Maximizing Interoperator Efficiency in Mobile Multi-Service Networks

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Annual Report 2018

Pakistan Telecommunication Company Limited Company Telecommunication Pakistan PTCL PAKISTAN ANNUAL REPORT 2018 REPORT ANNUAL /ptcl.official /ptclofficial ANNUAL REPORT Pakistan Telecommunication /theptclcompany Company Limited www.ptcl.com.pk PTCL Headquarters, G-8/4, Islamabad, Pakistan Pakistan Telecommunication Company Limited ANNUAL REPORT 2018 Contents 01COMPANY REVIEW 03FINANCIAL STATEMENTS CONSOLIDATED Corporate Vision, Mission & Core Values 04 Auditors’ Report to the Members 129-135 Board of Directors 06-07 Consolidated Statement of Financial Position 136-137 Corporate Information 08 Consolidated Statement of Profit or Loss 138 The Management 10-11 Consolidated Statement of Comprehensive Income 139 Operating & Financial Highlights 12-16 Consolidated Statement of Cash Flows 140 Chairman’s Review 18-19 Consolidated Statement of Changes in Equity 141 Group CEO’s Message 20-23 Notes to and Forming Part of the Consolidated Financial Statements 142-213 Directors’ Report 26-45 47-46 ہ 2018 Composition of Board’s Sub-Committees 48 Attendance of PTCL Board Members 49 Statement of Compliance with CCG 50-52 Auditors’ Review Report to the Members 53-54 NIC Peshawar 55-58 02STATEMENTS FINANCIAL Auditors’ Report to the Members 61-67 Statement of Financial Position 68-69 04ANNEXES Statement of Profit or Loss 70 Pattern of Shareholding 217-222 Statement of Comprehensive Income 71 Notice of 24th Annual General Meeting 223-226 Statement of Cash Flows 72 Form of Proxy 227 Statement of Changes in Equity 73 229 Notes to and Forming Part of the Financial Statements 74-125 ANNUAL REPORT 2018 Vision Mission To be the leading and most To be the partner of choice for our admired Telecom and ICT provider customers, to develop our people in and for Pakistan. -

Annual Report 2011

possibilities ANNUAL REPORT 2011 CONTENTS About the company ............................................................................... 2 Key financial & operational highlights ............................................. 12 Key events of 2011 & early 2012 ...................................................... 14 Bright upside potential from the reorganization ............................. 18 Strong market position ................................................................... 20 Up in the “Clouds” ........................................................................... 22 Chairman’s statement ........................................................................ 24 Letter from the President ................................................................... 26 Strategy .............................................................................................. 28 M&A activity ........................................................................................ 31 Corporate governance ........................................................................ 34 Board of Directors & committees .................................................... 34 Management Board & committees ................................................. 37 Internal Audit Commission ............................................................. 40 Remuneration of members of the Board of Directors and the Management Board ............................................................. 40 Dividend policy ................................................................................ -

PROVISIONALLY APPROVED by the Board of Directors of OJSC Rostelecom May 19, 2014 Minutes No 01 Dated May 22, 2014

PROVISIONALLY APPROVED by the Board of Directors of OJSC Rostelecom May 19, 2014 Minutes No 01 dated May 22, 2014 APPROVED by the Annual General Shareholders’ Meeting of OJSC Rostelecom June 30, 2014 Minutes No___ dated June __, 2014 ANNUAL REPORT OPEN JOINT STOCK COMPANY LONG-DISTANCE AND INTERNATIONAL TELECOMMUNICATIONS ROSTELECOM BASED ON YEAR 2013 RESULTS President of OJSC Rostelecom s/s S.B. Kalugin Acting Chief Accountant of OJSC Rostelecom s/s N.V. Lukashin May 22, 2014 Moscow, 2014 ANNUAL REPORT TABLE OF CONTENTS CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING STATEMENTS ....................................... 3 INFORMATION CONTAINED IN THIS ANNUAL REPORT .............................................................................. 4 ROSTELECOM AT A GLANCE ......................................................................................................................... 5 THE PRESIDENT’S MESSAGE ......................................................................................................................... 6 2013 HIGHLIGHTS ............................................................................................................................................ 8 OPERATING AND FINANCIAL RESULTS ...................................................................................................... 10 COMPANY’S POSITION IN THE INDUSTRY ................................................................................................. 12 COMPANIES IN ROSTELECOM GROUP ...................................................................................................... -

Comment Operators at Crossroads: Market Protection Or Innovation?

