Inner East London Demand Study

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Witness Statement of Stuart Sherbrooke Wortley Dated April 2021 Urbex Activity Since 21 September 2020

Party: Claimant Witness: SS Wortley Statement: First Exhibits: “SSW1” - “SSW7” Date: 27.04.21 Claim Number: IN THE HIGH COURT OF JUSTICE QUEEN’S BENCH DIVISION B E T W E E N (1) MULTIPLEX CONSTRUCTION EUROPE LIMITED (2) 30 GS NOMINEE 1 LIMITED (3) 30 GS NOMINEE 2 LIMITED Claimants and PERSONS UNKNOWN ENTERING IN OR REMAINING AT THE 30 GROSVENOR SQUARE CONSTRUCTION SITE WITHOUT THE CLAIMANTS’ PERMISSION Defendants ______________________________________ WITNESS STATEMENT OF STUART SHERBROOKE WORTLEY ________________________________________ I, STUART SHERBROOKE WORTLEY of One Wood Street, London, EC2V 7WS WILL SAY as follows:- 1. I am a partner of Eversheds Sutherland LLP, solicitors for the Claimants. 2. I make this witness statement in support of the Claimants’ application for an injunction to prevent the Defendants from trespassing on the 30 Grosvenor Square Construction Site (as defined in the Particulars of Claim). cam_1b\7357799\3 1 3. Where the facts referred to in this witness statement are within my own knowledge they are true; where the facts are not within my own knowledge, I believe them to be true and I have provided the source of my information. 4. I have read a copy of the witness statement of Martin Philip Wilshire. 5. In this witness statement, I provide the following evidence:- 5.1 in paragraphs 8-21, some recent videos and photographs of incidents of trespass uploaded to social media by urban explorers at construction sites in London; 5.2 in paragraphs 22-27, information concerning injunctions which my team has obtained -

Hot 100 2016 Winners in London’S Residential Market CBRE Residential 2–3 Hot 100 2016

CBRE Hot 100 2016 winners in London’s residential market CBRE Residential 2–3 Hot 100 2016 The year is drawing to a close and so our annual Hot 100 report is published. Find out where was hot in 2016. Contents Best performing locations 4–5 Most affordable boroughs 8–9 For nature lovers 10–11 For shopaholics 14–15 Boroughs for renters 16–17 Best school provision 20–21 Tallest towers 22–23 Highest level of development 24–25 Demographic trends 28–29 Best economic performance 30–31 CBRE Residential 4–5 Hot 100 2016 Top 10 Best performing locations Although prices remain highest in Central London, with homes in Kensington and Chelsea averaging £1.35 million, the other London boroughs continue to see the highest rate of growth. For the second year running Newham tops the table for price growth. This year prices in Newham increased by 24%; up from 16% last year. The areas characterised by significant regeneration, such as Croydon and Barking and Dagenham, are recording price rises of 18% and 17%, which is well above the average rate of 12%. Top Ten Price growth Top Ten Highest value 1 Newham 23.7% 1 Kensington and Chelsea £1,335,389 2 Havering 19.0% 2 City of Westminster £964,807 3 Waltham Forest 18.9% 3 City of London £863,829 4 Croydon 18.0% 4 Camden £797,901 5 Redbridge 18.0% 5 Ham. and Fulham £795,215 6 Bexley 17.2% 6 Richmond upon Thames £686,168 7 Barking and Dagenham 17.1% 7 Islington £676,178 8 Lewisham 16.7% 8 Wandsworth £624,212 9 Hillingdon 16.5% 9 Hackney £567,230 10 Sutton 16.5% 10 Haringey £545,025 360 Barking CBRE Residential 6–7 Hot 100 2016 CBRE Residential 8–9 Hot 100 2016 Top 10 Most affordable boroughs Using a simple ratio of house prices to earnings we can illustrate the most affordable boroughs. -

