10 SEPTEMBER 2010, the BREWERY, LONDON Enter Online

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

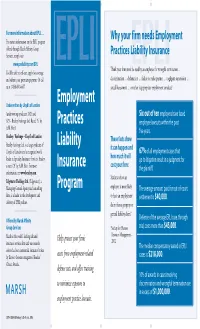

Employment Practices Liability Insurance Program EPLI

B5848_EPLI 2/14/06 2:49 PM Page 1 For more information about EPLI … Why your firm needs Employment For instant information on the EPLI program offered through Marsh Affinity Group Services, simply visit Practices Liability Insurance www.proliablity.com/EPLI Think your firm won’t be sued by an employee for wrongful termination … You’ll be able to self-rate, apply for coverage EPLI EPLI and submit your premium payment. Or call discrimination … defamation … failure to make partner … negligent supervision … us at 1-888-601-6667. sexual harassment … or other inappropriate employment conduct? Underwritten by Lloyd’s of London Employment (underwriting syndicates 2623 and Six out of ten employers have faced 623 – Beazley Furlonge Ltd. Rated “A” by Practices employee lawsuits within the past A.M. Best) five years. Beazley / Furlonge – Lloyd’s of London These facts show Beazley Furlonge Ltd. is a large syndicate of Liability it can happen and Lloyd’s of London and a recognized world 67% of all employment cases that leader in Specialty Insurance Services. Beazley how much it will go to litigation result in a judgment for is rated “A” by A.M. Best. For more Insurance cost your firm: the plaintiff. information, see www.beazley.com. Statistics show an Edgewater Holdings Ltd. (Edgewater), a Managing General Agency and consulting Program employer is more likely The average amount paid for out-of-court firm, is a leader in the development and to have an employment settlement is $40,000. delivery of EPLI policies. claim than a property or general liability claim.* Offered by Marsh Affinity Defense of the average EPLI case, through Group Services *Society for Human trial, costs more than $45,000. -

Consumers Guide to Auto Insurance

CONSUMERS GUIDE TO AUTO INSURANCE PRESENTED TO YOU BY THE DEPARTMENT OF BUSINESS REGULATION INSURANCE DIVISION 1511 PONTIAC AVENUE, BLDG 69-2 CRANSTON, RI 02920 TELEPHONE 401-462-9520 www.dbr.ri.gov Elizabeth Kelleher Dwyer Superintendent of Insurance TABLE OF CONTENTS Introduction………………………………………………………………1 Underwriting and Rating………………………………………………...1 What is meant by underwriting and how is it accomplished…………..1 How are rates and premium charges determined in Rhode Island……1 What factors are considered in ratemaking……………………………. 2 What discounts are used in determining final premium cost…………..3 Rhode Island Automobile Insurance Plan…………………..…………..4 Regulation of Rates……………………………………………………….4 The Tort System…………………………………………………………..4 Liability Coverages………………………………………………………..5 Coverages Other Than Liability…………………………………………5 Physical Damage to the Automobile……………………………………..6 Other Optional Coverages………………………………………………..6 The No-Fault System……………….……………………………………..7 Smart Shopping……………………………………………………………7 Shop for True Comparison………………………………………………..8 Consumer Protection Available...…………………………………………8 What to Do if You are in an Automobile Accident………………………9 Your State Insurance Department………………………………….........9 Auto Insurance Buyer’s Worksheet…………………………………….10 Introduction Auto insurance is an expensive purchase for most Americans, and is especially expensive for Rhode Islanders. Yet consumers rarely comparison-shop for auto insurance as they might for other products and services. Auto insurance companies vary substantially both in price and service to policyholders, so it pays to shop around and compare different insurance companies. This guide to buying auto insurance was developed to help you become a more knowledgeable policyholder and to get the combination of price and service best suited to your needs. It provides information on how to shop for coverage and how insurance premiums are determined. You will also find an Auto Insurance Buyer’s Worksheet in the guide to help you compare premium prices among insurers. -

