ETP & SXL Project Summary

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Would You Like to Write ''The Formation of Perhydrophenalenes and Polyalkyladamantanes by Lsomerization of Tricyclic Perhydroaromatics ?''

would you like to write ''The Formation of Perhydrophenalenes and Polyalkyladamantanes by lsomerization of Tricyclic Perhydroaromatics ?'' How's that again? Well, never mind Athabasca oil sands project in North ings in Exploration, Production, -Bob Warren, Ed Janoski, and Abe ern Alberta to multiply the world's Manufacturing, Research, Engineer Schneider already wrote it. They're petroleum resources; plan a new $125 ing, Sales, Accounting, Economics, chemists in Sun Oil Company's Re million processing facility in Puerto and Computer Operation. Locations search and Development Department. Rico; expand the Toledo Refinery to - Philadelphia, Toledo and Dallas Their paper is just one of many re the tune of $50 million; sponsor the areas. sulting from imaginative and origi "Sunoco Special" and the racing team You may write us for an appoint nal basic research conducted at Sun of Roger Penske and Mark Donohue ment, write for our book "Sunoco Oil. in big league sports car racing to Career Opportunities Guide," or con Maybe basic research and technical competition-prove and improve Sun tact your College Placement Director papers aren't your cup of tea. But oco products for the public; pursue a to see Sun's representative when on isn't the kind of company that in continuing program for air and water campus. SUN OIL COMPANY, Indus vests in and encourages such projects pollution control; beautify Sunoco trial Relations Dept. CED, 1608 Wal the kind of company you'd like to service stations everywhere. nut Street, Philadelphia, Pa.19103 or work for? Sunoco is geared for growth. We P . O. Box 2880, Dallas, Texas 75221. -

Conocophillips: Rule 14A-8 No-Action Letter

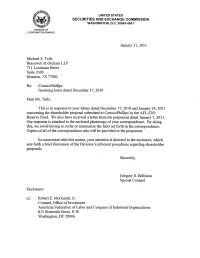

UNITED STATES SECURITIES AND EXCHANGE COMMISSION WASHINGTON, D.C. 20549-4561 Januar 31, 2011 Michael S. Telle Bracewell & Giuliani LLP 711 Louisiana Street Suite 2300 Houston, TX 77002 Re: ConocoPhillps . Incoming letter dated December 17, 2010 Dear Mr. Telle: Ths is in response to your letters dated December 17, 2010 and Janua 24,2011 concernng the shareholder proposal submitted to ConocoPhillps by the AFL-CIO Reserve Fund. We also have received a lttter from the proponent dated Januar 7, 201l. our response is attached to the enclosed photocopy of your correspondence. By doing this, we avoid having to recite or sumarze the facts set forth in the correspondence. Copies of all of the correspondence also will be provided to the proponent. In connection with this matter, your attention is directed to the enclosure, which sets forth a brief discussion ofthe Division's informal procedures regarding shareholder proposals. Sincerely, Gregory S. Bellston Special Counsel Enclosures cc: Robert E. McGarrah, Jr. Counsel, Office of Investment American Federation of Labor and Congress of Industrial Organizations 815 Sixteenth Street, N.W. Washington, DC 20006 Januar 31, 2011 Response of the Office of Chief Counsel Division of Corporation Finance Re: ConocoPhilips Incoming letter dated December 17, 2010 The proposal requests that the board prepare a report on the steps the company has taen to reduce the risk of accidents. The proposal fuher specifies that the report should describe the board's oversight of process safety management, staffing levels, inspection and maintenance of refineries and other equipment. Weare unable to concur in your view that ConocoPhilips may exclude the proposal under rule 14a-8(i)(10). -

