Central Pattana Plc Thai Airways International

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Central Pattana (CPN TB) Buy (Maintained)

Thailand Results Review 24 February 2020 Consumer Cyclical | Leisure & Entertainment Central Pattana (CPN TB) Buy (Maintained) Favourable 4Q19 Results; Keep BUY Target Price (Return): THB79.00 (32%) Price: THB60.00 Market Cap: USD8,516m Avg Daily Turnover (THB/USD) 379m/12.4m Keep BUY and DCF-based THB79.00 TP, 32% upside plus c.2% yield. Analyst We remain positive on Central Pattana’s positioning on mixed-use property development, which should secure its long-term outlook. 4Q/FY19 results Vatcharut Vacharawongsith were resilient – beat expectations – and we expect growth to continue this +662 2088 9736 year ie 6% for core profit and 20% for net profit from a big batch asset spin- [email protected] off to its REIT despite having no new malls. Strong 1Q20F bottomline may act as a near-term catalyst, while the stock looks undemanding (-1.5SD). 4Q19 results above expectations. 4Q19 net profit was THB3.61bn (+43% YoY, +28% QoQ). Excluding a THB203m one-time extra gain from the share sales of its subsidiary, core profit was THB3.4bn (+39%YoY, +21% QoQ). It was 15% higher than our forecast due to lower opex and tax expenses. Total revenue surge (20% YoY and 26% QoQ) was supported Share Performance (%) by rising occupancy rates at its key malls in Bangkok and strong residential YTD 1m 3m 6m 12m unit transfer – mainly the condominium project in the northern province of Absolute (3.6) (5.5) (5.9) (10.1) (22.6) Chiang Rai. The accounting re-classification of other income from related Relative 1.8 (0.4) 0.2 (1.4) (13.3) activities (ie marketing with its retail mall tenants) to its topline was applied, resulting in a GPM boost to 54%. -

Central Pattana Public Company Limited Major Events

Document Quick Link Central Pattana Public Company Limited Major Events Management’s Discussion and Analysis (MD&A) Performance Consolidated Financial Results: 1Q18 Business Plan Executive Summary In 1Q18, the Thai economy continues to expand, primarily driven by a number of supporting factors, namely 1) growth in exports with a record high in March 2018. 2) Growth in the tourism sector characterized by an increase in foreign inbound tourists, especially from China due to more available direct flights to Thailand and Europe due to the Easter holidays at the end of the period. 3) Gradual expansion of private consumption as consumer confidence continues to improve and 4) Other supporting factors, namely public and private investments and proposed stimulus schemes, such as increase in minimum wages, local SME projects and agricultural business reform, to support the low-income group. Overall, the Thai economy is on course for a steady year of growth, according to the Bank of Thailand, with its GDP growth in 2018 at 4.1%, a slight increment from that of 2017 at 3.9%. Growth in both revenue The performance of Central Pattana Public Company Limited (“The Company” or and net profit “CPN”) in 1Q18 shows a net profit of THB 2,822 mn, an increase of 1.7% from the demonstrates the same period in the previous year (YoY), whilst total revenues stood at THB 8,223 effectiveness of retail mn, an increase of 6.5% YoY. The result demonstrates the growth resiliency of properties and cost CPN’s operating results despite the impact on its revenue from rent and services management from the major renovation at CentralWorld, the transfer of CentralFestival Pattaya Beach to CPN Retail Growth Leasehold REIT (“CPNREIT”) in December 2017, and the increase in utility cost due to the increase in electricity Ft rate since May 2017. -

