Electronic Cash in Hong Kong

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Mobile Banking

Automated teller machine "Cash machine" Smaller indoor ATMs dispense money inside convenience stores and other busy areas, such as this off-premise Wincor Nixdorf mono-function ATM in Sweden. An automated teller machine (ATM) is a computerized telecommunications device that provides the customers of a financial institution with access to financial transactions in a public space without the need for a human clerk or bank teller. On most modern ATMs, the customer is identified by inserting a plastic ATM card with a magnetic stripe or a plastic smartcard with a chip, that contains a unique card number and some security information, such as an expiration date or CVVC (CVV). Security is provided by the customer entering a personal identification number (PIN). Using an ATM, customers can access their bank accounts in order to make cash withdrawals (or credit card cash advances) and check their account balances as well as purchasing mobile cell phone prepaid credit. ATMs are known by various other names including automated transaction machine,[1] automated banking machine, money machine, bank machine, cash machine, hole-in-the-wall, cashpoint, Bancomat (in various countries in Europe and Russia), Multibanco (after a registered trade mark, in Portugal), and Any Time Money (in India). Contents • 1 History • 2 Location • 3 Financial networks • 4 Global use • 5 Hardware • 6 Software • 7 Security o 7.1 Physical o 7.2 Transactional secrecy and integrity o 7.3 Customer identity integrity o 7.4 Device operation integrity o 7.5 Customer security o 7.6 Alternative uses • 8 Reliability • 9 Fraud 1 o 9.1 Card fraud • 10 Related devices • 11 See also • 12 References • 13 Books • 14 External links History An old Nixdorf ATM British actor Reg Varney using the world's first ATM in 1967, located at a branch of Barclays Bank, Enfield. -

Study on the Implementation of Recommendation 97/489/EC

Study on the implementation of Recommendation 97/489/EC concerning transactions carried out by electronic payment instruments and in particular the relationship between holder and issuer Call for Tender XV/99/01/C FINAL REPORT – Part b) Appendices 20th March 2001 Study on the implementation of Recommendation 97/489/EC 1 APPENDICES Appendices 1. Methodology.................................................................................3 Appendices 2. Tables..........................................................................................28 Appendices 3. List of issuers and EPIs analysed and surveyed........................147 Appendices 4. General summary of each Work Package.................................222 Appendices 5. Reports country per country (separate documents) Study on the implementation of Recommendation 97/489/EC 2 Appendices 1 Methodology Study on the implementation of Recommendation 97/489/EC 3 Content of Appendices 1 1. Structure of the report ..............................................................................5 2. Route Map................................................................................................6 3. Methodology.............................................................................................7 4. Tools used..............................................................................................14 Study on the implementation of Recommendation 97/489/EC 4 1. The Structure of the Report The aims of the study were to investigate how far the 1997 Recommendation has been -

Information Technology in the Banking and Financial Sectors

INFORMATION TECHNOLOGY IN THE BANKING AND FINANCIAL SECTORS MARCH 25, 1996 BACKGROUND BREIFING PAPER OF THE TELECOMMUNICATIONS INFOTECHNOLOGY FORUM (please attribute any quotation) Information Technology in the Banking and Financial Services Sector Smartcards, banks and telephones A brief historical introduction; what this suggests about the future Banks first started using computers linked to telecommunications systems in a big way in the 1970s and 1980s, when local area networks allowed them to start automating accounts—and thus to introduce automatic teller machines (ATMs) which customers could use to find out how much money was in their accounts and make cash withdrawals. ATMs appeared to offer two things: — A competitive advantage: better service for customers. — Savings on staff costs, as tellers were replaced with machines. The first of these is undoubtedly true. A network of ATMs operating 24 hours a day takes the necessity out of planning when to get money for individuals—it is hard to imagine anyone accepting a bank without an ATM network for their day-to-day financial needs (though judging by the queues in some banks, some people do not seem to have realised quite what can be done with an ATM card). The second, however, has not really happened, at least in the way it was originally imagined. What has happened is that on the one hand staff have been freed up for other things—such as handling the huge array of financial services banks now offer compared with a couple of decades ago—and on the other IT has taken on a life of its own as banks think of new ways to wire themselves and their customers. -

What Is a Chip Card?

