Hasbro, Inc. (Exact Name of Registrant, As Specified in Its Charter)

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Distribution De Jeux Et Jouets

IndexPresse Business Etude Secteurs & marchés Distribution de jeux et jouets Face à la domination des grandes surfaces et à la hausse de l’e-commerce, quel nouveau modèle pour le circuit spécialisé ? secteurs & marchés Distribution de jeux et jouets Face à la domination des grandes surfaces et à la hausse de l’e-commerce, quel nouveau modèle pour le circuit spécialisé ? ntre 2013 et 2018, la part des spécialistes de la distribution de jeux et jouets en France s’est for te- ment contractée sous l’effet de la progression du circuit de l’e-commerce. Auparavant immuable et solide, le secteur fait désormais face à une décélération des ventes et à une transformation du Epaysage de la distribution. Les redressements judiciaires de l’américain Toys’R’Us et de l’enseigne française La Grande Récré ali- mentent les inquiétudes des experts et des professionnels. La distribution spécialisée de jeux et jouets s’interroge sur son avenir. Fondé sur les codes anciens du commerce physique, son modèle doit être repensé pour répondre aux nouvelles attentes des consommateurs, sans renier pour autant les forces qui ont fait son succès. Les enseignes agissent pour asseoir leur ancrage local tout en investissant la sphère numérique. Les réseaux continuent de se développer. Les formats s’ajustent. Le multicanal s’impose. Face à la guerre des prix instaurée par les pure players de l’e-commerce et les grandes surfaces alimen- taires (GSA), il s’agit pour le circuit spécialisé de miser sur ses qualités propres pour faire la différence. L’expertise, la précision de l’offre et la relation de proximité doivent s’imposer pour développer le lien émotionnel qui le rapproche de ses clients. -

Hasbro Closes Acquisition of Saban Properties' Power Rangers And

Hasbro Closes Acquisition of Saban Properties’ Power Rangers and other Entertainment Assets June 12, 2018 PAWTUCKET, R.I.--(BUSINESS WIRE)--Jun. 12, 2018-- Hasbro, Inc. (NASDAQ: HAS) today announced it has closed the previously announced acquisition of Saban Properties’ Power Rangers and other Entertainment Assets. The transaction was funded through a combination of cash and stock valued at $522 million. “Power Rangers will benefit from execution across Hasbro’s Brand Blueprint and distribution through our omni-channel retail relationships globally,” said Brian Goldner, Hasbro’s chairman and chief executive officer. “Informed by engaging, multi-screen entertainment, a robust and innovative product line and consumer products opportunities all built on the brand’s strong heritage of teamwork and inclusivity, we see a tremendous future for Power Rangers as part of Hasbro’s brand portfolio.” Hasbro previously paid Saban Brands$22.25 million pursuant to the Power Rangers master toy license agreement, announced by the parties in February of 2018, that was scheduled to begin in 2019. Those amounts were credited against the purchase price. Upon closing, Hasbro paid $131.23 million in cash (including a $1.48 million working capital purchase price adjustment) and $25 million was placed into an escrow account. An additional $75 million will be paid on January 3, 2019. These payments are being funded by cash on the Company’s balance sheet. In addition, the Company issued 3,074,190 shares of Hasbro common stock to Saban Properties, valued at $270 million. The transaction, including intangible amortization expense, is not expected to have a material impact on Hasbro’s 2018 results of operations. -

Hasbro Second Quarter 2012 Financial Results Conference Call Management Remarks July 23, 2012

Hasbro Second Quarter 2012 Financial Results Conference Call Management Remarks July 23, 2012 Debbie Hancock, Hasbro, Vice President, Investor Relations: Thank you and good morning everyone. Our second quarter earnings release was issued earlier this morning and is available on our website. Additionally, also available on our web site, are presentation slides containing information covered in today’s earnings release and call. The press release and presentation include information regarding Non-GAAP financial measures included in today's call. Please note that during today’s call, whenever we discuss earnings per share or EPS, we are referring to earnings per diluted share. This morning, Brian Goldner, Hasbro’s President and Chief Executive Officer, and Deb Thomas, Hasbro’s CFO, will review our second quarter financial results and discuss important factors impacting our performance. Following their statements, David Hargreaves, Hasbro’s Chief Operating Officer, will join Brian and Deb to field your questions. Before we begin, please note that during this call and the question and answer session that follows, members of Hasbro management may 1 make forward-looking statements concerning management's expectations, goals, objectives and similar matters. These forward- looking statements may include comments concerning our product and entertainment plans, anticipated product performance, business opportunities, plans and strategies, costs, financial goals and expectations for our future financial performance, including expectations for revenues and earnings per share in 2012. There are many factors that could cause actual results or events to differ materially from the anticipated results or other expectations expressed in these forward-looking statements. Some of those factors are set forth in our annual report on form 10-K, our most recent 10-Q, in today's press release and in our other public disclosures. -

