Mastercard® Paypass™

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Is a High Refund Strategy Always Effective?

Is a High Refund Strategy Always Effective? Shueh-Chin Ting, Professor, Department of Education, National University of Tainan, Taiwan ABSTRACT Retailers often use a refund strategy to guarantee that their products are the lowest price. However, does a high refund strategy announced by retailers definitively help consumers to believe that their products have the lowest price? Hierarchical moderator regression analysis was used to examine the moderating effect of a retailer’s reputation on the relationship between refund size and the believability of the lowest price. The results indicate that refund size has no direct effect on the believability of the lowest price and the effect is moderated by a retailer’s reputation. For reputable retailers, refund size has a positive influence on the believability of the lowest price. For less reputable retailers, refund size has a negative influence on the believability of the lowest price. Prior studies neglected the importance of a retailer’s reputation in implementing refund strategies. This study has resolved this research gap. Keywords: believability of the lowest price, guarantee strategy, refund size, retailer’s reputation. INTRODUCTION Retailers often use low-price guarantees (LPGs) as a signal to attract consumers and increase sales. Consumers interpret LPGs as signals that a particular retailer is committed to low prices (Borges, and Babin, 2012). Price-matching guarantees (PMGs) are commonly used by retailers as promises to match the lowest price for an item that a customer can find elsewhere (Yuan and Krishna, 2011). Signaling theory has been used to understand the overall effect of a PMG on consumer perceptions (Borges, 2009). -

Visa's Annual Report

Annual Report 2017 Annual Report 2017 Mission Statement To connect the world through the most innovative, reliable and secure digital payment network that enables individuals, businesses and economies to thrive. Financial Highlights (GAAP) In millions (except for per share data) FY 2015 FY 2016 FY 2017 Operating revenues $13,880 $15,082 $18,358 Operating expenses $4,816 $7,199 $6,214 Operating income $9,064 $7, 883 $12,144 Net income $6,328 $5,991 $6,699 Stockholders' equity $29,842 $32,912 $32,760 Diluted class A common stock earnings per share $2.58 $2.48 $2.80 Financial Highlights (ADJUSTED)1 In millions (except for per share data) FY 2015 FY 2016 FY 2017 Operating revenues $13,880 $15,082 $18,358 Operating expenses $4,816 $5,060 $6,022 Operating income $9,064 $10,022 $12,336 Net income $6,438 $6,862 $8,335 Diluted class A common stock earnings per share $2.62 $2.84 $3.48 Operational Highlights² 12 months ended September 30 (except where noted) 2015 2016 2017 Total volume, including payments and cash volume³ $7.4 trillion $8.2 trillion $10.2 trillion Payments volume³ $4.9 trillion $5.8 trillion $7.3 trillion Transactions processed on Visa's networks 71.0 billion 83.2 billion 111.2 billion Cards⁴ 2.4 billion 2.5 billion 3.2 billion Stock Performance The accompanying graph and chart compares the cumulative total return on $350 Visa’s common stock with the cumulative total return on Standard & Poor’s 500 Index and the Standard & Poor’s 500 Data Processing Index from September 30, $300 2012 through September 30, 2016. -