Comment Operators at crossroads: Market protection or innovation? Arnd Webera*, Daniel Scukab Published in: Telecommunications Policy, Volume 40, Issue 4, April 2016, Pages 368–377, doi:10.1016/j.telpol.2015.11.009. Permission to publish an authors’ version has kindly been granted by Elsevier B.V. a KIT (ITAS), Kaiserstraße 12, 76131 Karlsruhe, Germany b Mobikyo K.K., Level 32, Shinjuku Nomura Building, 1‐26‐2 Nishi‐Shinjuku, Shinjuku‐ku, Tokyo 163‐0532, Japan Abstract Many today believe that the mobile Internet was invented by Apple in the USA with their iPhone, enabling a data‐driven Internet ecosystem to disrupt the staid voice and SMS busi‐ ness models of the telecom carriers. History, however, shows that the mobile Internet was first successfully commercialised in Japan, in 1999. Some authors such as Richard Feasey in Telecommunications Policy (Issue 6, 2015) argue that operators had been confused and un‐ prepared when the Internet emerged and introduced “walled gardens”, without Internet access. This comment article reviews in detail how the operators reacted when the fixed, and later the mobile Internet spread; some introduced walled gardens, some opened it for the “unofficial” content on the Internet. The article concludes that most large European tel‐ ecom and information technology companies and their investors have a tradition of risk avoidance and pursued high‐price strategies that led them to regularly fail against better and cheaper foreign products and services, not only when the wireless Internet was introduced, but also when PCs and the fixed Internet were introduced. Consequences, such as the need to enable future disruptions and boost the skills needed to master them, are presented. -

Proposal to Put Prestel Viewdata System Into Every British Home Racing for the Cosmic Flash

_4l_O _______________________ NEWS------------N_A_T_U_R_E_V_O_L_.3_3_0_3_D_E_C_E_M_B_E_R_1_98_7 Proposal to put Prestel viewdata Racing for the system into every British home cosmic flash London to supply continuously updated informa Sydney BRITISH Telecom has decided to embark tion on ferry availability. Indeed, by 1981, AsTRONOMERS in Australia and New on an ambitious scheme to put its pioneer British Telecom had changed its market Zealand are rushing to complete gamma ing viewdata system Prestel into every ing strategy to aim at the business world ray telescopes in time to catch the ex telephone subscriber's household. At rather than householders. Now, of Prestel's pected arrival of gamma rays from the present. only 24,000 British households 78,000 terminals, 69 per cent are in the February supernova in the Large Magel have Prestel terminals, out of 18 million workplace and 31 per cent in the home. lanic Cloud. domestic telephone subscribers. It is The lack of interest of domestic users is Two new instruments are under con understood that British Telecom will in generally blamed on poor marketing and struction; one in the Australian desert at the first instance set up a trial, with sub the cost of hardware. At present, the least Woomera and the other 1,650 m up a scribers in one London telephone district expensive means of using Prestel is to buy mountain near Blenheim on New Zea and one district outside London being an adaptor priced at around £100 for an land's South Island. supplied with Prestel terminals for a existing television set. Although Prestel's Visually, the supernova has long passed fixed time. -

