Open PDF 240KB

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

The State of Broadband 2019 Broadband As a Foundation for Sustainable Development

International The State of Broadband: Telecommunication Union Broadband as a Foundation Place des Nations CH-1211 Geneva 20 Switzerland for Sustainable Development September 2019 ISBN 978-92-61-28971-3 9 7 8 9 2 6 1 2 8 9 7 1 3 Published in Switzerland broadbandcommission.org Geneva, 2019 THE STATE OF BROADBAND 2019 Broadband as a Foundation for Sustainable Development ITU/UNESCO Broadband Commission for Sustainable Development © International Telecommunication Union and United Nations Educational, Scientific and Cultural Organization, 2019 Some rights reserved. This work is available under the Creative Commons Attribution-NonCommercial- ShareAlike 3.0 IGO licence (CC BY-NC-SA 3.0 IGO; https:// creativecommons .org/ licenses/by -nc -sa/ 3 .0/ igo).). Under the terms of this licence, you may copy, redistribute and adapt the work for non-commercial purposes, provided the work is appropriately cited, as indicated below. In any use of this work, there should be no suggestion that ITU or UNESCO endorses any specific organization, products or services. The unauthorized use of the ITU or UNESCO names or logos is not permitted. If you adapt the work, then you must license your work under the same or equivalent Creative Commons licence. If you create a translation of this work, you should add the following disclaimer along with the suggested citation: “This translation was not created by the International Telecommunication Union (ITU) or the United Nations Educational, Scientific and Cultural Organization (UNESCO). Neither ITU nor UNESCO are responsible for the content or accuracy of this translation. The original English edition shall be the binding and authentic edition”. -

Governance Report

Governance report In this section 82 Our Board of directors 86 Our Executive Committee 88 Chair’s introduction 90 Our leadership 97 Board evaluation 100 Audit and Risk Committee report 110 Nominations Committee report 115 Our compliance with the UK Corporate Governance Code 119 Directors’ report 123 Directors’ responsibilities statement 124 Directors’ remuneration report Airtel Africa plc Annual Report and Accounts 2021 81 © 2021 Friend Studio Ltd File name: BoardXandXExecXCommittee_v48 Modification Date: 26 May 2021 8:22 am Governance report Our Board of directors Sunil Bharti Mittal Raghunath Mandava Chair Chief executive officer N M Date appointed to Board: October 2018 Date appointed to Board: July 2018 Independent: no Independent: no Age: 63 Age: 54 Nationality: Indian Nationality: Indian Skills, expertise and contribution Skills, expertise and contribution Sunil is the founder and chairman of Bharti Enterprises, one of India’s leading Raghu has held a variety of sales, marketing, customer experience and general conglomerates with diversified interests in telecoms, insurance, real estate, management roles in the FMCG and telecoms industries. Raghu joined Airtel Africa agriculture and food, renewable energy and other ventures. Bharti Airtel, the flagship Group as chief operating officer in 2016 and took over as CEO in January 2017. company of Bharti Enterprises, is a global telecommunications company operating in To his role as CEO, he brings a deep understanding of telecoms and a strong belief 18 countries across South Asia and Africa. It’s one of the top three mobile operators that connectivity can accelerate growth by helping to bridge the digital divide and globally, with a network covering over two billion people. -

Airbus, Delta, Oneweb, Sprint, Airtel Announce the Formation Of

Airbus, Delta, OneWeb, Sprint, Airtel Announce the Formation of Seamless Air Alliance Enabling Airlines to Empower Passengers with Seamless In-Cabin Connectivity Experience The Alliance welcomes interested parties to join as members to be at the forefront of driving global change to enhance passenger experience Barcelona, 26th February 2018 – Airbus, Delta, OneWeb, Sprint, and Bharti Airtel (“Airtel”) announce the formation of the Seamless Air Alliance – which will usher in a new era of innovation for airlines on all routes. By empowering member mobile operators to extend their services into airline cabins, the Seamless Air Alliance will allow them to continuously provide their customers - via satellite technology - with the same high speed, low latency connectivity from ground, to air and back again. It will also significantly reduce costs for everyone involved while creating a smooth, positive user-experience. The alliance – which aims to attract additional industry operators beyond the five initial members – will eliminate the immense costs and hurdles commonly associated with acquisition, installation, and operation of data access infrastructure by streamlining system integration and certification, providing open specifications for interoperability, increasing accessibility for passengers, and enabling simple and integrated billing. “What if the best internet you ever experienced was in the air? Keeping this goal in mind, together, we will enable an affordable and frictionless experience for passengers everywhere,” said Greg Wyler, Founder and Executive Chairman of OneWeb. “With the launch of our first production satellites set for later this year, we’re one step closer to bridging the global Digital Divide on land and in the air.” “Easy-to-use, high-speed connectivity is part of the next revolution in aerospace,” said Marc Fontaine, Airbus Digital Transformation Officer. -