DC120/034 7.5 Committee

Committee: Date: Classification: Report Number: Agenda Item No: Development 17 March 2004 Unrestricted DC120/034 7.5 Committee Report of: Title: Town Planning Application Director of Customer Services Location: HERTSMERE HOUSE 2 HERTSMERE Case Officer: Simon Dunn-Lwin ROAD, LONDON, E14 4A (Columbus Tower) Ward: Millwall 1. SUMMARY 1.1 Registration Details Reference No: PA/03/00475 PA/03/00878 Date Received: 31/03/2003 Last Amended 31/03/2003 Date: 1.2 Application Details Existing Use: Office building occupied by Barclays and Morgan Stanley. Proposal: Demolition of existing building and erection of a 63 storey tower for office (B1), hotel and serviced apartments (C1 and sui generis), retail (A1/A2/A3) and leisure (D2) uses, with basement car parking and servicing. Applicant: SKMC & Farnham Properties Ltd Ownership: Barclays Bank PLC. Historic Building: N/A – adjacent to Grade II listed buildings on West India Quay, Grade I listed buildings known as Cannon Workshops, Grade I listed Dock Edge and Dock Wall. Conservation Area: Bordering West India Dock Conservation Area 2. RECOMMENDATION: 2.1 That the Development Committee grant planning permission, subject to the satisfactory completion of a legal agreement pursuant to Section 106 of the Town & Country Planning Act 1990 (and other appropriate powers) to include the matters outlined in Section 2.5 below; the conditions and informatives outlined in sections 2.6 and 2.7 below; and 5.1(22) relating to the OPDM Circular 1/2003. 2.2 That if the Committee resolve that planning permission be granted, that the application first be referred to the Mayor of London pursuant to the Town & Country Planning (Mayor of London) Order 2000, as an application for a new building exceeding 30 metres in height. -

The Isle of Dogs: Four Development Waves, Five Planning Models, Twelve

Progress in Planning 71 (2009) 87–151 www.elsevier.com/locate/pplann The Isle of Dogs: Four development waves, five planning models, twelve plans, thirty-five years, and a renaissance ... of sorts Matthew Carmona * The Bartlett School of Planning, UCL, 22 Gordon Street, London WC1H 0QB, United Kingdom Abstract The story of the redevelopment of the Isle of Dogs in London’s Docklands is one that has only partially been told. Most professional and academic interest in the area ceased following the property crash of the early 1990s, when the demise of Olympia & York, developers of Canary Wharf, seemed to bear out many contemporary critiques. Yet the market bounced back, and so did Canary Wharf, with increasingly profound impacts on the rest of the Island. This paper takes an explicitly historical approach using contemporaneous professional critiques and more reflective academic accounts of the planning and development of the Isle of Dogs to examine whether we can now conclude that an urban renaissance has taken place in this part of London. An extensive review of the literature is supplemented with analysis of physical change on the ground and by analysis of the range of relevant plans and policy documents that have been produced to guide development over the 35-year period since the regeneration began. The paper asks: What forms of planning have we seen on the Island; what role has design played in these; what outcomes have resulted from these processes; and, as a result, have we yet seen an urban renaissance? # 2009 Elsevier Ltd. All rights reserved. Keywords: Isle of Dogs; Urban design; Planning; Urban renaissance Contents 1. -

September 2009 1 COLUMBUS TOWER

COLUMBUS TOWER DEVELOPMENT, 2 HERTSMERE ROAD, LONDON, E14 4AB REVIEW OF DAYLIGHT, SUNLIGHT AND OVERSHADOWING EFFECTS Prepared on behalf of the Greater London Authority September 2009 1 Nathaniel Lichfield & Partners Ltd 14 Regent's Wharf All Saints Street London N1 9RL Offices also in T 020 7837 4477 Cardiff F 020 7837 2277 Manchester Newcastle upon Tyne [email protected] www.nlpplanning.com COLUMBUS TOWER DAYLIGHT AND SUNLIGHT REVIEW Executive Summary 1.1 This report reviews the Gordon Ingram Associates (GIA) Daylight and Sunlight Assessment and supplementary information submitted in support of the planning application for the Columbus Tower development at No. 2 Hertsmere Road, London E14 4AB (LBTH Ref. No. PA/08/02709). The review has been prepared on behalf of the Greater London Authority to assist the Mayor of London in determining the application. It considers the acceptability of the scope of the assessment, the accuracy of the daylight and sunlight modelling and results and the validity of the conclusions drawn. It also provides a commentary on the London Borough of Tower Hamlets determination of the application in terms of daylight and sunlight matters. 1.2 The review confirms that the scope of the assessment is appropriate in terms of the neighbouring properties and areas of amenity space assessed. The methodology and significance criteria employed in the assessment are also considered generally acceptable. 1.3 Comparison daylight and sunlight plots have been undertaken to verify the accuracy and precision of the data on which the assessment is based. The calculations corroborate the accuracy of GIA’s daylight and sunlight modelling and the validity of the assessment results. -

