Netsuite Inc. Napa Acquisition Corporation Oc Acquisition

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Wharton Class of 2002

Wharton0B Undergraduate Class of 2011 Career19B Plans Survey Report 20U 11U Number of Degrees Awarded 676 Number of Completed Surveys 600 Response20B Rate 88.8% SUMMARY OF POST-GRADUATION PLANS Additional Non-Grad Education Seeking Graduate This report summarizes responses from Graduate School 0.3% School 5.3% 0.2% December 2010 and May/August 2011 Seeking Employment Wharton Bachelor of Science in Part-time Employed 4.2% Other 0.3% Economics degree recipients. 0.5% Short-term Employed 1.2% Even though the national unemployment Self-Employed rate remained stubbornly high during the 2.2% 2010-2011 academic year, the Wharton students fared extremely well in their job and graduate school searches. Most students (89.5%) entered the working world, while another 5.6 pursued further education. The average base salary rose significantly to $66,412, nearly $3,000 Full-time Employed more than the average salary for the Class 85.8% of 2010. JOB FUNCTIONS OF WHARTON GRADUATES The Class of 2011 entered a wide range of job functions upon graduation with investment banking, consulting, sales and trading, investment management and marketing/sales being top areas of interest for our students. Large employers such as Goldman Sachs, Citi, Morgan Stanley, J.P. Morgan, Boston Consulting Group and McKinsey hired the greatest number of Wharton graduates. However, students accepted employment in smaller numbers with a wide range of other employers including Abercrombie & Fitch, Kraft Foods, Google, L’Oreal, Prophet, PepsiCo and Teach for America. Report prepared by Barbara Hewitt, Senior Associate Director, Career Services, University of Pennsylvania, November 2011 METHODOLOGY Students were asked via several e-mail requests during Spring 2011 to complete an online version of the Career Plans Survey. -

Announcing: Finalists Circle for the Prestigious M&A

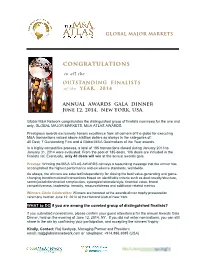

GLOBAL MAJOR MARKETS CONGRATULATIONS to all the OUTSTANDING FINALISTS of the YEAR, 2014 ANNUAL AWARDS GALA DINNER June 12, 2014, New YORK, USA. Global M&A Network congratulates the distinguished group of finalists nominees for the one and only, GLOBAL MAJOR MARKETS, M&A ATLAS AWARDS. Prestigious awards exclusively honors excellence from all corners of the globe for executing M&A transactions valued above a billion dollars as always in the categories of: 40 Deal, 7 Outstanding Firm and 4 Global M&A Dealmakers of the Year awards. In a highly competitive process, a total of 185 transactions closed during January 2013 to January 31, 2014 were evaluated. From the pool of 185 deals, 106 deals are included in the finalists list. Eventually, only 40 deals will win at the annual awards gala. Prestige: Winning the M&A ATLAS AWARDS conveys a resounding message that the winner has accomplished the highest performance and excellence standards, worldwide. As always, the winners are selected independently for closing the best value-generating and game- changing transformational transactions based on identifiable criteria such as deal novelty/structure, sector/jurisdiction/market complexities, synergies/rationale/style, financial value, brand competitiveness, leadership, tenacity, resourcefulness and additional related metrics. Winners Circle Celebration: Winners are honored at the awards dinner trophy presentation ceremony held on June 12, 2014 at the Harvard Club of New York. WHAT to DO if you are among the coveted group of distinguished finalists? If you submitted nominations, please confirm your guest attendance for the annual Awards Gala Dinner, held on the evening of June 12, 2014, NY. -

