The Whillans Report Auckland Market Update 4Th Quarter 2020

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

![Schedule 14.1 Schedule of Historic Heritage [Rcp/Dp]](https://docslib.b-cdn.net/cover/2664/schedule-14-1-schedule-of-historic-heritage-rcp-dp-142664.webp)

Schedule 14.1 Schedule of Historic Heritage [Rcp/Dp]

Schedule 14.1 Schedule of Historic Heritage [rcp/dp] Introduction The criteria in B5.2.2(1) to (5) have been used to determine the significant historic heritage places in this schedule and will be used to assess any proposed additions to it. The criteria that contribute to the heritage values of scheduled historic heritage in Schedule 14.1 are referenced with the following letters: A: historical B: social C: Mana Whenua D: knowledge E: technology F: physical attributes G: aesthetic H: context. Information relating to Schedule 14.1 Schedule 14.1 includes for each scheduled historic heritage place; • an identification reference (also shown on the Plan maps) • a description of a scheduled place • a verified location and legal description and the following information: Reference to Archaeological Site Recording Schedule 14.1 includes in the place name or description a reference to the site number in the New Zealand Archaeological Association Site Recording Scheme for some places, for example R10_709. Categories of scheduled historic heritage places Schedule 14.1 identifies the category of significance for historic heritage places, namely: (a) outstanding significance well beyond their immediate environs (Category A); or (b) the most significant scheduled historic heritage places scheduled in previous district plans where the total or substantial demolition or destruction was a discretionary or non-complying activity, rather than a prohibited activity (Category A*). This is an interim category until a comprehensive re-evaluation of these places is undertaken and their category status is addressed through a plan change process; or 1 (c) considerable significance to a locality or greater geographic area (Category B). -

SALES TRACK RECORD City Metro Team April 2018 Sales Track Record

SALES TRACK RECORD City MEtro Team April 2018 sales track record 777-779 NEW NORTH ROAD, MT ALBERT 31 MACKELVIE STREET, GREY LYNN 532-536 PARNELL ROAD, PARNELL PRICE: $1,300,000 PRICE: $2,715,000 PRICE: $13,600,000 METHOD: Tender METHOD: Deadline Private Treaty METHOD: Tender ANALYSIS: Part Vacant, $7,103/m² land & buildings ANALYSIS: $5,645/m² on land ANALYSIS: $7,039/m² land area BROKERS: Reese Barragar BROKERS: Reese Barragar, Murray Tomlinson BROKERS: Andrew Clark, Graeme McHoull, Cam Paterson DATE: March 2018 DATE: March 2018 DATE: March 2018 VENDOR: St Albans Limited VENDOR: Telecca New Zealand Limited VENDOR: Empire Trust (Mike & Irene Rosser) sales track record 35 CHURCH STREET, ONEHUNGA 57L LIVINGSTONE STREET, GREY LYNN 62 BROWN STREET, ONEHUNGA PRICE: $1,210,000 PRICE: $515,000 PRICE: $2,700,000 METHOD: Auction METHOD: Deadline Private Treaty METHOD: Auction ANALYSIS: $4,115/m² land & building ANALYSIS: Vacant, $8,583/m2 Land & Buildings ANALYSIS: 4.62% yield BROKERS: Murry Tomlinson BROKERS: Reese Barragar, Shaydon Young BROKERS: Murry Tomlinson, Reese Barragar DATE: March 2018 DATE: March 2018 DATE: March 2018 VENDOR: Walker Trust VENDOR: Lion Rock Roast Limited VENDOR: Shanks & Holmes sales track record 69/210-218 VICTORIA STREET WEST, VICTORIA QUARTER 10 ADELAIDE STREET, VICTORIA QUARTER 60 MT EDEN ROAD, MT EDEN PRICE: $1,300,000 PRICE: $855,000 PRICE: $2,600,000 METHOD: Private Treaty METHOD: Deadline Private Treaty METHOD: Tender ANALYSIS: Vacant, $6,075/m2 land & buildings ANALYSIS: Vacant, $8,066/m² land & building ANALYSIS: -

