciting material pursuant to Rule 14a-12 under the Exchange Act (17 CFR 240-14a-12) ¨ Pre-commencement communications pursuant to Rule 14d-2(b) under the Exchange Act (17 CFR 240.14d-2(b)) ¨ Pre-commencement communications pursuant to Rule 13e-4(c) under the Exchange Act (17 CFR 240.13e-4(c)) Securities registered pursuant to Section 12(b) of the Act: Title of each class Trading Symbol(s) Name of each exchange on which registered Common Stock, $0.01 par value LPI New York Stock Exchange Indicate by check mark whether the registrant is an emerging growth company as defined in Rule 405 of the Securities Act of 1933 (§230.405 of this chapter) or Rule 12b-2 of the Securities Exchange Act of 1934 (§240.12b-2 of this chapter). -

Pipeline and Processing Fac... - Pipeline Projects with Length Greater Than 20 Miles

12/29/2015 Pipeline and Processing Fac... - Pipeline projects with Length Greater than 20 Miles Pipeline projects with DEC-29-2015 Pipeline and Processing Facilities : SAVED REPORTS Length Greater than 1:37 PM 20 Miles Pipeline projects with Length Greater than 20 Miles Holding Company or Parent Operating Company: Project Status Project Project Name: Length Organization: Type: (New Miles) AK (6 Pipeline projects) Energia Cura Fairbanks Pipeline Doubtful New Arctic Fox (Fairbanks Pipeline) 443 Company Linc Energy Linc Energy On New Umiat Oil Field Pipeline 80 Hold/Postponed Alaska Housing Finance Alaska Gasline On New Alaska Stand Alone Pipeline (ASAP) 737 Corporation Development Hold/Postponed Corporation BP BP Under New Point Thomson Gas Field 22 Construction NovaGold Resources Inc. Donlin Gold, LLC Advanced New Donlin Gold 312 Development Alaska LNG Early New Alaska LNG (AKLNG) 800 Development TOT 2,394 AL (6 Pipeline projects) Southern Company Alabama Power Under New Gaston Natural Gas Pipeline 30 Construction Spectra Energy Spectra Energy Advanced New Sabal Trail 515 Development Williams Company Transcontinental Gas Early New Hillabee Expansion Project Phase 1 20 Pipeline Company LLC Development Miller Energy Resources Early New Trans - Foreland Pipeline (TFPL) system 23 Development Laclede Gas Alagasco On-going Replacement Alagasco Pipeline replacement program 850 PRP Williams Company Transcontinental Gas Early New Hillabee Expansion Project Phase 2 and 3 24 Pipeline Company LLC Development TOT 1,462 Alberta (43 Pipeline projects) TransCanada Imperial Oil Early New Mackenzie Gas Project 758 Development Enbridge Inc. Enbridge Income Fund Advanced New Northern Gateway Pipeline (westward 731 Development crude for export) TransCanada TransCanada Advanced New Keystone XL 1,661 Development Enhance Energy Inc. -

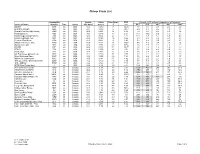

Chicap-Crude-List-7-15-2020.Pdf

Chicap Crude List Commodity Gravity Sulfur Pour Point RVP Viscosity (cST) at listed temperature in Fahrenheit Crude Oil Name Identifier Type Origin °API @60°F mass% °F psi 40°F 50°F 68°F 86°F 104°F Bakken BAK sw USA 42.5 0.080 -71 10.21 4.1 3.6 2.9 2.5 2.0 Grand Mesa Light GML sw USA 48.7 0.060 5 10.67 2.9 2.7 2.2 1.9 1.6 Grand Mesa Sweet@Cushing GMS sw USA 40.2 0.206 32 8.26 7.2 6.0 4.6 3.6 3.0 Mississippi Lime MSL sw USA 34.3 0.519 -11 6.27 16.1 13.2 9.6 7.2 6 Niobrara @Cushing Pony PL NIB sw USA 37.5 0.402 27 8.11 11.1 8.8 6.7 5.1 4.0 Niobrara @Saddlehorn SSC sw USA 43.2 0.144 -38 9.55 5.3 4.5 3.5 2.8 2.3 Permian Sour Blend PRM sw USA 41.9 0.281 -6 8.03 5.1 4.4 3.5 2.8 2.3 Saddlehorn Intermediate SHM sw USA 42.5 0.137 21 10.67 5.6 4.9 3.8 3.1 2.6 Saddlehorn Light SHL sw USA 48.4 0.058 -33 10.54 2.8 2.5 2.1 1.8 1.6 SCOOP SCP sw USA 54.4 0.015 -71 10.77 2.0 1.8 1.6 1.4 1.2 STACK STK sw USA 41.9 0.079 -22 9.71 7.1 6.4 4.9 4.0 3.2 Stack Light STL sw USA 47.4 0.022 5 8.17 3.6 3.3 2.7 2.3 2.0 US High Sweet @Clearbrook UHC sw USA 42.1 0.120 -71 9.78 4.7 4.1 3.2 2.6 2.2 West Oklahoma Sweet WOS sw USA 49.0 0.025 -38 7.84 3.1 2.8 2.3 1.9 1.7 Whitecliffs Condensate WCC sw USA 48.5 0.141 -71 8.82 2.5 2.5 2.1 1.9 1.6 WTI @Cushing - Domestic Sweet DSW sw USA 41.2 0.400 -38 7.69 6.7 5.7 4.4 3.5 2.8 WTI - Midland WTM sw USA 43.6 0.163 -11 7.13 5.3 4.5 3.4 2.7 2.3 WTS (West Texas Sour) C so USA 32.9 1.64 -23 5.67 18.0 14.3 9.9 7.2 5.5 Access Western Blend AWB H Canada 21.6 3.79 -46 6.67 672 457 248 145 91.0 Albian Heavy Synthetic AHS H Canada 20.0 -

