Annual Rept3/14

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Cooperbaschdissertation.Pdf

THE EVOLUTION OF VICTORIA FOUNDATION FROM 1924 TO 2003 WITH A SPECIAL FOCUS ON THE NEWARK YEARS FROM 1964 TO 2003 by IRENE COOPER-BASCH A Dissertation submitted to the Graduate School-Newark Rutgers, The State University of New Jersey & New Jersey Institute of Technology in partial fulfillment of the requirements for the degree of Doctor of Philosophy Joint Graduate Program in Urban Systems-Education Policy Written under the direction of Dr. Alan R. Sadovnik, Rutgers University Chair and approved by _____________________________________________ Dr. Alan R. Sadovnik, Rutgers University _____________________________________________ Dr. Gabrielle Esperdy, New Jersey Institute of Technology _____________________________________________ Dr. Clement A. Price, Rutgers University _____________________________________________ Dr. Christopher J. Daggett, Geraldine R. Dodge Foundation, Morristown, NJ Newark, New Jersey May, 2014 © 2014 Irene Cooper-Basch ALL RIGHTS RESERVED ABSTRACT OF THE DISSERTATION The Evolution of Victoria Foundation From 1924 to 2003 With a Special Focus on the Newark Years From 1964 to 2003 By IRENE COOPER-BASCH Dissertation Director: Professor Alan Sadovnik This dissertation examines the history of Victoria Foundation from its inception in 1924 through 2003, with a special emphasis on its place-based urban grantmaking in Newark, New Jersey from 1964 through 2003. Insights into Victoria’s role and impact in Newark, particularly those connected to its extensive preK-12 education grantmaking, were gleaned through an analyses of the evolution of Newark, the history of education in Newark, and the history of foundations in America. Several themes emerged from the research, an examination of the archives, and 28 oral history interviews including: charity vs. philanthropy, risk-taking, scattershot grantmaking, self-reflection, issues of race, and evaluation. -

Reiss Testimony

TESTIMONY OF ALAN REISS BEFORE THE NATIONAL COMMISSION ON TERRORIST ATTACKS UPON THE UNITED STATES May 18, 2004 Thank you Chairman Kean, Vice Chairman Hamilton and distinguished members of the Commission for the opportunity to testify before you today. My name is Alan Reiss and I am currently the Deputy Director of Aviation at The Port Authority of New York and New Jersey. Prior to assuming my current position, I was the Director of the agency’s World Trade Department, which operated the World Trade Center. Mr. Chairman, I know that you are familiar with the Port Authority, but for the benefit of the other members of the Commission, The Port Authority of New York and New Jersey operates many of the busiest and most important transportation links in the New York- New Jersey region. Most important to the Commission’s work, the Port Authority built and operated the World Trade Center and continues to own the 16-acre World Trade Center site in Lower Manhattan. September 11th was without a doubt the worst day in the long history of The Port Authority of New York & New Jersey and one of the worst in the history of the United States. This was a profound personal loss for us at the Port Authority. The World Trade Center was our headquarters and 84 members of the Port Authority family died that day; 16 of them civilian building management staff who reported to me and responded to their emergency posts that day. We grieve their loss, and our hearts continue to go out to their families, and to the families of all the victims who died that day. -

Joseph Patella, Esq. ANDREWS KURTH LLP 450 Lexington Avenue, 15Th Floor, New York, New York 10017 Tel: 609.716.6500 Fax: 609.799.7000