Marathon Agreement

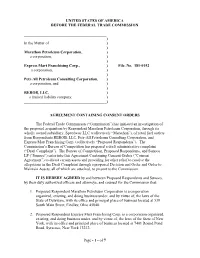

UNITED STATES OF AMERICA BEFORE THE FEDERAL TRADE COMMISSION __________________________________________ ) In the Matter of ) ) Marathon Petroleum Corporation, ) a corporation, ) ) Express Mart Franchising Corp., ) File. No. 181-0152 a corporation, ) ) Petr-All Petroleum Consulting Corporation, ) a corporation, and ) ) REROB, LLC, ) a limited liability company. ) __________________________________________) AGREEMENT CONTAINING CONSENT ORDERS The Federal Trade Commission (“Commission”) has initiated an investigation of the proposed acquisition by Respondent Marathon Petroleum Corporation, through its wholly owned subsidiary, Speedway LLC (collectively “Marathon”), of retail fuel outlets from Respondents REROB, LLC, Petr-All Petroleum Consulting Corporation, and Express Mart Franchising Corp. (collectively “Proposed Respondents”). The Commission’s Bureau of Competition has prepared a draft administrative complaint (“Draft Complaint”). The Bureau of Competition, Proposed Respondents, and Sunoco LP (“Sunoco”) enter into this Agreement Containing Consent Orders (“Consent Agreement”) to divest certain assets and providing for other relief to resolve the allegations in the Draft Complaint through a proposed Decision and Order and Order to Maintain Assets, all of which are attached, to present to the Commission. IT IS HEREBY AGREED by and between Proposed Respondents and Sunoco, by their duly authorized officers and attorneys, and counsel for the Commission that: 1. Proposed Respondent Marathon Petroleum Corporation is a corporation organized, existing, and doing business under, and by virtue of, the laws of the State of Delaware, with its office and principal place of business located at 539 South Main Street, Findlay, Ohio 45840. 2. Proposed Respondent Express Mart Franchising Corp. is a corporation organized, existing, and doing business under, and by virtue of, the laws of the State of New York, with its office and principal place of business located at 7401 Round Pond Road, Syracuse, New York 13212. -

Sunoco Pipeline L.P

Sunoco Pipeline L.P. 1300 Main St. Houston, TX 77002 Phone: (713) 989-7000 Website: www.energytransfer.com Energy Transfer Partners, a Texas-based energy company founded in 1995 as EMERGENCY CONTACT: a small intrastate natural gas pipeline 1-800-786-7440 or 877-839-7473 company, is now one of the largest and most diversified master limited PRODUCTS/DOT GUIDEBOOK ID#/GUIDE#: PRODUCTS/DOT GUIDEBOOK ID#/GUIDE#: partnerships in the United States. Butane 1011 115 Light Cycle Oil 1993 128 Strategically positioned in all of the major Ethane 1035 115 Propane 1075 115 U.S. production basins, the company Fuel Oil 1993 128 Diesel owns and operates a geographically Fuel, Aviation, (Ultra Low Sulfur) 1993 128 diverse portfolio of energy assets, Turbine Engine Kerosene (Ultra Low Sulfur) 1223 128 including midstream, intrastate and (Jet Fuel or Jet A) 1863 128 interstate transportation and storage Gasoline 1203 128 assets. Energy Transfer operates more than 90,000 miles of natural DELAWARE & PHILADELPHIA COUNTIES ONLY: gas, crude oil, natural gas liquids and PRODUCTS/DOT GUIDEBOOK ID#/GUIDE#: PRODUCTS/DOT GUIDEBOOK ID#/GUIDE#: refined products pipelines and related Crude Oil 1267 128 Naphtha, Petroleum facilities, including terminalling, storage, Alkylate (Light Alkylate (Gasoline Components) 1255 128 fractionation, blending and various Naphtha and Benzene) 1203 128 Raffinate acquisition and marketing assets in 38 Butane (N-Butane) 1075 115 (Naphtha, solvent) 1256 128 states. Butane-Butylene 1075 115 Reformate Cat. Gasoline 1203 128 (Naphtha petroleum) 1255 128 • Intrastate Transportation and Storage Isobutane 1075 115 Udex Feed Operations – approximately 7,900 (Benzene-rich Reformate) 1255 128 miles of natural gas pipelines and three storage facilities. -

Negativliste. Fossil Energi

Negativliste. Fossil energi Maj 2021 Udstedende selskab 1 ABJA Investment Co Pte Ltd 2 ABM Investama Tbk PT 3 Aboitiz Equity Ventures Inc 4 Aboitiz Power Corp 5 Abraxas Petroleum Corp 6 Abu Dhabi National Energy Co PJSC 7 AC Energy Finance International Ltd 8 Adams Resources & Energy Inc 9 Adani Electricity Mumbai Ltd 10 Adani Power Ltd 11 Adani Transmission Ltd 12 Adaro Energy Tbk PT 13 Adaro Indonesia PT 14 ADES International Holding PLC 15 Advantage Oil & Gas Ltd 16 Aegis Logistics Ltd 17 Aenza SAA 18 AEP Transmission Co LLC 19 AES Alicura SA 20 AES El Salvador Trust II 21 AES Gener SA 22 AEV International Pte Ltd 23 African Rainbow Minerals Ltd 24 AGL Energy Ltd 25 Agritrade Resources Ltd 26 AI Candelaria Spain SLU 27 Air Water Inc 28 Akastor ASA 29 Aker BP ASA 30 Aker Solutions ASA 31 Aksa Akrilik Kimya Sanayii AS 32 Aksa Enerji Uretim AS 33 Alabama Power Co 34 Alarko Holding AS 35 Albioma SA 36 Alexandria Mineral Oils Co 37 Alfa Energi Investama Tbk PT 38 ALLETE Inc 1 39 Alliance Holdings GP LP 40 Alliance Resource Operating Partners LP / Alliance Resource Finance Corp 41 Alliance Resource Partners LP 42 Alliant Energy Corp 43 Alpha Metallurgical Resources Inc 44 Alpha Natural Resources Inc 45 Alta Mesa Resources Inc 46 AltaGas Ltd 47 Altera Infrastructure LP 48 Altius Minerals Corp 49 Altus Midstream Co 50 Aluminum Corp of China Ltd 51 Ameren Corp 52 American Electric Power Co Inc 53 American Shipping Co ASA 54 American Tanker Inc 55 AmeriGas Partners LP / AmeriGas Finance Corp 56 Amplify Energy Corp 57 Amplify Energy Corp/TX 58 -