Pdf 8 Methodology Development, Ranking Digital Rights

SMEX is a Beirut-based media development and digital rights organization working to advance self-regulating information societies. Our mission is to defend digital rights, promote open culture and local content, and encourage critical engagement with digital technologies, media, and networks through research, knowledge-sharing, and advocacy. Design, illustration concept, and layout are by Salam Shokor, with assistance from David Badawi. Illustrations are by Ahmad Mazloum and Salam Shokor. www.smex.org A 2018 Publication of SMEX Kmeir Building, 4th Floor, Badaro, Beirut, Lebanon © Social Media Exchange Association, 2018 This work is licensed under a Creative Commons Attribution-ShareAlike 4.0 International License. Acknowledgments Afef Abrougui conceptualized this research report and designed and oversaw execution of the methodology for data collection and review. Research was conducted between April and July 2017. Talar Demirdjian and Nour Chaoui conducted data collection. Jessica Dheere edited the report, with proofreading assistance from Grant Baker. All errors and omissions are strictly the responsibility of SMEX. This study would not have been possible without the guidance and feedback of Rebecca Mackinnon, Nathalie Maréchal, and the whole team at Ranking Digital Rights (www.rankingdigitalrights.org). RDR works with an international community of researchers to set global standards for how internet, mobile, and telecommunications companies should respect freedom of expression and privacy. The 2017 Corporate Accountability Index ranked 22 of the world’s most powerful such companies on their disclosed commitments and policies that affect users' freedom of expression and privacy. The methodology developed for this research study was based on the RDR/ CAI methodology. We are also grateful to EFF’s Katitza Rodriguez and Access Now’s Peter Micek, both of whom shared valuable insights and expertise into how our research might be transformed and contextualized for local campaigns. -

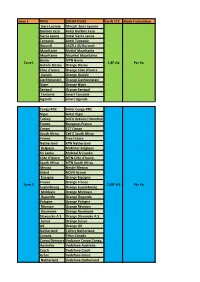

Zone 1 PAYS OPERATEURS Tarifs TTC Mode Facturation Siera

Zone 1 PAYS OPERATEURS Tarifs TTC Mode Facturation Siera Leonne Africell Siera Leonne Burkina Faso Airtel Burkina Faso Sierra Leone Airtel Sierra Leone Tanzanie Airtel Tanzanie Burundi LACELL SU Burundi Mauritanie Mattel Mauritania Mauritanie Mauritel Mauritanie Benin MTN Benin Zone1 1,8F cfa Par Ko Guinée Bissau Orange Bissau Côte d'Ivoire Orange Côte d'Ivoire Guinée Orange Guinée Liechteinstein Orange Liechteinstein Niger Orange Niger Senegal Orange Senegal Tanzanie Smart Tanzanie Uganda Smart Uganda Congo RDC Airtel Congo RDC Niger Airtel Niger Turkey AVEA Iletisim Hizmetleri A.S. (Aycell) Turkey France Bouygues France Congo CCT Congo South Africa Cell C South Africa France Free France Netherland KPN Netherland Belgique Mobistar Belgique Sri Lanka Mobitel Sri Lanka Côte d'Ivoire MTN Côte d'Ivoire South Africa MTN South Africa Mexico Nextel Mexico Island NOVA IsLand Espagne Orange Espagne France Orange France Zone 2 2,95F cfa Par Ko Luxembourg Orange Luxembourg Moldavie Orange Moldavie Ouganda Orange Ouganda Pologne Orange Pologne Réunion Orange Réunion Roumanie Orange Roumanie Slovensko A.S. Orange Slovensko A.S. Suisse Orange Suisse UK Orange UK Netherland Telfort Netherland Canada Telus Canada Congo DemocraticVodacom Congo Congo, Democratic Republic of the Australia Vodafone Australia Czech Vodafone Czech Grèce Vodafone Grèce Netherland Vodafone Netherland Belgique Base Belgique Belgacom Belgacom Benin Moov Benin Canada Rogiers Canada Canada Microcel Canada Swiss Com Swiss Com Côte d'Ivoire Moov Côte d'Ivoire Cap Vert Cap Vert Mobile -

