Study on the Implementation of Recommendation 97/489/EC

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Mobile Banking

Automated teller machine "Cash machine" Smaller indoor ATMs dispense money inside convenience stores and other busy areas, such as this off-premise Wincor Nixdorf mono-function ATM in Sweden. An automated teller machine (ATM) is a computerized telecommunications device that provides the customers of a financial institution with access to financial transactions in a public space without the need for a human clerk or bank teller. On most modern ATMs, the customer is identified by inserting a plastic ATM card with a magnetic stripe or a plastic smartcard with a chip, that contains a unique card number and some security information, such as an expiration date or CVVC (CVV). Security is provided by the customer entering a personal identification number (PIN). Using an ATM, customers can access their bank accounts in order to make cash withdrawals (or credit card cash advances) and check their account balances as well as purchasing mobile cell phone prepaid credit. ATMs are known by various other names including automated transaction machine,[1] automated banking machine, money machine, bank machine, cash machine, hole-in-the-wall, cashpoint, Bancomat (in various countries in Europe and Russia), Multibanco (after a registered trade mark, in Portugal), and Any Time Money (in India). Contents • 1 History • 2 Location • 3 Financial networks • 4 Global use • 5 Hardware • 6 Software • 7 Security o 7.1 Physical o 7.2 Transactional secrecy and integrity o 7.3 Customer identity integrity o 7.4 Device operation integrity o 7.5 Customer security o 7.6 Alternative uses • 8 Reliability • 9 Fraud 1 o 9.1 Card fraud • 10 Related devices • 11 See also • 12 References • 13 Books • 14 External links History An old Nixdorf ATM British actor Reg Varney using the world's first ATM in 1967, located at a branch of Barclays Bank, Enfield. -

Electronic Cash in Hong Kong

1 Focus THEME ity of users to lock their cards. Early in 1992, NatWest began a trial of Mondex in BY I. CHRISTOPHERWESTLAND. MANDY KWOK, ]OSEPHINESHU, TERENCEKWOK AND HENRYHO, HONG KONG an office complex in London with a 'can- UNIVERSITYOF SCIENCE&TECHNOLOGY. HONG KONG * teen card' known as Byte. The Byte trial is still continuing with more than 5,000 INTRODUCTION I teller cash for a card and uses it until that people using the card in two office res- Asian business has long had a fondness value is exhausted. Visa plans to offer a taurants and six shops. By December of for cash. While the West gravitated toward reloadable card later. 1993, the Mondex card was introduced on purchases on credit - through cards or a large scale. Sourcing for Mondex sys- installments - Asia maintained its passion HISTORY tem components involves more than 450 for the tangible. Four-fifths of all trans- Mondex was the brainchild of two NatWest manufacturers in over 40 countries. In actions in Hong Kong are handled with bankers - Tim Jones and Graham Higgins. October of 1994, franchise rights were sold cash. It is into this environment that They began technology development in to the Hong Kong and Shanghai Banking Mondex International, the London based 1990 with electronics manufacturers in the Corporation Limited to cover the Asian purveyor of electronic smart cards, and UK, USA and Japan. Subsequent market region including Hong Kong, China, In- Visa International, the credit card giant, research with 47 consumer focus groups dia, Indonesia, Macau, Philippines, are currently competing for banks, con- in the US, France, Germany, Japan, Hong Singapore and Thailand. -

