Stronger Together the Go-Ahead Group Plc

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

English Counties

ENGLISH COUNTIES See also the Links section for additional web sites for many areas UPDATED 23/09/21 Please email any comments regarding this page to: [email protected] TRAVELINE SITES FOR ENGLAND GB National Traveline: www.traveline.info More-detailed local options: Traveline for Greater London: www.tfl.gov.uk Traveline for the North East: https://websites.durham.gov.uk/traveline/traveline- plan-your-journey.html Traveline for the South West: www.travelinesw.com Traveline for the West & East Midlands: www.travelinemidlands.co.uk Black enquiry line numbers indicate a full timetable service; red numbers imply the facility is only for general information, including requesting timetables. Please note that all details shown regarding timetables, maps or other publicity, refer only to PRINTED material and not to any other publications that a county or council might be showing on its web site. ENGLAND BEDFORDSHIRE BEDFORD Borough Council No publications Public Transport Team, Transport Operations Borough Hall, Cauldwell Street, Bedford MK42 9AP Tel: 01234 228337 Fax: 01234 228720 Email: [email protected] www.bedford.gov.uk/transport_and_streets/public_transport.aspx COUNTY ENQUIRY LINE: 01234 228337 (0800-1730 M-Th; 0800-1700 FO) PRINCIPAL OPERATORS & ENQUIRY LINES: Grant Palmer (01525 719719); Stagecoach East (01234 220030); Uno (01707 255764) CENTRAL BEDFORDSHIRE Council No publications Public Transport, Priory House, Monks Walk Chicksands, Shefford SG17 5TQ Tel: 0300 3008078 Fax: 01234 228720 Email: [email protected] -

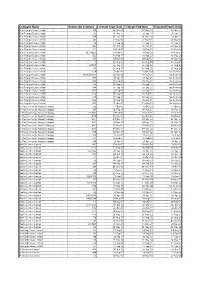

Operators Route Contracts

Company Name Routes On Contract Contract Start Date Contract End Date Extended Expiry Date Blue Triangle Buses Limited 300 06-Mar-10 07-Dec-18 03-Mar-17 Blue Triangle Buses Limited 193 01-Oct-11 28-Sep-18 28-Sep-18 Blue Triangle Buses Limited 364 01-Nov-14 01-Nov-19 29-Oct-21 Blue Triangle Buses Limited 147 07-May-16 07-May-21 05-May-23 Blue Triangle Buses Limited 376 17-Sep-16 17-Sep-21 15-Sep-23 Blue Triangle Buses Limited 346 01-Oct-16 01-Oct-21 29-Sep-23 Blue Triangle Buses Limited EL3 18-Feb-17 18-Feb-22 16-Feb-24 Blue Triangle Buses Limited EL1/NEL1 18-Feb-17 18-Feb-22 16-Feb-24 Blue Triangle Buses Limited EL2 18-Feb-17 18-Feb-22 16-Feb-24 Blue Triangle Buses Limited 101 04-Mar-17 04-Mar-22 01-Mar-24 Blue Triangle Buses Limited 5 26-Aug-17 26-Aug-22 23-Aug-24 Blue Triangle Buses Limited 15/N15 26-Aug-17 26-Aug-22 23-Aug-24 Blue Triangle Buses Limited 115 26-Aug-17 26-Aug-22 23-Aug-24 Blue Triangle Buses Limited 674 17-Oct-15 16-Oct-20 See footnote Blue Triangle Buses Limited 649/650/651 02-Jan-16 01-Jan-21 See footnote Blue Triangle Buses Limited 687 30-Apr-16 30-Apr-21 See footnote Blue Triangle Buses Limited 608 03-Sep-16 03-Sep-21 See footnote Blue Triangle Buses Limited 646 03-Sep-16 03-Sep-21 See footnote Blue Triangle Buses Limited 648 03-Sep-16 03-Sep-21 See footnote Blue Triangle Buses Limited 652 03-Sep-16 03-Sep-21 See footnote Blue Triangle Buses Limited 656 03-Sep-16 03-Sep-21 See footnote Blue Triangle Buses Limited 679 03-Sep-16 03-Sep-21 See footnote Blue Triangle Buses Limited 686 03-Sep-16 03-Sep-21 See footnote -