Central Pattana Plc. Property Development and Investment

Central Pattana Plc. Property Development and Investment CentralPlaza Nakhon Si Thammarat Corporate Presentation: 1Q16 Performance Review Contents ► Our Company ► Growth ► Financing ► Looking ahead ► Appendices 2 Our company CPN at a Glance Flagship business of the Central Group (Chirathivat Family) 29 1.6 mn sqm 93% 21% 15% Shopping Malls NLA Occ. Rate Market Share 5-yr top line growth Malls Other related business Residential Commercial Hotel 15 New Projects (2016-2020): 12 domestic malls and 3 overseas malls (i-City and 2 new malls) 1 Residence 7 Office Buildings 2 Hotels 1 Central City Residence @ Bangna • Lardprao Renovation projects: 21 • Pinklao Tower A 2016: Project 2016-2020 • Pinklao Tower B 6 BNA, RM3, PTC, and PKT • Bangna • CentralWorld Tower centralcenter 2017-2020: 1 • Chaengwattana CMA, CTW, CWN, and RM2 Announced: 3 Condominiums • Rama9 New Retail format and paid attraction Target: 3 Condominiums/Yr 3 Growth 5-yr target: revenue growth of 15%CAGR Overall NLA to increase by 20% between 2015 and 2018F Retail NLA and occupancy rates SQMmn % 97 98 96 96 97 2.0 95 96 96 94 94 94 94 100 1.8 90 1.6 80 36 1.4 70 33 1.2 60 30 1.0 29 50 0.8 25 40 23 0.6 20 30 18 15 0.4 15 20 10 11 0.2 projects 10 - - Existing New Unannounced RS: Occupancy rate Source: Company estimate as at 31 March 2016. Retail space: Includes leasable area of CentralPlaza Rama 2, CentralPlaza Rama 3, CentralPlaza Pinklao, and CentralPlaza Chiangmai Airport, which were 4 partially transferred to CPNRF, but still under CPN’s management. -

Stock Comparison

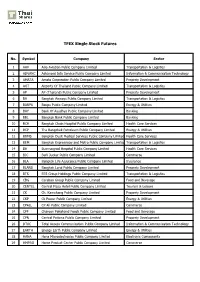

TFEX Single Stock Futures No. Symbol Company Sector 1 AAV Asia Aviation Public Company Limited Transportation & Logistics 2 ADVANC Advanced Info Service Public Company Limited Information & Communication Technology 3 AMATA Amata Corporation Public Company Limited Property Development 4 AOT Airports Of Thailand Public Company Limited Transportation & Logistics 5 AP AP (Thailand) Public Company Limited Property Development 6 BA Bangkok Airways Public Company Limited Transportation & Logistics 7 BANPU Banpu Public Company Limited Energy & Utilities 8 BAY Bank Of Ayudhya Public Company Limited Banking 9 BBL Bangkok Bank Public Company Limited Banking 10 BCH Bangkok Chain Hospital Public Company Limited Health Care Services 11 BCP The Bangchak Petroleum Public Company Limited Energy & Utilities 12 BDMS Bangkok Dusit Medical Services Public Company Limited Health Care Services 13 BEM Bangkok Expressway and Metro Public Company Limited Transportation & Logistics 14 BH Bumrungrad Hospital Public Company Limited Health Care Services 15 BJC Berli Jucker Public Company Limited Commerce 16 BLA Bangkok Life Assurance Public Company Limited Insurance 17 BLAND Bangkok Land Public Company Limited Property Development 18 BTS BTS Group Holdings Public Company Limited Transportation & Logistics 19 CBG Carabao Group Public Company Limited Food and Beverage 20 CENTEL Central Plaza Hotel Public Company Limited Tourism & Leisure 21 CK Ch. Karnchang Public Company Limited Property Development 22 CKP Ck Power Public Company Limited Energy & Utilities 23 CPALL CP All Public Company Limited Commerce 24 CPF Charoen Pokphand Foods Public Company Limited Food and Beverage 25 CPN Central Pattana Public Company Limited Property Development 26 DTAC Total Access Communication Public Company Limited Information & Communication Technology 27 EARTH Energy Earth Public Company Limited Energy & Utilities 28 HANA Hana Microelectronics Public Company Limited Electronic Components 29 HMPRO Home Product Center Public Company Limited Commerce TFEX Single Stock Futures No. -

CPN Retail Growth Property Fund “CPNRF”