H-1B Petition Approvals for Initial Benefits by Employers FY07

NUMBER OF H-1B PETITIONS APPROVED BY USCIS FOR INITIAL BENEFICIARIES FY 2007 Approved Employer Petitions INFOSYS TECHNOLOGIES LIMITED 4,559 WIPRO LIMITED 2,567 SATYAM COMPUTER SERVICES LTD 1,396 COGNIZANT TECH SOLUTIONS US CORP 962 MICROSOFT CORP 959 TATA CONSULTANCY SERVICES LIMITED 797 PATNI COMPUTER SYSTEMS INC 477 US TECHNOLOGY RESOURCES LLC 416 I-FLEX SOLUTIONS INC 374 INTEL CORPORATION 369 ACCENTURE LLP 331 CISCO SYSTEMS INC 324 ERNST & YOUNG LLP 302 LARSEN & TOUBRO INFOTECH LIMITED 292 DELOITTE & TOUCHE LLP 283 GOOGLE INC 248 MPHASIS CORPORATION 248 UNIVERSITY OF ILLINOIS AT CHICAGO 246 AMERICAN UNIT INC 245 JSMN INTERNATIONAL INC 245 OBJECTWIN TECHNOLOGY INC 243 DELOITTE CONSULTING LLP 242 PRINCE GEORGES COUNTY PUBLIC SCHS 238 JPMORGAN CHASE & CO 236 MOTOROLA INC 234 MARLABS INC 229 KPMG LLP 227 GOLDMAN SACHS & CO 224 TECH MAHINDRA AMERICAS INC 217 VERINON TECHNOLOGY SOLUTIONS LTD 213 THE JOHNS HOPKINS MED INSTS OIS 205 YASH TECHNOLOGIES INC 202 ADVANSOFT INTERNATIONAL INC 201 UNIVERSITY OF MARYLAND 199 BALTIMORE CITY PUBLIC SCHOOLS 196 PRICEWATERHOUSECOOPERS LLP 192 POLARIS SOFTWARE LAB INDIA LTD 191 UNIVERSITY OF MICHIGAN 191 EVEREST BUSINESS SOLUTIONS INC 190 IBM CORPORATION 184 APEX TECHNOLOGY GROUP INC 174 NEW YORK CITY PUBLIC SCHOOLS 171 SOFTWARE RESEARCH GROUP INC 167 EVEREST CONSULTING GROUP INC 165 UNIVERSITY OF PENNSYLVANIA 163 GSS AMERICA INC 160 QUALCOMM INCORPORATED 158 UNIVERSITY OF MINNESOTA 151 MASCON GLOBAL CONSULTING INC 150 MICRON TECHNOLOGY INC 149 THE OHIO STATE UNIVERSITY 147 STANFORD UNIVERSITY 146 COLUMBIA -

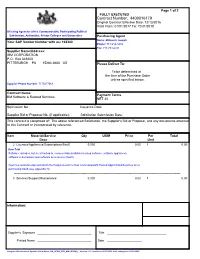

Contract Number: 4400016179

Page 1 of 2 FULLY EXECUTED Contract Number: 4400016179 Original Contract Effective Date: 12/13/2016 Valid From: 01/01/2017 To: 12/31/2018 All using Agencies of the Commonwealth, Participating Political Subdivision, Authorities, Private Colleges and Universities Purchasing Agent Name: Millovich Joseph Your SAP Vendor Number with us: 102380 Phone: 717-214-3434 Fax: 717-783-6241 Supplier Name/Address: IBM CORPORATION P.O. Box 643600 PITTSBURGH PA 15264-3600 US Please Deliver To: To be determined at the time of the Purchase Order unless specified below. Supplier Phone Number: 7175477069 Contract Name: Payment Terms IBM Software & Related Services NET 30 Solicitation No.: Issuance Date: Supplier Bid or Proposal No. (if applicable): Solicitation Submission Date: This contract is comprised of: The above referenced Solicitation, the Supplier's Bid or Proposal, and any documents attached to this Contract or incorporated by reference. Item Material/Service Qty UOM Price Per Total Desc Unit 2 Licenses/Appliances/Subscriptions/SaaS 0.000 0.00 1 0.00 Item Text Software: includes, but is not limited to, commercially available licensed software, software appliances, software subscriptions and software as a service (SaaS). Agencies must develop and attach the Requirements for Non-Commonwealth Hosted Applications/Services when purchasing SaaS (see Appendix H). -------------------------------------------------------------------------------------------------------------------------------------------------------- 3 Services/Support/Maintenance 0.000 0.00 -