The Go-Ahead Group Plc Annual Report and Accounts 2019 1 Stable Cash Generative

Annual Report and Accounts for the year ended 29 June 2019 Taking care of every journey Taking care of every journey Regional bus Regional bus market share (%) We run fully owned commercial bus businesses through our eight bus operations in the UK. Our 8,550 people and 3,055 buses provide Stagecoach: 26% excellent services for our customers in towns and cities on the south FirstGroup: 21% coast of England, in north east England, East Yorkshire and East Anglia Arriva: 14% as well as in vibrant cities like Brighton, Oxford and Manchester. Go-Ahead’s bus customers are the most satisfied in the UK; recently Go-Ahead: 11% achieving our highest customer satisfaction score of 92%. One of our National Express: 7% key strengths in this market is our devolved operating model through Others: 21% which our experienced management teams deliver customer focused strategies in their local areas. We are proud of the role we play in improving the health and wellbeing of our communities through reducing carbon 2621+14+11+7+21L emissions with cleaner buses and taking cars off the road. London & International bus London bus market share (%) In London, we operate tendered bus contracts for Transport for London (TfL), running around 157 routes out of 16 depots. TfL specify the routes Go-Ahead: 23% and service frequency with the Mayor of London setting fares. Contracts Metroline: 18% are tendered for five years with a possible two year extension, based on Arriva: 18% performance against punctuality targets. In addition to earning revenue Stagecoach: 13% for the mileage we operate, we have the opportunity to earn Quality Incentive Contract bonuses if we meet these targets. -

Firstgroup Plc Annual Report and Accounts 2015 Contents

FirstGroup plc Annual Report and Accounts 2015 Contents Strategic report Summary of the year and financial highlights 02 Chairman’s statement 04 Group overview 06 Chief Executive’s strategic review 08 The world we live in 10 Business model 12 Strategic objectives 14 Key performance indicators 16 Business review 20 Corporate responsibility 40 Principal risks and uncertainties 44 Operating and financial review 50 Governance Board of Directors 56 Corporate governance report 58 Directors’ remuneration report 76 Other statutory information 101 Financial statements Consolidated income statement 106 Consolidated statement of comprehensive income 107 Consolidated balance sheet 108 Consolidated statement of changes in equity 109 Consolidated cash flow statement 110 Notes to the consolidated financial statements 111 Independent auditor’s report 160 Group financial summary 164 Company balance sheet 165 Notes to the Company financial statements 166 Shareholder information 174 Financial calendar 175 Glossary 176 FirstGroup plc is the leading transport operator in the UK and North America. With approximately £6 billion in revenues and around 110,000 employees, we transported around 2.4 billion passengers last year. In this Annual Report for the year to 31 March 2015 we review our performance and plans in line with our strategic objectives, focusing on the progress we have made with our multi-year transformation programme, which will deliver sustainable improvements in shareholder value. FirstGroup Annual Report and Accounts 2015 01 Summary of the year and -

Focused on Partnership About Us

Go East Anglia Sustainability Report 2016 Focused on partnership About us Go East Anglia encompasses Anglianbus, Chambers, Hedingham and Konectbus. Some 8 million passenger journeys are made each year on its services and over 370 people are employed. The forming of the branding name Go East Anglia was designed in 2015 to bring together the separate business in terms of identifying opportunities to work collectively across the geography and introduce the idea of sharing best practice with being part of a wider group. Our network covers Norfolk, Suffolk and Essex providing essential links to local towns and hospitals and places of education. Places served include Norwich, Great Yarmouth, Lowestoft, Bury St Edmunds, Sudbury, Braintree, Colchester and Clacton. Where we operate Norfolk, Suffolk and Essex. Norwich Swaffham Great Yarmouth Lowestoft Bury St Edmunds Sudbury Colchester Braintree Clacton-on-Sea We’re part of The Group In this report 2 Managing Director’s message 6 Society 4 Our approach 8 Customers 5 Our stakeholders 10 Our people 12 Finance Highlights – Launch of new Norwich Park & Ride network 9% 8,018,153 increase in passengers passenger journeys – Norwich Park & Ride m-ticket app journeys goes live – Buses with USB charging points enter service – Introduction of 5S in the workplace – Shortlisted for UKBA National Bus 89% 46% average customer increase in buses Driver of the Year satisfaction score fitted with CCTV Website: Twitter: Facebook: www.anglianbus.co.uk anglianbus anglianbus www.chambersbus.co.uk chambersbus chambersbus -