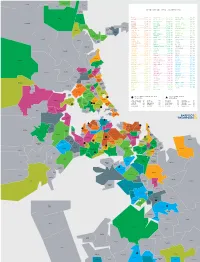

TOP MEDIAN SALE PRICE (OCT19—SEP20) Hatfields Beach

Warkworth Makarau Waiwera Puhoi TOP MEDIAN SALE PRICE (OCT19—SEP20) Hatfields Beach Wainui EPSOM .............. $1,791,000 HILLSBOROUGH ....... $1,100,000 WATTLE DOWNS ......... $856,750 Orewa PONSONBY ........... $1,775,000 ONE TREE HILL ...... $1,100,000 WARKWORTH ............ $852,500 REMUERA ............ $1,730,000 BLOCKHOUSE BAY ..... $1,097,250 BAYVIEW .............. $850,000 Kaukapakapa GLENDOWIE .......... $1,700,000 GLEN INNES ......... $1,082,500 TE ATATŪ SOUTH ....... $850,000 WESTMERE ........... $1,700,000 EAST TĀMAKI ........ $1,080,000 UNSWORTH HEIGHTS ..... $850,000 Red Beach Army Bay PINEHILL ........... $1,694,000 LYNFIELD ........... $1,050,000 TITIRANGI ............ $843,000 KOHIMARAMA ......... $1,645,500 OREWA .............. $1,050,000 MOUNT WELLINGTON ..... $830,000 Tindalls Silverdale Beach SAINT HELIERS ...... $1,640,000 BIRKENHEAD ......... $1,045,500 HENDERSON ............ $828,000 Gulf Harbour DEVONPORT .......... $1,575,000 WAINUI ............. $1,030,000 BIRKDALE ............. $823,694 Matakatia GREY LYNN .......... $1,492,000 MOUNT ROSKILL ...... $1,015,000 STANMORE BAY ......... $817,500 Stanmore Bay MISSION BAY ........ $1,455,000 PAKURANGA .......... $1,010,000 PAPATOETOE ........... $815,000 Manly SCHNAPPER ROCK ..... $1,453,100 TORBAY ............. $1,001,000 MASSEY ............... $795,000 Waitoki Wade HAURAKI ............ $1,450,000 BOTANY DOWNS ....... $1,000,000 CONIFER GROVE ........ $783,500 Stillwater Heads Arkles MAIRANGI BAY ....... $1,450,000 KARAKA ............. $1,000,000 ALBANY ............... $782,000 Bay POINT CHEVALIER .... $1,450,000 OTEHA .............. $1,000,000 GLENDENE ............. $780,000 GREENLANE .......... $1,429,000 ONEHUNGA ............. $999,000 NEW LYNN ............. $780,000 Okura Bush GREENHITHE ......... $1,425,000 PAKURANGA HEIGHTS .... $985,350 TAKANINI ............. $780,000 SANDRINGHAM ........ $1,385,000 HELENSVILLE .......... $985,000 GULF HARBOUR ......... $778,000 TAKAPUNA ........... $1,356,000 SUNNYNOOK ............ $978,000 MĀNGERE ............. -

