Our Branches

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Province, City, Municipality Total and Barangay Population AURORA

2010 Census of Population and Housing Aurora Total Population by Province, City, Municipality and Barangay: as of May 1, 2010 Province, City, Municipality Total and Barangay Population AURORA 201,233 BALER (Capital) 36,010 Barangay I (Pob.) 717 Barangay II (Pob.) 374 Barangay III (Pob.) 434 Barangay IV (Pob.) 389 Barangay V (Pob.) 1,662 Buhangin 5,057 Calabuanan 3,221 Obligacion 1,135 Pingit 4,989 Reserva 4,064 Sabang 4,829 Suclayin 5,923 Zabali 3,216 CASIGURAN 23,865 Barangay 1 (Pob.) 799 Barangay 2 (Pob.) 665 Barangay 3 (Pob.) 257 Barangay 4 (Pob.) 302 Barangay 5 (Pob.) 432 Barangay 6 (Pob.) 310 Barangay 7 (Pob.) 278 Barangay 8 (Pob.) 601 Calabgan 496 Calangcuasan 1,099 Calantas 1,799 Culat 630 Dibet 971 Esperanza 458 Lual 1,482 Marikit 609 Tabas 1,007 Tinib 765 National Statistics Office 1 2010 Census of Population and Housing Aurora Total Population by Province, City, Municipality and Barangay: as of May 1, 2010 Province, City, Municipality Total and Barangay Population Bianuan 3,440 Cozo 1,618 Dibacong 2,374 Ditinagyan 587 Esteves 1,786 San Ildefonso 1,100 DILASAG 15,683 Diagyan 2,537 Dicabasan 677 Dilaguidi 1,015 Dimaseset 1,408 Diniog 2,331 Lawang 379 Maligaya (Pob.) 1,801 Manggitahan 1,760 Masagana (Pob.) 1,822 Ura 712 Esperanza 1,241 DINALUNGAN 10,988 Abuleg 1,190 Zone I (Pob.) 1,866 Zone II (Pob.) 1,653 Nipoo (Bulo) 896 Dibaraybay 1,283 Ditawini 686 Mapalad 812 Paleg 971 Simbahan 1,631 DINGALAN 23,554 Aplaya 1,619 Butas Na Bato 813 Cabog (Matawe) 3,090 Caragsacan 2,729 National Statistics Office 2 2010 Census of Population and -

Angeles City Is Located in the Figur E 1 Percent Distribution of Total Population, Northeastern Part of Pampanga

2000 CENSUS OF POPULATION AND HOUSING Report No. 2 Volume I Demographic and Housing Characteristics AAANNNGGGEEELLLEEESSS CCCIIITTTYYY NATIONAL STATISTICS OFFICE REPUBLIC OF THE PHILIPPINES HER EXCELLENCY PRESIDENT GLORIA MACAPAGAL-ARROYO NATIONAL STATISTICAL COORDINATION BOARD Honorable Romulo L. Neri Chairperson NATIONAL STATISTICS OFFICE Carmelita N. Ericta Administrator Paula Monina G. Collado Deputy Administrator Josie B. Perez Officer-In-Charge Household Statistics Department ISSN 0117-1453 FOREWORD One main factor to consider in achieving development in a country, whether social or economic, is the population. The government makes plans and programs for the achievement of a better quality of life for the people. These programs include better health services, adequate nutrition, free education, housing for all, and social welfare for the needy. These programs can only be achieved, however, if there are sufficient and reliable data as bases for planning. The Census of Population and Housing (CPH) is one of the major activities undertaken by the National Statistics Office (NSO) every ten years. It takes an inventory of the total population of the country and a stock of the housing units, not to mention other demographic and housing characteristics that can provide the necessary data to planners. This report is the first of two parts of the provincial publication for the 2000 CPH that was conducted on May 1, 2000. Demographic data presented herein consist of population distribution according to age, sex, marital status, religious affiliation, disability, education, ethnicity, residence five years ago, household size, overseas workers, citizenship, literacy, place of school, language or dialect generally spoken, ever married women, number of children ever born, and age at first marriage. -