Pipeline and Processing Fac... - Pipeline Projects with Length Greater Than 20 Miles

12/29/2015 Pipeline and Processing Fac... - Pipeline projects with Length Greater than 20 Miles Pipeline projects with DEC-29-2015 Pipeline and Processing Facilities : SAVED REPORTS Length Greater than 1:37 PM 20 Miles Pipeline projects with Length Greater than 20 Miles Holding Company or Parent Operating Company: Project Status Project Project Name: Length Organization: Type: (New Miles) AK (6 Pipeline projects) Energia Cura Fairbanks Pipeline Doubtful New Arctic Fox (Fairbanks Pipeline) 443 Company Linc Energy Linc Energy On New Umiat Oil Field Pipeline 80 Hold/Postponed Alaska Housing Finance Alaska Gasline On New Alaska Stand Alone Pipeline (ASAP) 737 Corporation Development Hold/Postponed Corporation BP BP Under New Point Thomson Gas Field 22 Construction NovaGold Resources Inc. Donlin Gold, LLC Advanced New Donlin Gold 312 Development Alaska LNG Early New Alaska LNG (AKLNG) 800 Development TOT 2,394 AL (6 Pipeline projects) Southern Company Alabama Power Under New Gaston Natural Gas Pipeline 30 Construction Spectra Energy Spectra Energy Advanced New Sabal Trail 515 Development Williams Company Transcontinental Gas Early New Hillabee Expansion Project Phase 1 20 Pipeline Company LLC Development Miller Energy Resources Early New Trans - Foreland Pipeline (TFPL) system 23 Development Laclede Gas Alagasco On-going Replacement Alagasco Pipeline replacement program 850 PRP Williams Company Transcontinental Gas Early New Hillabee Expansion Project Phase 2 and 3 24 Pipeline Company LLC Development TOT 1,462 Alberta (43 Pipeline projects) TransCanada Imperial Oil Early New Mackenzie Gas Project 758 Development Enbridge Inc. Enbridge Income Fund Advanced New Northern Gateway Pipeline (westward 731 Development crude for export) TransCanada TransCanada Advanced New Keystone XL 1,661 Development Enhance Energy Inc. -

SUNOCO LP (Exact Name of Registrant As Specified in Its Charter)

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 10-K (Mark one) x ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the Fiscal Year Ended: December 31, 2015 or o TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the transition period from to Commission File Number: 001-35653 SUNOCO LP (Exact name of registrant as specified in its charter) Delaware 30-0740483 (State or other jurisdiction of (I.R.S. Employer incorporation or organization) Identification Number) 555 East Airtex Drive Houston, TX 77073 (Address of principal executive offices, including zip code) Registrant's telephone number, including area code: (832) 234-3600 (Former Name, former address and former fiscal year, if changed since last report) Securities registered pursuant to Section 12(b) of the Act: Title of each class Name of each exchange on which registered Common Units Representing Limited Partner Interests New York Stock Exchange (NYSE) Securities registered pursuant to Section 12(g) of the Act: NONE Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes x No o Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes o No x Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. -

