The Competitive Strategy of an Ethnic Chinese Corporate Group Under the Hong Kong Economic Development, with Special Emphasis on the Cheung Kong Group

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Case No COMP/M.2951 - A.S

EN Case No COMP/M.2951 - A.S. WATSON / KRUIDVAT Only the English text is available and authentic. REGULATION (EEC) No 4064/89 MERGER PROCEDURE Article 6(1)(b) NON-OPPOSITION Date: 27/09/2002 Also available in the CELEX database Document No 302M2951 Office for Official Publications of the European Communities L-2985 Luxembourg COMMISSION OF THE EUROPEAN COMMUNITIES Brussels, 27.09.2002 SG (2002) D/231850 In the published version of this decision, some PUBLIC VERSION information has been omitted pursuant to Article 17(2) of Council Regulation (EEC) No 4064/89 concerning non-disclosure of business secrets and other confidential information. The omissions are MERGER PROCEDURE shown thus […]. Where possible the information ARTICLE 6(1)(b) DECISION omitted has been replaced by ranges of figures or a general description. To the notifying party Dear Sir/Madam, Subject: Case No COMP/M.2951 - A.S. Watson/Kruidvat Notification of 29.08.2002 pursuant to Article 4 of Council Regulation No 4064/891 1. On 29 August 2002, the Commission received a notification of a proposed concentration whereby A.S. Watson & Co., Limited (“A.S. Watson”), which belongs to the Hong Kong based group Hutchison Whampoa Limited (“Hutchison”), intends to acquire within the meaning of Article 3(1)(b) of the Council Regulation (EEC) No 4064/89 (“the Merger Regulation”) control over Dutch companies Kruidvat Holding B.V., and Kruidvat Superdrug B.V. (hereinafter ”Kruidvat”). The companies are presently controlled by Kruidvat Beheer B.V. (”Kruidvat Beheer”). 2. After examination of the notification, the Commission has concluded that the notified operation falls within the scope of the Merger Regulation and does not raise serious doubts as to its compatibility with the common market and the functioning of the EEA Agreement. -

Is a High Refund Strategy Always Effective?

Is a High Refund Strategy Always Effective? Shueh-Chin Ting, Professor, Department of Education, National University of Tainan, Taiwan ABSTRACT Retailers often use a refund strategy to guarantee that their products are the lowest price. However, does a high refund strategy announced by retailers definitively help consumers to believe that their products have the lowest price? Hierarchical moderator regression analysis was used to examine the moderating effect of a retailer’s reputation on the relationship between refund size and the believability of the lowest price. The results indicate that refund size has no direct effect on the believability of the lowest price and the effect is moderated by a retailer’s reputation. For reputable retailers, refund size has a positive influence on the believability of the lowest price. For less reputable retailers, refund size has a negative influence on the believability of the lowest price. Prior studies neglected the importance of a retailer’s reputation in implementing refund strategies. This study has resolved this research gap. Keywords: believability of the lowest price, guarantee strategy, refund size, retailer’s reputation. INTRODUCTION Retailers often use low-price guarantees (LPGs) as a signal to attract consumers and increase sales. Consumers interpret LPGs as signals that a particular retailer is committed to low prices (Borges, and Babin, 2012). Price-matching guarantees (PMGs) are commonly used by retailers as promises to match the lowest price for an item that a customer can find elsewhere (Yuan and Krishna, 2011). Signaling theory has been used to understand the overall effect of a PMG on consumer perceptions (Borges, 2009). -

CK HUTCHISON HOLDINGS LIMITED (“CK Hutchison”) And

HUTCHISON WHAMPOA INTERNATIONAL (03/33) LIMITED (the “Issuer”) US$1,500,000,000 7.45% Guaranteed Notes due 2033 (the “Notes”) (ISIN: US44841SAC35/CUSIP: 44841SAC3/Common Code: 018124572 for Rule 144A Notes) (ISIN: USG4672CAC94/CUSIP: G4672CAC9/Common Code: 018124629 for Regulation S Notes) unconditionally and irrevocably guaranteed by CK HUTCHISON HOLDINGS LIMITED (“CK Hutchison”) and HUTCHISON WHAMPOA LIMITED In accordance with Regulation (EU) No. 596/2014 on market abuse and the law of 11 January 2008 on transparency requirements, as amended, the Issuer is filing with the Commission de Surveillance du Secteur Financier, storing with the Officially Appointed Mechanism and publishing the attached unaudited results for the six months ended 30 June 2019 of CK Hutchison, a guarantor of the Notes issued by the Issuer. The attached document was also published by CK Hutchison at 4:31 pm and 4:32 pm (Hong Kong time), 1 August 2019 on the websites of Hong Kong Exchanges and Clearing Limited and CK Hutchison, respectively. Hutchison Whampoa International (03/33) Limited Edith Shih Director and Company Secretary 1 August 2019 Hong Kong Exchanges and Clearing Limited and The Stock Exchange of Hong Kong Limited take no responsibility for the contents of this document, make no representation as to its accuracy or completeness and expressly disclaim any liability whatsoever for any loss howsoever arising from or in reliance upon the whole or any part of the contents of this document. UNAUDITED RESULTS FOR THE SIX MONTHS ENDED 30 JUNE 2019 HIGHLIGHTS -