Tax Risk Insurance: Taking It Captive

taxnotes federal ■ Volume 171, Number 4 April 26, 2021 Tax Risk Insurance: Taking It Captive by Ken Brewer and Albert Liguori Reprinted from Tax Notes Federal, April 26, 2021, p. 549 For more Tax Notes content, please visit www.taxnotes.com. © 2021 Tax Analysts. All rights reserved. Analysts does not claim copyright in any public domain or third party content. TAX PRACTICE tax notes federal Tax Risk Insurance: Taking It Captive by Ken Brewer and Albert Liguori is to explore the U.S. tax implications of that meeting. Behold: captive tax risk insurance!3 In our experiences, the use of tax risk insurance has been most prevalent in the mergers and acquisitions context. But as we mentioned in our last article, we have seen it becoming more common in the context of large corporate groups seeking to manage their global tax risks, regardless of whether they are related to M&A.4 In either context, the use of tax risk insurance lends itself to captive arrangements, for the same reasons that have caused captive arrangements to be desirable for other types of insurance risks. Ken Brewer is a senior adviser and Captive Insurance and the U.S. Tax Implications international tax practitioner with Alvarez & Thereof Marsal Taxand LLC in Miami, and Albert Liguori is a managing director in the firm’s New As an alternative to traditional insurance York office. The authors send special thanks to protection, which is obtained from one or more of Brian Pedersen, managing director at Alvarez & the many underwriters offering that coverage to Marsal Taxand, for his contributions and the public, captive insurance is obtained from a review. -

Auto Insurance and How Those Terms Affect Your Coverage

Arkansas Insurance Department AUTOMOBILE INSURANCE Asa Hutchinson Allen Kerr Governor Commissioner A Message From The Commissioner The Arkansas Insurance Department takes very seriously its mission of “consumer protection.” We believe part of that mission is accomplished when consumers are equipped to make informed decisions. We believe informed decisions are made through the accumulation and evaluation of relevant information. This booklet is designed to provide basic information about automobile insurance. Its purpose is to help you understand terms used in the purchase of auto insurance and how those terms affect your coverage. If you have questions or need additional information, please contact our Consumer Services Division at: Phone: (501) 371-2640; 1-800-852-5494 Fax: (501) 371-2749 Email: [email protected] Web site: www.insurance.arkansas.gov Mission Statement The primary mission of the State Insurance Department shall be consumer protection through insurer insolvency and market conduct regulation, and fraud prosecution and deterrence. 1 Coverages Provided by Automobile Insurance The automobile insurance policy is comprised of several separate types of coverages: COLLISION, COMPREHENSIVE, LIABILITY, PERSONAL INJURY PROTECTION, UNINSURED MOTORIST, UNDERINSURED MOTORIST and other coverages. You are required by law to purchase liability protection only. All others are voluntary unless required by a lienholder. LIABILITY Under Legislation passed in 1987 and 1999, it is unlawful for any person to operate a motor vehicle within this state unless the vehicle is insured with the minimum amount of liability coverage: $25,000 for bodily injury or death of one person in any one accident; $50,000 for bodily injury or death of two or more persons in any one accident and $25,000 for damage to or destruction of the property of others. -

Description Holding Book Cost Market Price Market Value £000'S £000'S

DORSET COUNTY PENSION FUND VALUATION OF PORTFOLIO AT CLOSE OF BUSINESS 31 March 2017 Book Market Description Holding Market Value Cost Price £000's £000's UK EQUITIES MINING ACACIA MINING 33,000 147.93 4.502 148.57 ANGLO AMERICAN ORD USD0.54 270,390 2,804.18 12.27 3,317.69 ANTOFAGASTA ORD GBP0.05 74,500 151.50 8.355 622.45 BHP BILLITON ORD USD0.50 436,926 2,401.54 12.395 5,415.70 CENTAMIN EGYPT LTD 226,000 349.07 1.732 391.43 FRESNILLO 35,500 88.20 15.52 550.96 GLENCORE XSTRATA 2,412,543 5,662.91 3.141 7,577.80 HOCHSCHILD MINING ORD GBP0.25 49,000 108.90 2.765 135.49 KAZ MINERALS 53,600 89.80 4.551 243.93 PETRA DIAMONDS 106,900 169.67 1.329 142.07 POLYMETAL INT'L 53,800 514.30 9.945 535.04 RANDGOLD RESOURCES ORD USD0.05 19,250 485.32 69.7 1,341.73 RIO TINTO ORD GBP0.10 (REG) 250,150 2,876.49 32.185 8,051.08 VEDANTA RESOURCES ORD USD0.10 18,500 75.07 8.11 150.04 Total MINING 15,924.89 28,524.69 OIL & GAS PRODUCERS AFREN PLC 218,000 215.93 0 0.00 BP ORD USD0.25 3,948,100 13,177.95 4.5885 18,115.86 CAIRN ENERGY ORD GBP0.06153846153 119,207 236.32 2.048 244.14 NOSTRUM OIL & GAS 17,700 84.36 4.796 84.89 ROYAL DUTCH 'B' ORD EUR0.07 1,642,961 20,190.09 21.945 36,054.78 TULLOW OIL ORD GBP 0.10 188,500 789.92 1.99026 375.16 Total OIL & GAS PRODUCERS 34,694.58 54,658.45 CHEMICALS CRODA INTL ORD GBP0.10 26,995 211.15 35.77 965.61 ELEMENTIS 99,000 130.23 2.899 287.00 JOHNSON MATTHEY ORD GBP1.00 40,357 446.31 30.82 1,243.80 SYNTHOMER 57,665 118.87 4.751 273.97 VICTREX ORD GBP0.01 17,000 111.61 19.02 323.34 Total CHEMICALS 1,018.16 3,087.91 CONSTRUCTION -