The Technology Is Ready Philip Andreae Philip Andreae & Associates Why are you Here • The globe is in migration to EMV • June 2003: Visa Canada announced its plans to migrate to chip • January 8, CTV W-5 documented the reality of debit card fraud • October 2005: Interac issued schedule for chip • American Express, MasterCard and JCB are ready to support the Canadian migration to chip The Time Has Come 2 What is a Chip Card? • A plastic credit card with an embedded computer chip containing a microcomputer –1976 a calculator in your card –Today the power of 1981 IBM PC –Tomorrow integrated with your body, PDA and Cell Phone? 3 History of Chip Cards a.k.a the Smart Card • 1968 German Inventors, • French Banks Jurgen Dethloff & Helmet Specifications 1977 Grotrupp German patent use of • Honeywell Bull plastic as a carrier for Microchips Produce First Cards 1978 • 1970 Japanese Inventor, • Payphone Cards 1983 Kunitake Arimura applied for • French Banking similar patent Pilot Begins 1984 • 1974 French Inventor, Roland • Used in TV 1990 Moreno patented the Smart Card • ETSI GSM SIM 1991 • 1978 Honeywell Bull proves • First ePurse in miniaturization of electronics Bulle, Switzerland 1992 • 1993 Work on EMV began • German Health Card 1993 • 1995 MasterCard Buys Mondex • First Combi Card 1997 • Mondex in Canada 1998 4 1984-1992 • France Banks elect to implement smart cards • Carte Bancaire develop chip application - B0’ • Merchants receive government incentives • Cardholders use PIN for both credit and debit • Domestic fraud down to 0.02% The World -

Smart Card Interfaces

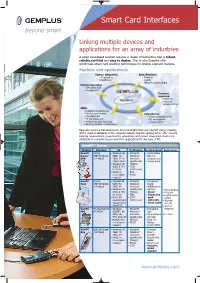

Smart Card Interfaces Linking multiple devices and applications for an array of industries A smart card-based solution requires a reader infrastructure that is robust, reliable,certified and easy to deploy. That is why Gemplus offer world-class smart card enabling technologies for diverse segment markets. Markets and applications System integrators: Bank/Retailers: • ID programs • Payment • Healthcare • Loyalty • Network access control Telecom operators: • SIM smart card management Transport operators: • Payment • Physical access control OEMs: • Keyboard manufacturers • Point of sale terminal Corporations: manufacturers • Physical access control • PC manufacturers • PC and network • Set-top box manufacturers access control • Vending machine manufacturers Easy and secure e-transactions are more important than ever. GemPC range, meeting all the required standards of the computer industry and the banking world, offer Telecom, banking organizations, governments, enterprises and system integrators smart card interfaces to complete secure electronic applications for any type of PC. GemPC™ Range Product Interface OS Certification Benefits & Options Applications GemPC RS232 • Windows 98, • Microsoft • Customizable Serial/ USB Full Speed 98SE, Me, Windows® • Slim line USB (12 Mbps) 2000, XP for Hardware compact case USB & Serial Quality Labs • Tamper proof • Windows 95 (WHQL) OSR2 & NT4 • CCID for Serial (USB mode) • MacOS X, • EMV Linux (upon • PC/SC request) GemPC RS232 • Windows 98, • Microsoft • Transparent Twin USB Full Speed 98SE, Me, Windows® -

Impact of E-Purse in Banking Sector

International Journal of Pure and Applied Mathematics Volume 118 No. 17 2018, 759-768 ISSN: 1311-8080 (printed version); ISSN: 1314-3395 (on-line version) url: http://www.ijpam.eu Special Issue ijpam.eu Impact of E-Purse in Banking Sector Ms. Sarmistha Saha 1 and Prof. G.P. Saradhi Varma 2 1Computer Science, Acharya Nagarjuna University Guntur, Andhra Pradesh , India . [email protected] 2Computer Science, S.R.K.R. Engineering College Bhimavaram, Andhra Pradesh , India . Abstract Technology is constantly improving and has limited shell life. The longer it takes to procure and develop a solution – the less useful the end results. Therefore it makes it all the more important bet on technologies which have exhibited robustness, scalability, support and easier inter-operability. E-purse is a type of smart card with an embedded microchip, provides multiple options, such as debit card or credit card type payments. In the era of progress in the information technology E-Purse is a great boon to us. This paper examines the capability and suitability of using e-purse in the banking sector. 759 International Journal of Pure and Applied Mathematics Special Issue Key Words and Phrases : Central Bank (ECB) , Points of Sale (PoS), Personal Identification Number(PIN) , Central European Purse Scheme(CEPS) 1 Introduction The recent developments across the globe in the payment systems arena, especially in e-commerce, have been marked by a gradual but steady trend towards electronic mode of payments as against the paper based payment instruments due to its convenience and ease of handling. European Central Bank (ECB) has broadly defined E- Money as an electronic store of monetary value on a technical device and used for making payments to undertakings other than the issuer without necessarily involving bank accounts in the transaction, but acting as a prepaid bearer instrument. -

