Mastercard Inc

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Mobile Banking

Automated teller machine "Cash machine" Smaller indoor ATMs dispense money inside convenience stores and other busy areas, such as this off-premise Wincor Nixdorf mono-function ATM in Sweden. An automated teller machine (ATM) is a computerized telecommunications device that provides the customers of a financial institution with access to financial transactions in a public space without the need for a human clerk or bank teller. On most modern ATMs, the customer is identified by inserting a plastic ATM card with a magnetic stripe or a plastic smartcard with a chip, that contains a unique card number and some security information, such as an expiration date or CVVC (CVV). Security is provided by the customer entering a personal identification number (PIN). Using an ATM, customers can access their bank accounts in order to make cash withdrawals (or credit card cash advances) and check their account balances as well as purchasing mobile cell phone prepaid credit. ATMs are known by various other names including automated transaction machine,[1] automated banking machine, money machine, bank machine, cash machine, hole-in-the-wall, cashpoint, Bancomat (in various countries in Europe and Russia), Multibanco (after a registered trade mark, in Portugal), and Any Time Money (in India). Contents • 1 History • 2 Location • 3 Financial networks • 4 Global use • 5 Hardware • 6 Software • 7 Security o 7.1 Physical o 7.2 Transactional secrecy and integrity o 7.3 Customer identity integrity o 7.4 Device operation integrity o 7.5 Customer security o 7.6 Alternative uses • 8 Reliability • 9 Fraud 1 o 9.1 Card fraud • 10 Related devices • 11 See also • 12 References • 13 Books • 14 External links History An old Nixdorf ATM British actor Reg Varney using the world's first ATM in 1967, located at a branch of Barclays Bank, Enfield. -

Electronic Cash in Hong Kong

1 Focus THEME ity of users to lock their cards. Early in 1992, NatWest began a trial of Mondex in BY I. CHRISTOPHERWESTLAND. MANDY KWOK, ]OSEPHINESHU, TERENCEKWOK AND HENRYHO, HONG KONG an office complex in London with a 'can- UNIVERSITYOF SCIENCE&TECHNOLOGY. HONG KONG * teen card' known as Byte. The Byte trial is still continuing with more than 5,000 INTRODUCTION I teller cash for a card and uses it until that people using the card in two office res- Asian business has long had a fondness value is exhausted. Visa plans to offer a taurants and six shops. By December of for cash. While the West gravitated toward reloadable card later. 1993, the Mondex card was introduced on purchases on credit - through cards or a large scale. Sourcing for Mondex sys- installments - Asia maintained its passion HISTORY tem components involves more than 450 for the tangible. Four-fifths of all trans- Mondex was the brainchild of two NatWest manufacturers in over 40 countries. In actions in Hong Kong are handled with bankers - Tim Jones and Graham Higgins. October of 1994, franchise rights were sold cash. It is into this environment that They began technology development in to the Hong Kong and Shanghai Banking Mondex International, the London based 1990 with electronics manufacturers in the Corporation Limited to cover the Asian purveyor of electronic smart cards, and UK, USA and Japan. Subsequent market region including Hong Kong, China, In- Visa International, the credit card giant, research with 47 consumer focus groups dia, Indonesia, Macau, Philippines, are currently competing for banks, con- in the US, France, Germany, Japan, Hong Singapore and Thailand. -

306-324 Angol Czimer Jozsef.Indd

306 JÓZSEF CZÍMER CHANGING PAYMENT LANDSCAPE1 József Czímer Th is paper is intended to be diff erent from others. I shall of course discuss almost all new achievements in the forefront of the payments industry – and there is a large number of them – but we shall see how very few systems in fact serve the vast numbers of diff erent payment tools. Also, this article tries not to be too technical, because the authors believe that even bankers claiming to be payments specialist are unfamiliar with the entire value chain of the payment service industry. Th e aim of this paper is to show what the customer sees and what is behind this front and accordingly, to show the interaction between the various elements of the system. JEL codes: G20, G21, G23 Keywords: payment services, bank card payments, mobile payments, payment infrastucure Although the European Parliament adopted European Commission proposal to create safer and more innovative European payments in Brussels on 8 October 2015, known as PSD2, this paper will refer to the PSD1 due to the fact that, fi rstly, the PSD2 has not yet entered into force and, secondly, the PSDs this paper deals with have not been changed signifi cantly. When PSD2 enters into force it will intend to amend and replace PSD1 to •reduce ambiguity; • level the playing fi eld for payments providers; • increase consumer protection; • stimulate innovation; • increase competition; and • enforce the implementation of new payments type. Th e two major provisions and implications of PSD2 will be the followings: • it accepts the Th ird Party Payment (TPP) provision; and • under the “Access to Accounts” (XS2A) rule it will force banks to provide customer account information to third parties via API, if the account holder agrees. -