Review of Narrative Reporting by UK Listed Companies: Key Findings

Rising to the challenge. A review of narrative reporting by UK listed companies The Accounting Standards Board The Accounting Standards Board (ASB) is an operating body of the Financial Reporting Council (FRC). The FRC is the UK’s independent regulator responsible for promoting confi dence in corporate reporting and governance. For corporate reporting, the outcome we seek is this: Corporate reports contain information which is relevant, reliable, understandable and comparable, and are useful for decision-making, including stewardship decisions. For further information visit www.frc.org.uk/asb Why did we write this report? The Accounting Standards Board (ASB), an operating body of the Financial Reporting Council Preparing a good (FRC), fi rst undertook a review of narrative reporting “quality annual report in 2006. The review concluded that certain areas that communicates effectively all the of reporting were a challenge for companies. Since important information then, further content requirements have come into is a major force for quoted companies in the form of the intellectual and enhanced business review requirements in the logistical challenge. Companies Act 2006 (CA), prompting us to take another look. ” Preparing a good quality annual report that communicates effectively all the important information is a major intellectual and logistical challenge. Many companies continue to devote signifi cant time and effort to improving their narrative reporting, but there are always opportunities for further enhancement as experience and best practice develop. We hope this report will be helpful to companies looking to rise to this challenge. We also have some internal goals as well. As the ASB is responsible for the UK best practice narrative reporting guidance in its Reporting Statement: Operating and Financial Review (RS), it is useful to continue to monitor the effects of the statement on current practice. -

Aberforth Smaller Companies Trust Plc

Aberforth Smaller Companies Trust plc Annual Report and Accounts 31 December 2007 INVESTMENT OBJECTIVE ‘‘The investment objective of Aberforth Smaller Companies Trust plc (ASCoT) is to achieve a net asset value total return (with dividends reinvested) greater than on the Hoare Govett Smaller Companies Index (Excluding Investment Companies) over the long term.’’ CONTENTS Financial Highlights 1 Ten Year Investment Record 2 Company Summary 3 Chairman’s Statement 4 Directors and Corporate Information 7 Aberforth Partners LLP – Information 8 Managers’ Report 9 Portfolio Information 14 Thirty Largest Investments 16 List of Investments 17 Long-Term Record 20 Directors’ Report 22 Corporate Governance Report 28 Directors’ Remuneration Report 32 Directors’ Responsibility Statement 34 Independent Auditors’ Report 34 Income Statement 36 Reconciliation of Movements in Shareholders’ Funds 37 Balance Sheet 38 Cash Flow Statement 39 Notes to the Accounts 40 Shareholder Information 50 Notice of the Annual General Meeting 52 THIS DOCUMENT IS IMPORTANT AND REQUIRES YOUR IMMEDIATE ATTENTION. If you are in any doubt as to the action you should take you should consult your stockbroker, bank manager, solicitor, accountant or other independent ¢nancial adviser authorised under the Financial Services and Markets Act 2000 immediately. If you have sold or otherwise transferred all of your ordinary shares in Aberforth Smaller Companies Trust plc, please forward this document and the accompanying form of proxy as soon as possible to the purchaser or transferee or to the stockbroker, bank or other agent through whom the sale or transfer was or is being effected for delivery to the purchaser or transferee. FINANCIAL HIGHLIGHTS Year to 31 December 2007 ASCoT Net Asset Value (total return) –10.4% Hoare Govett Smaller Companies Index (Excl. -