Frank Quattrone Launches Qatalyst

For Immediate Release Contact: Bob Chlopak (202) 777-3506, (202) 841-2051 (m) Frank Quattrone Launches Qatalyst: New Technology Merchant Banking Boutique Qatalyst Partners to Provide M&A, Corporate Finance Advice; Qatalyst Capital Partners to Make Principal Investments San Francisco, CA., March 18, 2008 -- Frank P. Quattrone announced today that he and some former colleagues are launching a new financial services venture called Qatalyst Group, a technology-focused merchant banking boutique, headquartered in San Francisco, CA. Qatalyst Partners, its investment banking business, will provide high-end merger & acquisition and corporate finance advice to technology companies globally. Qatalyst Capital Partners, its investing business, will make selective principal investments, typically alongside leading venture capital and private equity firms. Qatalyst Partners will provide high quality, independent advice to the senior management teams and boards of the technology industry’s established and emerging leaders on strategic matters crucial to their growth and success. Qatalyst’s advisors will combine a broad network of relationships with deep sector knowledge and seasoned M&A expertise to deliver a superior, senior level of service for clients who value experience, judgment, candor and insight. In addition to merger & acquisition advice, Qatalyst Partners will use its team’s extensive corporate finance and capital markets experience to advise companies on capital structure and capital raising alternatives, and will selectively raise private capital for clients. While it will not engage in public securities research, sales, trading or brokerage, Qatalyst Partners may participate as advisor or underwriter in clients’ public offerings. “The launch of Qatalyst is an important development for the technology industry,” said Eric Schmidt, Chairman and CEO of Google. -

Investment Banking Network

INVESTMENT BANKING NETWORK THIS DOCUMENT CONTAINS CONFIDENTIAL AND PROPRIETARY INFORMATION AND IS INTENDED TO BE USED INTERNALLY AT THE KELLEYIBC SCHOOL Presentation OF BUSINESS AND WITH 10.2.17 THOSE INVOLVED WITH THE IBN THIS DOCUMENT CONTAINS CONFIDENTIAL AND PROPRIETARY INFORMATION AND IS INTENDED TO BE USED INTERNALLY AT THE 2 KELLEY SCHOOL OF BUSINESS AND WITH THOSE INVOLVED WITH THE IBN Program Director – Professor David Haeberle • BS/MBA/JD Indiana University Kelley School of Business and Maurer School of Law • Financial Analyst by Training – MiniScribe Corporation • Entrepreneur - #2/#3 Guy – Capital Raising and CFO • Transaction Verifications Systems • EcoMed Corporation • Command Equity Group • Command Corporation • ConsulTech Technologies • Envisage Technologies • Haeberle Investments, LLC • Clinical Professor of Finance – Director of the Investment Banking Network THIS DOCUMENT CONTAINS CONFIDENTIAL AND PROPRIETARY INFORMATION AND IS INTENDED TO BE USED INTERNALLY AT THE3 KELLEY SCHOOL OF BUSINESS AND WITH THOSE INVOLVED WITH THE IBN Investment Banking Network • Investment Banking Club • F228 Introduction to Investment Banking • Apply January of sophomore year • F355 Investment Banking & Capital Markets • Admittance to the IBW in March of sophomore year • Summer Homework & Networking between sophomore and junior year. • NYC Boot Camp in August • On-campus interviews in September junior year • F428 Junior Year • F429 Senior Year THIS DOCUMENT CONTAINS CONFIDENTIAL AND PROPRIETARY INFORMATION AND IS INTENDED TO BE USED INTERNALLY AT THE4 KELLEY SCHOOL OF BUSINESS AND WITH THOSE INVOLVED WITH THE IBN Full-Time Placement Overview Firm Students Full-Time Placement by City Prior Year Jefferies 5 Lazard 5 New York 32 30 Bank of America Merrill Lynch 4 BMO Capital 4 Barclays 4 Chicago 23 17 J.P. -

Enterprise CRM Suites

Oracle Corporation et al v. SAP AG et al Doc. 844 Att. 14 EXHIBIT N Dockets.Justia.com August 29, 2008 | Updated: September 2, 2008 The Forrester Wave™: Enterprise CRM Suites, Q3 2008 by William Band for Business Process & Applications Professionals Making Leaders Successful Every Day ORCLX-PIN-000006_001 For Business Process & Applications Professionals Includes a Forrester Wave™ August 29, 2008 | Updated: September 2, 2008 The Forrester Wave™: Enterprise CRM Suites, Q3 2008 Buyers Face Difficult Choices In A Crowded Market by William Band with Sharyn C. Leaver, Pete Marston, Natalie L. Petouhoff, Ph.D., Elisse Gaynor, and Andrew Magarie EXECUTIVE SUMMARY Forrester evaluated leading enterprise CRM suite solutions against 516 criteria and found that with the latest releases of their solutions, Oracle’s Siebel and SAP maintain their status as Leaders with comprehensive functionality and much improved usability. Microsoft, salesforce.com, RightNow, and Oracle CRM On Demand have improved their credibility as enterprise-class solutions and have graduated into the Leaders group. The latter vendors all get high marks for ease-of-use and quick time-to-value. The Leaders are challenged by Strong Performers offering a diverse range of benefits. Oracle’s E-Business Suite CRM and PeopleSoft CRM are good options for their respective ERP customers looking for end-to-end integration. Chordiant, ciboodle, and Pegasystems offer business process management (BPM) strengths to help enterprises orchestrate complex customer-facing processes. Infor CRM Epiphany and Onyx CRM are working to regain market momentum through investments in product enhancements being made by their respective new corporate parents, Infor and Consona. -