1 Abundant Glory Limited British Virgin Islands Executive

Appendix B Present Directorships of Edith SHIH as at effective date of appointment Role Name of Company Place of Incorporation (Executive / Non-Executive) 1 Abundant Glory Limited British Virgin Islands Executive 2 Actionfirm Limited British Virgin Islands Executive 3 AICT Advisory Limited British Virgin Islands Executive Alexandria International Container Terminals 4 Egypt Executive Company S.A.E. 5 Alpha Metrics Limited British Virgin Islands Executive 6 Americas Intermodal Services SA/NV Belgium Executive 7 Americas Shipyard SA/NV Belgium Executive 8 Amsterdam Container Terminals B.V. Netherlands Executive 9 Amsterdam Marine Terminals B.V. Netherlands Executive 10 Amsterdam Port Holdings B.V. Netherlands Executive 11 Anovio Holdings Limited Cyprus Executive 12 APM Terminals Dachan Company Limited Hong Kong Executive 13 Aqaba Terminal Services Limited British Virgin Islands Executive 14 Asia Pacific Honour Holdings Limited British Virgin Islands Executive 15 Bajacorp, S.A. de C.V. Mexico Executive 16 Barcelona Europe South Terminal, S.A. Spain Executive 17 Best Fortune S.a r.l. Luxembourg Executive 18 Best Month Profits Limited British Virgin Islands Executive 19 Best Oasis Holdings Limited British Virgin Islands Executive 20 Best People Resources Limited British Virgin Islands Executive 21 Beyond Excel Investments Limited British Virgin Islands Executive 22 Brightease Profits Limited British Virgin Islands Executive 23 Brisbane Container Terminals Pty Limited Australia Executive Appendix B 24 Buenos Aires Container Terminal Services S.A. Argentina Alternate Director 25 Cape Fortune B.V. Netherlands Executive 26 Central America Shipyard SA/NV Belgium Executive 27 China Terminal Services Holding Company Limited Bermuda Executive 28 Clivedon Limited British Virgin Islands Executive 29 CLK Limited British Virgin Islands Executive 30 Coastal Work Logistics Limited British Virgin Islands Executive 31 Container Security Inc. -

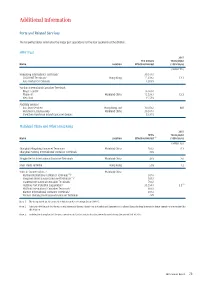

Additional Information

additional Information ports and related services The following tables summarise the major port operations for the four segments of the division. HpH trust 2015 The Group’s Throughput Name Location Effective Interest (100% basis) (million TEU) Hongkong International Terminals/ 30.07% / COSCO-HIT Terminals/ Hong Kong 15.03% / 12.1 Asia Container Terminals 12.03% Yantian International Container Terminals - Phase I and II/ 16.96% / Phase III/ Mainland China 15.53% / 12.2 West Port 15.53% Ancillary Services - Asia Port Services/ Hong Kong and 30.07% / N/A Hutchison Logistics (HK)/ Mainland China 30.07% / Shenzhen Hutchison Inland Container Depots 23.35% Mainland China and other Hong Kong 2015 HPH’s Throughput Name Location Effective Interest (1) (100% basis) (million TEU) Shanghai Mingdong Container Terminals/ Mainland China 50% / 8.3 Shanghai Pudong International Container Terminals 30% Ningbo Beilun International Container Terminals Mainland China 49% 2.0 River Trade Terminal Hong Kong 50% 1.2 Ports in Southern China - Mainland China (2) Nanhai International Container Terminals / 50% / (2) Jiangmen International Container Terminals / 50% / Shantou International Container Terminals/ 70% / (3) Huizhou Port Industrial Corporation/ 33.59% / 2.5 Huizhou International Container Terminals/ 80% / Xiamen International Container Terminals/ 49% / Xiamen Haicang International Container Terminals 49% Note 1: The Group holds an 80% interest in Hutchison Ports Holdings Group (“HPH”). Note 2: Although HPH Trust holds the economic interest in the two River Ports in Nanhai and Jiangmen in Southern China, the legal interests in these operations are retained by this division. Note 3: Includes the throughput of the port operations in Gaolan and Jiuzhou that were disposed during the second half of 2015. -

How We Will Calculate Your Balance:We Use a Method Called “Average Daily Balance (Including New Purchases)”. Index and When

232 - 121144 Platinum Edition® Visa® Card T-GULF-2005 Cards are issued by First Bankcard®, a division of First National Bank of Omaha, which is referred to below as “we”, “us”, “our”, and “First Bankcard”. PLEASE NOTE: If you apply for a credit card, you may receive a Platinum Edition® Visa® Card, a Visa Signature® Card, or we may decline to open an account for you. Eligibility for card products depends on the information provided in your application and your credit card history. The card you are approved for will determine your Visa benefits. IMPORTANT RATE, FEE AND OTHER COST INFORMATION (SUMMARY OF CREDIT TERMS) Interest Rates and Interest Charges Annual Percentage Rate (APR) for Purchases 26.99% when you open your account. This APR will vary with the market based on the Prime Rate. APR for Balance Transfers 26.99% This APR will vary with the market based on the Prime Rate. APR for Cash Advances 25.24%. This APR will vary with the market based on the Prime Rate. Penalty APR and When it Applies None How to Avoid Paying Interest on Your due date is at least 21 days after the close of each billing cycle. We will not charge you any interest on purchases if you pay your entire balance by the due date each month.1 Purchases Minimum Interest Charge If you are charged interest, the charge will be no less than $1.75. For Credit Card Tips from the To learn more about factors to consider when applying for or using a credit card, visit the website of the Consumer Financial Protection Bureau at Consumer Financial Protection Bureau www.consumerfinance.gov/learnmore. -