Rabobank Nederland Coo¨ Peratieve Centrale Raiffeisen-Boerenleenbank B.A

Base Prospectus Rabobank Nederland Coo¨ peratieve Centrale Raiffeisen-Boerenleenbank B.A. (a cooperative (coo¨peratie) formed under the laws of the Netherlands with its statutory seat in Amsterdam) Coo¨ peratieve Centrale Raiffeisen-Boerenleenbank B.A. (Rabobank Nederland) Australia Branch (Australian Business Number 70 003 917 655) (a cooperative (coo¨peratie) formed under the laws of the Netherlands with its statutory seat in Amsterdam) Coo¨ peratieve Centrale Raiffeisen-Boerenleenbank B.A. (Rabobank Nederland) Singapore Branch (Singapore Company Registration Number S86FC3634A) (a cooperative (coo¨peratie) formed under the laws of the Netherlands with its statutory seat in Amsterdam) EUR 160,000,000,000 Global Medium-Term Note Programme Due from seven days to perpetuity Under the Global Medium-Term Note Programme described in this Base Prospectus (the ‘‘Programme’’), Coo¨peratieve Centrale Raiffeisen-Boerenleenbank B.A. (Rabobank Nederland) (‘‘Rabobank Nederland’’, the ‘‘Bank’’ or the ‘‘Issuer’’), may through its head office or through its branches listed above, subject to compliance with all relevant laws, regulations and directives, from time to time issue Global Medium-Term Notes (the ‘‘Notes’’). References herein to the ‘‘Issuer’’ shall mean Rabobank Nederland, whether issuing Notes through its head office or through its branches listed above. The branches through which Rabobank Nederland may issue Notes are Coo¨peratieve Centrale Raiffeisen-Boerenleenbank B.A. (Rabobank Nederland) Australia Branch (‘‘Rabobank Australia Branch’’) and -

F. Van Lanschot Bankiers N.V. Credit Update

F. van Lanschot Bankiers N.V. Credit Update May 2013 Content Profile of Van Lanschot 2012 annual results and Q1 2013 trading update Funding and liquidity 1 1 Executive summary Profile of Van Lanschot Key financials Who•The weoldest are independent bank in the Netherlands with Q1 2013 FY 2012 history dating back more than 275 years Core Tier 1 ratio (%) 11.9% 11.0% •A relationship-oriented bank, with genuine personal Funding ratio (%) 83.1% 84.4% attention, whereby the interests of the client really do What we do Leverage ratio (%) 7.4% 7.5% come first Client assets (€) 53.0 billion 52.3 billion •Local visibility with 34 offices and client meeting centres Underlying profit (€) 26.3 million 2 million in the Netherlands, Belgium and Switzerland What sets us apart Strategy Financial targets 2017 •Our objective is to preserve and create wealth for clients Core Tier I ratio > 15% •We choose to be a pure-play, independent wealth manager Return on Core Tier I equity of 10-12% •We strongly believe that wealth management offers attractive growth opportunities and that we have inherent Cost-income ratio of 60-65% and distinctive strengths •Private banking, asset management and merchant 2 banking are the areas in which we excel 2 Evolution into an independent Private Bank 1737 2013 1737 29-6-1999 30-9-2004 1-1-2007 14-05-2013 Established as Listed on Acquisition Acquisition Strategic Review: a trading Euronext CenE Bankiers Kempen & Co focus on private house in Amsterdam banking, asset ‘s-Hertogenbosch management and merchant banking • Our objective -

Pdf, Last Accessed on Oc- Tober 24, 2019

A Service of Leibniz-Informationszentrum econstor Wirtschaft Leibniz Information Centre Make Your Publications Visible. zbw for Economics Hellwig, Michael; Laser, Falk Hendrik Working Paper Bank mergers in the financial crisis: A competition policy perspective ZEW Discussion Papers, No. 19-047 Provided in Cooperation with: ZEW - Leibniz Centre for European Economic Research Suggested Citation: Hellwig, Michael; Laser, Falk Hendrik (2019) : Bank mergers in the financial crisis: A competition policy perspective, ZEW Discussion Papers, No. 19-047, ZEW - Leibniz- Zentrum für Europäische Wirtschaftsforschung, Mannheim This Version is available at: http://hdl.handle.net/10419/206418 Standard-Nutzungsbedingungen: Terms of use: Die Dokumente auf EconStor dürfen zu eigenen wissenschaftlichen Documents in EconStor may be saved and copied for your Zwecken und zum Privatgebrauch gespeichert und kopiert werden. personal and scholarly purposes. Sie dürfen die Dokumente nicht für öffentliche oder kommerzielle You are not to copy documents for public or commercial Zwecke vervielfältigen, öffentlich ausstellen, öffentlich zugänglich purposes, to exhibit the documents publicly, to make them machen, vertreiben oder anderweitig nutzen. publicly available on the internet, or to distribute or otherwise use the documents in public. Sofern die Verfasser die Dokumente unter Open-Content-Lizenzen (insbesondere CC-Lizenzen) zur Verfügung gestellt haben sollten, If the documents have been made available under an Open gelten abweichend von diesen Nutzungsbedingungen -