Go East Anglia

Go East Anglia - Chambers, Hedingham, Konect Bus (PF0002189) Konect Bus Limited 5-7 John Goshawk Road, Rashes Green Industrial Estate, Dereham, Norfolk, NR19 1SY Part of the Go-Ahead Group PLC. Depots: Clacton-on-Sea Stephenson Road, Gorse Lane Industrial Estate, Clacton-on-Sea, Essex, CO15 4XA Colchester Wethersfield Road, Sible Hedingham, Halstead, Colchester, Essex, CO9 3LB Dereham 7 John Goshawk Road, Rashes Green Industrial Estate, Dereham, Norfolk, NR19 1SY Sudbury Windham Road, Meekings Road, Chilton Industrial Estate, Sudbury, Suffolk, CO10 6XE Outstations: Brunel Road 14 Brunel Road, Gorse Lane Industrial Estate, Clacton-on-Sea, Essex, CO15 4LU Kelvedon 215-217 High Street, Kelvedon, Colchester, Essex, CO5 9JT Rackheath 36R Ramirez Road, Rackheath Industrial Estate, Norwich, Norfolk, NR13 6LR Chassis Type: Mercedes-Benz 1836RL Body Type: Mercedes-Benz Touro Fleet No: Reg No: Layout: Year: Depot: Livery: Notes: 1 BX55FYH C49FT 2006 Colchester Chambers 2 BX55FYJ C49FT 2006 Colchester Chambers Chassis Type: Alexander-Dennis Enviro 200MMC Body Type: Alexander-Dennis Enviro 200MMC Fleet No: Reg No: Layout: Year: Depot: Livery: Notes: 200 YX69NPE B42F 2019 Dereham park & ride Norwich 201 YX69NPF B42F 2019 Dereham park & ride Norwich 202 YX69NPG B42F 2019 Dereham park & ride Norwich Chassis Type: Dennis Dart SLF Body Type: Plaxton Pointer 2 Fleet No: Reg No: Layout: Year: Depot: Livery: Notes: 253 EU04BVF B37F 2004 Clacton-on-Sea Hedingham BLT, 2012 Previous Owners: BLT, 2012: Blue Triangle, 2012 254 - 260 Chassis Type: Alexander-Dennis Dart SLF Body Type: Plaxton Pointer 2 Fleet No: Reg No: Layout: Year: Depot: Livery: Notes: 254 EU05AUR B37F 2005 Clacton-on-Sea Hedingham 255 EU05AUT B37F 2005 Clacton-on-Sea Hedingham 256 EU55BWC B37F 2005 Clacton-on-Sea Hedingham 257 EU56FLM B37F 2006 Clacton-on-Sea Hedingham 258 EU56FLN B37F 2006 Clacton-on-Sea Hedingham 259 EU56FLP B37F 2006 Colchester Hedingham 260 EU56FLR B37F 2006 Clacton-on-Sea Hedingham Unofficial fleet list compiled by www.ukbuses.co.uk - last updated Friday, 20 August 2021. -

Anticipated Acquisition by London and South Eastern Railway, a Wholly Owned Subsidiary of Govia Limited, of the Integrated Kent Rail Franchise

Anticipated acquisition by London and South Eastern Railway, a wholly owned subsidiary of Govia Limited, of the Integrated Kent Rail Franchise The OFT's decision on reference under section 33(1) given on 28 March 2006. Full text of decision published 4 April 2006. PARTIES 1. Govia Limited (Govia) is a rail franchise holding company. It was formed as a joint venture between The Go-Ahead Group Plc (Go-Ahead) and Keolis (UK) Limited (a subsidiary of Keolis SA), which have shareholdings in Govia of 65 per cent and 35 per cent respectively. Govia will acquire the Integrated Kent Rail Franchise through its wholly owned subsidiary, London and South Eastern Railway (LSER). 2. The Integrated Kent Rail Franchise (IKF) will include passenger rail services on the network currently operated by South Eastern Trains (SET), a subsidiary of the Strategic Rail Authority (SRA). IKF is a commuter network serving several areas around the South East of England, parts of Greater London and several London termini. IKF will also include new domestic high-speed services from London St Pancras, making use of the Channel Tunnel Rail Link. SET's turnover for the year ended 31 March 2005 was £443.3 million. TRANSACTION 3. Govia (through LSER) was named the preferred bidder for IKF on 30 November 2005. IKF is due to commence on 1 April 2006 and will run for six years, although the contract allows for an extension of two years if performance targets are met. Alternatively, in the event of a delay to the start of the new high speed services using the Channel Tunnel Rail Link, the franchise may be extended by two years. -