Global Payments 2020-30 a Quantium Shift in the Next Decade Australia's Challenge

McLean Roche Consulting Group Global Payments 2020-30 A quantium shift in the next decade Australia’s challenge – to keep up 1 Submission To RBA Payments Boards – Future of Payments – January 2020 McLean Roche Consulting Group AUSTRALIA’S PAYMENT CHALLENGE Australian payments will see more change in the next 10 years than the last 40 years combined. Australia has an expensive US/Anglo legacy based retail payments system which will be challenge by new technology, new data uses, new players and the need to protect consumer rights and data. Consumer retail payments total $975.7 billion in 2019 and will reach $3.2 trillion by 2030. A faster rate of expansion will occur in SME and Corporate payments. Payments are a very high volume, low margin business with even the smallest changes in revenues or margins delivering significant changes in actual dollars. Regulators around the globe will be challenged by forces of change and this requires all regulators and politicians to be aware of the scale of change and ensure the regulatory frame work changes and evolves quickly. 4 MYTHS DOMINATE THE NARRATIVE 1. CASH WILL DISAPPEAR – many including regulators keep predicting the death of cash. While bank notes may disappear, various forms of cash now dominate retail payments in Australia combining to total 71% share. 2. CREDIT CARDS DOMINATE LENDING – consumer credit cards are in decline having peaked 8 years ago. All the leading indicators are falling – average balance, average spend, revolve rate and number of cards. Corporate and Commercial cards are the only growth story. 3. DIGITAL PAYMENTS ARE THE FUTURE – many payment products use the ‘digital’ tag for marketing ‘glint’ however the reality is all payment products using Visa, MasterCard, Amex or eftpos payment networks are not digital. -

Chartered Secretaries American Express Credit Cards

Chartered Secretaries American Express Credit Cards Chartered Secretaries American Express® Platinum Credit Card and Chartered Secretaries American Express®Gold Credit Card are two co-branded cards that have been created in collaboration with The Hong Kong Institute of Chartered Secretaries (HKICS) and have been specifically designed to recognise and benefit our members. As a Member/Graduate/Student of HKICS, you are cordially invited to become a Chartered Secretaries American Express Platinum or Gold Card Cardmember. This card provides a highly convenient way to pay for HKICS membership fees, CPD events and seminars, examination fees and other fees. Application forms Exclusive privileges Merchants List Application forms Chartered Secretaries American Express Platinum Credit Card application form Chartered Secretaries American Express Gold Credit Card application form Application with required documents should be sent to: American Express International Inc Attn: New Accounts GPO Box 11250 Hong Kong Note: 1. Terms and conditions apply to the above offers and privileges. Please visit www.americanexpress.com.hk to learn more. 2. The Chartered Secretaries American Express co-branded Card is a privilege from HKICS. All Credit Card applicationapprovals will be at the sole discretion of American Express International Inc 3. For any enquiries, please call 2277 1370 Back to top Exclusive privileges: Chartered Secretaries American Express® Platinum Credit Card Half annualfee waiver saving you HK$800 a year Generous welcome offers including HK$500 Lane Crawford or Esso Synergy Fuel Cash Voucher, plus 10X Membership Rewards points in the first 3 months, up to 300,000 points Up to HK$500 travel package discount coupon when you purchasing travel packages from Farrington American Express Travel Services Ltd. -