Mines and Geosciences Bureau Regional Office No

ANNEX-B (MPSA) Republic of the Philippines Department of Environment and Natural Resources MINES AND GEOSCIENCES BUREAU REGIONAL OFFICE NO. III MINING TENEMENTS STATISTICS REPORT FOR MONTH OF APRIL, 2020 MINERAL PRODUCTION AND SHARING AGREEMENT (MPSA) ANNEX-B %OWNERSHIP HOLDER OF MAJOR SEQ (Integer no. of PARCEL DATE_FILED DATE_APPROVED TENEMENT_NO TEN_TYPE (Name, Address, Contact Nos. And FILIPINO AND AREA (has.) BARANGAY MUNICIPALITY PROVINCE COMMODITY TENEMENT_NO) No. (mm/dd/yyyy) (mm/dd/yyyy) Authorized Representative FOREIGN PERSON A. Mining Tenement Applications 1. Under Process BALER GOLD MINIG CORP. Mario Diabelo, gold , copper, 1 *PMPSA-IV-154 APSA 100% Filipino 3442.0000 11/8/1994 San Luis Aurora R. Guillermo - President Diteki silver MULTICREST MINING CORP. gold , copper, 2 *PMPSA-IV-160 APSA 100% Filipino 1701.0000 11/28/1994 Ditike, Palayan San Luis Aurora Manuel Lagman - Vice President silver OMNI MINES DEV'T CORP. Alfredo gold , copper, 3 *PMPSA-IV-184 APSA 100% Filipino 648.0000 3/7/1995 San Luis Aurora San Miguel Jr. - President silver BALER CONSOLIDATED MINES , copper, gold, 4 *AMA-IVA-07 APSA INC. 100% Filipino 7857.0000 10/3/1995 San Luis Aurora silver, etc. Michael Bernardino - Director SAGITARIUS ALPHA REALTY CORPORATION 5 APSA000019III APSA Reynaldo P. Mendoza - President 106 100% Filipino 81.0000 7/4/1991 Tubo-tubo Sta. Cruz Zambales limestone, etc. Universal Re Bldg., Paseo De Roxas, Makati City BENGUET CORPORATION Address: 845 Arnaiz Avanue, 1223 Masinloc, 6 APSA000020III APSA 100% Filipino 2434.0000 7/5/1991 Zambales chromite, etc. Makati City Tel. Candelaria No. 812-1380/819-0174 BENGUET CORPORATION Address: 845 Arnaiz Avanue, 1223 7 APSA000021III APSA 100% Filipino 1572.0000 7/5/1991 Masinloc Zambales chromite, etc. -

Infrastructure Damage Analysis of the April 22, 2019 Pampanga, Philippines Earthquake

JSCE Journal of Disaster FactSheets, FS2020-E-0002, 2020 Infrastructure damage analysis of the April 22, 2019 Pampanga, Philippines earthquake Lessandro Estelito GARCIANO1, Carlos VILLARAZA2, Christopher P. TAMAYO3, Miriam TAMAYO4, Reynaldo FLORDELIZA5, Megan Angela QUIAEM6, and Joaquin Miguel RAMOS7 1Professor, Department of Civil Engineering, De La Salle University (2401 Taft Avenue, Malate, Manila 1004, Philippines) E-mail: [email protected] 2Past President, Association of Structural Engineers of the Philippines (112 Panay Avenue, Quezon City 1103, Philippines) E-mail: [email protected] 3Past President, Association of Structural Engineers of the Philippines (112 Panay Avenue, Quezon City 1103, Philippines) E-mail: [email protected] 4Past President, Association of Structural Engineers of the Philippines (112 Panay Avenue, Quezon City 1103, Philippines) E-mail: [email protected] 5Member, Association of Structural Engineers of the Philippines (112 Panay Avenue, Quezon City 1103, Philippines) E-mail: [email protected] 6Undergraduate Student, Department of Civil Engineering, De La Salle University (2401 Taft Avenue, Malate, Manila 1004, Philippines) E-mail: [email protected] 7Undergraduate Student, Department of Civil Engineering, De La Salle University (2401 Taft Avenue, Malate, Manila 1004, Philippines) E-mail: [email protected] Key Facts • Hazard Type: Earthquake • Date of Disaster: April 22, 2019 • Location of the survey: Porac, Pampanga, Philippines • Date of the field survey: April 24, 2019 • Survey tools: Laser meter, Drone • Key Findings 1) Various structural and non-structural damages within the Central Luzon Region were observed. The collapse of the Chuzon Supermarket in Porac, Pampanga, was the leading major aftermath of the earthquake. 2) Majority of structures suffered minimal structural damage, most damages were to non- structural components. -