Tfl Corporate Archive Top 20 Records

LT000605/005 - Description of the New Administrative Offices of the Underground Group of Companies By the late 1920s, the Underground Electric Railways Companies of London Ltd was anxious to house all of its ‘head office’ staff in one new purpose-built office block on the site of the old Metropolitan District Railway offices above St James’s Park station. The plans developed by Adams, Holden and Pearson, the architects commissioned by the Group, were radical: • 55 Broadway would be the tallest office building in London; • there would be a cruciform design - in place of the customary hollow rectangle format – which would offer staff more natural daylight in wings projecting from a central core housing lifts, staircases and essential services; and • Contemporary artists would be invited to sculpt decorative features directly onto the stone facade. As detailed in this reprint of a 1929 brochure about the building, 55 Broadway was constructed between 1927 and 1929. 700 reinforced concrete piles sunk to an average depth of 40 feet below basement level support the building. Nineteen load-bearing steel girders span the railway, and special insulation was used to reduce vibration from the trains. Above ground, the building was constructed around a steel girder skeleton and faced with 78,000 cubic feet of high quality Portland stone. The building has a bold appearance, enhanced by progressive stepping back above the sixth, eighth and ninth floors – giving an uneven pyramid effect. The clock tower, 174 feet high, has a similar stepped back effect. Granite for the ground floor came from Norway whilst the Travertine marble used in the interior came from Italy. -

Cambridge University Library Map Department Collection of Plans of Towns in England, Wales, Scotland, Isle of Man and Channel Islands Classmark = Maps.TPE

Cambridge University Library Map Department collection of plans of towns in England, Wales, Scotland, Isle of Man and Channel Islands Classmark = Maps.TPE. followed by town name and date, the ID is also useful * Indicates that the item is filed in the Outsize sequence Abbots Bromley Staffordshire ID Date Pub Code Notes/Part 1076 2001 Abbots Bromley Parish Council Sm,G Abbots Langley Hertfordshire ID Date Pub Code Notes/Part 1693 1971 ? T Aberdeen ID Date Pub Code Notes/Part 4811 1960 ca. Bartholomew - Town plan T, E 1260 1988 Aberdeen Tourist Board T 1222 1994 ca. Footprints - The Pint Sized Guide T [Aberdeen pub guide.] 461 1996 Bartholomew - Streetfinder Map 658 1997 Bartholomew - Streetfinder Atlas 664 1997 Bartholomew - Streetfinder Colour Ma 654 1998 Collins - Streetfinder Atlas 629 1998 ca. Collins - Streetfinder Map Westhill, Elrick 905 1999 Hallewell Sm,GB,Walk Aberdeen on foot 628 1999 ca. Nicolson Westhill, Elrick 1307 2001 ca. Nicolson - Street Guide T 1316 2003 Collins - Streetfinder T 02 February 2021 Page 1 of 296 3293 2004 Cityscape Maps T,S,Transport,P Transport,Shopping, Guide map and 3048 2005 Nicolson - Street Atlas 3820 2010 ca. Nicolson T & Bieldside, Bridge of Don, Bucksbur 4974 2016 Nicolson Digital - Street map, 1:14,000 T Aberdour ID Date Pub Code Notes/Part 2944 2005 ca. Fife Tourist Board T, G Aberfan ID Date Pub Code Notes/Part 393 1997 ca. Manderley Sm Treharris, Troedyrhiw, Merthyr Vale Aberfeldy ID Date Pub Code Notes/Part 1659 1956 Scottish Field Studies Association T Abergavenny Monmouthshire ID Date Pub Code Notes/Part 395 1996 ca. -