GI JOE: RETALIATION Film to Be Released in 3D

May 23, 2012 G.I. JOE: RETALIATION Film to Be Released in 3D Hasbro Reaffirms 2012 Guidance that it Expects to Grow Revenues and Earnings Per Share Absent the Impact of Foreign Exchange PAWTUCKET, R.I.--(BUSINESS WIRE)-- Hasbro, Inc (NASDAQ:HAS), and Paramount Pictures, announced today that G.I. JOE: RETALIATION will now be released in 3D. The film, originally slated for release in June 2012, is scheduled to be released March 29, 2013. "It is increasingly evident that 3D resonates with movie-goers globally and together with Paramount, we made the decision to bring fans an even more immersive entertainment experience," said Brian Goldner, Hasbro's President and CEO. "In 2012, we continue to have several strong motion picture and television entertainment backed properties that are selling well at retail and our entertainment strategy remains strong and on-track," Goldner said. "Through our own Hasbro Studios for television and in partnership with several movie studios including Paramount, Universal, Sony and Relativity, we are creating entertainment experiences around many of our highly popular iconic brands. For the full year 2012, we continue to believe, absent the impact of foreign exchange, we will again grow revenues and earnings per share." Certain statements in this release contain "forward-looking statements" within the meaning of the Private Securities Litigation Reform Act of 1995. These statements include expectations concerning the Company's potential performance in 2012, including with respect to its revenues and earnings per share, and business goals and may be identified by the use of forward- looking words or phrases. The Company's actual actions or results may differ materially from those expected or anticipated in the forward-looking statements due to both known and unknown risks and uncertainties. -

History of the World Rulebook

TM RULES OF PLAY Introduction Components “With bronze as a mirror, one can correct one’s appearance; with history as a mirror, one can understand the rise and fall of a state; with good men as a mirror, one can distinguish right from wrong.” – Emperor Taizong of the Tang Dynasty History of the World takes 3–6 players on an epic ride through humankind’s history. From the dawn of civilization to the twentieth century, you will witness humanity in all its majesty. Great minds work toward technological advances, ambitious leaders inspire their 1 Game Board 150 Armies citizens, and unpredictable calamities occur—all amid the rise and fall (6 colors, 25 of each) of empires. A game consists of five epochs of time, in which players command various empires at the height of their power. During your turn, you expand your empire across the globe, gaining points for your conquests. Forge many a prosperous empire and defeat your adversaries, for at the end of the game, only the player with the most 24 Capitols/Cities 20 Monuments (double-sided) points will have his or her immortal name etched into the annals of history! Catapult and Fort Assembly Note: The lighter-colored sides of the catapult should always face upward and outward. 14 Forts 1 Catapult Egyptians Ramesses II (1279–1213 BCE) WEAPONRY I EPOCH 4 1500–450 BCE NILE Sumerians 3 Tigris – Empty Quarter Egyptians 4 Nile Minoans 3 Crete – Mediterranean Sea Hittites 4 Anatolia During this turn, when you fight a battle, Assyrians 6 Pyramids: Build 1 monument for every Mesopotamia – Empty Quarter 1 resource icon (instead of every 2). -

Credos About Children, P. 2 Littleclickers: Action Cams, P. 3 16 “Nice Touches” When Applying Technology to Language &Am