Bus Services in South Tower Hamlets and Surrounds

Bus Services In South Tower Hamlets And Surrounds TfL Surface Transport – Buses Directorate January 2014 1. BACKGROUND 1.1 This note seeks to understand what impact new development and rail enhancements (both planned and recently delivered) will have on the South Tower Hamlets bus network and how the network might change in response to the impact. South Tower Hamlets focuses mainly on Wapping and the Isle of Dogs but, inevitably, the results of the investigation extend beyond this to include most of Tower Hamlets and parts of the neighbouring boroughs. 1.2 The area has been the subject of previous reviews, particularly focusing on the Isle of Dogs. Reviews in 2003 and 2007 increased capacity on routes serving the island to accommodate the increased demand generated by new development. The 2007 review proposed the 135 which came into service in May 2008. Both reviews also proposed links to the east. Initially this was an extension of the D7 to Canning Town which was replaced by an extension of route 330 to the Isle of Dogs. Neither of these eastern extensions were implemented, in part due to developer contributions not being forthcoming. 1.3 In addition, routes in the study area have been continually monitored and adjusted to take account of changes in the area. Routes relevant to the study area have evolved as follows over the past 10 years: Route 135 introduced (May 2008) operating at up to 6 buses per hour (bph). Route 277 increased in frequency from 8 to 9 bph Monday – Saturday daytimes and from 4 to 6 bph on all evenings. -

Crossrail - Costs of Delay Prepared in Association With

Crossrail - Costs of Delay Prepared in association with February 2007 Crossrail - Costs of Delay Initial Report Project No: 125721 February 2007 Newcombe House 45 Notting Hill Gate, London, W11 3PB Telephone: 020 7309 7000 Fax: 020 7309 0906 Email : [email protected] Prepared by: Approved by: ____________________________________________ ____________________________________________ Paul Buchanan and Volterra Consulting PB Status: Final Issue no: 1 Date: February 2007 document1 (C) Copyright Colin Buchanan and Partners Limited. All rights reserved. This report has been prepared for the exclusive use of the commissioning party and unless otherwise agreed in writing by Colin Buchanan and Partners Limited, no other party may copy, reproduce, distribute, make use of, or rely on the contents of the report. No liability is accepted by Colin Buchanan and Partners Limited for any use of this report, other than for the purposes for which it was originally prepared and provided. Opinions and information provided in this report are on the basis of Colin Buchanan and Partners Limited using due skill, care and diligence in the preparation of the same and no explicit warranty is provided as to their accuracy. It should be noted and is expressly stated that no independent verification of any of the documents or information supplied to Colin Buchanan and Partners Limited has been made Crossrail - Costs of Delay Initial Report Contents Page 1. INTRODUCTION 1 1.1 Overview and Summary 1 2. COSTS OF DELAY 2 2.1 Introduction 2 2.2 Impact on scheme costs 2 2.3 Planning Blight 3 2.4 Transport Blight 6 2.5 Loss of Agglomeration Benefits 6 2.6 Loss of User Benefits 7 3. -

City Pride Public House, 15 Westferry Road, London, E14 8JH Existing

Committee: Date: Classification: Agenda Item Number: [Strategic] 13 th June 2013 Unrestricted Development Report of: Title: Town Planning Application Director of Development and Renewal Ref No: PA/12/03248 Case Officer: Ward: Millwall (February 2002 onwards) Beth Eite 1. APPLICATION DETAILS Location: City Pride Public House, 15 Westferry Road, London, E14 8JH Existing Use: Proposal: Erection of residential (Class C3) led mixed use 75 storey tower (239mAOD) comprising 822 residential units and 162 serviced apartments (Class C1), and associated amenity floors, roof terrace, basement car parking, cycle storage and plant, together with an amenity pavilion including retail (Class A1-A4) and open space. Drawing Nos/Documents: Drawings P-SL-C645-001 rev A, P-S-C645-001 rev B, P-LC-C645-001 rev A, P-L- C645-001 rev A, P-B2-C645-001 rev F, P-B1- C645-001 rev F, P-00-C645-001 rev G, P-01-C645-001 rev F, P-T0A-C645-001 rev D, P-T0B- C645-001 rev D, P-T1A- C645-001 rev B, B-T1B-C645-001 rev B, P-AM1-C645-001 rev E, P-T2-C645-001 rev E, P-T3-C645-001 rev E, P-AM2- C645-001 rev E, P-T4-C645-001 rev E, P-T5-C645-001 rev E, P-T6-C645-001 rev E, P-T7-C645-001 rev E, P-75-C645- 001 rev E, P-R-C645-001 rev E, P-LC-C645-001 rev B, P-L- C645-001 rev B, P_AM_C645_001 rev B, P_AM_C645_002 rev B, P_TY_D811_001 rev A, P-TY-D811-002 rev A E-JA-E-C645-001 rev A, E-JA-N-C645-001 rev A, E-JA-S- C645-001 rev A, E-JA-W-C645-001 rev A, E-01-C645-001 rev A, E-CE-N-645-001 rev A ,E-CE-S-645-001 rev A, E-CE- W-645-001 rev A, E-E-C645-001 rev C, E-N-C645-001 rev C, E-S-C645-001 -