Hong Kong Health and Beauty Retail Stores

Hong Kong Health and Beauty Retail Guide December 2014 Introduction With a wealthy population of 7 million and GDP of US$235 billion, Hong Kong is a large, high-value and expanding market for Australian consumer products, including beauty and health products. In 2013, A$132 million of Australian cosmetics and skin care were exported to Hong Kong. Australian cosmetic and skin care products have an international reputation as safe, environmentally friendly and consistently high quality. Australia is also recognised as a reliable source of quality cosmetics, skin care and health products, particularly in the natural and organic skincare categories. Hong Kong’s total sales in beauty and personal care products remained strong in 2013, reaching over HK$14.5 billion (over A$2 billion). Last year more than 50 million visitors, including some 40 million mainland Chinese, came to shop in Hong Kong, with cosmetics and skin care items a key focus. Hong Kong is a significant market in its own right and an excellent testing ground for international products entering the region. Austrade has launched a special video insights series to provide Australian beauty companies with first-hand perspectives from experts in the market. These videos provide advice on the latest market trends and tactics to be used in Hong Kong and China. Check it out from Austrade website. Table of Contents Page Number Overview of Hong Kong Distribution Channels - Beauty and Health Products 3 Hong Kong Health and Beauty Retail Stores Specialty Stores 4 Department Stores 5 Beauty Counters at Department Stores 6 Pharmacy Chains 8 Multi-brand Shops 8 Australian Concept Stores 9 Supermarkets 10 Austrade Contacts 12 November 2014 Austrade Health and Beauty Products Retail Stores in Hong Kong> 2 Overview of Hong Kong Distribution Channels - Beauty and Health Products Hong Kong has a sophisticated retail sector for the sale and distribution of health and beauty products. -

Bow Credit Card Agreement

CREDIT CARD AGREEMENT (Personal Accounts) By requesting or accepting any Standard MasterCard, account. If we accept a payment from you in excess of your Standard Visa, Platinum MasterCard, Platinum Visa, outstanding balance, your available Credit Limit will not be Platinum Rewards MasterCard, or Platinum Rewards Visa increased by the amount of the overpayment nor will we be account (individually or collectively called “Credit Card required to authorize transactions for an amount in excess account” or “Account”) with Bank of the West, you agree to of your Credit Limit. be bound by all the terms of this Agreement. In this 3. Temporary Reduction of Credit Limit. Merchants, Agreement, the words “you” or “your” mean everyone who such as car rental companies and hotels, may request prior has requested or accepted a Credit Card account with us. credit approval from us for an estimated amount of your The words “we,” “us,” “our,” or “Bank” mean Bank of the Purchases, even if you ultimately do not pay by credit. If our West. If you do not accept this Agreement, you must notify approval is granted, your available Credit Limit will us in writing within 5 days after receipt. Use of your card or temporarily be reduced by the amount authorized by us. If any feature (including a balance transfer) of your Credit you do not ultimately use your Credit Card account to pay Card Agreement shall constitute acceptance of this for your Purchases or if the actual amount of Purchases Agreement. posted to your Credit Card account varies from the 1. Use. Your Standard MasterCard, Standard Visa, estimated amount approved by us, it is the responsibility of Platinum MasterCard, Platinum Visa, Platinum Rewards the merchant, not us, to cancel the prior credit approval MasterCard, or Platinum Rewards Visa card (individually or based on the estimated amount. -

General Contracting Terms and Conditions

K&H Bank Zrt. H–1095 Budapest, Lechner Ödön fasor 9. phone: +(36 1) 328 9000 fax: +(36 1) 328 9696 www.kh.hu • [email protected] GENERAL CONTRACTING TERMS AND CONDITIONS FOR BANKCARD AND CREDIT CARD SERVICES Effective dates: December 13, 2017, January 13, 2018 and February 13, 2018 Date of announcement: December 13, 2017 These GCTC are amended pursuant to Sections XIX.1 and XIX.2 hereof with the scope and effective dates specified below. Amended provisions in Section X.6 – effective date: December 13, 2017 (the effective date is referenced in the footnotes as well) Amendments due to amended legal regulations on payment services, or required for more precise and accurate wording of these GTC – effective date: January 13, 2018 Amended provisions in Sections IX.2 and XV.8 – effective date: February 13, 2018 (provisions becoming effective as of February 13, 2018 are specified also in the footnotes. TABLE OF CONTENTS I. TERMS: ................................................................................................................................................... 4 II. BANKCARD AGREEMENT AND ISSUING BANKCARDS ................................................................. 14 DETAILS OF THE EXTERIOR OF THE BANKCARD ....................................................................................................... 14 EXPIRY OF A BANKCARD ....................................................................................................................................... 14 APPLYING FOR A BANKCARD, CONTRACTING ........................................................................................................ -