Geocene-24.Pdf

Geocene Auckland GeoClub Magazine Number 24, December 2020 Editor: Jill Kenny CONTENTS Instructions on use of hyperlinks last page 19 NEW 14C RESULT CONFIRMS 28,000 YEAR OLD Elaine R. Smid, 2 – 5 MAUNGAWHAU / MT EDEN ERUPTION AGE Bruce W. Hayward, Thomas Stolberger, Roderick Wallace, Ewart Barnsley FORTY-SEVEN YEARS OF EROSION AND WEATHERING Bruce W. Hayward 6 – 7 OF LION ROCK BOMB, PIHA MAORI BAY MICROMINERALS Tim Saunderson 8 – 14 PROXY EVIDENCE FROM TAMAKI DRIVE FOR THE Bruce W. Hayward 15 – 16 LOCATION OF SUBMERGED STREAM VALLEYS BENEATH HOBSON BAY, AUCKLAND CITY THE FIRST EXPLANATION IS NOT ALWAYS THE BEST Bruce W. Hayward 17 – 18 Corresponding authors’ contact information 19 Geocene is a periodic publication of Auckland Geology Club, a section of the Geoscience Society of New Zealand’s Auckland Branch. Contributions about the geology of New Zealand (particularly northern New Zealand) from members are welcome. Articles are lightly edited but not refereed. Please contact Jill Kenny [email protected] 1 NEW 14C RESULT CONFIRMS 28,000 YEAR OLD MAUNGAWHAU / MT EDEN ERUPTION AGE Elaine R Smid1, Bruce W Hayward2, Thomas Stolberger1, Roderick Wallace1, and Ewart Barnsley3 1 The University of Auckland 2 Geomarine Research 3 City Rail Link In February 2019, City Rail Link (CRL) reported that their The large obstruction (>1 m diameter in a 2 m drill hole) micro-tunnel boring machine “Jeffie” became entangled caused Jeffie to veer off course. CRL removed the wood in a large tree at 15 m depth, approximately 50 m north fragments and pulled them to the surface (Fig. -

The Demographic Transformation of Inner City Auckland

New Zealand Population Review, 35:55-74. Copyright © 2009 Population Association of New Zealand The Demographic Transformation of Inner City Auckland WARDLOW FRIESEN * Abstract The inner city of Auckland, comprising the inner suburbs and the Central Business District (CBD) has undergone a process of reurbanisation in recent years. Following suburbanisation, redevelopment and motorway construction after World War II, the population of the inner city declined significantly. From the 1970s onwards some inner city suburbs started to become gentrified and while this did not result in much population increase, it did change the characteristics of inner city populations. However, global and local forces converged in the 1990s to trigger a rapid repopulation of the CBD through the development of apartments, resulting in a great increase in population numbers and in new populations of local and international students as well as central city workers and others. he transformation of Central Auckland since the mid-twentieth century has taken a number of forms. The suburbs encircling the TCentral Business District (CBD) have seen overall population decline resulting from suburbanisation, as well as changing demographic and ethnic characteristics resulting from a range of factors, and some areas have been transformed into desirable, even elite, neighbourhoods. Towards the end of the twentieth century and into the twenty first century, a related but distinctive transformation has taken place in the CBD, with the rapid construction of commercial and residential buildings and a residential population growth rate of 1000 percent over a fifteen year period. While there are a number of local government and real estate reports on this phenomenon, there has been relatively little academic attention to its nature * School of Environment, The University of Auckland. -

Parking Changes for Eden Terrace

Your feedback on: Parking changes for Eden Terrace November 2020 – Report on Public Feedback – Parking Changes for Eden Terrace Contents 1. Summary .......................................................................................................................................... 3 Overview ...........................................................................................................................................................3 Q1: What do submitters think about proposal? ..............................................................................................3 Q2: Top 10 feedback themes ............................................................................................................................4 Q3: Top 10 feedback themes ............................................................................................................................5 Project decisions ...............................................................................................................................................6 Next steps .........................................................................................................................................................6 2. Background ...................................................................................................................................... 7 What did we seek feedback on?.......................................................................................................................7 Why did we propose these parking -