DSWD DROMIC Report #17 on the Earthquake Incident in Castillejos, Zambales As of 04 May 2019, 4PM

DSWD DROMIC Report #17 on the Earthquake Incident in Castillejos, Zambales as of 04 May 2019, 4PM Situation Overview On April 22, 2019 at exactly 5:11 PM, a Magnitude 6.1 earthquake shook Castillejos, Zambales. The epicenter of the earthquake was located 15.02°N, 120.34°E - 018 km N 58° E of Castillejos (Zambales) with a depth focus of 10 km and with a Tectonic origin. Reported Intensity VI - San Marcelino, and Subic, Zambales; Floridablanca, Lubao, and Porac, Intensities Pampanga; Angeles City; Olongapo City; (22 April 2019, 11:01 Intensity V - Castillejos, and San Felipe, Zambales; Magalang, Mexico, and San Fernando, PM): Pampanga; Abucay, Balanga, and Mariveles, Bataan; Malolos, and Obando, Bulacan; Indang, Cavite; Lipa City; Makati City; Mandaluyong City; Manila City; Quezon City; Pasay City; San Juan City; Taguig City; Tarlac City; Valenzuela City; Intensity IV - Meycauayan, Plaridel, and San Jose Del Monte, Bulacan; San Rafael, Tarlac; Rosales and Villasis, Pangasinan; Itogon, and La Trinidad, Benguet; Kasibu, Nueva Vizcaya; Gabaldon, Nueva Ecija; San Mateo, Rizal; Bacoor, Imus, and Maragondon, Cavite; Nasugbu, Batangas; Antipolo City; Baguio City; Caloocan City; Las Piñas City; Marikina City; Pasig City; Tagaytay City; Intensity III - Marilao, Bulacan; Santo Domingo, and Talavera, Nueva Ecija; Maddela, Quirino; Dingalan, Aurora; Lucban, Quezon; Santa Cruz, Laguna; Carmona, Dasmariñas, General Trias, and Silang, Cavite; San Nicolas and Talisay, Batangas; Cabanatuan City; Calamba City; Gapan City; Muntinlupa City; Palayan City; Page -

Kapampangan Folk Music, Games, and Theater

2021-4192-AJHA – 18 APR 2021 1 Kapampangan Folk Music, Games, and Theater: 2 An Endangered Oral Traditions 3 4 The culture of the Kapampangan people in the province of Pampanga, 5 Philippines is so diverse that even its name Pampang is rooted on the word 6 which means shore or the loading and unloading point of all transactions 7 that are foreign, starting from the time of the early Chinese down to the 8 Spaniards and so on. Among these diversities are the oral traditions found 9 in the province which they learned true word of mouth. The researcher used 10 2 folk songs, 2 games, and 1 local theatre in the study: The Atin Ku Pung 11 Sing-Sing and Inyang Malati Ku folk songs which tell how the common 12 Kapampangan live, love, and laugh; The ancient structured poetic game 13 bulaklakan, which is usually performed during funeral wakes to mitigate the 14 pain experienced by the bereaved family, and the salikutan (hide and seek) 15 game where the starter needs to utter a chant before the game will start; 16 And lastly, the re-enactment of Joseph and pregnant Mary looking for 17 shelter held only during the night of Christmas using the native language 18 traversing in the streets of the village which they called layunan. This study 19 covered history, tradition, and ceremonies observed in Pampanga; its results 20 included interviews with 22 elder informants and 88 young respondents. The 21 main results were (1) the established oral traditions of the Kapampangans 22 clashed with westernized trends and modern society, it is pushing out slowly 23 by technology, globalisation, modernisation, mass movements, political, 24 economic and natural calamities; (2) the attitude of using and choosing 25 English and Tagalog as the language/s at home instead of the Kapampangan 26 significantly contributed to the weakening Kapampangan oral tradition; (3) 27 Kapampangan oral traditions are slowly dying because of lack of exposure 28 and familiarity to it by the young Kapampangans. -

