Executive Summary

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Cost of Doing Business in the Province of Iloilo 2017 1

COST OF DOING BUSINESS IN THE PROVINCE OF ILOILO 2017 Cost of Doing Business in the Province of Iloilo 2017 1 2 Cost of Doing Business in the Province of Iloilo 2017 F O R E W O R D The COST OF DOING BUSINESS is Iloilo Provincial Government’s initiative that provides pertinent information to investors, researchers, and development planners on business opportunities and investment requirements of different trade and business sectors in the Province This material features rates of utilities, such as water, power and communication rates, minimum wage rates, government regulations and licenses, taxes on businesses, transportation and freight rates, directories of hotels or pension houses, and financial institutions. With this publication, we hope that investors and development planners as well as other interested individuals and groups will be able to come up with appropriate investment approaches and development strategies for their respective undertakings and as a whole for a sustainable economic growth of the Province of Iloilo. Cost of Doing Business in the Province of Iloilo 2017 3 4 Cost of Doing Business in the Province of Iloilo 2017 TABLE OF CONTENTS Foreword I. Business and Investment Opportunities 7 II. Requirements in Starting a Business 19 III. Business Taxes and Licenses 25 IV. Minimum Daily Wage Rates 45 V. Real Property 47 VI. Utilities 57 A. Power Rates 58 B. Water Rates 58 C. Communication 59 1. Communication Facilities 59 2. Land Line Rates 59 3. Cellular Phone Rates 60 4. Advertising Rates 61 5. Postal Rates 66 6. Letter/Cargo Forwarders Freight Rates 68 VII. -

Iloilo Provincial Profile 2012

PROVINCE OF ILOILO 2012 Annual Provincial Profile TIUY Research and Statistics Section i Provincial Planning and Development Office PROVINCE OF ILOILO 2012 Annual Provincial Profile P R E F A C E The Annual Iloilo Provincial Profile is one of the endeavors of the Provincial Planning and Development Office. This publication provides a description of the geography, the population, and economy of the province and is designed to principally provide basic reference material as a backdrop for assessing future developments and is specifically intended to guide and provide data/information to development planners, policy makers, researchers, private individuals as well as potential investors. This publication is a compendium of secondary socio-economic indicators yearly collected and gathered from various National Government Agencies, Iloilo Provincial Government Offices and other private institutions. Emphasis is also given on providing data from a standard set of indicators which has been publish on past profiles. This is to ensure compatibility in the comparison and analysis of information found therewith. The data references contained herewith are in the form of tables, charts, graphs and maps based on the latest data gathered from different agencies. For more information, please contact the Research and Statistics Section, Provincial Planning & Development Office of the Province of Iloilo at 3rd Floor, Iloilo Provincial Capitol, and Iloilo City with telephone nos. (033) 335-1884 to 85, (033) 509-5091, (Fax) 335-8008 or e-mail us at [email protected] or [email protected]. You can also visit our website at www.iloilo.gov.ph. Research and Statistics Section ii Provincial Planning and Development Office PROVINCE OF ILOILO 2012 Annual Provincial Profile Republic of the Philippines Province of Iloilo Message of the Governor am proud to say that reform and change has become a reality in the Iloilo Provincial Government. -