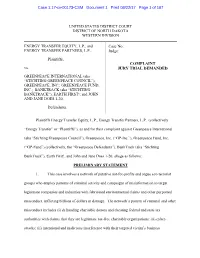

Case 1:17-Cv-00173-CSM Document 1 Filed 08/22/17 Page 1 of 187

Case 1:17-cv-00173-CSM Document 1 Filed 08/22/17 Page 1 of 187 UNITED STATES DISTRICT COURT DISTRICT OF NORTH DAKOTA WESTERN DIVISION ENERGY TRANSFER EQUITY, L.P., and Case No.: ___________ ENERGY TRANSFER PARTNERS, L.P., Judge: ___________ Plaintiffs, COMPLAINT vs. JURY TRIAL DEMANDED GREENPEACE INTERNATIONAL (aka “STICHTING GREENPEACE COUNCIL”); GREENPEACE, INC.; GREENPEACE FUND, INC.; BANKTRACK (aka “STICHTING BANKTRACK”); EARTH FIRST!; and JOHN AND JANE DOES 1-20, Defendants. Plaintiffs Energy Transfer Equity, L.P., Energy Transfer Partners, L.P. (collectively “Energy Transfer” or “Plaintiffs”), as and for their complaint against Greenpeace International (aka “Stichting Greenpeace Council”), Greenpeace, Inc. (“GP-Inc.”), Greenpeace Fund, Inc. (“GP-Fund”) (collectively, the “Greenpeace Defendants”), BankTrack (aka “Stichting BankTrack”), Earth First!, and John and Jane Does 1-20, allege as follows: PRELIMINARY STATEMENT 1. This case involves a network of putative not-for-profits and rogue eco-terrorist groups who employ patterns of criminal activity and campaigns of misinformation to target legitimate companies and industries with fabricated environmental claims and other purported misconduct, inflicting billions of dollars in damage. The network’s pattern of criminal and other misconduct includes (i) defrauding charitable donors and cheating federal and state tax authorities with claims that they are legitimate tax-free charitable organizations; (ii) cyber- attacks; (ii) intentional and malicious interference with their targeted victim’s business Case 1:17-cv-00173-CSM Document 1 Filed 08/22/17 Page 2 of 187 relationships; and (iv) physical violence, threats of violence and the purposeful destruction of private and federal property. Energy Transfer is the latest legitimate business targeted by this network. -

Fossilized Finance

Fossilized Finance How Canada’s banks still enable oil and gas production By Donald Gutstein APRIL 2021 Fossilized Finance HOW CANADA’S BANKS STILL ENABLE OIL AND GAS PRODUCTION By Donald Gutstein April 2021 This paper is part of the Corporate Mapping Project (CMP), a research and public engagement initiative investigating the power of the fossil fuel industry. The CMP is jointly led by the University of Victoria, Canadian Centre for Policy Alternatives and the Parkland Institute. This research was supported by the Social Science and Humanities Research Council of Canada (SSHRC). For more information visit corporatemapping.ca. PUBLISHING TEAM Shannon Daub, Jean Kavanagh, Emira Mears, Terra Poirier Copyedit: Dawn Loewen Layout: Susan Purtell Cover design: Paula Grasdal ISBN 978-1-77125-545-5 This report is available under limited copyright protection. You may download, distribute, photocopy, cite or excerpt this document provided it is properly and fully credited and not used for commercial purposes. The opinions and recommendations in this report, and any errors, are those of the author, and do not necessarily reflect the views of the publishers and the funders of this report. 520 – 700 West Pender Street Vancouver, BC V6C 1G8 604.801.5121 | [email protected] policyalternatives.ca The CCPA–BC is located on unceded Coast Salish territory, including the lands belonging to the xwməθwəýəm (Musqueam), Skwxwú7mesh (Squamish) and səÍílwətaʔɬ /Selilwitulh (Tsleil-Waututh) Nations. ABOUT THE AUTHOR DONALD GUTSTEIN is a writer and researcher, retired after teaching for 30 years in the Simon Fraser University School of Communication. He is the author of six books, most recently The Big Stall: How Big Oil and Think Tanks Are Blocking Action on Climate Change in Canada. -

PES Holdings, LLC Enters Into Restructuring Support Agreement to Create Sustainable Financial Foundation