Revue De Presse Sectorielle Numerique Une Publication Du Service Économique Regional De New Delhi

REVUE DE PRESSE SECTORIELLE NUMERIQUE UNE PUBLICATION DU SERVICE ÉCONOMIQUE REGIONAL DE NEW DELHI N° 9 1 au 15 Juillet 2021 G En bref NUMÉRIQUE : - La nouvelle stratégie indienne en matière de cybersécurité sera publiée cette année - Les nouvelles règles IT vont créer un écosystème responsable pour les médias sociaux le nouveau ministre de naw - WhatsApp n'appliquera pas sa nouvelle politique en matière de données personnelles tant que l'Inde n'aura pas adopté sa loi sur la protection des données. - Le gouvernement indien représente 25% des demandes mondiales d'information de gouvernements auprès de Twitter. - La RBI interdit Mastercard de nouvelles cartes en Inde au motif du non respect de l TÉLÉCOMMUNICATIONS: - La société néerlandaise de semi-conducteurs NXP fournira des puces à Jio pour son réseau 5G. - SpaceX prêt à s'associer à des entreprises indiennes pour fabriquer localement des équipements de communication satellitaire. - Brookfield asset management et Digital Realty forment une coentreprise pour construire des data centers en Inde. REVUE DE PRESSE SECTORIELLE NUMERIQUE The companies allowed must be a 'trusted Revue de presse source', he said adding, "We were able to create and launch the trusted telecom portal during the 1. NUMÉRIQUE pandemic and within six months." Govt to unveil national cyber security New IT rules will empower users, says strategy soon: National Cyber Security Ashwini Vaishnaw Coordinator ET Bureau, 11/07/2021 PTI, 3/07/2021 Ashwini Vaishnaw, the newly appointed Union The government will release a new cybersecurity Minister of Electronics and IT, Communication strategy this year, National Cyber Security and Railways, said on Sunday that the new Coordinator Rajesh Pant said at an event Information Technology Rules will empower organised by Public Affairs Forum of India (PAFI). -

Syrlinks Keeps Pace with Airbus Oneweb Satellites

NewSpace Syrlinks keeps pace with Airbus OneWeb Satellites Press Release In Cesson-Sévigné, France, May 4th, 2021. OneWeb continues the deployment of its large-constellation with 36 additional satellites launched April 25th,2021, from Vostochny Cosmodrome spaceport in Russia. (flight ST31 from Arianespace). OneWeb overall project aims at offering in 2022 high-speed, low- latency connectivity services thanks to a 648 LEO (Low Earth Orbit) satellite constellation. In this project, Syrlinks is supplying two key products for the manufacturing factory, Airbus OneWeb Satellites: © ArianeSpace • TT&C transceivers to control the satellites from ground stations • Low Noise Amplifier (LNA) at the input of the onboard GPS receiver. Thanks to these major elements, communication link (ie more precisely Telecommand & Control), between each Spacecraft and the ground, is permitted. Syrlinks is also supplying crystal oscillator for other subsystems within the spacecraft. TT&C LNA GPS OCXO “At Syrlinks, we are following with pride the successive launches of OneWeb to build this amazing large-constellation”, says Gwénaël GUILLOIS, General Manager at Syrlinks. “It’s a great recognition of our team’s capability to produce and deliver our space RF products in large quantities and despite the Covid-19 situation.” Adds Gwénaël. About Syrlinks Syrlinks, is a French company, founded in 2011 near Rennes. The company designs and deliver worldwide RF communication products to address four market segments: Space, Defense, Safety and Time-frequency. Its products are now deployed on hundreds of satellites and have also been used in many high-profile space missions such as Rosetta and its small Philae Robot to explore Comet Chury at the edge of our solar system. -