Real Bacolor-Layout

www.hau.edu.ph/kcenter The Juan D. Nepomuceno Center for Kapampangan Studies HOLY ANGEL UNIVERSITY ANGELES CITY, PHILIPPINES 1 RECENTRECENT VISITORS MARCH & APRIL F. Sionil Jose Ophelia Dimalanta Mayor Ding Anunciacion, Bamban, Mayor Genaro Mendoza, Tarlac City Joey Lina Sylvia Ordoñez Mayor Carmelo Lazatin, Angeles Vice Mayor Bajun Lacap, Masantol Ely Narciso, Kuliat Foundation Ching Escaler Maribel Ongpin Gringo Honasan Crisostomo Garbo Museum Foundation of the Philippines M A Y Kayakking among the mangroves in Masantol Dennis Dizon Senator Tessie Aquino Oreta Mikey Arroyo Mayor Mary Jane Ortega, San Fernando City, La Union Cecilia Leung River tours launched Ariel Arcillas, Pres, SK Natl Federation THE Center sponsored a multi-sector Congressman Bondoc promised to Mark Alvin Diaz, SK Nueva Ecija Tessie Dennis Felarca, SK Zambales research cruise down Pampanga River convert a portion of his fishponds into a Oreta Brayant Gonzales, Angeles City last summer, discovered that the river is mangroves nursery and to construct a port Council not as silted and polluted as many believe, in San Luis town where tourist boats can Vice Mayor Pete Yabut, Macabebe and as a result, organized cultural and dock. The town’s centuries-old church is Vice Mayor Emilio Capati, Guagua ecological tours in coordination with the part of the planned itinerary for church Carmen Linda Atayde, SM Department of Tourism Region 3, local gov- heritage river cruises. Other cruise options Foundation ernment units in the river communities, include a tour of the mangroves in Masantol Efren de la Cruz, ABC President Estelito Mendoza and a private boatyard owner. and Macabebe, and tours coinciding with Col. -

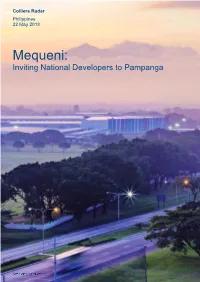

Mequeni: Inviting National Developers to Pampanga

Colliers Radar Philippines 22 May 2018 Mequeni: Inviting National Developers to Pampanga Mequeni1: Inviting National Developers to Pampanga The government’s active infrastructure implementation and decentralisation programme is encouraging developers to look closely at Pampanga, notably Clark Freeport and adjacent cities and municipalities. We think By Joey Roi Bondoc the Clark-Angeles-San Fernando corridor (Metro Clark) Manager| Research has high potential to become a key property investment hub outside Metro Manila. We see opportunities not only [email protected] for the office, residential, and retail segments, but also The Clark-Angeles-San Fernando for the leisure and industrial sectors. Given the relatively cheap developable land in the area, Colliers believes (Metro Clark) corridor in Pampanga that the development of integrated communities is a is benefiting from the government's practical route for many developers. To maximise Metro Clark’s potential, Colliers encourages both local and push to spread economic national developers to take the following steps: opportunities outside of Metro > Highlight differentiating features of townships; Manila. This is enticing national > Build three and four-star hotels and meeting, property developers to invest incentive, conference and exhibition (MICE) facilities; heavily in Metro Clark, resulting in > Explore transit-oriented, tourist-centric retail projects > Redevelop brownfield assets and old office and retail a pronounced development of buildings especially in downtown Angeles -