Master Document 'C'-25 11

Master Document C -25_11 25/11/04 3:31 pm Page 1 C Devon & Cornwall Winter/Spring Train Times 12 December 2004 to 10 June (Weekdays), 22 May (Weekends) 2005 Barnstaple Exeter Exeter St Davids Central Newquay Gunnislake St Ives Exmouth St St Erth Redruth Austell Liskeard Torquay Par Penzance Truro Plymouth Paignton HelstonFalmouth Eden Project Looe Table Route 1 Exeter to Penzance 2 Exmouth to Barnstaple 3 Exeter St Davids to Exeter Central 4 Plymouth to Gunnislake 5 Liskeard to Looe 6 Par to Newquay 7 St Austell to Eden Project Rail Bus Link 8Truro to Falmouth Docks 9 Redruth to Helston Rail Bus Link 10 Penzance & St Erth to St Ives Connecting People, Connecting Places Master Document C -25_11 25/11/04 3:31 pm Page 2 I Dear Customer, T in Welcome to the Winter 2004/Spring 2005 edition of our timetable 'C' covering rail r services in Devon and Cornwall. There is also a series of credit-card sized Train Service Summary Cards for our most popular routes, available from staffed stations or by calling the timetable distribution number 0870 900 2318. S Safety and security are naturally my first priority and this timetable devotes a whole B section to these. Please take the time to read these pages. If you have any concerns B while at stations or travelling, about your personal security, then please inform any of my staff or call the British Transport Police free on 0800 40 50 40. B B In your letters you tell me that punctuality, performance and cleanliness are the three B things you would most like to see improved. -

Notes of the London Regional Transport/Borough Liasion

Appendix to A15 NOTES OF THE LONDON REGIONAL TRANSPORT/BOROUGH LIAISON GROUP MEETING HELD AT THE TOWN HALL, HORNTON STREET, KENSINGTON, W8 7NX ON WEDNESDAY 11 TH OCTOBER 2000 AT 4:30 P.M. PRESENT: Councillor Mrs Frances Taylor (Chairman) Councillor Rima Horton Councillor Daniel Moylan (Chairman, Environmental Services Committee) Mr Mark Beauchamp (Better Government for Older People - RBKC) Mr Jim Brady (Business Manager - Centrewest) Mr Martyn Chaffer (Performance Delivery Support Manager - North ) Mr Daniel Collinge (Committee Services - RBKC) Mr Graham Cook (Manager Director - Travel London/Independent Way) Mr Martin Fisher (Operations Support Manager - Metroline) Ms Glynis Kelleher (Committee Services - RBKC) Mr David Knight (Service Quality Manager - London United) Mr Bill Mount (Group Leader Transportation - RBKC) Mr Tom Mansfield (Principal Transportation Officer - RBKC) Mr Richard Parry (London Underground Marketing Manager - Revenue) Mr David Richardson (Liaison and Special Projects Manager) Mr Mark Sexton (LUL Communication Manager for Closure of Routes) Mr Steve Travis (Director of Kensington & Chelsea Community Transport) Ms Gill Tynan (Road Manager - London General) 1. APOLOGIES FOR ABSENCE None 2. WELCOME AND INTRODUCTIONS 3. NOTES OF THE MEETING OF 5 th JULY 2000 The notes of the meeting held on 5 th July 2000 were confirmed as a correct record. 4. MATTERS ARISING FROM HIGHWAYS AND TRAFFIC COMMITTEE MEETING ON 12 TH SEPTEMBER 2000 Item 18 of the 12 th September Highways and Traffic Committee concerning infrastructure works was circulated. 2 The meeting noted that any matters arising from the Highways and Traffic Committee meeting would be covered during the course of the agenda. 5. BUS MATTERS Performance Indicators 5.1 Routes 10 and 52 The Chairman reported that these routes provided unreliable services to the public. -

Buses That We Don't Have Current Details For

Check List - buses that we don't have current details for The main lists on our website show the details of the many thousands of open top buses that currently exist throughout the world, and those that are listed as either scrapped or for scrap. However, there are a number of buses in our database that we don’t have current details for, that could still exist or have been scrapped. The buses listed on this page are those that we need to confirm the location and status of. These buses do not appear on any of our other lists, so if you're looking for a particular vehicle, it could be here. Please have a look at this page and if you can update any of it, even if only a small piece of information that helps to determine where a bus is now, then please contact us using the link button on the Front Page. The buses are divided into lists in Chassis manufacturer order. ? REG NO / LICENCE PLATE CHASSIS BODY STATUS/LAST KNOWN OWNER J2374 ? ? Last reported with JMT in 1960s, no further trace AEC Regent REG NO / LICENCE PLATE CHASSIS BODY STATUS/LAST KNOWN OWNER AUO 90 AEC Regent Unidentified Devon General AUO 91 AEC Regent Unidentified Devon General GW 6276 AEC Regent Brighton & Hove Acquired by Southern Vectis (903) from Brighton Hove and District in 1955. Sold, 1960, not traced further. GW 6277 AEC Regent Brighton & Hove Acquired by Southern Vectis (902) from Brighton Hove and District in 1955, never entered service, disposed of in 1957.