Coronavirus Insurance Coverage and Claims Guidance

Coronavirus Insurance Coverage and Claims Guidance April 15, 2020 With the exposure of the coronavirus (COVID-19) increasing, organizations are evaluating the potential coverage which may be triggered from their insurance policies. Actual loss situations and a review of individual policy forms will be a crucial step to properly evaluate potential available coverage application. Insurance carriers have the ultimate authority in determining coverage for presented claims. Any suspected COVID-19 related losses should be reported per the policy guidelines. Policyholders should be aware that some policies may require specific time frames from notice of potential claim, such as 48 hours. This document provides factors that will be examined in the event losses related to COVID-19 occur. Coronavirus Insurance Coverage and 2 Lockton Companies Claims Guidance Workers’ compensation Each injured employee situation will be evaluated on its own individual merits. Workers’ compensation insurance covers employees who suffer injury or illness “arising out of or in the course of their employment.” Many factors will need to be considered if presented COVID-19-type claims are work related. These include but are not limited to: • The timing of when the loss occurs: were there reports of previously infected individuals made in this same time period? • The location(s) where the injured worker was present leading up the injury or exposure: was the injured worker within an area where exposure of the virus was present or carried a greater risk? • The activities the injured worker was engaged in leading up to when the loss or exposure took place: was the individual in contact with others or working remotely? • The specific nature of the loss: what further details can be uncovered to provide greater clarity around exposure to the virus as an occupational disease? In most jurisdictions, individuals seeking benefits under workers’ compensation will also need to meet the burden that the coronavirus illness arose out of, or was caused by, conditions “peculiar” to the work. -

Captive Insurance Companies

Estate Planning – August 2011 CAPTIVE INSURANCE COMPANIES Possibilities and Pitfalls With Captive Insurance Companies Profitable family businesses can use captive insurance companies to manage business risk and shift wealth accumulated in a profitable captive from senior to junior generations thereby avoiding inclusion of those funds in the senior generation's estates. Author: KIMBERLY S. BUNTING, J. SCOT KIRKPATRICK, AND KAREN S. KURTZ, ATTORNEYS KIMBERLY S. BUNTING is a shareholder in Chamberlain, Hrdlicka, White, Williams & Martin LLP's Atlanta, Georgia, office. She practices in the areas of commercial and corporate law, and has significant experience with risk management and captive insurance companies. J. SCOT KIRKPATRICK is also a shareholder in Chamberlain, Hrdlicka's Atlanta office. His practice focuses principally on estate and income tax planning for high net worth individuals and their businesses. KAREN S. KURTZ is an associate in the Tax Section of Chamberlain Hrdlicka's Atlanta office, concentrating in estate and gift tax planning and litigation. A captive insurance company ("Captive") is an insurance company formed by a business owner to insure the risks of related or affiliated businesses. A Captive permits a business to manage its risks while potentially providing substantial benefits to that related business. The premiums received by the Captive are invested and thus not "lost" if not used to pay claims in the same sense that commercial insurance premiums are when paid to an unrelated insurer. This one benefit drives the use of Captives for the family business more than any other. Captives may issue property or casualty insurance coverage against a wide variety of possible liabilities. -

Effective with UNDERWRITERS at LLOYD's, LONDON Insurance For

Effective with UNDERWRITERS AT LLOYD'S, LONDON Administered by Hiscox Inc. 520 Madison Avenue 32nd Floor, New York, NY 10022 (646) 452-2353 Insurance for General Liability DECLARATIONS This insurance has been placed with an insurer that is not licensed by the state of Michigan. In case of insolvency, payment of claims may not be guaranteed. Broker No.: US 0001488 RT Specialty of Illinois, LLC Policy No.: MPL1934916.18 500 W. Monroe St., 30th Floor Renewal of: MPL1934916.17 Chicago, IL 60661 1. Named Insured: Stateside APM Address: 6445 Citation Dr Ste F Clarkston, MI 48346-2996 2. Policy Period: Inception Date: 03/31/2018 Expiration Date: 03/31/2019 Inception date shown shall be at 12:01 A.M. (Standard Time) to Expiration date shown above at 12:01 A.M. (Standard Time) at the address of the Named Insured. 3. General terms and WCL P0001 CW (09/14) conditions wording: The General terms and conditions apply to this policy in conjunction with the specific wording detailed in each section below. 4. Endorsements: E6015.6 - Lloyd’s Syndicate (3624) Endorsement, E6016.1 - Service of Suit, E6017.2 - Nuclear Incident Exclusion Clause-Liability-Direct (Broad) Endorsement, E6018.2 - Applicable Law Endorsement, E6020.2 - War and Civil War Exclusion Endorsement, E6023.1 - Minimum Earned Premium Endorsement, and E9998.2 - TRIA Not Purchased Endorsement 5. Optional Extension Extended Reporting Period of 12/24/36 months at 75/150/225 percent of the annual premium. Period: 6. Notification of Hiscox Claims claims to: 520 Madison Avenue, 32nd floor New York, NY 10022 Fax: 212-922-9652 Email: [email protected] 7. -