Central Kingsland Including Eden Terrace, Western Springs and Morningside

Central Kingsland including Eden Terrace, Western Springs and Morningside erched on the fringe of the central city, Kingsland is a long-neglected suburb whose P time has finally come to shine. As well as the cafés, designer handcraft retailers and fashion boutiques, there are now new apartment buildings, trendy shops, funky bars and busy restaurants. Originally a working-class neighbourhood, old Kingsland is typified by the narrow streets of old cottages running parallel to the northwestern motorway. The further down the hill you are, the less sun and the more motorway noise you get. Eden Terrace is an edgy mix of commercial and residential; it has an idiosyncratic, bohemian character and a number of student flats. Morningside, fictional home of TV3’s Bro’Town, is primarily commercial and light industrial. Western Springs has a mix of gentrified bungalows and state housing. Population Profile Population 6,291 % Aged Under 15 Years 10.78 % Aged Over 65 Years 3.62 % European 55.65 % Maori 7.72 % Pacific Peoples 11.44 % Asian 18.17 Who Lives There? This once less-than-desirable area is now humming to the sound of coffee machines and the cry of wee ones following in their trendy parents’ footsteps. There is still some blue- collar presence here, but the newer residents are white-collar-types who can’t quite afford Grey Lynn. Rental properties are plentiful across these suburbs and popular with students, but Western Springs has largely become a thriving family area. The do-ups that renovators have bought in the past are now ripe for re-sale and are being snapped up by willing buyers. -

Proposed Mixed Use Development 360 Dominion Road Mount Eden, Auckland Special Character Assessment Prepared for Pudong Housing Development Ltd & Foodstuffs (Nz) Ltd

Plan.Heritage PROPOSED MIXED USE DEVELOPMENT 360 DOMINION ROAD MOUNT EDEN, AUCKLAND SPECIAL CHARACTER ASSESSMENT PREPARED FOR PUDONG HOUSING DEVELOPMENT LTD & FOODSTUFFS (NZ) LTD MARCH 2021 Plan.Heritage Ltd. 48 Lake Road Narrow Neck Auckland 0624 [email protected] www.planheritage.co.nz Plan.Heritage Proposed Mixed Used Development 360 Dominion Road Mt Eden, Auckland Special Character Assessment Prepared for Pudong Housing Development Ltd & Foodstuffs (NZ) Ltd March 2021 CONTROLLED DOCUMENT Version Date Prepared by: Reviewed: Approved: FINAL for 02/03/2021 J Brown (MA E Key J Dalzell ISSUE MCIfA) Revision record Date Prepared by: Summary of Changes Approved Final Draft 01/03/2021 Minor corrections to text J Dalzelll Update references DRAFT 1 January 2020 J Brown (MA Reviewed by A Brown (MA E Key ACIfA) MSc) Reference this document: Brown. J, March 2021. Proposed Mixed Use Development; 360 Dominion Road Mt Eden, Auckland. Special Character Assessment. Prepared for Pudong Housing Development Ltd & Foodstuffs (NZ) Ltd. Cover image: Dominion Road and Valley Road intersection, Auckland (Plan.Heritage Ltd. 2020) Plan.Heritage Ltd. 48 Lake Road Narrow Neck Auckland 0624 [email protected] www.planheritage.co.nz 021 02973641 © Plan.Heritage Ltd. 2021. Reproduction of this document in whole or in part without permission is not authorised. 2 | P a g e Plan.Heritage Special Character Assessment: 360 Dominion Road Auckland March 2021 Plan.Heritage EXECUTIVE SUMMARY Pudong Housing Development Ltd & Foodstuffs (NZ) Ltd is proposing the construction of a mixed use development including retail, office space, and apartment blocks at 360 Dominion Road Mt Eden, Auckland. -