Emerging Technologies for Academic Libraries in the Digital Age CHANDOS INFORMATION PROFESSIONAL SERIES

Emerging Technologies for Academic Libraries in the Digital Age CHANDOS INFORMATION PROFESSIONAL SERIES Series Editor: Ruth Rikowski (email: [email protected]) Chandos’ new series of books are aimed at the busy information professional. They have been specially commissioned to provide the reader with an authoritative view of current thinking. They are designed to provide easy-to-read and (most importantly) practical coverage of topics that are of interest to librarians and other information professionals. If you would like a full listing of current and forthcoming titles, please visit our web site www.chandospublishing.com or contact Hannah Grace-Williams on email [email protected] or telephone number +44 (0) 1993 848726. New authors: we are always pleased to receive ideas for new titles; if you would like to write a book for Chandos, please contact Dr Glyn Jones on email [email protected] or telephone number +44 (0) 1993 848726. Bulk orders: some organisations buy a number of copies of our books. If you are interested in doing this, we would be pleased to discuss a discount. Please contact Hannah Grace-Williams on email [email protected] or telephone number +44 (0) 1993 848726. Emerging Technologies for Academic Libraries in the Digital Age LILI LI Chandos Publishing Oxford · England Chandos Publishing (Oxford) Limited TBAC Business Centre Avenue 4 Station Lane Witney Oxford OX28 4BN UK Tel: +44 (0) 1993 848726 Fax: +44 (0) 1865 884448 E-mail: [email protected] www.chandospublishing.com First published in Great Britain in 2009 ISBN: 978 1 84334 320 2 (paperback) 978 1 84334 323 3 (hardback) 1 84334 320 7 (paperback) 1 84334 323 1 (hardback) © LiLi Li, 2009 British Library Cataloguing-in-Publication Data. -

15 Recruiters Guide.Pdf

1 WELCOME Whatever your company seeks, Michigan Ross has a lot to offer. If you’re looking for new hires or interns, our talent pool is deep and diverse. Employers tell us Ross graduates stand out as bright, energetic, and creative. They excel at core business skills, and they’re grounded in the Ross dedication to positive business principles. If you’d like to see for yourself, we take pride in a smooth and rewarding recruiting process. Even if your company is not currently hiring, we’d like to partner with you. You might participate in a class or a conference, enlist a team of MBAs to solve a business challenge, or introduce students to your company at an on-site visit. You’ll likely find that you gain just as much from these interactions as the students do. We look forward to working together! 22 3 MEET OUR STUDENTS If you want to hire someone who can make an immediate impact and excel over time, you’ll want to look at Michigan Ross. We emphasize hands-on learning, excellent quantitative skills, and a multidisciplinary view of business and the wider world. Through our groundbreaking leadership development programs, Ross students learn how to make organizations more collaborative, more competitive, and more innovative. This is why the world’s top companies recruit at Ross every year. When you are seeking that perfect fit for a job in finance, consulting, marketing, or any other role in business — from entry-level to executive — you’ll find them at Michigan Ross. 44 BACHELOR OF BUSINESS ADMINISTRATION MASTER OF MANAGEMENT Students in the top-ranked Ross BBA Program Students in Ross’ innovative new MM program learn critical business skills with a boundary-breaking move directly from an undergraduate degree in approach. -

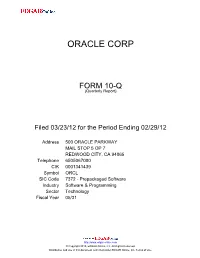

Oracle Corporation (Exact Name of Registrant As Specified in Its Charter)