Joseph Patella, Esq. ANDREWS KURTH LLP 450 Lexington Avenue, 15th Floor, New York, New York 10017 Tel: 609.716.6500 Fax: 609.799.7000 Thomas E. Starnes, Esq. Charles M. Crout, Esq. ANDREWS KURTH LLP 1350 I Street NW Suite 1100 Washington, DC 20005 Tel: 202.662.2700 Fax: 202.662.2739 NEW JERSEY DEPARTMENT OF ENVIRONMENTAL PROTECTION, THE COMMISSIONER OF THE NEW JERSEY ENVIRONMENTAL PROTECTION AGENCY, and THE ADMINISTRATOR OF THE NEW JERSEY SPILL COMPENSATION FUND, Plaintiffs, vs. SUPERIOR COURT OF NEW JERSEY OCCIDENTAL CHEMICAL CORPORATION, TIERRA SOLUTIONS, INC., MAXUS ENERGY LAW DIVISION - ESSEX COUNTY CORPORATION, REPSOL YPF, S.A, YPF, S.A, DOCKET NO. L-009868-05 YPF HOLDINGS, INC. and CLH HOLDINGS, Defendants, MAXUS ENERGY CORPORATION and TIERRA SOLUTIONS, INC., Third-Party Plaintiffs, vs. 3M COMPANY, AC.C., INC., ACH FOOD COMPANIES, INC., ACTIVE OIL SERVICE, ADCO CHEMICAL COMPANY, AGC CHEMICALS AMERICAS, INC., WAS:144301.l ALDEN-LEEDS, INC., ALLIANCE CHEMICAL, INC., ALUM AX MILL PRODUCTS, INC., AMCOL REALTY CO., AMERICAN INKS AND COATINGS CORPORATION, APEXICAL, INC., APOLAN INTERNATIONAL, INC., ARKEMA, INC., ASHLAND INC., ASHLAND INTERNATIONAL HOLDINGS, INC., ASSOCIATED AUTO BODY & TRUCKS, INC., ATLAS REFINERY, INC., AUTOMATIC ELECTRO-PLATING CORP., AKZO NOBEL COATINGS, INC., BASF CATALYSTS LLC, BASF CONSTRUCTION CHEMICALS INC., BASF CORPORATION, BAYER CORPORATION, BEAZER EAST, INC., BELLEVILLE INDUSTRIAL CENTER, BENJAMIN MOORE & COMPANY, BEROL CORPORATION, B-LINE TRUCKING, INC., BORDEN & REMINGTON CORP., C.S. OSBORNE & CO., CAMPBELL -

Procurement Department Attn: Bid/Proposal Custodian

PROCUREMENT DEPARTMENT ATTN: BID/PROPOSAL CUSTODIAN 2 MONTGOMERY STREET 3RD FLOOR JERSEY CITY, NJ 07302 REQUEST FOR PROPOSALS (RFP) TITLE: DEVELOPMENT & MAINTENANCE OF AN AVIATION FACILITIES MAPPING SYSTEM (FMS) NUMBER: 29362 RESPONSE DUE DATE: Monday March 11, 2013 TIME: 2:00 PM QUESTION DUE DATE: Wednesday February 20, 2013 TIME: 3:00 PM BUYERS NAMES: ISABEL AMADO PHONE#: (201) 395‐3435 EMAIL: [email protected] STACEY WILLNER PHONE#: (201) 395‐3343 EMAIL: [email protected] SUBJECT: REQUEST FOR PROPOSALS FOR PERFORMANCE OF EXPERT PROFESSIONAL SERVICES - DEVELOPMENT AND MAINTENANCE OF AN AVIATION FACILITIES MAPPING SYSTEM (RFP #29362) The Port Authority of New York and New Jersey (hereinafter referred to as the “Authority”) is seeking Proposals in response to this Request for Proposals (RFP) for performance of expert professional services as required to design, develop, and maintain a Facilities Mapping System (FMS) comprised of subsurface utility and surface assets for John F. Kennedy International Airport (JFK), LaGuardia Airport (LGA), Newark Liberty International Airport (EWR), Stewart International Airport (SWF), and Teterboro Airport (TEB), and to include ongoing source document data entry. Work shall also include tasks related to the migration of the existing Utility Management System (UMS), as more fully described herein, to the FMS as well as ongoing field services and UMS document data entry until cutover to the FMS. The selected Proposer shall enter into an agreement with the Authority for two (2) years, with two (2), one (1) year renewal options, at the Authority’s discretion. The scope of the tasks to be performed by the Consultant are set forth in Attachment A (including Appendices thereto) to the Authority’s Standard Agreement (the “Agreement”), included herewith. -

Major Projects ($ in Millions )

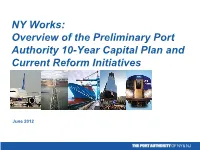

NY Works: Overview of the Preliminary Port Authority 10-Year Capital Plan and Current Reform Initiatives June 2012 Backdrop . The Great Recession and unacceptable levels of unemployment in the region . New York Building Congress 1st Qtr Report on Construction Employment states that employment in the NYC construction industry fell to its lowest level since 1999 . Construction employment was down 3% from the 1st Qtr of 2011 in NYC . Billions of dollars of infrastructure investment required in the State and region . Port Authority doesn’t itself have resources to make all required investment so private capital must be explored and priorities selected . Port Authority a solid credit but is significantly more leveraged than 10 years ago. Ratings: S&P: AA- (Stable), Moody’s: Aa2 (Negative), Fitch: AA- (Stable) . Tolls have increased significantly in excess of CPI and growth in Median Family Income over last 10 years . Burden on Stated Island commuters . Direction from Governor Cuomo to Reform, Rationalize, and Repair . State Level Reform: Design/Build (December 2011); TIF Reform (April 2012); NY Works (April 2012) 2 Backdrop: Toll and Fare Growth in Excess of CPI Tolls & fares have reached a ceiling in this low-growth economic environment Tolls & fares have grown at a rate in excess of CPI and Median Household Income PANYNJ Tolls vs. CPI PANYNJ Annual Tolls as % of Median $14 Household Income $12 4.0% $10 3.5% $8 3.0% $6 2.5% $4 2.0% $2 1.5% $0 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 1.0% 0.5% Cash Toll 0.0% E-ZPass Peak Toll [Roundtrip] 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2001 EZ Pass Toll escalated with CPI PA toll increases during the past decade have Tolls for PA daily commuters have increased by 50% outpaced inflation significantly as a percentage of median household income 3 Backdrop: High Debt Load . -