Study on the Implementation of Recommendation 97/489/EC

Study on the implementation of Recommendation 97/489/EC concerning transactions carried out by electronic payment instruments and in particular the relationship between holder and issuer Call for Tender XV/99/01/C FINAL REPORT – Part b) Appendices 20th March 2001 Study on the implementation of Recommendation 97/489/EC 1 APPENDICES Appendices 1. Methodology.................................................................................3 Appendices 2. Tables..........................................................................................28 Appendices 3. List of issuers and EPIs analysed and surveyed........................147 Appendices 4. General summary of each Work Package.................................222 Appendices 5. Reports country per country (separate documents) Study on the implementation of Recommendation 97/489/EC 2 Appendices 1 Methodology Study on the implementation of Recommendation 97/489/EC 3 Content of Appendices 1 1. Structure of the report ..............................................................................5 2. Route Map................................................................................................6 3. Methodology.............................................................................................7 4. Tools used..............................................................................................14 Study on the implementation of Recommendation 97/489/EC 4 1. The Structure of the Report The aims of the study were to investigate how far the 1997 Recommendation has been -

Banktocustomerdebitcreditnoti

Usage Guideline BankToCustomerDebitCreditNotificationV06 - Mixed Bank to Corporate Messages Portfolio - Draft - January 31, 2017 This document describes a usage guideline restricting the base message MX camt.054.001.06. You can also consult this information online. Published by Payments Canada and generated by MyStandards. 30 January 2017 Usage Guideline Table of Contents .Message Functionality ................................................................................................................................................. 3 1 Restriction summary ......................................................................................................................................... 5 2 Structure ................................................................................................................................................................. 6 3 Rules ......................................................................................................................................................................... 7 4 Message Building Blocks ............................................................................................................................... 8 5 Message Components .................................................................................................................................... 10 6 Message Datatypes ........................................................................................................................................ 226 7 Restriction appendix -

Information Technology in the Banking and Financial Sectors

INFORMATION TECHNOLOGY IN THE BANKING AND FINANCIAL SECTORS MARCH 25, 1996 BACKGROUND BREIFING PAPER OF THE TELECOMMUNICATIONS INFOTECHNOLOGY FORUM (please attribute any quotation) Information Technology in the Banking and Financial Services Sector Smartcards, banks and telephones A brief historical introduction; what this suggests about the future Banks first started using computers linked to telecommunications systems in a big way in the 1970s and 1980s, when local area networks allowed them to start automating accounts—and thus to introduce automatic teller machines (ATMs) which customers could use to find out how much money was in their accounts and make cash withdrawals. ATMs appeared to offer two things: — A competitive advantage: better service for customers. — Savings on staff costs, as tellers were replaced with machines. The first of these is undoubtedly true. A network of ATMs operating 24 hours a day takes the necessity out of planning when to get money for individuals—it is hard to imagine anyone accepting a bank without an ATM network for their day-to-day financial needs (though judging by the queues in some banks, some people do not seem to have realised quite what can be done with an ATM card). The second, however, has not really happened, at least in the way it was originally imagined. What has happened is that on the one hand staff have been freed up for other things—such as handling the huge array of financial services banks now offer compared with a couple of decades ago—and on the other IT has taken on a life of its own as banks think of new ways to wire themselves and their customers. -

An Empirical Analysis of New Zealand Bank Customers' Satisfaction

View metadata, citation and similar papers at core.ac.uk brought to you by CORE provided by Lincoln University Research Archive Lincoln University Digital Thesis Copyright Statement The digital copy of this thesis is protected by the Copyright Act 1994 (New Zealand). This thesis may be consulted by you, provided you comply with the provisions of the Act and the following conditions of use: you will use the copy only for the purposes of research or private study you will recognise the author's right to be identified as the author of the thesis and due acknowledgement will be made to the author where appropriate you will obtain the author's permission before publishing any material from the thesis. AN EMPIRICAL ANALYSIS OF NEW ZEALAND BANK CUSTOMERS’ SATISFACTION _______________________________________________________ A thesis submitted in partial fulfillment of the requirements for the Degree of Master of Commerce and Management at Lincoln University by Jing Wei _______________________________________________________ Lincoln University 2010 Abstract of a thesis submitted in partial fulfilment of the requirements for the Degree of M.C.M AN EMPIRICAL ANALYSIS OF NEW ZEALAND BANK CUSTOMERS’ SATISFACTION By Jing Wei It is important that banks deliver quality services which in turn results in customer satisfaction in today’s competitive banking environment. Within the New Zealand financial service market, competition is deemed to be strong given that there have been new entrants into the market as well as mergers and acquisition and exits over the last ten years (Chan, Schumacher, and Tripe, 2007). In order to retain the customers, customer satisfaction becomes a crux issue to bank management. -