CentralCentral PattanaPattana PlcPlc.. ““CPNCPN”” CPNCPN RetailRetail GrowthGrowth PropertyProperty FundFund ““CPNRFCPNRF”” Opportunity Day March 28, 2006 Content Economic Overview and Marketing Situation CPN Achievements and Plans Operation Review Financial Highlights CPN Retail Growth Property Fund (CPNRF) 2 Economic Overview & Marketing Situation Economic Overview Thai economy in Q405 grew by 4.7% Q-o-Q. However, for full year 2005 the economy grew by only 4.5%, a moderate decrease from 6.2% from the previous year. The decrease was attributed to the slowdown in household spending, lower overall production and a decrease in export. The contributing factors: - Higher oil price - Higher inflation - Higher interest rate - Reduction in consumer confidence - Other non-macroeconomic factors such as Tsunami, southern unrest, avian influenza, drought and flooding Note: Source from NESDB 4 Marketing Situation Retail Market Total supply of retail space in Bangkok rose by approximately 8% to 4.2 million sq.m. at the end of 2005, as compared with 3.9 million sq.m. at year-end 2004 and vacancy at year-end 2005 stood at approximately 5%. Retail rent in Bangkok was broadly stable in Q405, however, 2005 saw approximately 5% growth from 2004. New retail supply in 2006 is expected to be around 300,000 sq.m. Competition in Rajprasong is becoming increasingly intense, due to the growth in supply from the newly opened Paragon mall and the near completion of Centralworld. Office Market Total supply of office in Bangkok was stable in 2005 with an increase of less than 1% over 2004. Office space in 2005 stood at 7.2 million sq.m. -

Annual Report 2020 (56-1 One Report) Summary of Specified Items Per Form 56-1 One Report

Annual Report 2020 (56-1 One Report) Summary of Specified Items per Form 56-1 One Report Topics Page Part 1: Business and Operating Performance 1. Business Structure and Operating Performance 1.1 Business Policy and Business Overview 17, 33-41 1.2 Nature of Business 42-67 1.3 Investment Structure 68-85 1.4 Authorized Share Capital and Paid-up Share Capital 86 1.5 Other Securities (Debenture) 86-87 1.6 Dividend Policy 87 2. Risk Management 2.1 Risk Policy and Risk Management Plan 88 2.2 Risk Factors 88-92 3. Sustainable Development 3.1 Materiality Issue and Strategy 94-100 3.2 Sustainable Management for Stakeholder in Business Value Chain 101-135 3.3 Sustainable Management for Environment 143-159 3.4 Sustainable Management for Society 136-142 4. Management Discussion and Analysis 4.1 Analysis at Business and Financial Performance 161-170 4.2 Significant Factors that may Impact Future Business and Financial Performance 171-172 4.3 Financial Highlights 172-180 5. General Information and Other Information 5.1 General Information and Reference Persons 182, 185 5.2 Other Information 183-184 5.3 Legal Dispute 186 5.4 Secondary Market N/A 5.5 Financial Institution for Debenture 185 Part 2: Corporate Governance 6. Corporate Governance Policy 6.1 General Policy and Corporate Governance Practice 188-189 6.2 Code of Business Ethics 188 6.3 Key Development of Policy and Corporate Governance in the Year 189-199 7. Corporate Governance Structure and Information of Board of Directors, Sub-committee, Management, Employees and Others 7.1 Corporate Governance Structure Chart 200-201 7.2 Board of Directors 202-206 7.3 Sub-committees 207-208 7.4 Management 209-213 7.5 Employees 119-131, 214 7.6 Other Information 214 8. -

Rental Rates Have Generally Been Stable Since 2H05 Due 0 4.0% 2003 2004 2005 9M 2006 to the Steady Supply of New Retail Leasable Area

CentralCentral PattanaPattana PlcPlc.. Property Development & Investment Analyst Briefing – 4Q06 and FY2006 13 March 2007 Important Notice The information contained in this presentation is for information purposes only and does not constitute an offer or invitation to sell or the solicitation of an offer or invitation to purchase or subscribe for share in Central Pattana Public Company Limited (“CPN” and shares in CPN, “shares”) in any jurisdiction nor should it or any part of it form the basis of, or be relied upon in any connection with, any contract or commitment whatsoever. This presentation may include information which is forward-looking in nature. Forward-looking information involve known and unknown risks, uncertainties and other factors which may impact on the actual outcomes, including economic conditions in the markets in which CPN operates and general achievement of CPN business forecasts, which will cause the actual results, performance or achievements of CPN to differ, perhaps materially, from the results, performance or achievements expressed or implied in this presentation. This presentation has been prepared by the CPN. The information in this presentation has not been independently verified. No representation, warranty, express or implied, is made as to, and no reliance should be placed on, the fairness, accuracy, completeness or correctness of the information and opinions in this presentation. None of the CPN or any of its agents or advisers, or any of their respective affiliates, advisers or representatives, shall have any liability (in negligence or otherwise) for any loss howsoever arising from any use of this presentation or its contents or otherwise arising in connection with this presentation. -