Procurement Department 4 World Trade Center, 21St Fl. 150 Greenwich Street New York, Ny 10007

PROCUREMENT DEPARTMENT 4 WORLD TRADE CENTER, 21ST FL. 150 GREENWICH STREET NEW YORK, NY 10007 INVITATION FOR BID/PUBLIC BID OPENING BID INFORMATION TITLE: MOVING SERVICES ON A WORK ORDER BASIS FOR VARIOUS PORT AUTHORITY FACILITIES IN NEW YORK AND NEW JERSEY BID NO.: 53782 SUBMIT SEALED BIDS BEFORE THE DUE DATE AND TIME TO THE ABOVE ADDRESS WHERE THEY WILL BE PUBLICLY OPENED AND READ FACILITY INSPECTION: JULY 12, 2018 TIME: 1:00 P.M. BID DUE DATE: JULY 17, 2018 TIME: 11:00 A.M. BUYER NAME: LUZ SANTANA PHONE NO.: 212-435-4625 FAX NO.: 212-435-4691 EMAIL: [email protected] BIDDER INFORMATION (TO BE COMPLETED BY THE BIDDER) (PLEASE PRINT) ________________________________________________________________________________________________________ (BIDDING ENTITY’S LEGAL BUSINESS NAME) ________________________________________________________________________ (ADDRESS) ________________________________________________________________________ (CITY, STATE AND ZIP CODE) ________________________________________________________________________ (REPRESENTATIVE TO CONTACT - NAME & TITLE) (TELEPHONE) _________________________________________________________________________ (FEDERAL TAX I.D. NO.) (FAX NO.) _____ BUSINESS CORPORATION _______PARTNERSHIP ______INDIVIDUAL _____ OTHER (SPECIFY): __________________________________________________ Rev. 12/12/2017 INVITATION FOR BID o COVER PAGE: BID AND BIDDER INFORMATION o PART I – STANDARD INFORMATION FOR BIDDERS o PART II – CONTRACT SPECIFIC INFORMATION FOR BIDDERS o PART III – CONTRACT SPECIFIC TERMS AND CONDITIONS o PART IV – SIGNATURE SHEET, NAME AND RESIDENCE OF PRINCIPALS AND PRICING SHEET(S) o PART V – SPECIFICATIONS o STANDARD CONTRACT TERMS AND CONDITIONS TABLE OF CONTENTS PART I - 1 PART I – STANDARD INFORMATION FOR BIDDERS Rev. 12/21/17 (PA) PART I - STANDARD INFORMATION FOR BIDDERS, TABLE OF CONTENTS 1. General Information: The Port Authority of New York and New Jersey ............... 3 2. Form and Submission of Bid ................................................................................. -

A Port Authority That Works

A Port Authority That Works March 2014 Mitchell L. Moss Hugh O’Neill Mitchell L. Moss is Director of the Rudin Center for Transportation Policy and Management at New York University, and Henry Hart Rice Professor of Urban Planning at NYU’s Wagner School of Public Service. Hugh O’Neill is President of Appleseed, an economic development consulting firm based in New York City. From 1985 to 1991, he was Assistant Executive Director of the Port Authority of New York and New Jersey. This report and additional information on the Rudin Center, are available at www.NYURudinCenter.com A Port Authority That Works 3 Executive Summary The Port Authority of New York and New Airport) for two important purposes: Jersey has been a vital force in the physical and economic growth of the New York-New • To help meet the capital and operating Jersey region. During the past few years, needs of Port Authority facilities that don’t however, public attention has focused on the generate sufficient revenue to cover their Port Authority’s spending, management, and own costs; political interference in the agency’s operations. In recent weeks, several sources have called for • To allow the Port Authority to invest in reform, restructuring, or even abolition of the new facilities that over time will help to Port Authority. grow both its own revenues and the region’s economy. However, the critical problem facing the Port Authority today is not mismanagement, While this basic framework remains in place political abuse, or rivalry between New York today, the ways in which it is used have evolved and New Jersey. -