Helping Teachers, Parents, and Librarians Find Interactive Media Since 1993 May 2016 Volume 24, No. 5, Issue 194 Credos About Children, p. 2 LittleClickers: Action Cams, p. 3 16 “Nice Touches” When Applying Technology to Language & Literacy, p. 4 The Infinite Arcade Children’s Technology Review The the cover: imagesMay 2016 from the well designed by Tinybop, reviewed on page 9 Fisher-Price Soothing Motions Seat, NumberShapes Whiteboard*, p. 13 p. 8 Quasi's Quest, p. 13 Volume 24, No. 5, Issue 194 FurReal Friends Torch My Blazin' Sago Mini Robot Party*, p. 14 Dragon, p. 8 This is My Spacecraft - Rocket Science A Montessori Approach to Math, p. 5 Iconia One 10, p. 8 for Kids, p. 14 And So To Bed - Educational Bedtime Infinite Arcade, The by Tinybop*, p. 9 Time Drop - The Colorful Time Travel, Routine App for Children, p. 5 IQ Safari MATH, p. 9 p. 14 Annie's Picking Apples 2: Learning Labo Paper Plate, p. 9 Veggie Bottoms Kitchen, Games, p. 5 LightUp Edison Kit, p. 10 p. 15 Brainventures, p. 6 MarcoPolo Arctic, p. 10 View-Master Captain McFinn's Swim & Play*, p. 6 Miaomiao’s Chinese New Year, p. 10 Virtual* Denotes Reality Dr. Panda School*, p. 6 MLB The Show 16, p. 11 Viewer“Editor’s 2.0, Monopoly Ultimate Banking, p. 11 p. 15 DYI Gamer Kit, p. 7 Choice.” ExplorArt Klee - The Art of Paul Klee, Montessori Numbers: Learn to Count for Kids*, p. 7 from 1 to 1000*, p. 12 Find Adventure,Our Alfie 12,160th Atkins, Reviewp. -

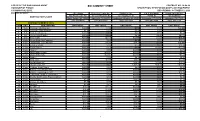

Bid Summary Sheet Contract No

OFFICE OF THE PURCHASING AGENT BID SUMMARY SHEET CONTRACT NO. 14-04-24 TOWNSHIP OF EDISON DESCRIPTION: RECREATION GAMES AND EQUIPMENT 100 MUNICIPAL BLVD. BID OPENING: OCTOBER 10, 2014 EDISON, NJ 08817 ARC Sports Metuchen Center Inc. Flaghouse Inc. S & S Worldwide School Specialty Inc. 850 Peach Lake Rd 10-12 Embroidery St 601 Flaghouse Dr 75 Mill St 140 Marble Dr CONTRACTOR'S NAME North Salem, NY 10560 Sayreville, NJ 08872 Hasbrouck Heights, NJ 07604 Colchester, CT 06415 Lancaster, PA 17601 (203) 775-4140 (732) 418-1388 (800) 793-7900 (800) 642-7354 (888) 388-3224 CONTRACT EXPIRES:1/9/16 ITEM UNIT DESCRIPTION UNIT PRICE UNIT PRICE UNIT PRICE UNIT PRICE UNIT PRICE 1 Sets Checkers (No Boards) NO BID $1.65 $1.53 $1.76 NO BID 2 Sets Checkers (With Boards) $2.75 $2.75 $3.34 $3.07 $2.58 3 Sets Chinese Checkers NO BID $2.95 $4.61 $9.10 $3.56 4 Dz Chess Sets (Plastic) NO BID $35.00 $4.18 $56.40 $43.32 5 Sets Bocci Balls NO BID $21.95 NO BID $12.00 $11.98 6 Each Koosh Balls (No Paddles) NO BID $2.95 $2.12 $2.46 $13.46 7 Each Ladder Ball Toss (Blongo) NO BID $21.50 $27.29 $21.00 NO BID 8 Each Hackey Sacks NO BID $2.95 $2.52 $1.76 $11.98 9 Each Potato Sacks NO BID $2.00 $1.00 * $14.64 * $13.24 10 Each "Skip It" NO BID $5.50 NO BID $1.40 $9.73 11 Pairs Magic Mitts & Balls NO BID NO BID NO BID $5.70 $4.30 12 Each Magic Mitts Balls NO BID NO BID NO BID $1.32 *$5.38 13 Each Frisbee NO BID $3.95 $6.11 $1.00 $4.67 14 Each Ring Toss NO BID $11.95 $10.07 $9.80 $10.86 15 Each Hoola Hoops 30" NO BID $1.95 *$36.97 * $24.48 * $16.25 16 Each Hoola Hoops 36" NO BID $2.25 * $47.74 * $30.96 * $17.72 17 Each Chinese Jump Ropes NO BID $2.95 $2.58 $1.13 $8.63 18 Each Rubber Jump Ropes-9 ft. -