ABCD Life Sciences Top Titles

ABCD springer.com Life Sciences Top Titles September 2009 springer.com Biochemistry (general) 2 Biochemistry (general) powerful tool that enables us to seek a deeper under- ine the relevant physiological, emotional, cognitive standing of the complex mechanisms underpinning so and social processes. The resulting understanding of many vital biologic systems. In this fully revised and the functional interplay of these processes gives valu- updated second edition of Bioluminescence: Meth- able insights into the biological roots and benefits of ods and Protocols, expert researchers contribute a religion. readable and utilitarian compilation of the newest More on www.springer.com/978-3-642-00127-7 and most innovative techniques that have emerged in this rapidly expanding and progressively diverse Available field including methods to assess cell trafficking, pro- 2009. X, 304 p. 13 illus. (The Frontiers Collection, ) tein-protein interactions, intracellular signaling, and 978-3-642-00127-7 ▶ 69,95 € apoptosis. Also opening up the possibility to visual- ize and quantify biological mechanisms in real-time and in in vivo settings, the volume also describes the in vivo study of bacterial or viral infections, trans- planted cells, stem cells proliferation, vascular flow, E. Jacoby and tumors. Written in the highly successful Meth- ods in Molecular Biology™ series format, chapters Chemogenomics include brief introductions to their respective top- Methods and Applications ics, lists of the necessary materials, equipment, and reagents, step-by-step, readily reproducible laboratory The establishment, analysis, prediction, and expan- protocols, and notes on troubleshooting and avoiding sion of a comprehensive ligand-target Struc- known pitfalls. Authoritative and cutting-edge, Bio- ture-Activity Relationship (SAR) in the post-genomic luminescence: Methods and Protocols, Second Edi- era presents a key research challenge for this cen- tion provides protocols that are detailed enough to tury. -

What Is a Chip Card?

The Technology Is Ready Philip Andreae Philip Andreae & Associates Why are you Here • The globe is in migration to EMV • June 2003: Visa Canada announced its plans to migrate to chip • January 8, CTV W-5 documented the reality of debit card fraud • October 2005: Interac issued schedule for chip • American Express, MasterCard and JCB are ready to support the Canadian migration to chip The Time Has Come 2 What is a Chip Card? • A plastic credit card with an embedded computer chip containing a microcomputer –1976 a calculator in your card –Today the power of 1981 IBM PC –Tomorrow integrated with your body, PDA and Cell Phone? 3 History of Chip Cards a.k.a the Smart Card • 1968 German Inventors, • French Banks Jurgen Dethloff & Helmet Specifications 1977 Grotrupp German patent use of • Honeywell Bull plastic as a carrier for Microchips Produce First Cards 1978 • 1970 Japanese Inventor, • Payphone Cards 1983 Kunitake Arimura applied for • French Banking similar patent Pilot Begins 1984 • 1974 French Inventor, Roland • Used in TV 1990 Moreno patented the Smart Card • ETSI GSM SIM 1991 • 1978 Honeywell Bull proves • First ePurse in miniaturization of electronics Bulle, Switzerland 1992 • 1993 Work on EMV began • German Health Card 1993 • 1995 MasterCard Buys Mondex • First Combi Card 1997 • Mondex in Canada 1998 4 1984-1992 • France Banks elect to implement smart cards • Carte Bancaire develop chip application - B0’ • Merchants receive government incentives • Cardholders use PIN for both credit and debit • Domestic fraud down to 0.02% The World -