Centralplaza Udon Thani Was Acquired on 8 April 09

CentralCentral PattanaPattana Plc.Plc. Property Development & Investment Opportunity Day Presentation : 2Q 2009 The Stock Exchange of Thailand, 25th August 2009 1 Important Notice The information contained in this presentation is for information purposes only and does not constitute an offer or invitation to sell or the solicitation of an offer or invitation to purchase or subscribe for share in Central Pattana Public Company Limited (“CPN” and shares in CPN, “shares”) in any jurisdiction nor should it or any part of it form the basis of, or be relied upon in any connection with, any contract or commitment whatsoever. This presentation may include information which is forward-looking in nature. Forward-looking information involve known and unknown risks, uncertainties and other factors which may impact on the actual outcomes, including economic conditions in the markets in which CPN operates and general achievement of CPN business forecasts, which will cause the actual results, performance or achievements of CPN to differ, perhaps materially, from the results, performance or achievements expressed or implied in this presentation. This presentation has been prepared by the CPN. The information in this presentation has not been independently verified. No representation, warranty, express or implied, is made as to, and no reliance should be placed on, the fairness, accuracy, completeness or correctness of the information and opinions in this presentation. None of the CPN or any of its agents or advisers, or any of their respective affiliates, advisers or representatives, shall have any liability (in negligence or otherwise) for any loss howsoever arising from any use of this presentation or its contents or otherwise arising in connection with this presentation. -

Thai News Update: 27 March 2020

Thai News Update: 27 March 2020 1. Malls waive rental fees for outbreak Source: Bangkok Post (Link) Central Pattana Plc, the SET-listed retail developer under Central Group, on 26 March announced measures to help tenants at its closed malls Preecha Ekkunagul, CPN's president and chief executive, said the company is waiving rent for tenants at shuttered malls and offering discounts on rent of 10-50% for stores that remain open. Some 3,000 shops at 27 malls will benefit from the waiver CPN is also providing pickup and delivery zones at closed malls and preparing a business plan for the return of service once the crisis is over. 2. True triples bandwidth capacity as Internet, mobile usage see big leap due to Covid-19 Source: The Nation (Link) There has been a sharp spike in internet and mobile usage as more people are staying at home due to the Covid-19 threat, Jirachai Kunakorn, chief network operations officer at True Corporation Plc, said. “We detected increased usage in all of our channels, including fiber and broadband internet, cable TV and mobile phone,” he said. “In the past month, the internet bandwidth usage has increased 52 per cent while mobile data usage has increased 18.4 per cent.” To cope with the increase in demand, True Corp has increased its domestic and international bandwidth capacity by up to three times, Jirachai said. 3. Ministry creates war rooms to handle essential goods Source: Bangkok Post (Link) The Commerce Ministry has set up war rooms to supervise seven essential consumer goods and services sectors to curb any possible shortages and hoarding during the coronavirus outbreak. -

Central Pattana (CPN TB ) Share Price: Bt48.25 Target Price: Bt58.0 (+20%)