030416 E-Commerce Payment

Electronic Payment Systems n To transfer money over the Internet n Methods of traditional payment E-Commerce Payment ¨Check, credit card, or cash n Methods of electronic payment ¨Electronic cash, software wallets, smart cards, Jane Hsu and credit/debit cards ¨Scrip is digital cash minted by third-party organizations The Vision of Electronic Payments The Reality of Electronic Payments The transition from atoms to bits is unstoppable The transition from atoms to bits is unstoppable, and irrevocable irrevocable but it will be slow and have limitations. -- Seasoned Banker - N. Negroponte n Checks are still around in the US – 60+ billion of them. n Computing, storage power and narrowband n Physical cards of any type are anachronisms. They will die a slow death much like checks. connectivity growing exponentially n Vested interests will slow the pace of change but will not n Science of networks is better understood be able to resist the winds of change. n Will a new phoenix emerge from the ashes of n Will a new player like eBay lead the change or will it be a large incumbent FI? History sides with the likes of eBay. the dotcom meltdown ? Requirements for e-payments Desirable Properties of Digital Money n Atomicity n Universally accepted n Transferable electronically ¨Money is not lost or created during a transfer n Divisible n Good atomicity n Non-forgeable, non-stealable ¨Money and good are exchanged atomically n Private (no one except parties know the amount) n Anonymous (no one can identify the payer) n Non-repudiation n Work off-line (no on-line verification needed) ¨No party can deny its role in the transaction ¨Digital signatures n No known system satisfies all. -

A Brief History of Payments

A Brief History of Payments October 2015 A Brief History of Payment Year Up to 1799 13th Century In Venice bills of exchange were developed as a legal device to allow international trade without the need to carry gold 14th Century First known reference to bills of exchange in English law as a means to carry funds abroad 17th Century Bills of exchange were being used for domestic as well as international payments. One of the earliest handwritten cheques known still to be in existence was drawn on Messrs Morris and Clayton, scriveners and bankers based in the City of London, and dated 16 February 1659. It was for £400 (about £43,000 today) made payable to a Mr Delboe and signed by Nicholas Vanacker . 1694 At the very first meeting of the Court of the Bank of England on 27 June 1694, it was decided that customers who deposited money would have the choice of three types of account. One of these allowed customers to draw notes on the Bank up to the extent of their deposits. 1727 The Royal Bank of Scotland invented the overdraft, one of the most important banking innovations. The bank allowed William Hog, a merchant, to take £1,000 - the equivalent of £63,664 today - more out of his account than 2015 Consulting Polymath he had in it. Source: Source: 1717 The Bank of England pioneered the use of printed forms, the first of which were produced in 1717 at Grocers’ Hall, London. The printed slips had scrollwork at the left-hand edge which could be cut through, leaving part on the cheque and part on the counterfoil – the real “check” – which is how the cheque got its name. -

Conditional Approval #220 December 1996

Comptroller of the Currency Administrator of National Banks Washington, DC 20219 Conditional Approval #220 December 2, 1996 December 1996 Mark J. Welshimer, Esquire Sullivan & Cromwell 125 Broad Street New York, N.Y. 10004-2498 Re: Notices of Wells Fargo Bank, N.A., Michigan National Bank, First National Bank of Chicago, and Texas Commerce Bank of Intent to Establish an Operating Subsidiary Pursuant to 12 C.F.R. § 5.34 to Become a Member of Limited Liability Companies Operating a Stored Value System - Application Control Nos. 96-WO-08-0012, -0013, -0025, and -0026 Dear Mr. Welshimer: This is in response to the operating subsidiary notices pursuant to 12 C.F.R. § 5.341, submitted on behalf of Wells Fargo Bank, N.A.(“Wells Fargo”), Michigan National Bank (“MNB”), First National Bank of Chicago, and Texas Commerce Bank, N.A. (collectively, the “Banks”), to establish operating subsidiaries to acquire membership interests in two Delaware limited liability companies (the “LLCs” or the “Companies”) that will operate a stored value card system known as “Mondex.” Each of the operating subsidiaries will be wholly owned by its parent Bank and will engage in no activities other than holding membership interests in the Companies. For the reasons discussed below, we approve, subject to certain conditions, the establishment of such operating subsidiaries by the Banks because we find that national banks may under 12 U.S.C. § 24(Seventh) engage in the business of developing and operating a stored value system. Please note that our response is solely directed to the question stated above. We do not address how other federal and state laws and regulations will or might apply to the Banks’ 1 The OCC recently amended its operating subsidiary rule , 12 C.F.R. -