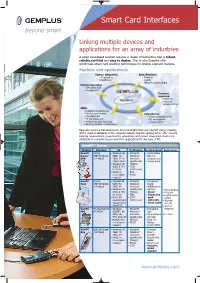

Smart Card Interfaces

Smart Card Interfaces Linking multiple devices and applications for an array of industries A smart card-based solution requires a reader infrastructure that is robust, reliable,certified and easy to deploy. That is why Gemplus offer world-class smart card enabling technologies for diverse segment markets. Markets and applications System integrators: Bank/Retailers: • ID programs • Payment • Healthcare • Loyalty • Network access control Telecom operators: • SIM smart card management Transport operators: • Payment • Physical access control OEMs: • Keyboard manufacturers • Point of sale terminal Corporations: manufacturers • Physical access control • PC manufacturers • PC and network • Set-top box manufacturers access control • Vending machine manufacturers Easy and secure e-transactions are more important than ever. GemPC range, meeting all the required standards of the computer industry and the banking world, offer Telecom, banking organizations, governments, enterprises and system integrators smart card interfaces to complete secure electronic applications for any type of PC. GemPC™ Range Product Interface OS Certification Benefits & Options Applications GemPC RS232 • Windows 98, • Microsoft • Customizable Serial/ USB Full Speed 98SE, Me, Windows® • Slim line USB (12 Mbps) 2000, XP for Hardware compact case USB & Serial Quality Labs • Tamper proof • Windows 95 (WHQL) OSR2 & NT4 • CCID for Serial (USB mode) • MacOS X, • EMV Linux (upon • PC/SC request) GemPC RS232 • Windows 98, • Microsoft • Transparent Twin USB Full Speed 98SE, Me, Windows® -

Bin Qty Brand Code Bank Level Type Country 180006 1

BIN QTY BRAND CODE BANK LEVEL TYPE COUNTRY 180006 1 Unknown 120 Unknown Unknown Unknown Unknown 180015 1 Unknown 120 Unknown Unknown Unknown Unknown 180028 1 Unknown 120 Unknown Unknown Unknown Unknown 180036 1 Unknown 120 Unknown Unknown Unknown Unknown 180039 1 Unknown 101 Unknown Unknown Unknown Unknown 180050 1 Unknown 120 Unknown Unknown Unknown Unknown 180051 1 Unknown 101 Unknown Unknown Unknown Unknown 213168 1 Unknown 221 Unknown Unknown Unknown Unknown 300000 2 Unknown 101 Unknown Unknown Unknown Unknown 300070 1 Unknown 101 Unknown Unknown Unknown Unknown 300087 1 Unknown 101 Unknown Unknown Unknown Unknown 300100 1 Unknown 101 Unknown Unknown Unknown Unknown 300400 1 Unknown 101 Unknown Unknown Unknown Unknown 300583 1 Unknown 101 Unknown Unknown Unknown Unknown 300600 1 Unknown 101 Unknown Unknown Unknown Unknown 300718 1 Unknown 101 Unknown Unknown Unknown Unknown 300752 35 Unknown 101 Unknown Unknown Unknown Unknown 300763 17 Unknown 101 Unknown Unknown Unknown Unknown 300800 6 Unknown 101 Unknown Unknown Unknown Unknown 300901 1 Unknown 101 Unknown Unknown Unknown Unknown 300903 1 Unknown 101 Unknown Unknown Unknown Unknown 300928 4 Unknown 101 Unknown Unknown Unknown Unknown 300940 1 Unknown 101 Unknown Unknown Unknown Unknown 300941 1 Unknown 101 Unknown Unknown Unknown Unknown 300947 2 Unknown 101 Unknown Unknown Unknown Unknown 301305 1 Unknown 101 Unknown Unknown Unknown Unknown 301460 1 Unknown 101 Unknown Unknown Unknown Unknown 301702 1 Unknown 101 Unknown Unknown Unknown Unknown 301801 1 Unknown 101 Unknown Unknown -

E-Admin Terms and Conditions Administrator Is Appointed by the Login Credentials Company, Is Responsible for E-Admin Temporary Password and User ID

E-admin Terms and Conditions administrator is appointed by the Login Credentials Company, is responsible for e-admin Temporary password and User ID. 2020/04 within the Company and will be the contact person that Eurocard sends PCI DSS 1. Introduction information regarding e-admin to. The The Payment Card Industry Data Security E-admin is Eurocard's online system for super administrator is able to access all Standard (PCI DSS) is a widely accepted the administration of Cards and Accounts. functions and modules that the Company set of policies and procedures intended to has been granted access to and has optimize the security of credit, debit and E-admin offers a number of different immediate access to all Cards and cash card transactions and protect functions that the Company has Accounts connected to the Company in e- cardholders against misuse of their immediate access to, as well as a number admin. Super administrators also have the personal information. Websites of the PCI of optional modules that the Company right to appoint new administrators and Security Standards Council, (www. pcisecuritystandards.org) include can request access to. update and delete administrators’ access rights. A super administrator is not instructions and information concerning The Company has access to the following allowed to appoint new super safe handling of card data. functions in e-admin: administrators. Temporary password Card An eight-digit OTP (One-Time Password) • View Cards and Accounts Refers to Eurocard Corporate cards with sent to the Administrator’s mobile phone • Apply for and close Cards and the exception of Eurocard Corporate Limit number .