2015 Budget MISSION STATEMENT

December 10, 2014 Corrected as of January 22, 2015 2015 Budget MISSION STATEMENT MEET THE CRITICAL TRANSPORTATION INFRASTRUCTURE NEEDS OF THE BI-STATE REGION'S PEOPLE, BUSINESSES, AND VISITORS BY PROVIDING THE HIGHEST QUALITY AND MOST EFFICIENT TRANSPORTATION AND PORT COMMERCE FACILITIES AND SERVICES TO MOVE PEOPLE AND GOODS WITHIN THE REGION, PROVIDE ACCESS TO THE NATION AND THE WORLD AND PROMOTE THE REGION’S ECONOMIC DEVELOPMENT. Port Authority of New York and New Jersey Facilities NEW YORK STATE THRUWAY NEW STATE YORK Y A Poughkeepsie W U ULSTER R H T NEW YORK E T A T S K DUTCHESS R O Y W E WESTCHESTER N 84 Beacon Newburgh STEWART INTERNATIONAL AIRPORT 87 ORANGE PUTNAM ROCKLAND West Point NYNJ RAIL GREENVILLE YARD NYNJ RAIL 51ST STREET YARD NYNJ RAIL 65th STREET YARD ATLANTIC CITY EXPRESSWAY A TL ATLANTIC AN T ATLANTIC CITY IC C AIRPORT I T Y E X Galloway P R ESSW AY Absecon Egg Harbor AY Township W K R A P E AT T S ATLANTIC CITY N E D GARDENR STATE PARKWAY A ATLANTIC G OCEAN Legend: Aviation Development Port Authority Trans-Hudson Port Commerce Tunnels, Bridges & Terminals TABLE OF CONTENTS Section Page Government Finance Officers Association Award ……………………………………………………………… 2 Message from the Chairman and the Executive Director …………………………………………………… 3 2015 Budget Summary ……………………………………………………………………………………………………… 5 2015 Line Department Budget Summary …………………………………………………………………………… 17 Aviation 19 Tunnels, Bridges and Terminals 25 Port Authority Trans Hudson 31 Port Commerce 37 Development 43 World Trade Center 47 2015 Budget Schedules ……………………………………………………………………………………………………… 51 Reader's Guide 53 Summary of 2015 Budget - Sources & Uses 54 2015 Budget* 57 Sources 58 Uses 62 Budget Support Schedules 68 Outstanding Obligations and Financing 74 Staffing 76 Activity Highlights 78 2015 Capital Budget Summary …………………………………………………………………………………………… 81 By Department 83 By Department, Facility, & Program 84 Appendices ………………………………………………………………………………………………………………………. -

Hearing Unit Cover and Text

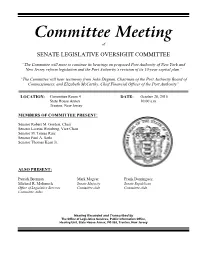

Committee Meeting of SENATE LEGISLATIVE OVERSIGHT COMMITTEE “The Committee will meet to continue its hearings on proposed Port Authority of New York and New Jersey reform legislation and the Port Authority’s revision of its 10-year capital plan” “The Committee will hear testimony from John Degnan, Chairman of the Port Authority Board of Commissioners, and Elizabeth McCarthy, Chief Financial Officer of the Port Authority” LOCATION: Committee Room 4 DATE: October 28, 2015 State House Annex 10:00 a.m. Trenton, New Jersey MEMBERS OF COMMITTEE PRESENT: Senator Robert M. Gordon, Chair Senator Loretta Weinberg, Vice Chair Senator M. Teresa Ruiz Senator Paul A. Sarlo Senator Thomas Kean Jr. ALSO PRESENT: Patrick Brennan Mark Magyar Frank Dominguez Michael R. Molimock Senate Majority Senate Republican Office of Legislative Services Committee Aide Committee Aide Committee Aides Hearing Recorded and Transcribed by The Office of Legislative Services, Public Information Office, Hearing Unit, State House Annex, PO 068, Trenton, New Jersey TABLE OF CONTENTS Page John J. Degnan Chairman Board of Commissioners The Port Authority of New York and New Jersey 6 Elizabeth M. McCarthy Chief Financial Officer Office of the Chief Financial Officer Office of the Executive Director The Port Authority of New York and New Jersey 14 APPENDIX: The Port Authority of New York and New Jersey 2014 Annual Report A Clear Path Forward submitted by John J. Degnan 1x The Port Authority of New York and New Jersey Capital Projects Timeline submitted by Elizabeth M. McCarthy 120x pnf: 1-66 SENATOR ROBERT M. GORDON (Chair): Good morning, everyone, and welcome to the Senate Legislative Oversight Committee. -