Check out More Details and Book At

CHECK OUT MORE DETAILS AND BOOK AT WWW.RESTAURANTHUB.CO.NZ Tick Iconic Auckland Eat Iconic Auckland Eat Venue Address Te Mana Lamb & Cheese Savoury Ahi 7 Queen Street, Auckland CBD Pulled Lamb Shoulder Amano 66-68 Tyler Street, Britomart Place, Britomart, Auckland CBD Angus Beef Dip Baguette Angus Steak House 8 Fort Lane, Auckland CBD Antoine’s Tripe Antoine’s 333 Parnell Road, Parnell Homemade Pork Sausage with Pickles and Mustard Apero 280 Karangahape Road, K Road, Auckland CBD Volcano Sushi Azabu 26 Ponsonby Road, Grey Lynn Karitane Crayfish Meatballs Baduzzi 10-26 Jellicoe Street, North Wharf, Auckland CBD Manchego and Jalapeño Croquetas Baruhlo 2-16 Watt Street, Parnell Flatbread with Chilli Fried Egg Bestie Café Shop 13, St Kevins Arcade, 183 Karangahape Road, Auckland CBD Steamed Bun with Roasted Pork Belly Blue Breeze Inn 146 Ponsonby Road, Ponsonby Central, Ponsonby Beef Brisket Blue Ox Babe BBQ 127 Manukau Road, Pukekohe Koko Samoa Cupcake Blue Rose Café 414 Sandringham Road, Sandringham Crispy Pata Boracay 124 Customs Street West, Viaduct, Auckland CBD Char Kway Teow KL Style Bunga Raya Restaurant 3062 Great North Road, New Lynn Kari Kepala Ikan (Nyonya Fish Head Curry) Bunga Raya Restaurant 3062 Great North Road, New Lynn Beef with Cheese Burger Burger Burger 3B York Street, Newmarket NZ Octopus & Kaffir Lime Sauce Café Hanoi 27 Galway Street, Britomart Auckland CBD Goat’s Cheese Croquettes Casita Miro 3 Brown Road, Onetangi, Waiheke Island Special Fish Curry Cassia 5 Fort Lane, Auckland CBD The Cazador Sandwich Cazador 854 -

DISTRICT PLAN ISTHMUS SECTION - OPERATIVE 1999See Key on Page A1 Page C1 of This Appendix Updated 05/03/2010 APPENDIX 11

APPENDIX 11 The centre contains the following scheduled buildings or 1.7 UPPER SYMONDS STREET objects: • Alex Evans Street 5-7, Newton: St Benedicts Church The Symonds Street / Khyber Pass Road junction was likely • St Benedicts Street 1-9, Newton: St Benedicts's to have been an early walking track that, like many similar Presbytery paths, became bridle tracks and later roads that eventually • St Benedicts Street 30A-E, Newton, (off Stable lane): became linked into a formalised roading network. The Stables Europeans settled the area in the 1840s as fringe city suburban residences for the wealthy because of its elevated • Mt Eden Road 4, Mt Eden: Pumphouse position and views of the Waitemata. • Khyber Pass 69-71, Grafton: Holy Sepulchre Church Like many fringe suburban centres, Upper Symonds Street • Mt Eden Road 2, Mt Eden: Grafton Library (Galbraith's developed and grew in conjunction with the rapidly Public House 2001) increasing population and improvements in public transport particularly the tram lines, with a significant period of built development occurring in the 1880s and 1910s. At the height 1.8 WEST LYNN of its traditional development period 1920s-30s the centre provided most of the everyday services, supplies and entertainment needed by the surrounding suburbs (Newton, The West Lynn shopping precinct developed in the early Grafton, Eden Terrace and Arch Hill). decades of the twentieth century along the ridgeline of Richmond Road near the junction with Francis Street and Upper Symonds Street has retained a number of buildings Hakanoa Street, servicing the expanding residential from the 1880's-1930's with a significant emphasis on population in this area. -