1735 Market Street Philadelphia, PA 19103 | 215 339 1200 www.pes-companies.com PES Holdings, LLC Enters Into Restructuring Support Agreement to Create Sustainable Financial Foundation Agreement Provides $260 Million in New Financing From Term B Lenders and Owners PES Expects to Complete Recapitalization Through Prepackaged Court Process While Continuing Operations Without Interruption Employee Pay and Benefits to Continue as Usual and Vendors to be Paid in Ordinary Course of Business Before and During Court Process Philadelphia, PA. (January 22, 2018) – PES Holdings, LLC (“PES Holdings” or the “Company”), a subsidiary of Philadelphia Energy Solutions LLC (“PES LLC”), announced today that it has entered into a Restructuring Support Agreement (“RSA” or the “Agreement”) with the holders of 100% of the Company’s outstanding Term A debt and more than 90% of the Company’s outstanding Term B debt. In addition to restructuring existing debt and receiving relief from current debt service obligations, the Company has secured access to $260 million in new financing comprising $120 million in debtor-in-possession and exit financing, $75 million in additional capital from Sunoco Logistics Partners Operations L.P. (“Sunoco Logistics”) and a $65 million equity investment from existing equity holders, led by The Carlyle Group along with management and other partners. The recapitalized Company will have a stronger financial foundation to support operations amid continuing pressure on refining margins and soaring costs for merchant refiners associated with the purchase of Renewable Identification Numbers (“RINs”) to satisfy requirements under the Renewable Fuel Standard (“RFS”) established by the Environmental Protection Agency (“EPA”). The Agreement provides that the recapitalization will be completed pursuant to a proposed prepackaged restructuring (the “Restructuring”) through the filing of a Chapter 11 Plan of Reorganization (the “Plan”) for PES Holdings and affiliated subsidiaries. -

Susser Holdings and Energy Transfer Partners Announce Stockholder Approval of Merger

Susser Holdings and Energy Transfer Partners Announce Stockholder Approval of Merger 8/28/2014 CORPUS CHRISTI, Texas & DALLAS--(BUSINESS WIRE)--Susser Holdings Corporation (NYSE: SUSS) and Energy Transfer Partners, L.P. (NYSE: ETP) are pleased to announce that Susser Holdings Corporation stockholders voted to approve the proposed merger with ETP at today's special meeting of Susser stockholders. Approximately 99 percent of the shares voted at today's meeting voted in favor of the adoption of the merger agreement, which represented approximately 77 percent of Susser's total outstanding shares of common stock as of the July 22, 2014 record date for the special meeting. As previously announced on April 28, 2014, ETP and Susser entered into a merger agreement, pursuant to which Susser stockholders were entitled to elect to receive, (i) a combination of $40.125 in cash and 0.7253 of an ETP common unit, (ii) $80.25 in cash or (iii) 1.4506 ETP common units, for each share of Susser Holdings Corporation common stock they own immediately prior to the merger (the “Merger”). Elections in excess of either the cash or common unit limits will be subject to proration. After receiving this stockholder approval, all significant closing conditions for the Merger have been met. ETP and Susser expect to complete the merger on August 29, 2014, subject to the satisfaction or waiver of the conditions set forth in the merger agreement. Susser Holdings Corporation (NYSE: SUSS) is a third-generation family led business based in Corpus Christi, Texas, that operates more than 640 convenience stores in Texas, New Mexico and Oklahoma, with 595 under the Stripes® banner and 47 under the Sac-N-Pac banner. -

ENERGY TRANSFER OPERATING, L.P. (Exact Name of Registrant As Specified in Its Charter)

As filed with the Securities and Exchange Commission on October 19, 2018 Registration No. 333-96897 Registration No. 333-208327 Registration No. 333-217592 UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 Post-Effective Amendment No. 1 to Form S-8 Registration Statement No. 333-96897 Post-Effective Amendment No. 1 to Form S-8 Registration Statement No. 333-208327 Post-Effective Amendment No. 2 to Form S-8 Registration Statement No. 333-217592 UNDER THE SECURITIES ACT OF 1933 ENERGY TRANSFER OPERATING, L.P. (Exact name of registrant as specified in its charter) Delaware 73-1493906 (State or other jurisdiction (I.R.S. Employer of incorporation or organization) Identification Number) 8111 Westchester Drive, Suite 600 Dallas, Texas 75225 (214) 981-0700 (Address, including zip code, and telephone number, including area code, of registrant’s principal executive offices) Delaware (State or other jurisdiction of incorporation or organization) Second Amended and Restated Energy Transfer Partners, L.P. 2008 Long-Term Incentive Plan Energy Transfer Partners, L.P. Amended and Restated 2011 Long-Term Incentive Plan Sunoco Partners LLC Long-Term Incentive Plan (as Amended and Restated) (Full title of the plan) Thomas E. Long Chief Financial Officer Energy Transfer Operating, L.P. 8111 Westchester Drive, Suite 600 Dallas, Texas 75225 (214) 981-0700 (Name, address, including ZIP code, and telephone number, including area code, of agent for service) Copies to: Lande A. Spottswood Stephen M. Gill Vinson & Elkins L.L.P. 1001 Fannin Street, Suite 2500 Houston, Texas 77002 (713) 758-2222 Large accelerated filer ☒ Accelerated filer ☐ Non-accelerated filer ☐ (Do not check if a smaller reporting company) Smaller reporting company ☐ Emerging growth company ☐ If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 7(a)(2)(B) of the Securities Act.