CDP Climate Change Report 2015 United Kingdom Edition

CDP Climate Change Report 2015 United Kingdom Edition Written on behalf of 822 investors with US$95 trillion in assets CDP Report | October 2015 1 Contents Foreword 3 Global overview 4 2015 Leadership criteria 8 The Climate A List 2015 10 2015 FTSE 350 Climate Disclosure Leadership Index (CDLI) 12 Investor engagement in the UK 13 Profile: BT Group 14 United Kingdom snapshot 16 Profile: SSE 18 Natural Capital 20 Appendix I 24 Investor signatories and members Appendix II 25 FTSE 350 scores Appendix III 30 Responding FTSE SmallCap climate change companies Please note: The selection of analyzed companies in this report is based on market capitalization of regional stock indices whose constituents change over time. Therefore the analyzed companies are not the same in 2010 and 2015 and any trends shown are indicative of the progress of the largest companies in that region as defined by market capitalization. Large emitters may be present in one year and not the other if they dropped out of or entered a stock index. ‘Like for like’ analysis on emissions for sub-set of companies that reported in both 2010 and 2015 is included for clarity. Some dual listed companies are present in more than one regional stock index. Companies referring to a parent company response, those responding after the deadline and self-selected voluntary responding companies are not included in the analysis. For more information about the companies requested to respond to CDP’s climate change program in 2015 please visit: https://www.cdp.net/Documents/disclosure/2015/Companies-requested-to-respond-CDP-climate-change.pdf Important Notice The contents of this report may be used by anyone providing acknowledgement is given to CDP Worldwide (CDP). -

Phoenix Unit Trust Managers Manager's Interim Report

130535_BothUKEqIncmIR_v6 14/01/2016 11:46 Page 1 PHOENIX UNIT TRUST MANAGERS MANAGER’S INTERIM REPORT For the half year: 16 May 2015 to 15 November 2015 PUTM BOTHWELL UK EQUITY INCOME FUND 130535_BothUKEqIncmIR_v6 14/01/2016 11:46 Page 2 130535_BothUKEqIncmIR_v6 14/01/2016 11:46 Page 3 Contents Investment review 2-3 Portfolio of investments 4-7 Top ten purchases and sales 8 Statistical information 9-11 Statements of total return & change in net assets attributable to unitholders 12 Balance sheet 13 Distribution table 14 Corporate information 15 1 130535_BothUKEqIncmIR_v6 14/01/2016 11:46 Page 4 Investment review Performance Review Over the review period, the UK Equity Income Fund returned -6.2%, which compares with a benchmark return of -9.6 %. (Source: Lipper, bid-to-bid, net income reinvested for six months to 15/11/2015.) Standardised Past Performance Nov 14-15 Nov 13-14 Nov 12-13 Nov 11-12 Nov 10-11 % growth % growth % growth % growth % growth PUTM Bothwell UK Equity Income (B) (Inc) 0.83 3.35 18.86 6.14 -8.37 Benchmark* -2.20 3.09 24.22 8.54 -2.10 *FTSE All Share ex IT. Source: Lipper, bid to bid to 15 November each year. Past Performance is not a guide to future performance. The value of units and the income from them can go down as well as up and is not guaranteed. You may not get back the full amount invested. Please note that all past performance figures are calculated without taking the initial charge into account. 2 130535_BothUKEqIncmIR_v6 14/01/2016 11:46 Page 5 Investment review Portfolio and Market Review Key transactions included the purchase of ARM Holdings In the first half of the review period, investor sentiment in in the technology sector.