Effectivity of Permit Expiration of Permit III Non-Metallic Aurora

ORY OF MINES & QUARRIES, Regional Office No. III F DECEMBER 31, 2017) Duration of Permit Location (Barangay, Municipality, Region Mineral Province Municipality/City Commodity Permit Holder Operator Managing Official/Position Mailing Address Type of Permit Permit Number Effectivity of Expiration of Area (hectares) Province) Status Permit Permit Industries Development Industries Development IDC Building, Ortigas Avenue, Ugong Norte, Quezon City III Non-Metallic Aurora Dinalongan & Casiguran Dimension stones Corporation Corporation Anthony A. Dy, President MPSA 050-2007-IV 09/17/1996 09/16/2027 2,092.52 Dinalongan & Casiguran, Aurora under exploration Gold/Silver/ Copper 154-2000-III 03/31/2000 03/30/2025 1,410.24 Limay, Bagac & Mariveles, Bataan III Metallic Bataan Limay, Bagac & Mariveles Balanga Bataan Minerals Corp. Benguet Corporation Oscar T. Tranate, President 369 Adelfa St., San Jose, Balanga, Bataan MPSA 182-2002-III 12/09/2002 12/08/2027 126.52 Ipag Mariveles, Bataan under exploration Diamante Cement & Mining Diamante Cement & Mining III Non-Metallic Bataan Mariveles Basalt/Rocks/ Andesite Corporation Corporation Philip Jasa, President 7064 Wilson Stree, Pio del Pilar, Makati City MPSA under exploration Orient Aggregates & Structural Orient Aggregates & Structural Concept Suite 803, Antel Global Corporate Center, Ortigas Ave., Pasig City III Non-Metallic Bataan Mariveles Basalt/Rocks/ Andesite Concept Developers, Inc. Developers, Inc. Juan Julio Evangelista, President MPSA 248-2007-III 07/272007 07/26/2032 51.30 Sisiman, Mariveles, Bataan under exploration Aggregates/Sand/ III Non-Metallic Bataan Balanga Gravel Rockmix, Inc. Rockmix, Inc. Ruben C. Tagle, Vice President AlauUli, Pilar, Bataan MPSA 089-1997-III 11/20/1997 11/19/2022 20.79 Cupang, Balanga, Bataan producing Aggregates/Sand/ Mariveles Aggregates Base & Mariveles Aggregates Base & III Non-Metallic Bataan Mariveles Gravel Development Corporation Development Corporation Nicolas T. -

CDO List July.Xlsx

PROJECTS WITH ISSUED CDO's Regional Field Office: Northern Tagalog Region as of July 2019 CDO PROJECT LOCATION OWNER/DEVELOPER DATE ISSUED REASON FOR ISSUANCE Ace Executive Homes Brgy. Daang Sarile, Mr. Angel D. Concepcion June 29, 2015 Incomplete development within prescribed period. Cabanatuan City, Nueva Owner/developer requested for Cease and Desist Ecija Order due to its incapacity to develop the project. Amaresa 2 Muzon and Gaya-gaya, City Blue Mountain Properties January 28, 2019 Utilized National Housing Authority (NHA) project: of San Jose Del Monte, Sunshineville Phase 1 as compliance projects Bulacan required under R.A. 7279 as amended by R.A. 10884. Amber Homes Brgy. Poblacion, Sta. Maria, Northgate Land Philippines, May 19, 2014 Non-completion of development within prescribed Bulacan Inc. period. Angel Gabriel Residences Mandasig, Candaba, Renante T. Balagtas January 28, 2019 Utilized National Housing Authority (NHA) project: Pampanga Pili Peoples Village 1 as compliance projects required under R.A. 7279 as amended by R.A. 10884. Angeleños Ville Brgy. Cuayan, Angeles City Angeles City Government / August 18, 2014 Non-completion of development within prescribed E.A. Ygona Construction period. Aqua Fun Brgy. Biaan, Mariveles, Eath & Leisure Communities May 21, 2018 Non-compliance with HLURB directive on NOV Bataan Corporation issued February 22, 2018 Belvue Residences Muzon, City of San Jose Del Titan Primestate Realty & January 28, 2019 Utilized National Housing Authority (NHA) project: Monte, Bulacan Development Corp. Sunshineville Phase 1 as compliance projects required under R.A. 7279 as amended by R.A. 10884. Benjamin Village 8 De Muzon Hoa Brgy. Muzon, City of San JRC Holdings Corporation October 16, 2018 Non-completion of development within prescribed Jose Del Monte, Bulacan period. -