INVITATION to BID Properties of PDIC and Various Closed Banks

THE PHILIPPINE STAR SUNDAY | OCTOBER 22, 2017 classifinder B INVITATION TO BID Properties of PDIC and various closed banks December 8, 2017 (Friday) Venue: Bangko Sentral ng Pilipinas, Cebu Regional Office, Cor. Osmena Blvd & P. del Rosario St., Cebu City Bids shall be accepted starting 9:00 A.M. until 2:00 P.M. (PDIC time/no extension) UNIT UNIT PROPERTY MINIMUM BID DISCLO- PROPERTY MINIMUM BID DISCLO- DESCRIPTION TITLE / TD NO. LOCATION AREA DESCRIPTION TITLE / TD NO. LOCATION AREA NO. (PhP) SURES NO. (PhP) SURES (SqM.) (SqM.) AKLAN Lot 1 Blk. 11, Sitio Vacant interior 1-0541- Vacant Malinawon (Dumdum 1-0585- TD No. 05-015- Lot 3084, Brgy. TCT No. T-79065 297 103,950.00 bkn2126 residential lot w/o 541 dkln926 000000003 residential lot Subd.), Poblacion, 000000051 000485 Mambog, Banga ROW District II, Toboso 327,300.00 Vacant interior Lot 2 Blk. 11, Sitio 1-0585- Lot 3082, Brgy. residential lot w/ TCT No. T-25112 550 akln926 1-0541- Vacant Malinawon (Dumdum 000000068 Mambog, Banga TCT No. T-79066 299 74,750.00 bkn2126 ROW 000000004 residential lot Subd.), Poblacion, Lot 19-B, Block 10, District II, Toboso 1-0585- Interior residential TCT No. T- 23651 Capitol Subdivision, 309 247,200.00 akln26 Lot 4 Blk. 7, Sitio 000000065 lot w/ ROW 1-0525- Vacant Malinawon (Dumdum Brgy. Estancia, Kalibo TCT No. T-79949 298 89,400.00 bkn2126 1-0585- Vacant residential Lot 4839-D, Brgy. 000000002 residential lot Subd.), Poblacion, TCT No. T- 13726 936 280,800.00 bkl26 000000062 lot Pooc, Kalibo District II, Toboso Vacant interior 1-0579- Lot 8-A, Brgy. -

The Preparatory Study for Sector Loan on Disaster Risk Management in the Republic of the Philippines

DEPARTMENT OF PUBLIC WORKS AND HIGHWAYS THE REPUBLIC OF THE PHILIPPINES THE PREPARATORY STUDY FOR SECTOR LOAN ON DISASTER RISK MANAGEMENT IN THE REPUBLIC OF THE PHILIPPINES FINAL REPORT PART II-B FEASIBILITY STUDY ON ILOG-HILABANGAN RIVER BASIN (KABANKALAN AND ILOG) JANUARY 2010 JAPAN INTERNATIONAL COOPERATION AGENCY CTI ENGINEERING INTERNATIONAL CO., LTD. in association with NIPPON KOEI CO., LTD GED JR 10-012 DEPARTMENT OF PUBLIC WORKS AND HIGHWAYS THE REPUBLIC OF THE PHILIPPINES THE PREPARATORY STUDY FOR SECTOR LOAN ON DISASTER RISK MANAGEMENT IN THE REPUBLIC OF THE PHILIPPINES FINAL REPORT PART II-B FEASIBILITY STUDY ON ILOG-HILABANGAN RIVER BASIN (KABANKALAN AND ILOG) JANUARY 2010 JAPAN INTERNATIONAL COOPERATION AGENCY CTI ENGINEERING INTERNATIONAL CO., LTD. in association with NIPPON KOEI CO., LTD Exchange Rate used in the Report is: US$ 1.00 = PhP. 49.70 = JpY. 93.67 Jp¥ 1.00 = PhP. 0.5306 (as of 31st August 2009) LIST OF REPORTS Summary Part I : Main Report Part II-A : Feasibility Study on the Lower Cagayan River Flood Control Project for the Sector Loan Application Part II-B : Feasibility Study on the Ilog Hilabangan River Flood Control Project for the Sector Loan Application Part II-C : Feasibility Study on the Tagoloan River Flood Control Project for the Sector Loan Application Needs Assessment Study on Flood Disasters Caused by Typhoons No.16 (ONDOY) and No.17 (PEPENG) THE PREPARATORY STUDY FOR SECTOR LOAN ON DISASTER RISK MANAGEMENT IN THE REPUBLIC OF THE PHILIPPINES FINAL REPORT PART II-B: F/S ON ILOG-HILABANGAN RIVER BASIN (KABANKALAN AND ILOG) LOCATION MAP COMPOSITION OF THE REPORT TABLE OF CONTENTS ABBREVIATION (REFER TO MAIN REPORT (PART-I)) TABLE OF CONTENTS Page CHAPTER 1 INTRODUCTION.......................................................................... -