Laredo Petroleum Announces William Albrecht to Succeed Randy Foutch As Chairman of the Board of Directors

Laredo Petroleum Announces William Albrecht to Succeed Randy Foutch as Chairman of the Board of Directors May 18, 2020 TULSA, OK, May 18, 2020 (GLOBE NEWSWIRE) -- Laredo Petroleum, Inc. (NYSE: LPI) ("Laredo" or "the Company"), today announced the appointment of William Albrecht as independent Chairman of the Board of Directors (the "Board"), succeeding Randy Foutch upon the expiration of Mr. Foutch's term on May 14, 2020. Mr. Albrecht, currently an independent member of the Board, will continue to serve on the Compensation Committee and Nominating and Corporate Governance Committee. "Bill's appointment as Chairman fulfills Laredo's prior commitment to separate the roles of Chairman and Chief Executive Officer and name an independent Chairman," stated Dr. Bill Scoggins, Chair of the Nominating and Corporate Governance Committee. "His extensive energy industry background and leadership experience will be instrumental in providing guidance to Laredo's leadership team in these unprecedented times." "Since joining our Board in February, Bill's insight and perspective have been crucial to shaping our strategy," commented Jason Pigott, President and Chief Executive Officer. "I look forward to continuing to work closely with him as we position Laredo for long-term, sustainable growth." Mr. Albrecht has served on Laredo's Board since February 2020. Additionally, he currently serves as Chairman of the Board of California Resources Corporation (NYSE: CRC) and as a member of the Boards of Halliburton (NYSE: HAL) and Valaris (NYSE: VAL). "Speaking on behalf of the entire Board, I would like to thank Randy for his tireless commitment to building Laredo Petroleum," continued Mr. Pigott. -

ETP & SXL Project Summary

ENERGY TRANSFER EQUITY & ENERGY TRANSFER PARTNERS DISCLAIMER This presentation relates to a presentation the management of Energy Transfer Equity, L.P. (ETE) and Energy Transfer Partners, L.P. (ETP) will give to investors on September 7, 2016. At this meeting, members of the Partnerships’ management may make statements about future events, outlook and expectations related to Energy Transfer Partners, L.P. (ETP), Sunoco Logistics Partners L.P. (SXL), Panhandle Eastern Pipe Line Company, LP (PEPL), Sunoco LP (SUN), and ETE (collectively, the Partnerships), and their subsidiaries and this presentation may contain statements about future events, outlook and expectations related to the Partnerships and their subsidiaries all of which statements are forward-looking statements. Any statement made by a member of management of the Partnerships at this meeting and any statement in this presentation that is not a historical fact will be deemed to be a forward-looking statement. These forward-looking statements rely on a number of assumptions concerning future events that members of management of the Partnerships believe to be reasonable, but these statements are subject to a number of risks, uncertainties and other factors, many of which are outside the control of the Partnerships. While the Partnerships believe that the assumptions concerning these future events are reasonable, we caution that there are inherent risks and uncertainties in predicting these future events that could cause the actual results, performance or achievements of the Partnerships and their subsidiaries to be materially different. These risks and uncertainties are discussed in more detail in the filings made by the Partnerships with the Securities and Exchange Commission, copies of which are available to the public. -

SUNOCO LP (Exact Name of Registrant As Specified in Its Charter)

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 10-K (Mark one) x ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the Fiscal Year Ended: December 31, 2015 or o TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the transition period from to Commission File Number: 001-35653 SUNOCO LP (Exact name of registrant as specified in its charter) Delaware 30-0740483 (State or other jurisdiction of (I.R.S. Employer incorporation or organization) Identification Number) 555 East Airtex Drive Houston, TX 77073 (Address of principal executive offices, including zip code) Registrant's telephone number, including area code: (832) 234-3600 (Former Name, former address and former fiscal year, if changed since last report) Securities registered pursuant to Section 12(b) of the Act: Title of each class Name of each exchange on which registered Common Units Representing Limited Partner Interests New York Stock Exchange (NYSE) Securities registered pursuant to Section 12(g) of the Act: NONE Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes x No o Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes o No x Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.