Payment Systems in Canada, the Automated Clearing Settlement System (ACSS) and the Large Value Transfer System (LVTS)

Payment systems in Canada Canada Table of contents List of abbreviations ............................................................................................................................... 35 Introduction ............................................................................................................................................ 37 1. Institutional aspects ..................................................................................................................... 38 1.1 The general institutional framework .................................................................................. 38 1.1.1 The legal and regulatory framework ....................................................................... 38 1.1.2 Financial intermediaries providing payment services.............................................. 40 1.2 The role of the central bank .............................................................................................. 44 1.2.1 Operational roles..................................................................................................... 44 1.2.2 Oversight................................................................................................................. 45 1.3 The role of other private and public bodies ....................................................................... 46 1.3.1 Ministry of Finance .................................................................................................. 46 1.3.2 The Canadian Payments Association (CPA) ......................................................... -

Moving Money 2025 Report

Moving Money 2025 The future of payments and what it means to you Expert opinions on innovation in the UK PAGE 1 MOVING MONEY 2025 MOVING MONEY 2025 PAGE 2 Foreword Payments are an essential part of our lives and there the UK economy. As well as boosting payments efficiency, has never been a greater choice of ways to pay. Almost this technology is driving payments innovation throughout everyone in the UK makes several payments each day and financial services and beyond. New mobile payment services electronic payments have recently overtaken cash as the such as Paym and Zapp are firmly rooted in VocaLink’s real- most popular payment method. In 2014, the average total time technology, as are many other payment innovations. number of transactions per person processed by VocaLink was 196, with an average of 57 Direct Debits throughout In practical terms, a real-time payments system is the bridge the year. between the digital economy and the real economy. With the growth of mobile, people expect to be able to make But making a payment is seldom an end in itself. It is payments while they are on the go. This is reflected in the invariably part of a bigger transaction, for example paying exponential growth of new payment services and mobile for groceries, transferring money to friends or making phone apps that promise to make payment easier than ever. a charitable donation. Making a payment is a means to So what about the future? an end, because all transactions end with a payment. Most people simply want to make and receive payments The global payments industry is in a state of constant flux conveniently, securely and with certainty. -

M/Chip 4 for MULTOS Application Security Target Summary

Proprietary M/Chip 4 for MULTOS Application Security Target Summary Document Number mxi-mchip-stg-005 Version 1-0 Released date 11 Jul 2003 Archived by: ____________________________________ Date: __________ Copyright 2003 Mondex International Limited Proprietary Copyright Copyright 2003 Mondex International Limited. This document is confidential. No part of this document may be reproduced, published or disclosed in whole or part, by any means: mechanical, electronic, photocopying, recording or otherwise without the prior written permission of Mondex International Ltd. This document is made available under the terms of the confidentiality agreement signed with Mondex International Ltd. and must not be disclosed to any other person or organisation otherwise than as set out in the terms of that confidentiality agreement. History Version Date Change Notes Author 0-1 27 Jun 2003 First release, based on mxi-mchip-stg-003 v4-1 J Tierney 1-0 11 Jul 2003 Minor updates following formal review. J Tierney ii mxi-mchip-stg-005 v1-0 2003 Mondex International Limited Proprietary Preface Objectives The objective of this document is to summarise the security target for the Common Criteria Evaluation of the M/Chip 4 for MULTOS Application. Scope • This Security Target summary is limited to the M/Chip 4 for MULTOS application (version 1.0.1.1) only. • This Security Target summary does not cover chip embedding, MULTOS enablement or M/Chip 4 for MULTOS application loading (which includes customisation and personalisation) prior to delivery to the end-user. Key load is included in the application load process and hence is outside the scope of the evaluation, as is the platform upon which the application will run.