Cebu-Negros-Panay 230 Kv Backbone Project – Stage 3

Cebu-Negros-Panay 230 kV Backbone Project – Stage 3 Presentation to the 2019 Visayas 30 May 2019 Energy Investment Forum Outline 1. Project Components and Status 2. Other Transmission Projects Project Components and Status Cebu-Negros-Panay 230 kV Backbone Project PANAY BAROTAC VIEJO S/S CADIZ S/S CNP 230 kV Backbone Project Stage 3 CADIZ MANAPLA CITY E.B. MAGALONA S/S CITY ETC: Dec 2020 E.B. MAGALONA CITY VICTORIAS CITY Cebu-Negros transfer CNP 230 kV Backbone capacity: 180 MW + 800 MW Project Stage 1 ETC: Dec 2019 Negros-Panay transfer NEGROS capacity: 2019: 90 MW + 240 MW CEBU 2020: 90 MW + 400 MW BACOLOD S/S CALATRAVA S/S CALATRAVA CTS CNP 230 kV Backbone Project Stage 2 (Cebu 230 kV Substation) SAN CARLOS SWS ETC: Dec 2020 CEBU S/S TALAVERA SWS MAGDUGO S/S Project Components and Status Cebu-Negros-Panay 230 kV Backbone Project – Stage 3 PANAY BAROTAC VIEJO S/S (3x300 MVA) CADIZ MANAPLA CITY CITY E.B. MAGALONA CITY VICTORIAS CITY NEGROS CEBU CALATRAVA CTS TALAVERA–CALATRAVA S/C, 29 km SAN CARLOS SWS (2x400 MW) . Sites of the Barotac Viejo and Magdugo S/S are workable. CEBU S/S . Manufacturing of the Talavera– TALAVERA SWS MAGDUGO S/S Calatrava S/C is almost finished. (3x300 MVA) Project Components and Status Cebu-Negros-Panay 230 kV Backbone Project – Stage 3 PANAY CADIZ S/S E.B. MAGALONA-CADIZ (2x150 MVA) 230 kV T/L, 45 km CADIZ MANAPLA CITY CITY CADIZ-CALATRAVA 230 E.B. MAGALONA CITY VICTORIAS CITY kV T/L, 80 km NEGROS BACOLOD S/S (2x300 MVA) CEBU CALATRAVA S/S (2x100 MVA) CALATRAVA CTS . -

RAPID ASSESSMENT for MARKET REPORT (Panay Island, Philippines, Typhoon Haiyan November 2013)

RAPID ASSESSMENT FOR MARKET REPORT (Panay Island, Philippines, Typhoon Haiyan November 2013) Report Author: Ma. Rowena D. Balino Position/ Job Title: DME Team Leader/ RAM Focal Person RAM team members and positions: Christopher Leones, Monitoring & Evaluation Specialist Visminda D. Cabasan, DME Specialist Report date: 29 November 2013 Agency World Vision Section 1: Shock and needs analysis summary Type(s) of shock: Typhoon Haiyan/Yolanda Date(s) of shock(s): November 8, 2013 Date of RAM assessment: November 23-27, 2013 Affected areas assessed: Panay Island: Iloilo, Capiz, Aklan, Antique Areas covered by World Vision Total population in affected area: 315,237 households or 2,309,292 total population (Number of households and people) Affected population within affected area: 299,387 households or 1,453,325 total population 28,167 World Vision registered families or 140,835 population (Number of households and people) Average Household size: 5 (National Statistics Coordination Board) (Source of information) Location of affected population: Some are internally displaced, others have returned to their homes in the provinces of Iloilo, Capiz, Aklan, Antique (IDP/ stationary in homes etc…) Markets assessed: Iloilo: Iloilo City, Estancia, Barotac Viejo Capiz: Roxas City, Aklan: Batan, Kalibo, Altavas Antique: Bugasong, Laua-an, Barbasa (Areas selected are within World Vision covered areas, based on Purposive Sampling) Number of traders (wholesalers and retailers) 4 Regional Wholesalers (Iloilo City) and market representatives included in 23 Wholesalers -