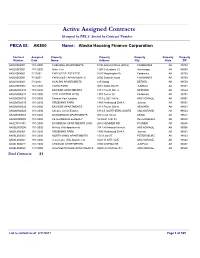

Active Contracts to Be Posted On

Active Assigned Contracts Grouped by PBCA Sorted by Contract Number PBCA ID:AK800 Name: Alaska Housing Finance Corporation Contract Assigned Property Property Property Property Property Number Date Name Address City State ZIP AK020002001 11/1/2000 CHENANA APARTMENTS 5190 Amherst Drive (office) FAIRBANKS AK 99709 AK020003001 11/1/2000 Glen, The 1200 Columbine Ct Anchorage AK 99508 AK020004001 7/1/2001 EXECUTIVE ESTATES 1620 Washington Dr Fairbanks AK 99709 AK020005001 7/1/2001 PARKWEST APARTMENTS 2006 Sandvik Road FAIRBANKS AK 99709 AK020006001 7/1/2001 AYALPIK APARTMENTS 105 Atsaq BETHEL AK 99559 AK020007002 12/1/2004 COHO PARK 3601 AMALGA ST JUNEAU AK 99801 AK02M000010 11/1/2000 BAYSIDE APARTMENTS 1011 Fourth Street SEWARD AK 99664 AK02M000011 11/1/2000 LITTLE DIPPER APTS 1910 Turner St Fairbanks AK 99701 AK02M000012 11/1/2000 Chester Park Estates 1019 E 20TH AVE ANCHORAGE AK 99501 AK02M000016 11/1/2000 GRUENING PARK 1800 Northwood Dr # A Juneau AK 99801 AK02M000022 11/1/2000 BAYSIDE APARTMENTS 1011 Fourth Street SEWARD AK 99664 AK02M000023 11/1/2000 Chester Creek Estates 5814 E NORTHERN LIGHTS ANCHORAGE AK 99504 AK02R000003 11/1/2000 WOODRIDGE APARTMENTS 903 Cook Street KENAI AK 99611 AK02R000004 11/1/2000 PETERSBURG ELDERLY 16 North 12th ST PETERSBURG AK 99833 AK02T851001 11/1/2000 DAYBREAK APARTMENTS (CMI) 2080 HEMMER RD PALMER AK 99645 AK06E000005 11/1/2000 McKay Villa Apartments 3741 Richmond Avenue ANCHORAGE AK 99508 AK06L000001 11/1/2000 GRUENING PARK 1800 Northwood Dr # A Juneau AK 99801 AK06L000003 11/1/2000 NORTH WIND APARTMENTS -

Growing Horizons 12M Price Target MYR 1.12 (+9%)

June 14, 2017 Eco World International (ECWI MK) HOLD Share Price MYR 1.03 Growing horizons 12m Price Target MYR 1.12 (+9%) Company Description Internationalizing the ‘ECOWORLD’ brandname A property developer with property projects in Eco World International (EWI) is the first and only Malaysia listed London and Australia. developer with pure overseas exposure in the UK and Australia property markets. Earnings growth would be strong in FY18-FY20 with the staggered contributions from its London and Sydney/Melbourne projects. We initiate coverage with a HOLD and MYR1.12 RNAV-TP (0.75x P/RNAV). Statistics Shariah status Yes Well-located projects to sustain earnings visibility 52w high/low (MYR) na/na 3m avg turnover (USDm) 2.3 All EWI’s projects in UK and Australia are well connected with close Free float (%) 57.7 proximity to existing/future train/tram lines. Since most of the projects Issued shares (m) 2,400 Real Estate are strategically located in new growth/mature areas catering for Market capitalisation MYR2.5B different market segments, pre-sales rates have been encouraging at 68- USD580M 83% since their launches in 2015 (except for Embassy Gardens Phase 2’s Major shareholders: 37%). Total pre-sales were MYR6.4b (87% GBP, 13% AUD) at end-Jan 2017, Gll Ewi Hk Ltd. 27.0% providing earnings visibility over the medium term. LIEW KEE SIN 10.3% Syabas Tropikal Sdn. Bhd. 3.3% Price Performance A new name in the hands of an experienced team EWI’s management is led by a team which includes former SP Setia (SPSB 1.30 105 Malaysia MK; BUY) directors and executives with considerable experiences in UK 1.25 100 and Australia property markets. -