Speech Sounds Vowels HOPE

This is the Cochlear™ promise to you. As the global leader in hearing solutions, Cochlear is dedicated to bringing the gift of sound to people all over the world. With our hearing solutions, Cochlear has reconnected over 250,000 cochlear implant and Baha® users to their families, friends and communities in more than 100 countries. Along with the industry’s largest investment in research and development, we continue to partner with leading international Speech Sounds:Vowels researchers and hearing professionals, ensuring that we are at the forefront in the science of hearing. A Guide for Parents and Professionals For the person with hearing loss receiving any one of the Cochlear hearing solutions, our commitment is that for the rest of your life in English and Spanish we will be here to support you Hear now. And always Ideas compiled by CASTLE staff, Department of Otolaryngology As your partner in hearing for life, Cochlear believes it is important that you understand University of North Carolina — Chapel Hill not only the benefits, but also the potential risks associated with any cochlear implant. You should talk to your hearing healthcare provider about who is a candidate for cochlear implantation. Before any cochlear implant surgery, it is important to talk to your doctor about CDC guidelines for pre-surgical vaccinations. Cochlear implants are contraindicated for patients with lesions of the auditory nerve, active ear infections or active disease of the middle ear. Cochlear implantation is a surgical procedure, and carries with it the risks typical for surgery. You may lose residual hearing in the implanted ear. -

Ah-80Catalog-Alt

STRATEGY GAME CATALOG I Reaching our Peek! FEATURING BATTLE, COMPUTER, FANTASY, HISTORICAL, ROLE PLAYING, S·F & ......\Ci l\\a'C:O: SIMULATION GAMES REACHING OUR PEEK Complexity ratings of one to three are introduc tory level games Ratings of four to six are in Wargaming can be a dece1v1ng term Wargamers termediate levels, and ratings of seven to ten are the are not warmongers People play wargames for one advanced levels Many games actually have more of three reasons . One , they are interested 1n history, than one level in the game Itself. having a basic game partlcularly m1l11ary history Two. they enroy the and one or more advanced games as well. In other challenge and compet111on strategy games afford words. the advance up the complexity scale can be Three. and most important. playing games is FUN accomplished within the game and wargaming is their hobby The listed playing times can be dece1v1ng though Indeed. wargaming 1s an expanding hobby they too are presented as a guide for the buyer Most Though 11 has been around for over twenty years. 11 games have more than one game w1th1n them In the has only recently begun to boom . It's no [onger called hobby, these games w1th1n the game are called JUSt wargam1ng It has other names like strategy gam scenarios. part of the total campaign or battle the ing, adventure gaming, and simulation gaming It game 1s about Scenarios give the game and the isn 't another hoola hoop though. By any name, players variety Some games are completely open wargam1ng 1s here to stay ended These are actually a game system. -

View from the Trenches Avalon Hill Sold!

VIEW FROM THE TRENCHES Britain's Premier ASL Journal Issue 21 September '98 UK £2.00 US $4.00 AVALON HILL SOLD! IN THIS ISSUE HIT THE BEACHES RUNNING - Seaborne assaults for beginners SAVING PRIVATE RYAN - Spielberg's New WW2 Movie LANDING CRAFT FLOWCHART - LC damage determination made easy GOLD BEACH - UK D-Day Convention report IN THIS ISSUE PREP FIRE Hello and welcome the latest issue of View From The Trenches. PREP FIRE 2 The issue is slightly bigger than normal due to Greg Dahl’s AVALON HILL SOLD 3 excellent but rather large article and accompanying flowchart dealing with beach assaults. Four extra pages for the same price. Can’t be INCOMING 4 bad. SCOTLAND THE BRAVE 5 In keeping with the seaborne theme there is also a report on the replaying of the Monster Scenarios ‘Gold Beach’ scenario in the D-DAY AT GOLD BEACH 6 D-Day museum in June, and a review of the new Steve Spielberg WW2 movie, Saving Private Ryan. HIT THE BEACHES RUNNING! 7 I hope to be attending ASLOK this year, so I’m not sure if the “THIS IS THE CALL TO ARMS!” 9 next issue will be out at INTENSIVE FIRE yet. If not, it’ll be out soon after IF’98. THE CRUSADERS 12 While on the subject of conventions, if anyone is planning on SAVING PRIVATE RYAN 18 attending the German convention GRENADIER ’98 please get in touch with me. If we can get enough of us to go as a group, David ON THE CONVENTION TRAIL 19 Schofield may be able to organise transport for all us. -