Special Panel on the Future of the Port Authority

New debt KEEPING THE REGION MOVING The Port Authority of New York and New Jersey A report prepared by The Special Panel on the Future of the Port Authority for The Governors of New York and New Jersey December 26, 2014 i Special Panel on the Future of the Port Authority The Port Authority of NY & NJ: Keeping the Region Moving Special Panel on the Future of the Port Authority John J. Degnan Scott H. Rechler Chairman of the Port Authority of Vice Chairman of the Port Authority of New York and New Jersey New York and New Jersey Richard H. Bagger Mylan L. Denerstein* Commissioner of the Port Authority of Counsel to the Governor of New York New York and New Jersey xxxxxxxxx Christopher S. Porrino Seth H. Agata Chief Counsel to the Governor of New Jersey Acting Counsel to the Governor of New York ∗ Served from May to September 2014. Special Panel on the Future of the Port Authority The Port Authority of NY & NJ: Keeping the Region Moving Table of Contents 1. Executive Summary ............................................................................................................................................1 1.1. Background .................................................................................................................................................1 1.2. Recommendations ......................................................................................................................................3 A. Governance and Accountability .................................................................................................................3 -

Preliminary 2012 Budget Summary…………………………………………………………..… 13

Prelimina ry 2012 Budget December 8, 2011 MISSION To identify and meet the critical transportation infrastructure needs of the bistate region’s businesses, residents, and visitors: providing the highest quality, most efficient transportation and port commerce facilities and services that move people and goods within the region, providing access to the rest of the nation and to the world, while strengthening the economic competitiveness of the New York-New Jersey Metropolitan Region. TABLE OF CONTENTS Government Finance Officers Association Award………………………………………..……. 2 Message from the Chairman and Executive Director……………………..……………………. 3 The Port Authority in a Post-Recession Environment……...………………………………..…. 7 Preliminary 2012 Budget Summary…………………………………………………………..… 13 Preliminary 2012 Budget Summary by Line Department………………………………..……. 25 a. Aviation…………………………………………………………………………… 27 b. Tunnels, Bridges and Terminals…………………………………………….… 32 c. PATH…………………………………………………………………………….. 37 d. Port Commerce………………………..………………………………………… 41 e. Real Estate and Development…………………………………………………. 45 f. World Trade Center……………………………………………………………… 47 Preliminary 2012 Budget Schedules.…………………………………………..………………...51 a. Summary of Preliminary 2012 Budget………………………………………… 53 b. Sources…………………………………………………………………………… 56 c. Uses…………………………………………………………………………………60 d. Changes in Retained Earnings, Consolidated Statement of Net Assets, Information on P.A. Operations by Facility, Revenues and Reserves, and Assets & Liabilities………………………………………………………… 67 e. Outstanding Obligations -

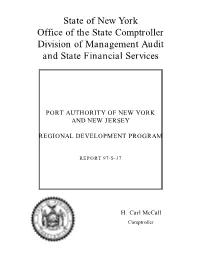

State of New York Office of the State Comptroller Division of Management Audit and State Financial Services

State of New York Office of the State Comptroller Division of Management Audit and State Financial Services PORT AUTHORITY OF NEW YORK AND NEW JERSEY REGIONAL DEVELOPMENT PROGRAM REPORT 97-S-37 H. Carl McCall Comptroller State of New York Office of the State Comptroller Division of Management Audit and State Financial Services Report 97-S-37 Mr. Lewis M. Eisenberg Chairman Port Authority of New York and New Jersey One World Trade Center New York, NY 10048 Dear Mr. Eisenberg: The following is our report on the Port Authority of New York and New Jersey’s Regional Development Program. We did this audit according to the State Comptroller’s authority as stated in Section 7071 of the Unconsolidated Laws of New York. We list major contributors to this report in Appendix A. September 30, 1998 OSC Management Audit reports can be accessed via the OSC Web Page : http://www.osc.state.ny.us. If you wish your name to be deleted from our mailing list or if your address has changed, contact the Management Audit Group at (518) 474-3271 or at the Office of the State Comptroller, Alfred E. Smith State Office Building, 13th Floor, Albany, NY 12236. Executive Summary Port Authority of New York and New Jersey Regional Development Program Scope of Audit In 1978, the legislatures of the states of New York and New Jersey authorized the Port Authority of New York and New Jersey (Port Authority) to undertake a regional development program that included the construction and operation of industrial parks and other economic development projects in the inner cities of the Port Authority region.