London Hotel Development Monitor May 2005

LONDON HOTEL DEVELOPMENT MONITOR MAY 2005 London - New Hotel Room Supply 2004-2005 Introduction Since 1989, Visit London has been compiling data about new hotel developments across London. This information details new hotel openings, as well as potential developments which 1800 are likely to be constructed. This data can help identify gaps in London’s hotel market, and geographical areas where hotel coverage is poor. 1600 Limitations Information covers market facing hotels and excludes B&B’s, 1400 student accommodation and small hotels under 20 rooms. Purely speculative opportunities which are unlikely to proceed are also excluded. 1200 Recent Openings 1000 s Over the past 18 months, the London hotel market has witnessed a large amount of new built activity. Favourable oom macro economic conditions, combined with a sustained r f 800 recovery in visitor numbers to the capital, have helped o r support this growth. In addition, a number of large e b redevelopment schemes with significant hotel elements have m u 600 also come on stream. N All major hotel groups, with the exception of Hilton, have opened new London properties over the last 18 months. A 400 number of smaller hotel companies, such as: Baglioni, Firmdale and Urban Hotels have also entered the London market. 200 Another factor adding to this growth has been the renewed dash for growth by the major budget operators. Both Premier Travel Inn and Travelodge have committed themselves to 0 expanding their London hubs, with Travelodge recently Q1 Q2 Q3 Q4 Q1 Q2f Q3f Q4f stating that they need a minimum of 3,000 rooms in central London as soon as possible. -

Air Traffic Controller Workforce Plan 2019-2028

Air Traffic Controller WORKFORCE PLAN 2019–2028 his 2019 report is the FAA’s fourteenth annual update to Tthe controller workforce plan. The FAA issued the first comprehensive controller workforce plan in December 2004. It provides staffing ranges for all of the FAA’s air traffic control facilities and actual onboard controllers as of September 29, 2018. Section 221 of Public Law 108-176 (updated by Public Law 115-141) requires the FAA Administrator to transmit a report to the Senate Committee on Commerce, Science and Transportation and the House of Representatives Committee on Transportation and Infrastructure that describes the overall air traffic controller workforce plan. 2 . Air Traffic Controller Workforce Plan Contents 4 EXECUTIVE SUMMARY 38 Controller Losses Due to Promotions and Other Transfers 8 CHAPTER 1 | INTRODUCTION 39 Total Controller Losses 8 Staffing to Traffic 41 CHAPTER 5 | HIRING PLAN 10 Meeting the Challenge 42 Controller Hiring Profile 12 CHAPTER 2 | FACILITIES & SERVICES 43 Trainee-to-Total-Controller Percentage 12 Terminal and En Route Air Traffic Services 46 CHAPTER 6 | HIRING PROCESS 12 FAA Air Traffic Control Facilities 46 Controller Hiring Sources 14 CHAPTER 3 | STAFFING REQUIREMENTS 46 Recruitment 17 Staffing Ranges 49 CHAPTER 7 | TRAINING 21 Air Traffic Staffing Standards Overview 49 The Training Process 23 Tower Cab Overview 50 Designing and Delivering Effective Training 24 TRACON Overview 51 Infrastructure Investments 25 En Route Overview 51 Time to Certification 26 Summary 52 Investing for the Future 27 Air Traffic Controller Scheduling 53 CHAPTER 8 | FUNDING STATUS 27 Technological Advances 54 APPENDIX 31 CHAPTER 4 | LOSSES 54 2019 Facility Staffing Ranges 31 Controller Loss Summary 32 Actual Controller Retirements 32 Cumulative Retirement Eligibility 33 Controller Workforce Age Distribution 34 Controller Retirement Eligibility 35 Controller Retirement Pattern 36 Controller Losses Due to Retirements 37 Controller Losses Due to Resignations, Removals and Deaths 37 Developmental Attrition 37 Academy Attrition 2019-2028 .