Hasbro's Iconic MR. POTATO HEAD Character Celebrates 60Th Birthday

February 14, 2012 Hasbro's Iconic MR. POTATO HEAD Character Celebrates 60th Birthday Everyone's Favorite Tater Commemorates 60 Spud-tastic Years as a Pop Culture Icon PAWTUCKET, R.I.--(BUSINESS WIRE)-- This year, Hasbro, Inc. (NASDAQ: HAS) will mark the 60th anniversary of the Company's official "spokes spud," the MR. POTATO HEAD character. A classic rite of passage for most preschoolers, the MR. POTATO HEAD toy is one of Hasbro's most cherished characters with more than 100 million toys sold in more than 30 markets around the world. Through the past 60 years, the timeless tater has evolved from a toy box classic into a pop culture icon and has kept himself relevant by tapping into trends and entertainment. "For the past 60 years, the MR. POTATO HEAD toy has inspired imaginative play in young children and charmed fans of all ages through his roles in movies and on television." said Jerry Perez, Senior Vice President and Global Brand Leader, Playskool. "We're thrilled to see that he has evolved from classic parts and pieces to a household name that is ‘rooted' in pop culture and entertainment." The MR. POTATO HEAD character will celebrate this milestone year on his Facebook page enjoying a year of adventures with the MRS. POTATO HEAD character, starting with a birthday bash at American International Toy Fair in New York City. New product introductions for 2012 include the MASHLY IN TH LOVE MR. AND MRS. 60 ANNIVERSARY EDITION set featuring the couple holding Mr. and Mrs. Potato Head admire a birthday cake as a group sings to celebrate Mr. -

November 28, 2005

This holiday season let's give thanks for what we have by helping others. Please place new and unwrapped gifts in the box in 3rd Floor Kitchen. AGE GROUP SUGGESTIONS ONLY Newborn – 2 Years A-B-C ball that rolls, Ring Stacker, Baby’s First Blocks (Fisher Price), Koosh Balls, Soft Cubes-Battat, Tactile Books. Mega Blocks, stacking cups, pegboards, bath toys, knobby shape puzzles, shape sorter, Push n’ Go Vehicles, Musical Stacker, Chime Garden, Dunk n’ Clunk, soft books. Small farm animals, little people, hard plastic cups and plates, push & pull toys, musical instruments, dolls, busy box. 3 – 5 Years Play doh, large beads to string, pip-squeak markers, cars, Magna-doodles, Aquadoodles, magnetic sets, books with flaps, dolls, toy phones, bath toys. Cars, play tools, school bus toy, puzzles, matching games, Barnyard Bingo game, Elefun game, Candyland board game, Chutes and Ladder board game, etc. 6 – 9 Years Character dolls, Don’t Break The Ice Game, other age appropriate games, play cell phones, Trucks, Mr. Mouth Game, Medical Kit, Melissa & Doug Happy Handle Stamp Set. AGE GROUP SUGGESTIONS ONLY 10 – 14 Years ZhuZhu Pets, Lego Sets, Dora Link Dolls, Barbie Dolls and Accessories, Spinmaster Aquadoodle Wall Mat, Alex Toys: Friends 4 Ever Bracelet Kit, Creativity for Kids: Fashion Design Studio, Fisher Price Color Me Flowerz Bouquet Set, Puzzles Wild Planet Hyper Dash Game, Magnext Battle Striker Turbo Tops, Nerf Toys, Lego Sets, Rocky Robot Truck, Remote Control Cars, anything Star Wars, Beyblade Metal Fusion Battle Tops Age appropriate games - Blokus Settlers of Catan, Cadoo by Cranium, Pictionary Jr., Qwirkle, Bananagrams, Bop It, Scrabble, Operation, Connect 4, Apples to Apples, Trouble, Sorry, Monopoly, Taboo, Guess Who.