Regional Telecoms

Global Equity Research Sector Flash Fixed-line telecoms Russia 28 August 2008 Regional telecoms TPs cut 7%-37% on tighter margins ● The regional telecoms’ non-consolidated RAS EBITDA margins lost 1pp-4pp y-o-y in 1H08 due to outpacing cost growth. Operating expenses (less depreciation) rose 8%-15% y-o-y in rubles (compared to top-line growth of 4%-8%), mainly driven by higher staff costs, interconnect payments and SG&A. As a result, four of the seven incumbents saw EBITDA decline 2%-7% y-o-y in rubles. ● We expect the underlying salary and interconnect cost increases to be reflected in the incumbents’ 1H08 IFRS results (due in September) despite the accounting differences. We reduce our 2008F EBITDA estimates for all the regional telecoms except Dalsvyaz by 5%- 15%, and now expect EBITDA margins of 28%-35% vs. our previous estimate of 32%-36%. ● We raise our projections for capex on acquisitions this year to reflect the companies’ spending on minority stakes in Hybrid Print Systems. We increase our 2008F capex/sales ratio for Centertelecom from 19% to 29%, as the company raised its 2008F capex guidance. ● We cut our 12-month TPs by 7%-37% due to lower operational forecasts and higher capex projections. We downgrade Centertelecom from Buy to Hold, following a 37% decrease in its 12-month TP to $0.49. We upgrade Southern Telecom from Sell to Hold due to the stock’s recent weakness, and maintain our Buy ratings for North-West Telecom, VolgaTelecom, Uralsvyazinform, Sibirtelecom and Dalsvyaz. ● Our top picks are Dalsvyaz and VolgaTelecom, given their upsides of 116% and 83%, respectively, to our new target prices and the fact that their 2008F EV/EBITDA multiples are below 3X. -

APPROVED by the Annual General Shareholders' Meeting of OJSC

APPROVED by the Annual General Shareholders’ Meeting of OJSC Rostelecom June 14, 2012 Minutes #1 dated June 18, 2012 ANNUAL REPORT FOR THE LONG-DISTANCE AND INTERNATIONAL TELECOMMUNICATIONS OPEN JOINT STOCK COMPANY ROSTELECOM BASED ON YEAR 2011 RESULTS President of OJSC Rostelecom s/s A. Yu. Provorotov Chief Accountant of OJSC Rostelecom s/s R.A. Frolov April 27, 2012 Moscow, 2012 ANNUAL REPORT CONTENTS OJSC ROSTELECOM AT A GLANCE ............................................................................................................. 4 THE CHAIRMAN’S STATEMENT ..................................................................................................................... 5 THE PRESIDENT’S MESSAGE ........................................................................................................................ 6 CALENDAR OF 2011 EVENTS ......................................................................................................................... 8 THE COMPANY’S POSITION IN THE INDUSTRY ......................................................................................... 10 THE COMPANY AND THE BOARD OF DIRECTORS’ REVIEW OF THE YEAR 2011 ................................ 15 GUARANTEE OF HIGH QUALITY COMMUNICATION SERVICES ........................................................... 16 DEVELOPING RETAIL RELATIONSHIPS .................................................................................................. 17 RUSSIAN OPERATORS MARKET ............................................................................................................. -