THE INTELLIGENT ADVANTAGE Harnessing the Power of IT to Stay Ahead of the Game

THE INTERNATIONAL JOURNAL OF THE HUTCHISON WHAMPOA GROUP SPHERE 11 TTHEHE IINTELLIGENTNTELLIGENT AADVDVANTAGEANTAGE SPHERE CONTENTS Number 11 April 2004 2 14 UPDATES TELECOMS NEWSBITES 3 CHEERS Latest developments from the Hong Kong enters the new era Hutchison press box. of video mobile communications. 20 COVER STORY THE INTELLIGENT ADVANTAGE Harnessing the power of IT to stay ahead of the game. 9 COMMUNITY COMMUNAL BONDS HPH makes every effort to contribute to the well-being of the communities in which it operates. 28 HOSPITALITY CAPITAL COMFORT Beijing’s newest luxury hotel offers the best of both worlds for discerning travellers. Cover: Illustration by Eamonn O'Boyle PUBLISHED BY Hutchison Whampoa Limited, 22/F Hutchison House, 10 Harcourt Road, Central, Hong Kong.Website: hutchison- whampoa.com. In-house Editorial Team: Laura Cheung, Nora Yong, Jeremy Lau, Pamela Wan, Wendy Luk. Editor: Mark Caldwell – Great Pacific Marketing Services Ltd. Design and production: Fiona Wat,Alvin Fong,Tanny Shek, Kelly Cheung – , a division of the Asia City Publishing Group.Tel:2850 5500. Fax 2543 1220. Colour Separation and Printing by bigboXX.com Limited. No part of this magazine may be reproduced without the written permission of Hutchison Whampoa Limited.All rights reserved. Copyright © 2003 by Hutchison Whampoa Limited.Opinions expressed herein are those of the writers and do not necessarily reflect the opinion of Hutchison Whampoa Limited.All currency conversions are approximations. HUTCHISON UPDATES News CORPORATE HWL Annual Results Performance -

2015 Annual Report

Ports and Related Services Retail Infrastructure Energy Telecommunications 2015 Annual Report 22nd Floor, Hutchison House, 10 Harcourt Hutchison House, Hong Kong Road, 22nd Floor, Telephone: +852 2128 1188 Facsimile: www.ckh.com.hk +852 2128 1705 Corporate Information CK Hutchison Holdings Limited Board of dIreCtors eXeCUtIVe dIreCtors NoN-eXeCUtIVe dIreCtors Chairman CHOW Kun Chee, Roland, LLM LI Ka-shing, GBM, KBE, LLD (Hon), DSSc (Hon) LEE Yeh Kwong, Charles, GBM, GBS, OBE, JP Commandeur de la Légion d’Honneur Grand Officer of the Order Vasco Nunez de Balboa LEUNG Siu Hon, BA (Law) (Hons), Hon LL.D. Commandeur de l’Ordre de Léopold George Colin MAGNUS, OBE, BBS, MA Group Co-Managing director and INdepeNdeNt NoN-eXeCUtIVe dIreCtors Deputy Chairman KWOK Tun-li, Stanley, BSc (Arch), AA Dipl, LLD (Hon), ARIBA, MRAIC LI Tzar Kuoi, Victor, BSc, MSc, LLD (Hon) CHENG Hoi Chuen, Vincent, GBS, OBE, JP Group Co-Managing director The Hon Sir Michael David KADOORIE, GBS, LLD (Hon), DSc (Hon) FOK Kin Ning, Canning, BA, DFM, FCA (ANZ) Commandeur de la Légion d’Honneur Commandeur de l’Ordre des Arts et des Lettres Commandeur de l’Ordre de la Couronne CHOW WOO Mo Fong, Susan, BSc Commandeur de l’Ordre de Leopold II Group Deputy Managing Director LEE Wai Mun, Rose, JP, BBA Frank John SIXT, MA, LLL Group Finance Director and Deputy Managing Director William Elkin MOCATTA, FCA Alternate to Michael David Kadoorie IP Tak Chuen, Edmond, BA, MSc Deputy Managing Director William SHURNIAK, SOM, LLD (Hon) KAM Hing Lam, BSc, MBA WONG Chung Hin, CBE, JP Deputy -