Point to Point Pick Up/Drop Off Rates Kalibo to Any

POINT TO POINT PICK UP/DROP OFF RATES KALIBO TO ANY POINT OF PANAY (POINT TO POINT) RATE ORIGIN DESTINATION (VISE VERSA) KILOMETERS AUV/VAN CAR Kalibo Ajuy 4,200.00 3,900.00 Kalibo Alimodian 4,100.00 3,800.00 Kalibo Anilao 4,000.00 3,700.00 Kalibo Badiangan 3,900.00 3,600.00 Kalibo Balasan 3,800.00 3,500.00 Kalibo Banate 3,800.00 3,500.00 Kalibo Barotac Nuevo 3,900.00 3,600.00 Kalibo Barotac Viejo 3,800.00 3,500.00 Kalibo Batad 3,900.00 3,600.00 Kalibo Bingawan 3,100.00 2,900.00 Kalibo Cabatuan 3,900.00 3,600.00 Kalibo Calinog 3,200.00 3,000.00 Kalibo Carles 4,200.00 3,900.00 Kalibo Concepcion 4,200.00 3,900.00 Kalibo Dingle 3,400.00 3,100.00 Kalibo Duenas 3,300.00 3,000.00 Kalibo Dumangas 3,800.00 3,500.00 Kalibo Estancia 4,000.00 3,700.00 Kalibo Guimbal 4,300.00 4,000.00 Kalibo Igbaras 4,600.00 4,300.00 Kalibo Janiuay 3,600.00 3,300.00 Kalibo Lambunao 3,500.00 3,200.00 Kalibo Leganes 3,700.00 3,500.00 Kalibo Lemery 3,700.00 3,400.00 Kalibo Leon 4,300.00 4,000.00 Kalibo Maasin 3,900.00 3,600.00 Kalibo Miagao 4,600.00 4,300.00 Kalibo Mina 3,700.00 3,400.00 Kalibo New Lucena 3,800.00 3,500.00 Kalibo Oton 4,300.00 4,000.00 Kalibo Pavia 3,700.00 3,400.00 Kalibo Pototan 3,700.00 3,400.00 Kalibo San Dionisio 4,200.00 3,900.00 Kalibo San Enrique 3,400.00 3,100.00 Kalibo San Joaquin 4,700.00 4,400.00 Kalibo San Miguel 4,200.00 3,900.00 Kalibo San Rafael 3,500.00 3,200.00 Kalibo Santa Barbara 3,700.00 3,400.00 Kalibo Sara 4,100.00 3,800.00 Kalibo Tigbauan 4,300.00 4,000.00 Kalibo Tubungan 4,500.00 4,200.00 Kalibo Zarraga 3,700.00 3,400.00 Kalibo -

2021–2029 Iloilo City Comprehensive Land Use Plan (CLUP) Volume 1 Preliminary Pages

2021–2029 Iloilo City Comprehensive Land Use Plan (CLUP) Volume 1 Preliminary Pages 3 City Planning and Development Office i 2021–2029 Iloilo City Comprehensive Land Use Plan (CLUP) Volume 1 Preliminary Pages Message from the Mayor Our beloved Iloilo City has progressively built on its glorious past to usher in a present, which is a source of pride and hope for our people, and an inspiring benchmark for our neighbors in Western Visayas, and beyond. Yet we are not a people who rest on our laurels. We aim higher. We move further. We scale greater heights. We level up. To level up Iloilo City, we begin with the end in mind. We need to envision a future where our city is livable, sustainable and resilient. We aim for a culturally vibrant and economically well-developed city where governance is a shared responsibility and where people are innovative and creative. We dream big, yet we stay realistic. We know that our collective journey as Ilonggos towards our envisioned future has to factor in developments in our external environment. Prudence likewise dictates that our resolve to level-up needs to consider our strengths and weaknesses as a local government unit and as a community. We need to assess our competencies and our resources, particularly our land and its current and future uses, so we are well-informed in determining the best development strategy to level up Iloilo City. I am, therefore, most pleased that we have already crafted the 2021-2029 Iloilo City Comprehensive Land Use Plan (CLUP), which is a product of a series of consultations with various sectors. -