From Packet Switching to the Cloud

Professor Nigel Linge FROM PACKET SWITCHING TO THE CLOUD Telecommunication engineers have always drawn a picture of a cloud to represent a network. Today, however, the cloud has taken on a new meaning, where IT becomes a utility, accessed and used in exactly the same on-demand way as we connect to the National Grid for electricity. Yet, only 50 years ago, this vision of universal access to an all- encompassing and powerful network would have been seen as nothing more than fanciful science fiction. he first electronic, digital, network - a figure that represented a concept of packet switching in which stored-program computer 230% increase on the previous year. data is assembled into a short se- was built in 1948 and This clear and growing demand for quence of data bits (a packet) which heralded the dawning of data services resulted in the GPO com- includes an address to tell the network a new age. missioning in July 1970 an experi- where the data is to be sent, error de- T mental, manual call-set-up, data net- tection to allow the receiver to confirm DATA COMMUNICATIONS 1 work that used modems operating at that the contents of the packet are cor- These early computers were large, 48,000bit/s (48kbit/s). rect and a source address to facilitate cumbersome and expensive machines However, computer communica- a reply. and inevitably a need arose for a com- tions is different to voice communi- Since each packet is self-contained, munication system that would allow cations not only in its form but also any number of them can be transmit- shared remote access to them. -

Than 400000 Points-Of-Sale

2009 PREPAID PROCESSING BUSINESS WITH FLEXIBLE MICRO TOP-UP For Mobile Communication Brand Stores Payment Terminal Networks Retail Chains Cash Desks Banks The largest electronic payment system More than 400,000 points-of-sale More than $6.5 billion 2008 financial turnover Contents Our directors say 1 About the company 2 Awards 3 Key figures 4 Glossary 6 Current trends in the financial markets 7 Technology 8 CyberPlat® business scheme 10 Operators list 11 International operators and operations 15 CyberPlat® – the global payment system 16 Payment for Public Utility Services 17 Cash Acceptance chains 18 Social mission of the CyberPlat® system 19 Be a Regional Representative for CyberPlat®! 20 Become a CyberPlat® Dealer in 5 minutes! 22 Why is it profitable for your business 23 How to accept payments in a shop 24 New service «Change to the phone» 26 Payment for the period of using software 28 CyberPlat® Offer to Banks 30 CyberPlat® supports various hardware 40 Terminals (cash-in self-service kiosks) 41 POS terminals 42 Preprocessing 43 CyberPlat® is failure free! 44 Open source code 45 Secure document workflow 46 CyberPlat® system strength and features 47 Contact Information 48 Our directors say | Page 1 Andrey Gribov, General Director of CyberPlat OJSC: Russia entered the 21st century, a century of the knowledge-based economy – and the CyberPlat® system emerged as a consequence of increased needs of modern people and businesses in the third millennium. A rapid growth in the number of new services and their availability for the growing population necessitate a development of new payment instruments. Banks first appeared as storages for big sums of money, so it’s not surprising that the banks have strong walls, armoured doors, and employ highly professional and therefore highly-paid personnel along with state-of-the-art technologies to keep the money safe. -

African Mobile Factbook 2008

African Mobile Factbook 2008 This briefing paper provides a snapshot of the African mobile phone market at the start of 2007, written and produced as a free service for executives involved in the mobile phone industry by the editorial team of ‘Africa & Middle East Telecom Week’. For further information, please visit www.africantelecomsnews.com Blycroft Publishing www.blycroft.com Blycroft Limited Published 1st. February 2008. Copyright 2008 www.africantelecomsnews.com Disclaimer and Legal Notices. Disclaimer. Every care has been taken in the preparation of this report to ensure that the information contained herein is accurate, factual and correct to the best of our knowledge, at the time of publishing. All opinions, suppositions, estimates and recommendations included in this report are solely the opinions of the authors unless otherwise stated. Blycroft Limited accepts no liability for any loss or damage or unforeseen consequential loss or damage arising from the use of the information contained within this document. The opinions, suppositions, estimates and recommendations within this report cannot be guaranteed, and readers use this information at their own risk. The information published in this document is subject to change without notice at any time, and Blycroft Limited accepts no liability or obligation to inform the reader of such changes. Blycroft Limited do not promote or endorse any specific companies or products, the views and opinions we express in this report are wholly our own assessments, and independent from any external interest or influence. Many terms and phrases and trade names used in this document are proprietary and Blycroft Limited recognises and acknowledges that all trademarks are copyright, belonging to their respective owners.