Board and Senior Management (PDF)

BOARD AND SENIOR MANAGEMENT Executive Committee Front (from left to right) Andrew Hunter, H L Kam, Victor Li, Edmond Ip Back (from left to right) Joanna Chen, Pak Lam Lun, Lambert Leung, Dominic Chan, Ivan Chan, Victor Luk, Wendy Tong Barnes DIRECTORS’ BIOGRAPHICAL INFORMATION LI Tzar Kuoi, Victor aged 45, has been the Chairman of the Company since its incorporation in May 1996. He is the Chairman of the Remuneration Committee of the Company since March 2005. He is also the Managing Director and Deputy Chairman of Cheung Kong (Holdings) Limited, Deputy Chairman of Hutchison Whampoa Limited, the Chairman of CK Life Sciences Int’l., (Holdings) Inc., an Executive Director of Hongkong Electric Holdings Limited, Co-Chairman of Husky Energy Inc. and a Director of The Hongkong and Shanghai Banking Corporation Limited (“HSBC”). Except for HSBC, all the companies mentioned above are listed companies. Mr. Victor Li serves as a member of the Standing Committee of the 11th National Committee of the Chinese People’s Political Consultative Conference of the People’s Republic of China. He is also a member of the Commission on Strategic Development, the Greater Pearl River Delta Business Council and the Council for Sustainable Development of the Hong Kong Special Administrative Region, and Vice Chairman of the Hong Kong General Chamber of Commerce. Mr. Victor Li is also the Honorary Consul of Barbados in Hong Kong. He is a director of certain substantial shareholders of the Company within the meaning of Part XV of the Securities and Futures Ordinance (“SFO”). He also holds directorships in certain companies controlled by certain substantial shareholders of the Company. -

75 Watson Cover

th Anniversary Quarter 2 • 2008 A.S. Watson quarterly75 family magazine "PARIS", the backbone of ICI PARIS XL's philosophy Marionnaud to change Hong Kong beauty retail Shining stars at Drogas Student fever Light the Passion & Share the Dream Relief forces mobilise Wats Our Aroundthe world Focusstory Home Ourcommunity Hutchstory tents With a history dating back to 1828, the A.S. Watson Group (ASW) has evolved into an international retail and manufacturing businessn with operations in 36 Co Record year of profit for "PARIS" the backbone of Light the Passion & Share Relief forces Li Ka Shing Center for markets worldwide. Today, the Group owns more than 8,000 retail stores ASW...... ICI PARIS XL's philosophy ...... the Dream...... mobilise...... Learning & Knowledge...... running the gamut from health & beauty chains, luxury perfumeries & cosmetics to food, electronics, fine wine and airport retail arms. An established player 19 33 in the beverage industry, ASW provides a full range of beverages from bottled water, fruit juices, soft drinks and tea products to the world's finest wine labels 28 40 via its international wine wholesaler and distributor. 05 ASW employs over 80,000 staff and is a member of the world renowned Hong Kong-based conglomerate Hutchison Whampoa Limited, which has five core businesses - ports and related services; property and hotels; retail; energy, About A.S. Watson Group About A.S. Watson infrastructure, investments and others; and telecommunications in 57 countries. Editorial committee Published by • Adviser : Dominic Lai • Members : A.S. Watson & Co., Limited Wats On is the quarterly family magazine of the A.S. -

Annual Report 2006 Annual Report2006

(incorporated in the Cayman Islands with limited liability) (Stock Code: 8222) Better Health Better Life Annual Report 2006 Annual Report2006 2 Dai Fu Street, Tai Po Industrial Estate, Hong Kong Tel: (852) 2126 1212 Fax: (852) 2126 1211 www.ck-lifesciences.com Characteristics of the Growth Enterprise Market (”GEM”) of The Stock Exchange of Hong Kong Limited (the “Stock Exchange”) GEM has been established as a market designed to accommodate companies to which a high investment risk may be attached. In particular, companies may list on GEM with neither a track record of profi tability nor any obligation to forecast future profi tability. Furthermore, there may be risks arising out of the emerging nature of companies listed on GEM and the business sectors or countries in which the companies operate. Prospective investors should be aware of the potential risks of investing in such companies and should make the This annual report (“Annual Report”) is available in both decision to invest only after due and careful consideration. English and Chinese. Shareholders who have received either The greater risk profi le and other characteristics of GEM the English or the Chinese version of the Annual Report mean that it is a market more suited to professional and other may request a copy in the language different from that has sophisticated investors. been received by writing to: Computershare Hong Kong Investor Services Limited, 46th Floor, Hopewell Centre, 183 Given the emerging nature of companies listed on GEM, there Queen’s Road East, Hong Kong. is a risk that securities traded on GEM may be more susceptible to high market volatility than securities traded on the Main The Annual Report (in both English and Chinese versions) Board and no assurance is given that there will be a liquid has been posted on the Company’s website at market in the securities traded on GEM. -