Information Technology in the Banking and Financial Sectors

INFORMATION TECHNOLOGY IN THE BANKING AND FINANCIAL SECTORS MARCH 25, 1996 BACKGROUND BREIFING PAPER OF THE TELECOMMUNICATIONS INFOTECHNOLOGY FORUM (please attribute any quotation) Information Technology in the Banking and Financial Services Sector Smartcards, banks and telephones A brief historical introduction; what this suggests about the future Banks first started using computers linked to telecommunications systems in a big way in the 1970s and 1980s, when local area networks allowed them to start automating accounts—and thus to introduce automatic teller machines (ATMs) which customers could use to find out how much money was in their accounts and make cash withdrawals. ATMs appeared to offer two things: — A competitive advantage: better service for customers. — Savings on staff costs, as tellers were replaced with machines. The first of these is undoubtedly true. A network of ATMs operating 24 hours a day takes the necessity out of planning when to get money for individuals—it is hard to imagine anyone accepting a bank without an ATM network for their day-to-day financial needs (though judging by the queues in some banks, some people do not seem to have realised quite what can be done with an ATM card). The second, however, has not really happened, at least in the way it was originally imagined. What has happened is that on the one hand staff have been freed up for other things—such as handling the huge array of financial services banks now offer compared with a couple of decades ago—and on the other IT has taken on a life of its own as banks think of new ways to wire themselves and their customers. -

MJ Bijlsma CM Van Den Broek JFG Bruggert E

The following staff of NMa contributed to the realisation of this document: M.J. Bijlsma C.M. van den Broek J.F.G. Bruggert E.J.R. Droste M. Gerritsen W. Meester I.S. Nobel M.M. Oijevaar C. Wolfsen C.J. Zonderland The contents of this publication closed on 1 October 2005. Developments after this date could therefore no longer be included in the texts. 1 Contents Foreword 4 1 The Financial Sector Monitor in 2005 6 1.1 Introduction 6 1.2 Activities of FSM in 2005 6 1.3 Success factors 8 1.4 Structure 9 1.5 Market developments in 2005 10 2 Competition between insurance brokers 15 2.1 Introduction 15 2.2 Responses to the consultation document 15 2.3 Survey 16 2.4 Analysis of consumer choice 20 2.5 Conclusions 24 3 Effects of the transfer of PIN contracts 26 3.1 Introduction 26 3.2 Outcomes of the research by NIPO/ECORYS-NEI 27 3.3 Outcomes of FSM's research into tariffs 29 3.4 Conclusions 30 4 Entry and exit of banks 32 4.1 Introduction 32 4.2 Registrations and deregistration under the Credit System (Supervision) Act 32 4.2.1 Breakdown according to the type of institution 34 4.2.2 Registrations and Deregistrations of Dutch commercial banks according to their background 36 4.3 Entries and exits 37 4.4 Conclusions 38 5 The geographical dimension of the health insurance market 39 5.1 Introduction 39 5.2 The healthcare market 40 5.3 Relevant geographical dimension 42 5.4 Dynamic factors 44 5.4.1 Regional mechanism 44 5.4.2 Counteracting factors 47 5.4.3 Empirical research 49 5.5 Conclusions 52 6 Interbank charges: economic theory and international -