Eight Transformational Moves - Ideas, Programmes and This Transformation

City Centre Masterplan 2020 Transformational Moves: Full Text September 2019 City Centre Masterplan Refresh We want your feedback on the future planning of Auckland’s Since 2012: What has been done so far city centre. The City Centre Masterplan and The Waterfront Plan are being refreshed and combined as part of a six-yearly • The resident population has increased from 24,000 to over The original City Centre Masterplan and Waterfront Plan upgrade. 55,000 were adopted in 2012. We need to keep them up-to-date and • The number of daily workers has jumped from 90,000 to relevant in line with other high-level planning documents. The City Centre Masterplan refresh is a high-level, non- over 120,000 statutory document that supports the Auckland Plan 2050 and • Every day over 200,000 people visit the city centre The City Centre Masterplan refresh looks to build on the 2012 Auckland Unitary Plan. Together with the Waitematā Local • An estimated 20 per cent of Auckland’s gross domestic plans taking them online and combining them to: Board Plan, these documents provide the overall vision that sets product is now generated from the city centre alone. the direction for Auckland’s city centre. • Showcase progress Auckland continues to grow at an unprecedented rate. Right • Reconfirm strategic direction Have your say on the City Centre Masterplan refresh [h3] now, there is $73 billion of commercial construction across the • Highlight specific new initiatives and projects – most region and more than 150 major development projects either in notably Access for Everyone Your feedback will help shape the vision for Auckland’s city progress or in the pipeline. -

Restaurant Name

Restaurant Name Address Line 1 Address Line 2 City Name Postal Code Location 16 TUN 10-26 JELLICOE STREET WYNYARD QUARTER 1010 CENTRAL AUCKLAND 1947 EATERY 60 FEDERAL STREET AUCKLAND 1010 CENTRAL AUCKLAND 46 & YORK 46 PARNELL ROAD PARNELL 1052 CENTRAL AUCKLAND AMANO 68 TYLER STREET BRITOMART 1010 CENTRAL AUCKLAND ANDY'S BURGERS & BAR SKYCITY AUCKLAND CNR VICTORIA ST WEST & HOBSON ST AUCKLAND 1010 CENTRAL AUCKLAND ANGUS STEAK HOUSE 8 FORT LANE AUCKLAND 1010 CENTRAL AUCKLAND ANTOINE'S RESTAURANT 333 PARNELL RD PARNELL 1052 CENTRAL AUCKLAND ARCHIE'S RESTAURANT & PIZZERIA 61-73 DAVIS CRESCENT NEWMARKET 1023 CENTRAL AUCKLAND ARIA RESTAURANT AND BAR 128 ALBERT STREET AUCKLAND 1010 CENTRAL AUCKLAND AUGUSTUS 1 ST MARYS RD ST MARYS BAY 1011 CENTRAL AUCKLAND AZABU 26 PONSONBY ROAD PONSONBY 1011 CENTRAL AUCKLAND BADUZZI 10-26 JELLICOE STREET WYNYARD QUARTER 1010 CENTRAL AUCKLAND BANGKOK RESTAURANT 1 WELLESLEY STREET AUCKLAND 1010 CENTRAL AUCKLAND BASIL THAI 236 DOMINION ROAD SHOP 2 MOUNT EDEN 1024 CENTRAL AUCKLAND BEAST & BUTTERFLIES RESTAURANT 196-200 QUAY STREET AUCKLAND CENTRAL 1010 CENTRAL AUCKLAND BEDFORD SODA AND LIQUOR 4 BROWN ST SHOP 10 PONSONBY 1021 CENTRAL AUCKLAND BELLOTA SKYCITY AUCKLAND 91 FEDERAL ST AUCKLAND 1010 CENTRAL AUCKLAND BESOS LATINOS 39 ELLIOTT STREET SHOP M16 AUCKLAND 1010 CENTRAL AUCKLAND BIEN IZAKAYA 53B DAVIS CRESCENT NEWMARKET 1023 CENTRAL AUCKLAND BIG LITTLE GRILL 41 ELLIOTT ST AUCKLAND 1010 CENTRAL AUCKLAND BILLFISH CAFE 31 WESTHAVEN DR SHOP 3 ST MARYS BAY 1010 CENTRAL AUCKLAND BISTRO BAMBINA 268 PONSONBY RD PONSONBY