Presentation to Australian Smart Cards Summit 2007: Review of Payments System Reforms

Review of Payments System Reforms Michele Bullock Head of Payments Policy Reserve Bank of Australia Overview 1. Scope of the review 2. What issues are being addressed? 3. Developments since the reforms? 4. Progress on the studies 5. Where to from here? Scope Credit cards EFTPOS Scheme debit American Express/Diners Club BPAY ATMs The Issues Source: The Australian What are the Issues? Effects of the reforms? Alternatives to regulation? Changes to current regulations? Developments In the market? Overseas? Analysis? Non-cash Payments per Capita* Per year No No 60 60 Cheques Credit cards 50 50 Debit cards 40 40 Direct credits 30 30 20 20 Direct debits 10 10 BPAY 0 0 1994 19961998 2000 2002 2004 2006 *Debit and credit card data prior to 2002 have been adjusted for a break in the series due to an expansion in the coverage of the Retail Payments Statistics in 2002. Sources: ABS; APCA; BPAY; RBA Number of Card Payments Year-on-year growth %% 30 30 Credit 20 20 Debit 10 10 0 0 1997 1999 2001 2003 2005 2007 Source: RBA Market Shares of Card Schemes By value of purchases % Bankcard, MasterCard and Visa % 90 90 85 85 % American Express and Diners Club % 15 15 10 10 5 5 2002 2003 2004 2005 2006 2007 Source: RBA Merchants Surcharging Credit Cards* Per cent of surveyed merchants %% 12 12 Very large merchants Large merchants 8 8 Small merchants 4 4 Very small merchants 0 0 Jun 2005 Dec 2005 Jun 2006 Dec 2006 * Very large merchants are those with turnover greater than $340 million, large merchants $20 million to $340 million, small merchants $5 million to $20 million and very small merchants $1 million to $5 million. -

![GC Cabbie Nov 9 for PDF[1]](https://docslib.b-cdn.net/cover/0253/gc-cabbie-nov-9-for-pdf-1-1200253.webp)

GC Cabbie Nov 9 for PDF[1]

I S S U E MONTHLY 9 N O V E M B E R 2 0 0 9 GC Cabbie this issue From the CEO CEO News P.1 Operational News P.2 Once again the Gold Coast has shown it’s resiliency in the face of global pressures; the media has essentially reported that we are now in the Marketing / Ombudsman Survey P.3 middle of a boom, the restaurants are busy, there are people out and Accounts P.4 about and the public are travelling again. Our figures have shown the same trend: bookings have increased over the last three months and Technical Services P .5 our hope is that the trend continues. Our Contact Centre Staff have Human Resources / Dreamworld Rank P.6 been under pressure as the calls have increased faster than antici- pated, thus, we have hired additional staff to assist with the Christmas Customer Feedback P.7 period. I would like to congratulate all of the Customer Service Reps Customer Feedback P.8 and Radio Operators for their efforts. Following on from a disappointing SuperGP we are heading into our traditionally busy period. Everyone within the Gold Coast Cabs group needs to ensure that we continue to provide exceptional customer service even when it is busy: • Smile • Be courteous • Be helpful (put the luggage / shopping into the car, open the door for the passenger etc) • Take pride in your work, car and appearance • Drive safely • Offer to change the radio station or to turn it off • Ask if they are comfortable, adjust / turn on the air-conditioning • Don’t speak on your mobile phone (even hands free) with passengers in the car • Be positive Do every job: every customer is to be treated equally, regardless of whether they are travelling around the cor- ner or going further.