Approved For

Ed Approved for Republic of the Philippines ENERGY REGULATORY COMMISSION San Miguel Avenue, Pasig City IN THE MATTER OF THE APPLICATION FOR THE APPROVAL OF THE CEBU- NEGROS-PANAY 230 KV BACKBONE PROJECT (STAGE 1), WITH PRAYER FOR THE ISSUANCE OF A PROVISIONAL AUTHORITY ERC CASE NO. 201 3-024 RC NATIONAL GRID CORPORATION OF THE PHILIPPINES (NGCP), 1)0 CKTED Applicant. Date: ,J4i,J..2fli4 x----------------------- x 'V — DECISION Before this Commission for resolution is the application filed on February 15, 2013 by the National Grid Corporation of the Philippines (NGCP) for approval of its Cebu-Negros-Panay 230 kV backbone project (Stage I), with prayer for provisional authority. Having found said application sufficient in form and in substance with the required fees having been paid, an Order and a Notice of Public Hearing, both dated March 11, 2613, were issued selling the case for jurisdictional hearing, expository presentation, pre-trial conference and evidentiary hearing on April 24, 2013. In the same Order, NGCP was directed to cause the publication of the Notice of Public Hearing, at its own expense, twice (2x) for two (2) successive weeks in. two (2) newspapers of general circulation in the Philippines, with the date of the last publication to be made not later than ten (10) days before the date of the scheduled initial hearing. It was also directed to inform the consumers, by any other means available and appropriate, of the filing of the instant application, its reasons therefor and of the scheduled hearing thereon. ERC Case No. 2013-024 RC DECISION/June 24, 2013 Pane 2 of 8 The Office of the Solicitor General (OSG), the Commission on Audit (COA) and the, Committees on Energy of both Houses of Congress were furnished with copies of the Order and Notice of Public Hearing and were requested to have their respective duly authorized representatives present at the initial hearing. -

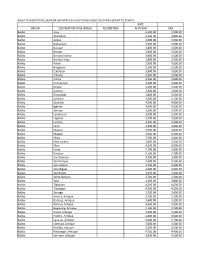

Bank of Commerce ROPA PRICELIST - VISAYAS As of 1ST QTR, 2019

Bank of Commerce ROPA PRICELIST - VISAYAS As of 1ST QTR, 2019 AREA PROPERTY DESCRIPTION PROPERTY LOCATION TCT / CCT NO. POSTED PRICE STATUS (SQM) REGION VI - WESTERN VISAYAS AKLAN Two-Storey Residential Bldg. L2-C-19-B, Vizcarra Subd., Brgy. Andagao, Kalibo, Aklan T-31851 322.00 For re-appraisal ** Residential Vacant Lot L F-2-D-3, Vizcarra Subd., Brgy. Andagao, Kalibo, Aklan T-28420 1,012.00 For re-appraisal Lot 2-A, Psd-06-000471, Brgy. Dumaguit, New Washington, Residential Vacant Lot 087-2014000215 9,651.00 For re-appraisal * Aklan Agricultural Lot Lot 611, Brgy Magugma, Libacao, Aklan T-17614 45,974.00 690,000.00 Residential Vacant Lot Lot 804-K-13, Brgy. Julita, Libacao, Aklan T-6233 11,506.25 For re-appraisal * Residential/ Commercial Lot Lot 11, New Washington, Aklan T-16238 254.00 For re-appraisal Residential/ Commercial Lot Lot 12, New Washington, Aklan T-16239 256.00 For re-appraisal CAPIZ Residential Lot with Improvement L247-B-1, Poblacion, Pontevedra, Capiz T-30625 5,839.00 For re-appraisal * Owner: AAOD Head Classification: Confidential Page 1 of 62 AREA PROPERTY DESCRIPTION PROPERTY LOCATION TCT / CCT NO. POSTED PRICE STATUS (SQM) Lot 2683-A, Brgy. Alayunana (formerly Batabat), Maayon Agricultural Lot T-16535 557,527.00 For re-appraisal (formerly Pontevedra), Capiz Agricultural Lot Lot 3-A, Brgy. Sinamongan, Pilar, Capiz T-11966 743,018.00 Agricultural Lot Lot 3-B, Brgy. Sinamongan, Pilar, Capiz T-11967 742,718.00 For re-appraisal * Agricultural Lot Lot 3-C, Brgy. Sinamongan, Pilar, Capiz T-11968 742,698.00 Agricultural Lot Lot 3-D, Brgy. -

Province, City, Municipality Total and Barangay Population AKLAN 535,725 ALTAVAS 23,919 Cabangila 1,705 Cabugao 1,708 Catmon