CK Hutchison Highlights of the Unaudited Results for the Six Months Ended 30 June 2015

Hong Kong Exchanges and Clearing Limited and The Stock Exchange of Hong Kong Limited take no responsibility for the contents of this document, make no representation as to its accuracy or completeness and expressly disclaim any liability whatsoever for any loss howsoever arising from or in reliance upon the whole or any part of the contents of this document. Highlights of the Unaudited Results for the six months ended 30 June 2015 CKHH six months statutory results (1) For the six months ended 30 June 2015 HK$ millions Total Revenue 117,250 Profit attributable to ordinary shareholders from continuing business 21,477 Profit attributable to ordinary shareholders from discontinued business 80,381 Profit attributable to ordinary shareholders 101,858 Earnings per share – statutory (2) HK$39.87 CKHH six months management pro forma results (3) (compared to HWL results for businesses continued by CKHH) CKHH Results HWL Results for the six for the six months ended months ended 30 June 2015 30 June 2014 HK$ millions HK$ millions Change Total Revenue (4) 197,019 196,671 - Total EBITDA (4) 46,165 42,587 +8% Total EBIT (4) 30,677 26,815 +14% Profit attributable to ordinary shareholders before profits on disposal of investments & others (5) 14,938 10,220 +46% Profits on disposal of investments & others (482) 14,921 -103% Total profit attributable to ordinary shareholders (6) 14,456 25,141 -43% Recurring earnings per share – pro forma (7) HK$3.87 For the six months ended 30 June 2015 Interim dividend per share HK$0.70 CKHH 2015 Interim Results Page 1 of 98 Note (1) Statutory results of CK Hutchison Holdings Limited (“CKHH” or the “Group”) for the six months ended 30 June 2015 include the one-time effects of the Reorganisation that occurred on 3 June 2015. -

1 Abundant Glory Limited British Virgin Islands Executive

Appendix B Present Directorships of Edith SHIH as at effective date of appointment Role Name of Company Place of Incorporation (Executive / Non-Executive) 1 Abundant Glory Limited British Virgin Islands Executive 2 Actionfirm Limited British Virgin Islands Executive 3 AICT Advisory Limited British Virgin Islands Executive Alexandria International Container Terminals 4 Egypt Executive Company S.A.E. 5 Alpha Metrics Limited British Virgin Islands Executive 6 Americas Intermodal Services SA/NV Belgium Executive 7 Americas Shipyard SA/NV Belgium Executive 8 Amsterdam Container Terminals B.V. Netherlands Executive 9 Amsterdam Marine Terminals B.V. Netherlands Executive 10 Amsterdam Port Holdings B.V. Netherlands Executive 11 Anovio Holdings Limited Cyprus Executive 12 APM Terminals Dachan Company Limited Hong Kong Executive 13 Aqaba Terminal Services Limited British Virgin Islands Executive 14 Asia Pacific Honour Holdings Limited British Virgin Islands Executive 15 Bajacorp, S.A. de C.V. Mexico Executive 16 Barcelona Europe South Terminal, S.A. Spain Executive 17 Best Fortune S.a r.l. Luxembourg Executive 18 Best Month Profits Limited British Virgin Islands Executive 19 Best Oasis Holdings Limited British Virgin Islands Executive 20 Best People Resources Limited British Virgin Islands Executive 21 Beyond Excel Investments Limited British Virgin Islands Executive 22 Brightease Profits Limited British Virgin Islands Executive 23 Brisbane Container Terminals Pty Limited Australia Executive Appendix B 24 Buenos Aires Container Terminal Services S.A. Argentina Alternate Director 25 Cape Fortune B.V. Netherlands Executive 26 Central America Shipyard SA/NV Belgium Executive 27 China Terminal Services Holding Company Limited Bermuda Executive 28 Clivedon Limited British Virgin Islands Executive 29 CLK Limited British Virgin Islands Executive 30 Coastal Work Logistics Limited British Virgin Islands Executive 31 Container Security Inc. -