The Commercial Satellite Industry: What’S up and What’S on the Horizon

S. HRG. 115–569 THE COMMERCIAL SATELLITE INDUSTRY: WHAT’S UP AND WHAT’S ON THE HORIZON HEARING BEFORE THE COMMITTEE ON COMMERCE, SCIENCE, AND TRANSPORTATION UNITED STATES SENATE ONE HUNDRED FIFTEENTH CONGRESS FIRST SESSION OCTOBER 25, 2017 Printed for the use of the Committee on Commerce, Science, and Transportation ( Available online: http://www.govinfo.gov U.S. GOVERNMENT PUBLISHING OFFICE 35–753 PDF WASHINGTON : 2019 VerDate Nov 24 2008 13:09 Mar 27, 2019 Jkt 000000 PO 00000 Frm 00001 Fmt 5011 Sfmt 5011 S:\GPO\DOCS\35753.TXT JACKIE SENATE COMMITTEE ON COMMERCE, SCIENCE, AND TRANSPORTATION ONE HUNDRED FIFTEENTH CONGRESS FIRST SESSION JOHN THUNE, South Dakota, Chairman ROGER F. WICKER, Mississippi BILL NELSON, Florida, Ranking ROY BLUNT, Missouri MARIA CANTWELL, Washington TED CRUZ, Texas AMY KLOBUCHAR, Minnesota DEB FISCHER, Nebraska RICHARD BLUMENTHAL, Connecticut JERRY MORAN, Kansas BRIAN SCHATZ, Hawaii DAN SULLIVAN, Alaska EDWARD MARKEY, Massachusetts DEAN HELLER, Nevada CORY BOOKER, New Jersey JAMES INHOFE, Oklahoma TOM UDALL, New Mexico MIKE LEE, Utah GARY PETERS, Michigan RON JOHNSON, Wisconsin TAMMY BALDWIN, Wisconsin SHELLEY MOORE CAPITO, West Virginia TAMMY DUCKWORTH, Illinois CORY GARDNER, Colorado MAGGIE HASSAN, New Hampshire TODD YOUNG, Indiana CATHERINE CORTEZ MASTO, Nevada NICK ROSSI, Staff Director ADRIAN ARNAKIS, Deputy Staff Director JASON VAN BEEK, General Counsel KIM LIPSKY, Democratic Staff Director CHRIS DAY, Democratic Deputy Staff Director RENAE BLACK, Senior Counsel (II) VerDate Nov 24 2008 13:09 Mar 27, 2019 Jkt 000000 PO 00000 Frm 00002 Fmt 5904 Sfmt 5904 S:\GPO\DOCS\35753.TXT JACKIE C O N T E N T S Page Hearing held on October 25, 2017 ......................................................................... -

On the Path to 6G: Embracing the Next Wave of Low Earth Orbit Satellite Access

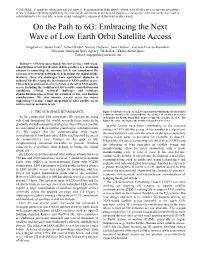

© 2021 IEEE. Personal use of this material is permitted. Permission from IEEE must be obtained for all other uses, in any current or future media, including reprinting/republishing this material for advertising or promotional purposes, creating new collective works, for resale or redistribution to servers or lists, or reuse of any copyrighted component of this work in other works. On the Path to 6G: Embracing the Next Wave of Low Earth Orbit Satellite Access Xingqin Lin†, Stefan Cioni‡, Gilles Charbit§, Nicolas Chuberre⊥, Sven Hellsten†, and Jean-Francois Boutillon⊥ †Ericsson, ‡European Space Agency, §MediaTek, ⊥Thales Alenia Space Contact: [email protected] Abstract— Offering space-based Internet services with mega- constellations of low Earth orbit (LEO) satellites is a promising solution to connecting the unconnected. It can complement the coverage of terrestrial networks to help bridge the digital divide. However, there are challenges from operational obstacles to technical hurdles facing the development of LEO satellite access. This article provides an overview of state of the art in LEO satellite access, including the evolution of LEO satellite constellations and capabilities, critical technical challenges and solutions, standardization aspects from 5G evolution to 6G, and business considerations. We also identify several areas for future exploration to realize a tight integration of LEO satellite access with terrestrial networks in 6G. I. THE NEW SPACE RENAISSANCE Figure 1: Global coverage of a LEO constellation with hundreds of satellites at 600 km altitude. (The colors indicate the number of satellites in view for As the commercial fifth generation (5G) systems are being each point on Earth. Dark blue denotes only one satellite in view. -

Airtel Sunil Bharti Mittal on a Chairman, Airtel Strong Wicket with Price War Over and a Digital Portfolio in Place, Airtel Is Keen to Play on the Front Foot Again