March 21, 2016 OUTPERFORM Central Pattana (CPN TB ) Share Price: Bt48.25 Target Price: Bt58.0 (+20%) Conquering Southeast Asia Company Update Company Earnings expected to jump 23%/17% in FY16/17F, strongest growth among SE Asia peers despite fragile economy Potential upside to earnings if CPN converts CPNRF into REIT, expected to be finalized by 2Q16 Reiterate OUTPERFORM and Bt58 TP based on DCF; attractive valuation at 22.4x FY16F PE vs 28.6x average over FY13-15 Most promising retail space developer in SE Asia CPN is primed for a rerating. It is expected to register the strongest earnings growth among SE Asia peers in FY16F (+23%) and FY17F (+17%) compared with 18% and 9% regional average, respectively. This would be driven by the opening of five shopping malls in FY15-16 Kittisorn PRUITIPAT, CFA, FRM that will expand total leasable area by 15%, 3-6% higher rents, and 662 - 659 7000 ext 5019 high occupancy rate of 95%. CPN has been registering positive [email protected] COMPANY RESEARCH | RESEARCH COMPANY earnings growth in the last seven consecutive years despite a shaky economy, suggesting limited downside to our forecasts. Synergies with Key Data Central Group, which owns leading retail and restaurant chains and 12-mth High/Low (Bt) 50.5 / 39.8 54% stake in CPN, would also ensure the success of future projects. Market capital (Btm/US$m) 218,790 / 6,277 3m avg Turnover (Btm/US$m) 251.7 / 7.2 Potential upside from converting CPNRF from a property fund into Free Float (%) 49.0 REIT Issue Shares (m shares) 4,488 The management is considering several options: (i) convert CPNRF Major shareholders: (27% stake) into a REIT, (ii) set up a new REIT, or (iii) raise capital at - CENTRAL HOLDING COMP 26.2 CPNRF to renovate existing properties to enhance yields. -

Central Pattana (CPN TB) Buy (Maintained)

Thailand Company Update 26 January 2021 Consumer Cyclical | Leisure & Entertainment Central Pattana (CPN TB) Buy (Maintained) Expansions On Track; Maintain BUY Target Price (Return): THB66.00 (24.5%) Price: THB53.00 Market Cap: USD7,904m Avg Daily Turnover (THB/USD) 699m/23.1m • BUY, as we roll over to FY21F’s THB66.00 TP from THB58.00, 25% Analyst upside, 1-2% yields. We like this stock, expecting solid 18-28% core profit growth in 2021-2022. The ongoing launch of new mall, residential, and Vatcharut Vacharawongsith mixed-use projects may strengthen the long-term outlook. Planned asset +66 2088 9736 sales and improving post-pandemic operations may be upcoming catalysts. [email protected] • Three out of Central Pattana’s 35 retail malls had 80% closures of leasable areas: Central Plaza Mahachai, Central Plaza Rayong, and Central i-City (Malaysia) – the rest saw limited temporary tenant closures (20%) and 50-60% drops in traffic. Yet, we are optimistic on the re-opening of certain activities (eg fitness centres, spas, beauty clinics, educational centres, etc) in Bangkok from 22 Jan, which may indicate more relaxing of Share Performance (%) pandemic controls in the near term. Assuming COVID-19’s resurgence here YTD 1m 3m 6m 12m is curbed in March, we expect CPN’s mall operations to recover and see Absolute 11.0 4.4 37.7 8.2 (15.5) less rental rate discounts from the current c.30% by 2Q21. Relative 7.4 3.4 14.0 (3.8) (11.2) • Mall investments to go on. CPN plans to open 14 retail malls with a total 52-wk Price low/high (THB) 33.25 – 63.00 capex of THB70bn over 2021-2025, adding >0.6m sq m NLAs (2020: 1.65m sq m). -

The Hilton Pattaya Beach Hotel”

CentralCentral PattanaPattana Plc.Plc. Property Development & Investment Corporate Presentation: 3Q 2009 Important Notice The information contained in this presentation is for information purposes only and does not constitute an offer or invitation to sell or the solicitation of an offer or invitation to purchase or subscribe for share in Central Pattana Public Company Limited (“CPN” and shares in CPN, “shares”) in any jurisdiction nor should it or any part of it form the basis of, or be relied upon in any connection with, any contract or commitment whatsoever. This presentation may include information which is forward-looking in nature. Forward-looking information involve known and unknown risks, uncertainties and other factors which may impact on the actual outcomes, including economic conditions in the markets in which CPN operates and general achievement of CPN business forecasts, which will cause the actual results, performance or achievements of CPN to differ, perhaps materially, from the results, performance or achievements expressed or implied in this presentation. This presentation has been prepared by the CPN. The information in this presentation has not been independently verified. No representation, warranty, express or implied, is made as to, and no reliance should be placed on, the fairness, accuracy, completeness or correctness of the information and opinions in this presentation. None of the CPN or any of its agents or advisers, or any of their respective affiliates, advisers or representatives, shall have any liability (in negligence or otherwise) for any loss howsoever arising from any use of this presentation or its contents or otherwise arising in connection with this presentation.