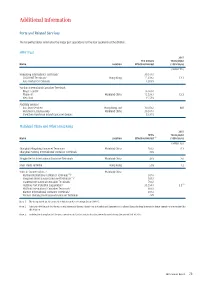

Additional Information

additional Information ports and related services The following tables summarise the major port operations for the four segments of the division. HpH trust 2015 The Group’s Throughput Name Location Effective Interest (100% basis) (million TEU) Hongkong International Terminals/ 30.07% / COSCO-HIT Terminals/ Hong Kong 15.03% / 12.1 Asia Container Terminals 12.03% Yantian International Container Terminals - Phase I and II/ 16.96% / Phase III/ Mainland China 15.53% / 12.2 West Port 15.53% Ancillary Services - Asia Port Services/ Hong Kong and 30.07% / N/A Hutchison Logistics (HK)/ Mainland China 30.07% / Shenzhen Hutchison Inland Container Depots 23.35% Mainland China and other Hong Kong 2015 HPH’s Throughput Name Location Effective Interest (1) (100% basis) (million TEU) Shanghai Mingdong Container Terminals/ Mainland China 50% / 8.3 Shanghai Pudong International Container Terminals 30% Ningbo Beilun International Container Terminals Mainland China 49% 2.0 River Trade Terminal Hong Kong 50% 1.2 Ports in Southern China - Mainland China (2) Nanhai International Container Terminals / 50% / (2) Jiangmen International Container Terminals / 50% / Shantou International Container Terminals/ 70% / (3) Huizhou Port Industrial Corporation/ 33.59% / 2.5 Huizhou International Container Terminals/ 80% / Xiamen International Container Terminals/ 49% / Xiamen Haicang International Container Terminals 49% Note 1: The Group holds an 80% interest in Hutchison Ports Holdings Group (“HPH”). Note 2: Although HPH Trust holds the economic interest in the two River Ports in Nanhai and Jiangmen in Southern China, the legal interests in these operations are retained by this division. Note 3: Includes the throughput of the port operations in Gaolan and Jiuzhou that were disposed during the second half of 2015. -

CK Hutchison Holding(1

Equity Market Hong Kong Equity Morning note Martin Ma (SFC CE:BOB758) (852) 3519 1055 Friday, September 25,2020 Market Wrap HSI▼1.82% HSCEI▼1.96% Turnover HK$117.16 bn ▼9% (30-day average) SSE Composite▼1.72% SZSE Component ▼2.24% Sector tracking Stock tracking 1D ▲% 1Y ▲% 1D ▲% 1Q ▲% Utilities 0.5 Automobiles 88.6 SOLARGIGA ENERGY(757) 38.0 NEXION TECHNOLOG(8420) 339.6 Real Estate 1.0 Durable & Tech 54.9 GOLDWAY EDUCATIO(8160) 21.4 HAINAN MEILAN IN(357) 286.2 GOLDWAY EDUCATIO HAINAN MEILAN IN Consumer Goods Health Care IN TECHNICAL PRO(8446) 1.4 49.8 CORNERSTONE FINA(8112) 20.0 227.1 CORNERSTONE FINA IN TECHNICAL PRO Capital Goods 1.4 Consumer Goods 29.2 CHINA ALUMINUM C(6898) 19.5 KNK HOLDINGS LTD(8039) 222.8 Telecom Services 1.6 Materials 25.6 ROYALCHINA CENTURY ALUMINUM RE(8125) C 18.2 YTOKNK EXPRESS HOLDINGS HOLD LTD(6123) 220.9 MarketROYAL CENTURY Highlight RE YTO EXPRESS HOLD Hong Kong Utilities Series 4 – CKGOLDWAY Hutchison EDUCATIO Holding(1 HK): CORNERSTONE FINA CK Hutchison Holding Limited is a CHINA ALUMINUM C Hutchison Telecommunications HK Holding multinational conglomerate that ROYAL CENTURY RE (0215 HK) operate variety sector of business in around 50 countries and have over CK Infrastructure Holding 300,000 employees around the world. (01038 HK) The business involve including Ports and related services, retail, infrastructure, Energy and Li Ka-shing Telecommunications. CK Hutchison Holding For the year 20201H, Hutchison Group (0001 HK) reported HK$ 189,942 million revenue, with YoY changes of -12%, HK$28,619 of total EBIT, with YoY changes of -21%.