RNI No.35850/80; Reg. No. MCS-123/2018-20; Published on: Every alternate Monday; Posted at Patrika Channel Sorting office, Mumbai-400001 on every alternate Wednesday-Thursday R100 n SEMICONDUCTORS n CP COMMUNITIES n GR INFRAPROJECTS April 19 to May 2, 2021 n KPIT Airtel Sunil Bharti Mittal On a Chairman, Airtel strong wicket With price war over and a digital portfolio in place, Airtel is keen to play on the front foot again... BUSINESS INDIA u THE MAGAZINE OF THE CORPORATE WORLD From the Publisher Publisher Ashok H. Advani Executive Editors Lancelot Joseph, Daksesh Parikh, Sarosh Bana, Deputy Editors Shonali Shivdasani (Mumbai), Sajal Bose (Kolkata) Consulting Editors Dr. Shashank Shah, Sunil Damania (Mumbai), Sekhar Seshan (Pune) Assistant Editors Arbind Gupta, Ryan Rodrigues, Kayus Wadia (Mumbai), Yeshi Seli (Delhi) Sunil Mittal and Airtel is a story of grit and resilience. Principal Correspondent Krishna Kumar C.N. (Mumbai) Photo Editor Palashranjan Bhaumick Many of our readers will recall that Sunil Mittal was Business India’s Photographers Prakash Jadhav, Sanjay Borade Businessman of the Year, as far back as 2002. As Sunil has often said, this Design Trilokesh Mukherjee Art Director Mukesh Pandya was the first major recognition by a national magazine. Many awards and Graphics Prajakta Sawant accolades followed as Airtel became the largest player in India. Cartoonist Panju Ganguli Manager – Design Cell Mathew Thomas Sunil, who won the Delhi licence, was one among the first 8 licensees, Production Team Balachandran, Kisan Kumbhar, Najeeb Fatehi, Sudhir Khaladkar, Vasant Dhasade with 2 licences being granted for the four major metros in November 1994. -

Spacex Eyes Local Partners to Make Satcom Gear

AHEAD OF LAUNCH OF ITS HIGH-SPEED STARLINK SATELLITE BROADBAND SERVICES IN INDIA NEXT YEAR... SpaceX Eyes Local Partners to Make Satcom Gear [email protected] Kolkata: Elon Musk’s SpaceX plans to partner with Indian companies to locally manufacture satellite communications equipment, including antenna systems and user terminal devices, as it gears up to launch its highspeed Starlink satellite broadband services in the country next year. “SpaceX is excited to find ways to work together with the Indian industry for manufacturing products for its Starlink devices,” Matt Botwin, director (market access with the Starlink program), said on Monday during SpaceX’s first official interaction with Department of Telecommunications (DoT) secretary Anshu Prakash. The company always looks for opportunities to maximise the efficiency of its (global) supply chain, and “is now looking forward to working with its partners in India to recognise those opportunities”, Botwin said. The DoT had called a meeting with global satellite companies to discuss a holistic roadmap for locally manufacturing satellit e communications gear and ways to create an enabling regulatory regime for global low earth orbit (LEO) satellite constellation operators to establish in-country gateways in India. Those present at the meeting included officials from OneWeb, Viasat, Hughes, Airtel, Reliance Jio, Vodafone Idea, Department of Space, and the Telecom Regulatory Authority of India. India's satellite based communications space is heating up with the likes of SpaceX, Bharti Global-backed OneWeb and Jeff Bezos-led Amazon’s Project Kuiper looking to enter the country’s nascent satellite broadband space starting next year. During the meeting, Botwin, one of Musk’s key lieutenants, said, “SpaceX has been working with the Indian industrial sector for a long time, buying steel and steel-tubing for many of its rockets.” It is now committed to manufacturing hardware and satellite components and components of (satellite broadband) networks in India, he said. -

De New Delhi

REVUE DE PRESSE SECTORIELLE NUMERIQUE UNE PUBLICATION DU SERVICE ÉCONOMIQUE REGIONAL DE NEW DELHI N° 4 –20 au 30 Avril 2021 G En bref NUMÉRIQUE : - Atos acquiert le canadien Processia, le britannique Ipsotek et l’allemand Cryptovision après l'échec du rachat de l’américain DXC technology. - L'Australie et l'Inde annoncent un programme conjoint de recherche sur l’IA, la 5G, l'internet des objets et l'informatique quantique. - La RBI interdit à American Express et Diners Club International de recruter de nouveaux clients en Inde au nom du non respect de la localisation des données. - Le gouvernement indien ordonne à Twitter et Facebook de censurer les messages critiquant la gestion de la crise de la COVID-19. - Multiplication des attaques informatiques chinoises contre les infrastructures critiques indiennes. TÉLÉCOMMUNICATIONS: - L’internet satellitaire semble promis à un bel avenir en Inde. - OneWeb a levé 550 millions de dollars auprès de l'opérateur de satellites français Eutelsat Communications pour une participation de 24 %. - L’Inde pourrait atteindre 820 millions d’utilisateurs 4G cette année, avec une intensification de la couverture du pays. REVUE DE PRESSE SECTORIELLE NUMERIQUE Australia and India team up on critical Revue de presse technology 1. NUMÉRIQUE TechTarget, 22/04/2021 Atos makes three more acquistions while Australia and India have joined hands to advance the reporting a drop in revenue development of critical and emerging technologies such as artificial intelligence (AI), 5G networks, the internet of Reuters, 20/04/2021 things (IoT) and quantum computing through a research grant programme. Gdansk, Poland: Atos SE has acquired three more companies as the French IT consulting group continues its Through the programme, the two countries hope to “help series of bolt-on acquisitions while reporting a drop in its shape a global technology environment that meets first-quarter revenue. -