Van Lanschot Kempen

Van Lanschot Credit Update SEPTEMBER 2012 - Profile of Van Lanschot - 2012 half-year results - putting solidity before profit - The best Private Bank in the Netherlands and Belgium - Funding and liquidity 1 Evolution into an independent Private Bank 1737 2012 1737 29-6-1999 30-9-2004 2006 1-1-2007 30-11-2007 2012 Established as Listed on Acquisition Strategy to be the Acquisition Sale of 51% of Sale of Van Lanschot a trading Euronext CenE Bankiers best Private Bank Kempen & Co insurance arm Curacao and trust house in Amsterdam in the Netherlands to De Goudse activities ‘s-Hertogenbosch and Belgium Van Lanschot aims to be the best Private Bank in the Netherlands and Belgium • Van Lanschot’s strategy is focused on offering high quality financial services • Van Lanschot has a solid capital base, strong funding and liquidity position • Van Lanschot has offices in the Netherlands and Belgium and also has a presence in Switzerland (Zurich and Geneva), Edinburgh and New York 2 Van Lanschot: a local and authentic bank • Widespread presence in the Netherlands and Belgium • Around 15% market share in the Private Banking market making it the number 2 player in the Netherlands and Belgium • Almost 2,000 employees • International Private Banking concentrated in Switzerland • Target client groups: - wealthy individuals - entrepreneurs and their businesses - business professionals and executives - charitable associations - institutional investors 3 Van Lanschot is unique compared with other banks Predominantly retail banking Extensive branch network -

What Is a Chip Card?

The Technology Is Ready Philip Andreae Philip Andreae & Associates Why are you Here • The globe is in migration to EMV • June 2003: Visa Canada announced its plans to migrate to chip • January 8, CTV W-5 documented the reality of debit card fraud • October 2005: Interac issued schedule for chip • American Express, MasterCard and JCB are ready to support the Canadian migration to chip The Time Has Come 2 What is a Chip Card? • A plastic credit card with an embedded computer chip containing a microcomputer –1976 a calculator in your card –Today the power of 1981 IBM PC –Tomorrow integrated with your body, PDA and Cell Phone? 3 History of Chip Cards a.k.a the Smart Card • 1968 German Inventors, • French Banks Jurgen Dethloff & Helmet Specifications 1977 Grotrupp German patent use of • Honeywell Bull plastic as a carrier for Microchips Produce First Cards 1978 • 1970 Japanese Inventor, • Payphone Cards 1983 Kunitake Arimura applied for • French Banking similar patent Pilot Begins 1984 • 1974 French Inventor, Roland • Used in TV 1990 Moreno patented the Smart Card • ETSI GSM SIM 1991 • 1978 Honeywell Bull proves • First ePurse in miniaturization of electronics Bulle, Switzerland 1992 • 1993 Work on EMV began • German Health Card 1993 • 1995 MasterCard Buys Mondex • First Combi Card 1997 • Mondex in Canada 1998 4 1984-1992 • France Banks elect to implement smart cards • Carte Bancaire develop chip application - B0’ • Merchants receive government incentives • Cardholders use PIN for both credit and debit • Domestic fraud down to 0.02% The World -

Friesland Bank N.V. € 5,000,000,000

This document constitutes the base prospectus of Friesland Bank N.V. in respect of non-equity securities within the meaning of article 22 No. 6 (4) of the Commission Regulation (EC) No. 809/2004 of 29 April 2004 (the "Base Prospectus"). PROSPECTUS DATED 9 JULY 2010 Base Prospectus FRIESLAND BANK N.V. (incorporated under the laws of the Netherlands with limited liability and having its corporate seat in Leeuwarden) € 5,000,000,000 Debt Issuance Programme ___________________________________ Under its € 5,000,000,000 Debt Issuance Programme (the "Programme") Friesland Bank N.V. (the "Issuer", or "Friesland Bank" and such expression, except where the context does not permit, shall include Friesland Bank N.V. and its consolidated subsidiaries), may from time to time issue notes (the "Notes") denominated in any currency agreed between the Issuer and the relevant Dealer (as defined below), if any. Subject as set out herein, the maximum aggregate nominal amount of the Notes from time to time outstanding under the Programme will not exceed € 5,000,000,000 (or its equivalent in other currencies calculated as described herein). The Notes may be issued on a continuing basis to one or more of the Dealers specified under "Key Features of the Programme – Dealers in respect of the Notes" and any additional Dealer appointed in respect of Notes under the Programme from time to time, which appointment may be for a specific issue or on an ongoing basis (each a "Dealer" and together the "Dealers"). Notes may be distributed by way of a public offer or private placements and, in each case, on a syndicated or non-syndicated basis. -