ORACLE CORP FORM 10-Q (Quarterly Report) Filed 03/23/12 for the Period Ending 02/29/12 Address 500 ORACLE PARKWAY MAIL STOP 5 OP 7 REDWOOD CITY, CA 94065 Telephone 6505067000 CIK 0001341439 Symbol ORCL SIC Code 7372 - Prepackaged Software Industry Software & Programming Sector Technology Fiscal Year 05/31 http://www.edgar-online.com © Copyright 2015, EDGAR Online, Inc. All Rights Reserved. Distribution and use of this document restricted under EDGAR Online, Inc. Terms of Use. Table of Contents UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 10-Q x QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the quarterly period ended February 29, 2012 or ¨ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the transition period from to Commission File Number: 000-51788 Oracle Corporation (Exact name of registrant as specified in its charter) Delaware 54-2185193 (State or other jurisdiction of (I.R.S. Employer incorporation or organization) Identification No.) 500 Oracle Parkway Redwood City, California 94065 (Address of principal executive offices) (Zip Code) (650) 506-7000 (Registrant’s telephone number, including area code) Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. -

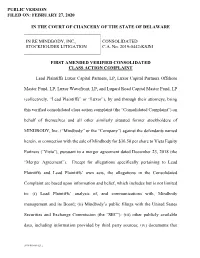

02-19-20 First Amended Cons. Complaint

PUBLIC VERSION FILED ON: FEBRUARY 27, 2020 IN THE COURT OF CHANCERY OF THE STATE OF DELAWARE IN RE MINDBODY, INC., CONSOLIDATED STOCKHOLDER LITIGATION C.A. No. 2019-0442-KSJM FIRST AMENDED VERIFIED CONSOLIDATED CLASS ACTION COMPLAINT Lead Plaintiffs Luxor Capital Partners, LP, Luxor Capital Partners Offshore Master Fund, LP, Luxor Wavefront, LP, and Lugard Road Capital Master Fund, LP (collectively, “Lead Plaintiffs” or “Luxor”), by and through their attorneys, bring this verified consolidated class action complaint (the “Consolidated Complaint”) on behalf of themselves and all other similarly situated former stockholders of MINDBODY, Inc. (“Mindbody” or the “Company”) against the defendants named herein, in connection with the sale of Mindbody for $36.50 per share to Vista Equity Partners (“Vista”), pursuant to a merger agreement dated December 23, 2018 (the “Merger Agreement”). Except for allegations specifically pertaining to Lead Plaintiffs and Lead Plaintiffs’ own acts, the allegations in the Consolidated Complaint are based upon information and belief, which includes but is not limited to: (i) Lead Plaintiffs’ analysis of, and communications with, Mindbody management and its Board; (ii) Mindbody’s public filings with the United States Securities and Exchange Commission (the “SEC”); (iii) other publicly available data, including information provided by third party sources; (iv) documents that {FG-W0461423.} Lead Plaintiffs obtained pursuant to Section 220 of the Delaware General Corporation Law; and (v) limited and incomplete document productions in the above-captioned consolidated action. NATURE OF THE CASE 1. This action is brought by Luxor, which owned 18.9% of Mindbody’s outstanding common stock prior to the challenged buyout of Mindbody by Vista (the “Merger”). -

Is Open Source the ERP Cure-All? Page 1 of 5

Is Open Source the ERP Cure-All? Page 1 of 5 Enterprise Resource Planning PRINT THIS PAGE NOW Is Open Source the ERP Cure-All? 5/1/2008 By Joseph C. Panettieri Conventional and hosted applications thrive, but open source ERP is coming on strong. Here's how to choose the best type of solution for your own institution. Campus CIOs John Bielec and Bradley Wheeler are IT experts with strikingly similar missions: They want modern enterprise applications to manage their respective universities' critical information. Ultimately, Bielec and Wheeler took divergent paths to ERP (enterprise resource planning) success. Importantly, each CIO carefully assessed campus need and the most current options available, before committing to an ERP solution or solutions. Wheeler, VP for IT and CIO of Indiana University, has focused his efforts on open source ERP. In contrast, Bielec, Drexel University (PA) CIO, is leveraging closed source ERP software, but in a hosted model. Evolution of Options In many ways, the evolution of the ERP market is littered with ironies. When Oracle began buying up customer relationship management (CRM) and ERP companies, some universities worried that they would be left with fewer choices and higher prices. Yet, the rise of open source-coupled with the advent and growth of software as a service (SaaS)-has created a whole range of new ERP options. In addition to Oracle, today's options include Jenzabar, Campus Management, Datatel, SunGard Higher Education, and numerous others. For instance, 20-plus universities have joined the Kuali Foundation, a nonprofit organization driving open source ERP forward. Bigname Kuali backers include Cornell University (NY), Carnegie Mellon University (PA), the Massachusetts Institute of Technology, and Indiana University.