Transforming Lives Strategic Report

Airtel Africa plc Annual Report and Accounts 2021 Transforming lives Strategic report Transforming lives by bridging the digital divide Strategic report Governance report Financial statements 1 Airtel Africa overview 82 Our Board of directors 140 Independent auditors’ report 8 Chair’s statement 86 Our Executive Committee 150 Consolidated statement 10 Chief executive officer’s review 88 Chair’s introduction of comprehensive income 13 Our investment proposition 90 Our leadership 151 Consolidated statement 14 Our key performance indicators 97 Board evaluation of financial position 16 Covid-19 statement 100 Audit and Risk Committee report 152 Consolidated statement of changes in equity 18 Our market environment 110 Nominations Committee report 153 Consolidated statement 20 Legislation and regulation 115 Our compliance with the UK of cash flows 22 Our business model Corporate Governance Code 154 Notes to consolidated 119 Directors’ report 24 Our strategy financial statements 123 Directors’ responsibilities statement 32 Our stakeholders 210 Company statement 38 Business reviews 124 Directors’ remuneration report of financial position 38 – Nigeria 211 Company statements 40 – East Africa of changes in equity 42 – Francophone Africa 212 Notes to company only 44 – Mobile services financial statements 46 – Airtel Money 48 Airtel Business Other information 49 Digital Labs 214 Forward-looking statements 50 Our sustainability ambition 215 Glossary 54 Corporate responsibility 218 General shareholders’ 60 Chief financial officer’s introduction information to the financial review 62 Financial review 67 Alternative performance measures 72 Managing our risk 79 Our long-term viability statement © 2021 Friend Studio Ltd File name: Overview_v42 Modification Date: 25 May 2021 4:45 pm Strategic report Our business is transforming lives across Africa by bringing telecoms and mobile money services to almost 118.2 million customers in 14 sub- Saharan countries. -

On the Anthropogenic and Natural Injection of Matter Into Earth's

On the Anthropogenic and Natural Injection of Matter into Earth’s Atmosphere Leonard Schulza,∗, Karl-Heinz Glassmeiera,b aInstitut f¨ur Geophysik und extraterrestrische Physik, Technische Universit¨at Braunschweig, 38106 Braunschweig, Germany bMax-Planck-Institut f¨ur Sonnensystemforschung, 37077 G¨ottingen, Germany Abstract Every year, more and more objects are sent to space. While staying in orbit at high altitudes, objects at low altitudes reenter the atmosphere, mostly disintegrating and adding material to the upper atmosphere. The increasing number of countries with space programs, advancing commercialization, and ambitious satellite constellation projects raise concerns about space debris in the future and will continuously increase the mass flux into the atmosphere. In this study, we compare the mass influx of human-made (anthropogenic) objects to the natural mass flux into Earth’s atmosphere due to meteoroids, originating from solar system objects like asteroids and comets. The current and near future significance of anthropogenic mass sources is evaluated, considering planned and already partially installed large satellite constella- tions. Detailed information about the mass, composition, and ablation of natural and anthropogenic material are given, reviewing the relevant literature. Today, anthropogenic material does make up about 2.8 % compared to the annual injected mass of natural origin, but future satellite constellations may increase this fraction to nearly 40 %. For this case, the anthropogenic injection of several metals prevails the injection by natural sources by far. Additionally, we find that the anthropogenic injection of aerosols into the atmosphere increases disproportionately. All this can have yet unknown effects on Earth’s atmosphere and the terrestrial habitat. Keywords: Atmosphere, Satellite constellations, Mass influx, Human-made injection, Anthropogenic effect, Meteoroids, Ablation, Meteorite composition 1.