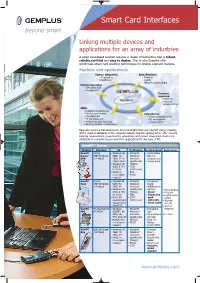

Smart Card Interfaces

Smart Card Interfaces Linking multiple devices and applications for an array of industries A smart card-based solution requires a reader infrastructure that is robust, reliable,certified and easy to deploy. That is why Gemplus offer world-class smart card enabling technologies for diverse segment markets. Markets and applications System integrators: Bank/Retailers: • ID programs • Payment • Healthcare • Loyalty • Network access control Telecom operators: • SIM smart card management Transport operators: • Payment • Physical access control OEMs: • Keyboard manufacturers • Point of sale terminal Corporations: manufacturers • Physical access control • PC manufacturers • PC and network • Set-top box manufacturers access control • Vending machine manufacturers Easy and secure e-transactions are more important than ever. GemPC range, meeting all the required standards of the computer industry and the banking world, offer Telecom, banking organizations, governments, enterprises and system integrators smart card interfaces to complete secure electronic applications for any type of PC. GemPC™ Range Product Interface OS Certification Benefits & Options Applications GemPC RS232 • Windows 98, • Microsoft • Customizable Serial/ USB Full Speed 98SE, Me, Windows® • Slim line USB (12 Mbps) 2000, XP for Hardware compact case USB & Serial Quality Labs • Tamper proof • Windows 95 (WHQL) OSR2 & NT4 • CCID for Serial (USB mode) • MacOS X, • EMV Linux (upon • PC/SC request) GemPC RS232 • Windows 98, • Microsoft • Transparent Twin USB Full Speed 98SE, Me, Windows® -

Impact of E-Purse in Banking Sector

International Journal of Pure and Applied Mathematics Volume 118 No. 17 2018, 759-768 ISSN: 1311-8080 (printed version); ISSN: 1314-3395 (on-line version) url: http://www.ijpam.eu Special Issue ijpam.eu Impact of E-Purse in Banking Sector Ms. Sarmistha Saha 1 and Prof. G.P. Saradhi Varma 2 1Computer Science, Acharya Nagarjuna University Guntur, Andhra Pradesh , India . [email protected] 2Computer Science, S.R.K.R. Engineering College Bhimavaram, Andhra Pradesh , India . Abstract Technology is constantly improving and has limited shell life. The longer it takes to procure and develop a solution – the less useful the end results. Therefore it makes it all the more important bet on technologies which have exhibited robustness, scalability, support and easier inter-operability. E-purse is a type of smart card with an embedded microchip, provides multiple options, such as debit card or credit card type payments. In the era of progress in the information technology E-Purse is a great boon to us. This paper examines the capability and suitability of using e-purse in the banking sector. 759 International Journal of Pure and Applied Mathematics Special Issue Key Words and Phrases : Central Bank (ECB) , Points of Sale (PoS), Personal Identification Number(PIN) , Central European Purse Scheme(CEPS) 1 Introduction The recent developments across the globe in the payment systems arena, especially in e-commerce, have been marked by a gradual but steady trend towards electronic mode of payments as against the paper based payment instruments due to its convenience and ease of handling. European Central Bank (ECB) has broadly defined E- Money as an electronic store of monetary value on a technical device and used for making payments to undertakings other than the issuer without necessarily involving bank accounts in the transaction, but acting as a prepaid bearer instrument.