2010 Census of Population and Housing Aklan Total Population by Province, City, Municipality and Barangay: as of May 1, 2010 Province, City, Municipality Total and Barangay Population AKLAN 535,725 ALTAVAS 23,919 Cabangila 1,705 Cabugao 1,708 Catmon 1,504 Dalipdip 698 Ginictan 1,527 Linayasan 1,860 Lumaynay 1,585 Lupo 2,251 Man-up 2,360 Odiong 2,961 Poblacion 2,465 Quinasay-an 459 Talon 1,587 Tibiao 1,249 BALETE 27,197 Aranas 5,083 Arcangel 3,454 Calizo 3,773 Cortes 2,872 Feliciano 2,788 Fulgencio 3,230 Guanko 1,322 Morales 2,619 Oquendo 1,226 Poblacion 830 BANGA 38,063 Agbanawan 1,458 Bacan 1,637 Badiangan 1,644 Cerrudo 1,237 Cupang 736 National Statistics Office 1 2010 Census of Population and Housing Aklan Total Population by Province, City, Municipality and Barangay: as of May 1, 2010 Province, City, Municipality Total and Barangay Population Daguitan 477 Daja Norte 1,563 Daja Sur 602 Dingle 723 Jumarap 1,744 Lapnag 594 Libas 1,662 Linabuan Sur 3,455 Mambog 1,596 Mangan 1,632 Muguing 695 Pagsanghan 1,735 Palale 599 Poblacion 2,469 Polo 1,240 Polocate 1,638 San Isidro 305 Sibalew 940 Sigcay 974 Taba-ao 1,196 Tabayon 1,454 Tinapuay 381 Torralba 1,550 Ugsod 1,426 Venturanza 701 BATAN 30,312 Ambolong 2,047 Angas 1,456 Bay-ang 2,096 Caiyang 832 Cabugao 1,948 Camaligan 2,616 Camanci 2,544 Ipil 504 Lalab 2,820 National Statistics Office 2 2010 Census of Population and Housing Aklan Total Population by Province, City, Municipality and Barangay: as of May 1, 2010 Province, City, Municipality Total and Barangay Population Lupit 1,593 Magpag-ong -

Legend Lantangan SCI Early Recovery & Livelihoods FAO Bancal Food Security and Agriculture Carles

Region VI (Western Visayas) : Food Security and Agriculture And Early Recovery & Livelihoods Clusters Ongoing Response Activities in ILOILO Province (a s of 23 May 2014) 123°0'0"E CARLES Concern Worldwide Carles Gabi Punta SCI Legend Lantangan SCI Early Recovery & Livelihoods FAO Bancal Food Security and Agriculture Carles Abong Organisations Acronyms Tabugon Cawayan NAA-NCCP ACT Alliance Binuluangan SOS Save Our Species Tarong TFB-Task Force Buliganay BALASAN Pantalan Tinigban Data Source: ACF Manlot OCHA, DSWD, GADM Barangcalan Gogo 01.75 3.5 7 San Roque Daculan Talingting Carles Km Poblacion Norte ¯ Bayuyan Tacbuyan Punta Batuanan philippines.humanitarianresponse.info Loguingot Bito-On Feedback: [email protected] Created 27 May 2014 Balasan Cano-An Pa-On BATAD Daan Banua Estancia Botongan Manipulon Tanza SCI Santa Ana ESTANCIA Bayas KAISA Fdt. Jolog NAA SCI Embarcadero SOS Salong TFB Batad Banban WVI Alinsolong Binon-An ACF Tanao SCI Madanlog Odiongan World Renew Capiz Tamangi Mandu-Awak Agdaliran Bagacay Boroñgon Cubay SAN DIONISIO Hacienda Conchita San Dionisio SCI Cudionan KAISA Fdt. Sua San Nicolas ACF Sara Tuble Tiabas FAO Capinang Dugman SCI Pase Santol Bondulan Siempreviva Malangabang Bacjawan Norte CONCEPCION CALINOG Lemery Bacjawan Sur ACF Igbon Concern Worldwide Poblacion One Meal World Renew Polopina Pantalan Navarro SCI Bingawan Lo-Ong Lanjagan FAO Niño SCI Taguhangin Rojas Plandico Nipa Concepcion Passi City Ajuy Pantalan Nabaye Bucana Bunglas AJUY Silagon San Rafael Bato Biasong Maliogliog ADRA Mangorocoro Calinog Concern Worldwide Bagongon KAISA Fdt. Tagubanhan Canabajan ADRA Pili FAO Punta Buri San Enrique Malayu-An Santo Rosario Barrido Culasi Luca Barotac Viejo Nasidman Duenas Banate Pedada Dingle Bay-Ang Badiangan Anilao.