NDRRMC Update Re Effects of Southwest Monsoon 23 July 2012

Pagasa 1.5 Paco 1.5 San Pascual 1.5 Paliwas 1 Hulo 1 Lawa 1 Marilao Poblacion 2 2.3 Due to high tide Calumpit Meysulao 3 Due to high tide Sapang Bayan 1 Pulilan Tibag 1.5 Overflowed Irrigation Guiginto Poblacion 1.5 Panginay 1-2 Malis 1.5 (As of 11:00 AM, 23 July 2012 ) Valenzuela Balangkas Road, 2.5 Not Passable to Light Brgy. Balangkas Vehicles Rosemarie St. / Inner 2 Not Passable to Light St., Brgy. Tagalag Vehicles Bisig Road, Brgy. 2 Not Passable to Light Bisig Vehicles III. STATUS OF EVACUEES (As of 8:00 AM, 23 July 2012) • REGION III Affected Evacuation Municipality Barangay Families Persons Center Pulilan, Tibag 30 109 Tibag Chapel Bulacan • REGION IV-B NUMBER OF AFFECTED NAME OF EVACATION NAME OF BRGY FAMILIES PERSONS CENTER Alipaoy, Paluan,Occ. 2-Story residential houses 30 150 Mindoro Seven, Paluan, Brgy. Hall 40 200 Occ. Mindoro IV.SUSPENSION OF CLASSES (As of 7:00 AM, 23 July 2012) NCR • Valenzuela (Pre School, Elementary School and High School) • Malabon (Pre School, Elementary School and High School) • Quezon City ° Brgy. Bagong Silangan (Pre School, Elementary School and High School) ° Brgy. Payatas (Pre School, Elementary School and High School) REGION III • Pampanga ° Angeles, Candaba, Mexico, Porac, Apalit and Masantol (All Schools Public and Private) ° San Fernando (All levels in Don Honorio Ventura Technological State University, Saint Francis Academy) • Bulacan ° Meycauayan City (Pre School and Elementary) 2 Meycauayan East Elementary School Bangkal Elementary School Saluysoy Elementary School Calvario Elementary School Longos Elementary School Bayugo Elementary School Zamora Elementary School Ubihan Elementary School ° Balagtas, Hagonoy, Marilao, Malolos City, Obando, Pulilan, Paombong, San Miguel and San Ildefenso (All Schools Public and Private) ° Calumpit (Ecclesiastical Christian Institute, Pre School to High School) • Laguna ° San Pablo City (All levels) • Cavite ° Rosario (Sapa National High School) ° Cavite City (Private and Public) V. -

Directory of Field Office, Areas of Jurisdiction

` REGION III I. REGIONAL OFFICE 2/F Hyatt Garden Building, Dolores, City of San Fernando, Pampanga Tel. No. (045) 961-2292; Fax No. (045) 961-2282 E-mail Address: [email protected] / [email protected] Marissa DC. Alquetra - Regional Director Judea P. Asuncion - Assistant Regional Director Rachel C. Zulueta - Administrative Officer IV Rebecca V. Castro - Accountant I Neptalie L. Santos - Administrative Officer II/Budget Officer Asuncion Y. Pamintuan - Administrative Assistant II Judy Anne V. Yabut - Administrative Aide VI II. CITIES ANGELES CITY PAROLE AND PROBATION OFFICE Room 396, Hall of Justice Building, Pulung Maragul, Angeles City Tel. No. (045) 893-2173 E-mail Address: [email protected] / [email protected] PERSONNEL COMPLEMENT Elmer B. Gumapos - Chief Probation and Parole Officer Dolores M. Sigua - Supervising Probation and Parole Officer Gladys R. Valencia - Senior Probation and Parole Officer Mary Joy M. Gallardo - Administrative Aide IV AREAS OF JURISDICTION Angeles City, Mabalacat, Magalang, Porac COURTS SERVED RTC Branches 57 – 62 - Angeles City Branches 114 -118 - Angeles City Branch 10 - Angeles City MTCC Branches 1 to - Mabalacat City MTC Branches I, II, III - Angeles City Porac, Pampanga CABANATUAN CITY PAROLE AND PROBATION OFFICE Hall of Justice Building, ACCFA District, Maharlika Highway, Cabanatuan City Tel. No. (044) 600-4552 E-mail Address: [email protected] / [email protected] PERSONNEL COMPLEMENT Dustin G. Catacutan - Chief Probation